All the numbers you need to make sense of the world’s evolving digital behaviours.

The first three months of 2023 have seen some particularly interesting developments in the world’s connected behaviours.

As ever, our new Digital 2023 April Global Statshot Report – published in partnership with Meltwater and We Are Social – brings you all the latest data and analysis you need to make sense of these changes, and understand how they might affect you and your work.

And in addition to all of our usual datasets, we’ve also included a special study on the use of connected tech in the workplace, which will be of particular interest to B2B marketers, HR teams, and internal comms managers.

Top stories in April 2023

Some of the trends to watch out for in this latest Statshot report include:

A new milestone for internet adoption in India;

Further declines in the time that the world spends online;

Insights into how businesses are using social media for marketing;

Intriguing trends in social media ad spend;

Some juicy new numbers for Snapchat;

Accelerating internet connection speeds; and

The social media platforms driving the greatest share of web traffic referrals

That’s just a brief taster of the insights you’ll find in the full report though, which is packed with 300+ slides exploring what people are really doing on the internet, social media, mobile devices, and online shopping platforms.

The definitive source of digital data

In addition to thanking We Are Social and Meltwater for making these reports possible, I’d also like to offer my heartfelt thanks our wonderful data partners, without whom the Global Digital Reports series would be a lot less informative:

Before we begin this quarter’s analysis, please note that there have been widespread and significant changes to the source data that we include in the Global Digital Reports series over recent weeks:

We’ve changed the way that we label our headline metric for global social media use to “social media user identities”, to make it clearer that this figure may not represent unique individuals.

GWI has modified its survey methodology to facilitate more consistent comparison across cultures. These changes ensure that GWI’s data is even more robust than ever, but the updates have also resulted in meaningful adjustments to the figures in many of our regular datasets. As a result, please beware of comparing figures included in this quarter’s report with data published in previous reports in this series.

We’ve also seen incongruous trends in the data published in the ad tools of various social media platforms over recent weeks. We’ll explore some of these changes in detail below, but please note that these changes also affect our overall figures for social media user identities, which use these ad reach figures as a key input.

Due to increasing incongruities in source data, we’ve changed the sources that we use to inform and calculate key metrics for Indonesia. As a result, the figures that appear in our latest update may appear lower than those that appear in our previously published reports. However, these changes reflect revisions in data, and do not represent a drop in actual use of connected tech in the country.

For further details, please refer to our comprehensive guide to changes in data sources, research methodologies, and reporting approaches.

Top 10 takeaways

If you need quick insights, I’d recommend starting with the video below, which will help you understand all of this quarter’s top headlines and trends in just 10 minutes.

But once you’ve finished watching that, read on below for the full report.

The complete Digital 2023 April Global Statshot Report

You’ll find this quarter’s complete report in the embed below (click here if that’s not working for you), but continue reading past that to find our in-depth analysis of what all these numbers might mean for you and your work.

OK, ready to go deeper?

Essential digital stats for April 2023

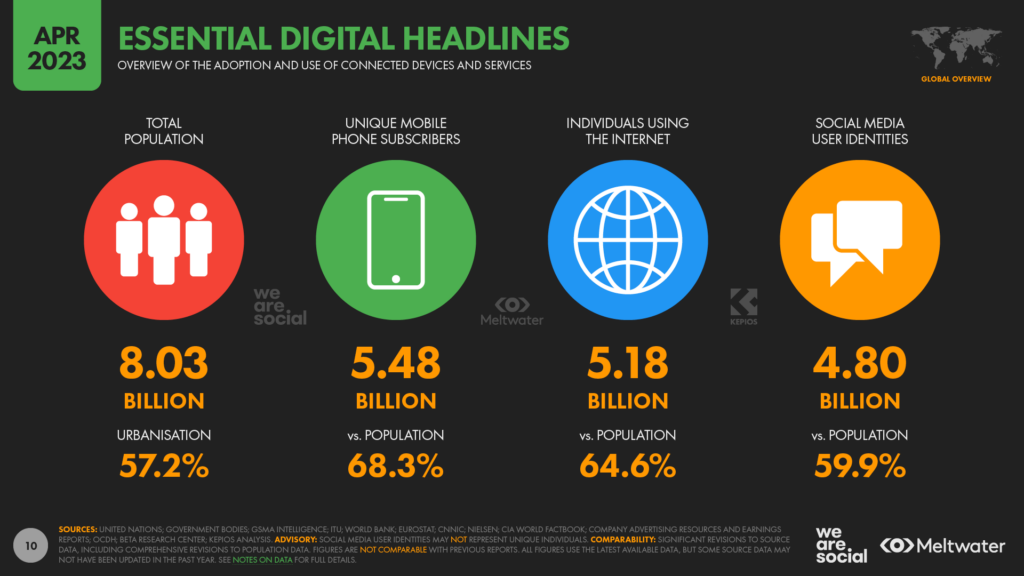

As always, let’s begin with the latest essential headlines for the adoption and use of digital around the world.

For context, the world’s population had reached 8.03 billion at the start of April 2023. That figure was just under 1 percent higher than the figure for the same time last year, with the world’s population growing by 69 million over the past 12 months.

GSMA Intelligence reports that there are now 5.48 billion unique mobile subscribers around the world, equating to 68.3 percent of the world’s total population. That total grew by almost 3 percent over the past year, thanks to the addition of 152 million new subscribers. For added perspective, Ericsson reports that there are now roughly 6.9 billion smartphones in use around the world, and these devices account for more than 5 in every 6 mobile handsets in use today.

The latest data indicate that there are now more than 5.18 billion individuals using the internet, equating to 64.6 percent of the world’s population. Kepios analysis reveals that 147 million people started to use the internet in the 12 months to April 2023, but delays in the reporting of internet research mean that growth may be meaningfully higher than this figure suggests.

The worldwide number of active social media “user identities” reached 4.80 billion in April 2023. This figure may not represent unique individuals, because the data we use to inform this total inevitably includes a certain degree of duplication and “false” accounts. However, for ease of comparison, that total is now tantalisingly close to 60 percent of the world’s population. Social media use continues to grow too, with 150 million new user identities over the past year delivering annual growth of 3.2 percent.

That’s a great overview of the current “state of digital”, but the real insights come when we start to explore the underlying trends.

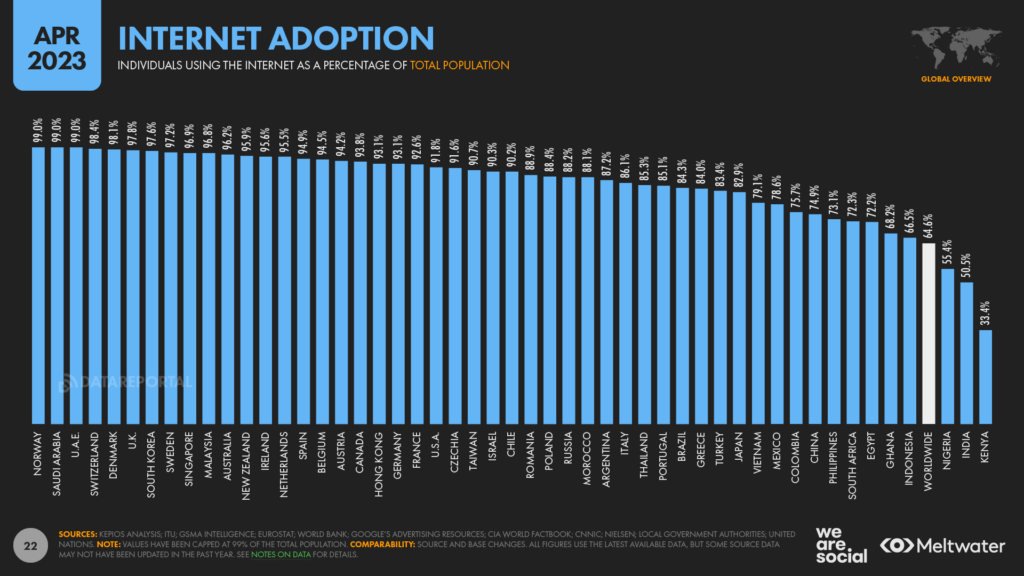

India passes 50% internet penetration

The latest data reveal that more than half of India’s population now uses the internet.A recent report from Nielsen indicates that the number of internet users in the country reached 720 million at the end of 2022, equating to 50.5 percent of the country’s total inhabitants.

Interestingly, Nielsen’s report highlights that India’s rural areas are now home to 44 percent more internet users than its urban areas, and that rural areas are also responsible for most of the country’s internet user growth.

The latest figures point to 425 million internet users in rural areas, with that figure increasing at an annual rate of roughly 30 percent.

Meanwhile, India’s urban areas are home to 295 million users, with that figure currently growing by roughly 10 percent per year.

For added clarity, India’s government defines rural areas as locations with fewer than 5,000 inhabitants and fewer than 400 people per square kilometre, where more than 25 percent of the male population is engaged in agricultural pursuits.

Encouragingly, the report also reveals that India’s female internet user population is growing at a rate of 27 percent per year.

However, data from the ITU and GSMA Intelligence indicates that India’s male internet users continue to outnumber their female peers by a significant margin, and there’s still a long way to go before India closes its digital divide.

For added context, our analysis of the latest data suggests that women may account for as little as 30 percent of India’s social media users, even in April 2023.

Moreover, despite encouraging growth in internet users, India is still home to the world’s largest “unconnected” population, and more than 700 million people in the country are still waiting to come online at the time of writing.

Similarly, while India will soon become home to the world’s largest overall population, the country still has a long way to go before it can claim the world’s largest connected population.

China still has a firm grip on that title, with data in CNNIC’s latest report putting internet user numbers in the country at 1.07 billion.

More than 350 million people in China remain “unconnected” too, so the country still has plenty of potential for continued digital growth.

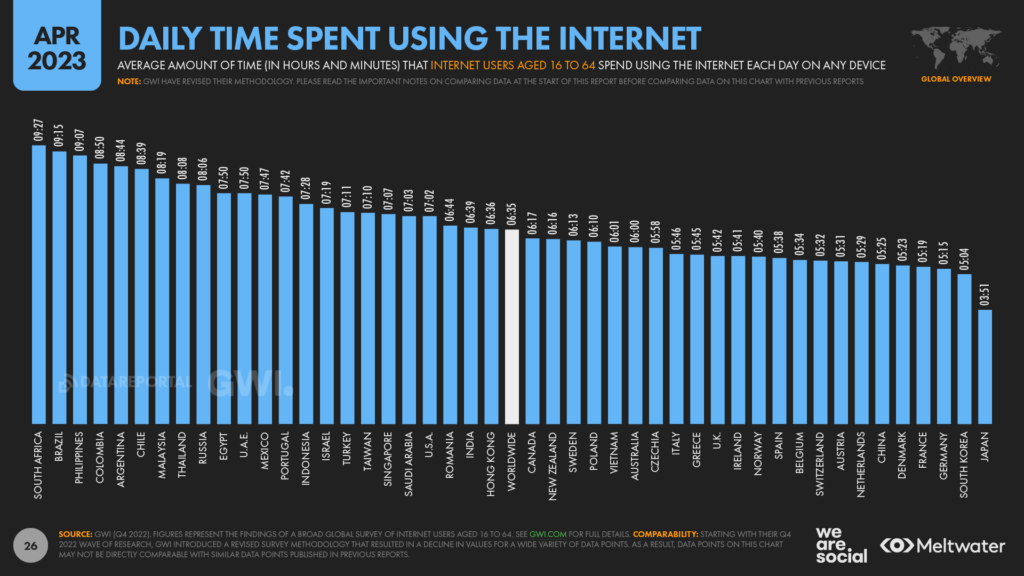

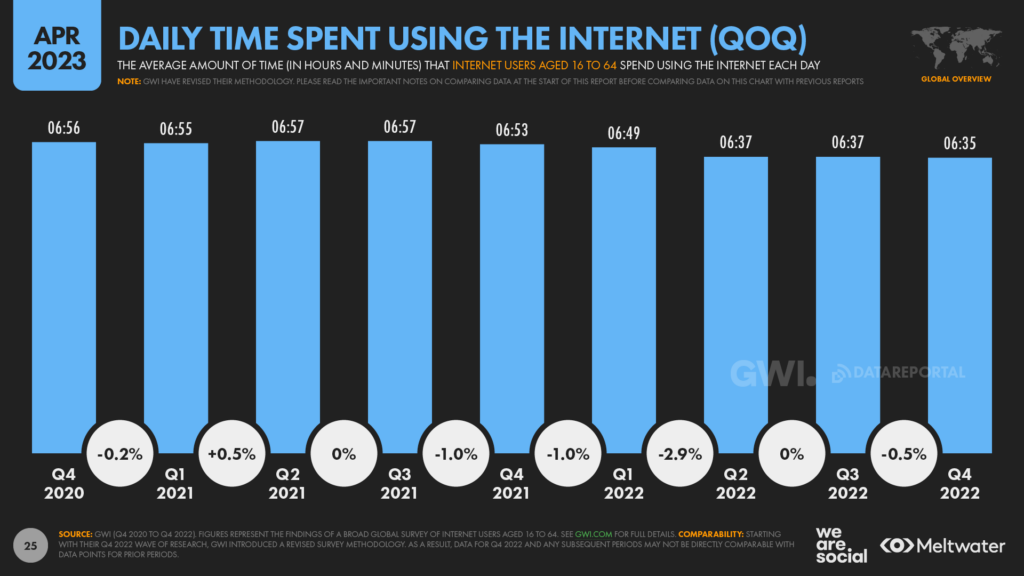

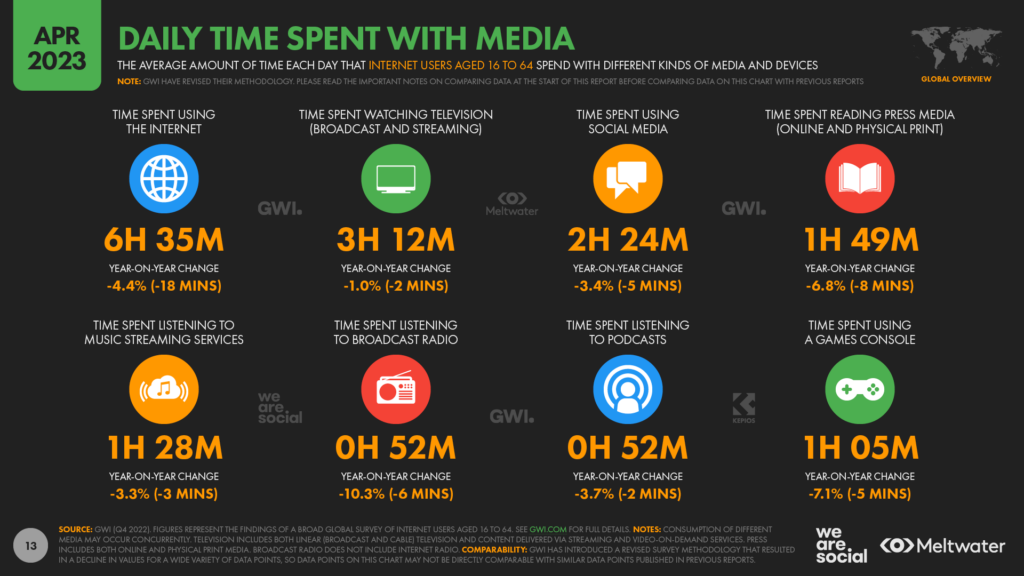

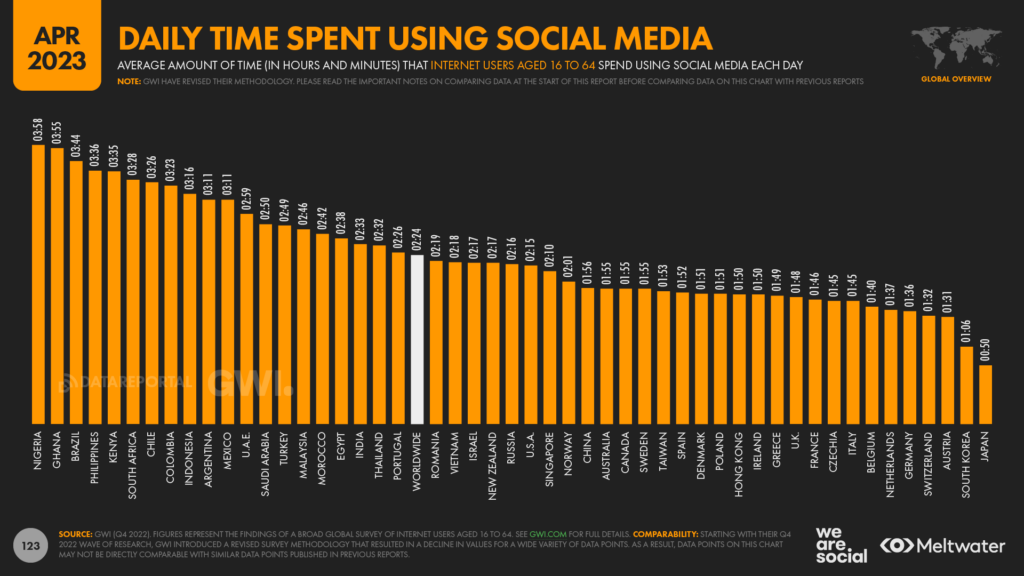

Online time continues to fall

GWI’s latest wave of research indicates that the amount of time the world spends online continues to decline.

It’s worth highlighting that the latest figures have been impacted by the changes to GWI’s methodology that we highlighted above.

However, our analysis – together with that of GWI’s own trends team – suggests that the continued downward trend isn’t just the result of these methodology updates.

The latest figures reveal that the typical internet user now spends an average of 6 hours and 35 minutes per day using connected tech.

That worldwide average is down by 2 minutes per day compared with the figure that we reported in our Digital 2023 Global Overview Report back in January, equating to a quarter-on-quarter decline of half a percent.

Meanwhile, GWI’s data indicates that internet users have reduced their online activities by an average of 18 minutes per day since this time last year, resulting in a year-on-year reduction of 4.4 percent.If you’d like to know more about what’s driving this trend, we explored potential reasons for these declines in our detailed Digital 2023 Deep-Dive.

But while these changes in the time that we spend online are important, it’s also worth putting the latest figures in perspective.

For example, we’re still spending an average of over 6½ hours per day using the internet, which is more than twice as much time as we spend watching television.

Moreover, the current average suggests that the world will still spend a combined total of 1.4 billion years of cumulative human existence using connected tech in 2023 alone.So, while we may be spending less time on the internet, there’s nothing to suggest that the internet is becoming any less important in our lives.

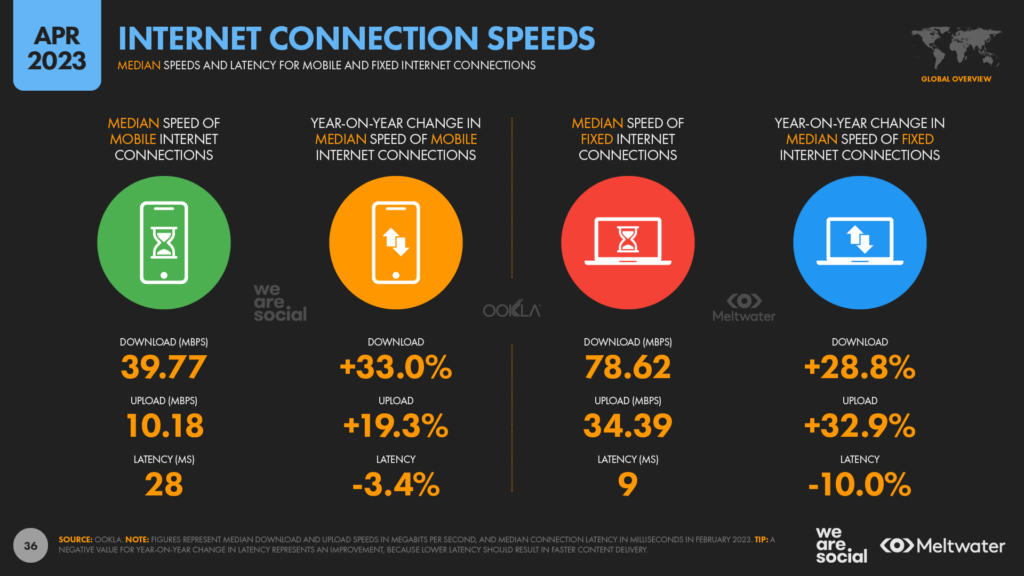

Internet connection speeds have surged

Meanwhile, data reveals that it now takes less time for us to access the content that we want when we do go online, with analysis from Ookla revealing that internet connection speeds have increased significantly over recent months.Mobile bandwidth has jumped by a third over the past year, with the worldwide median reaching almost 40 Mbps in February 2023.

For comparison, the median speed for mobile cellular data (39.77 Mbps) is now almost as fast as the mean value for fixed connections that we reported just 5 years ago (40.7 Mbps).

In total, 9 countries around the world now enjoy median mobile download speeds in excess of 100 Mbps, although an equal number of countries still struggle with median speeds below 10 Mbps.

The speed of fixed connections continues to accelerate too, with Ookla’s Speedtest data showing an annual growth rate of almost 29 percent.

At a worldwide level, internet users going online via fixed connections enjoy a median download speed of 78.62 Mbps, which should be enough to enable the streaming of five separate 4K movies over the same connection at the same time.

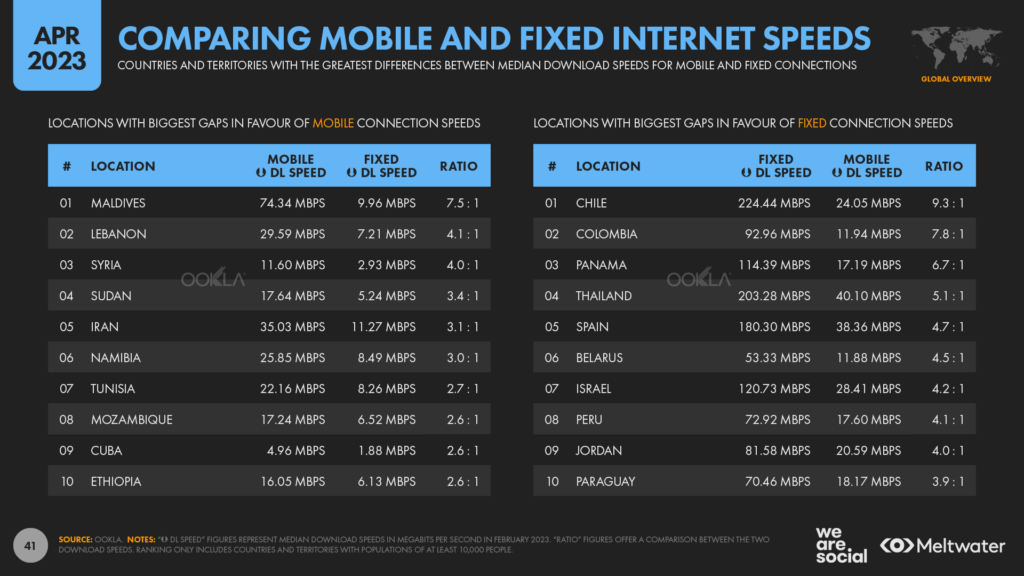

However, fixed connection bandwidth varies meaningfully around the world.Internet users in top-ranked Singapore enjoy a median download speed in excess of 237 Mbps, which is more than 125 times faster than the download speeds endured by Cuba’s fixed internet users.

But it’s interesting to note that the gap between mobile and fixed connection speeds appears to be closing.

This time last year, Ookla’s data showed that the typical fixed connection was still more than twice as fast as the typical mobile connection, but that multiple has fallen below two in the company’s February 2023 data.

And the continued advance of 5G networks has likely played an important role in closing this gap.For context, median mobile connections now outpace median fixed connections in a total of 48 countries around the world, and in six countries, cellular data is at least three times faster than fixed connections.

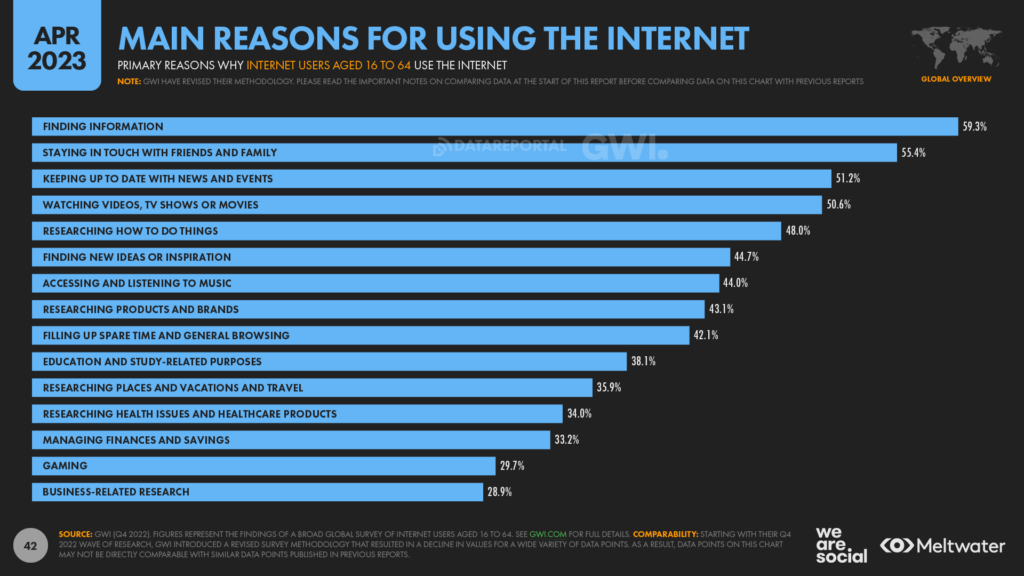

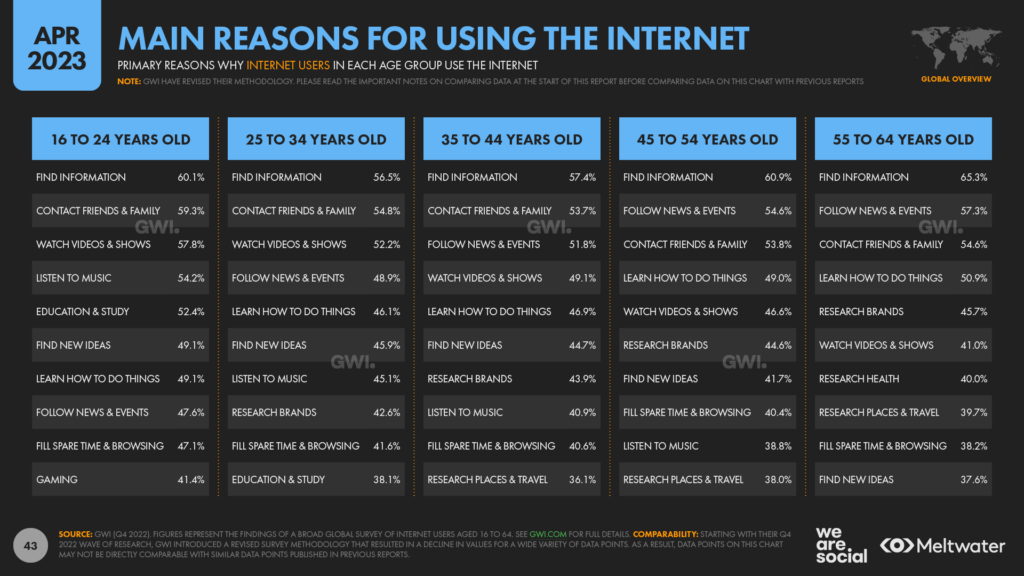

Comparing internet use motivations

With the help of GWI, we’re pleased to include a new chart in this quarter’s report that compares the reasons why people go online by age.

Just before we explore this new data, here are the world’s overall internet motivations, averaged across all users aged 16 to 64:

So how do things vary with age?

Well, perhaps the most obvious takeaway in the age-specific data is that “finding information” remains the primary motivation across all age groups.

However, it’s interesting to note that the number of respondents who select this option varies meaningfully across age groups, from a low of 56.5 percent amongst people aged 25 to 34, to a high of 65.2 percent amongst people aged 55 to 64.

Once we move past that top motivation however, clearer differences start to emerge.

Staying in touch with friends and family ranks second amongst younger age groups, but slips to third place amongst users over the age of 45, who place greater importance on following news and current events.

In contrast, following the news ranks just eighth amongst users aged 16 to 24.

Younger people are also significantly more likely to use the internet for entertainment than their parents are.

For example, watching video content and accessing music rank third and fourth (respectively) amongst users aged 16 to 24.

However, watching video content slips to sixth place amongst users aged 55 to 64, while accessing music doesn’t even rank in the top 10 motivations for this older age group.

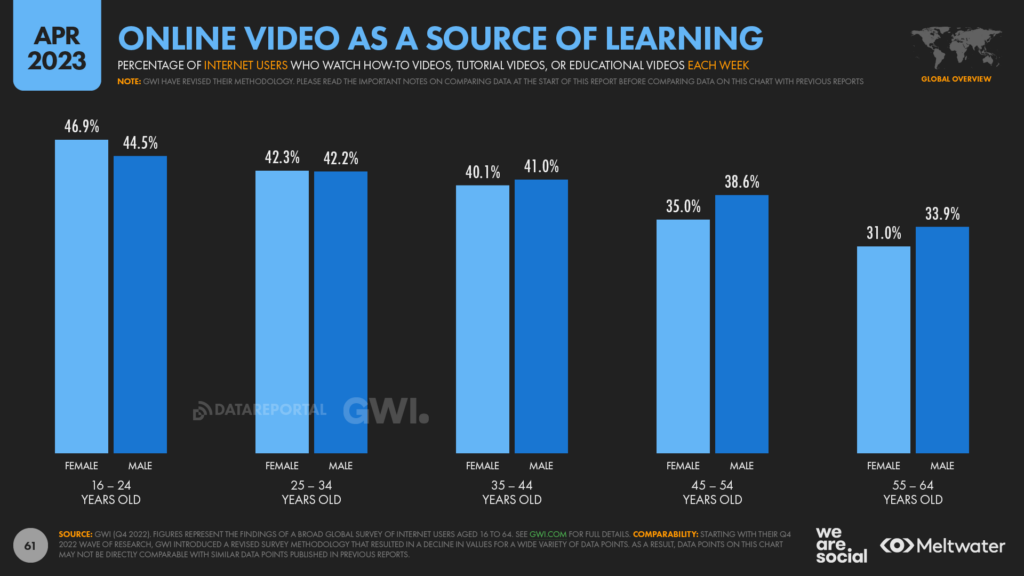

Somewhat surprisingly though, older people are more likely to say that they go online to learn how to do things.

This motivation only ranks seventh amongst the youngest age group in GWI’s survey, but it rises to fourth place amongst the oldest users.

However, it’s worth noting that video might not be the top opportunity here, because GWI’s data also reveals that older generations are less likely to seek out online video as a source of learning.

So, if you’re creating “how to” content, it’s probably a good idea to offer text and images as well as video.

But perhaps the most important takeaway for marketers in the age-specific motivations data is the extent to which older generations rely on the internet to inform their purchase decisions.

Crucially, internet users aged 55 to 64 say that researching brands is the fifth most important reason why they go online, while researching health and researching places and travel also rank in their top 10.

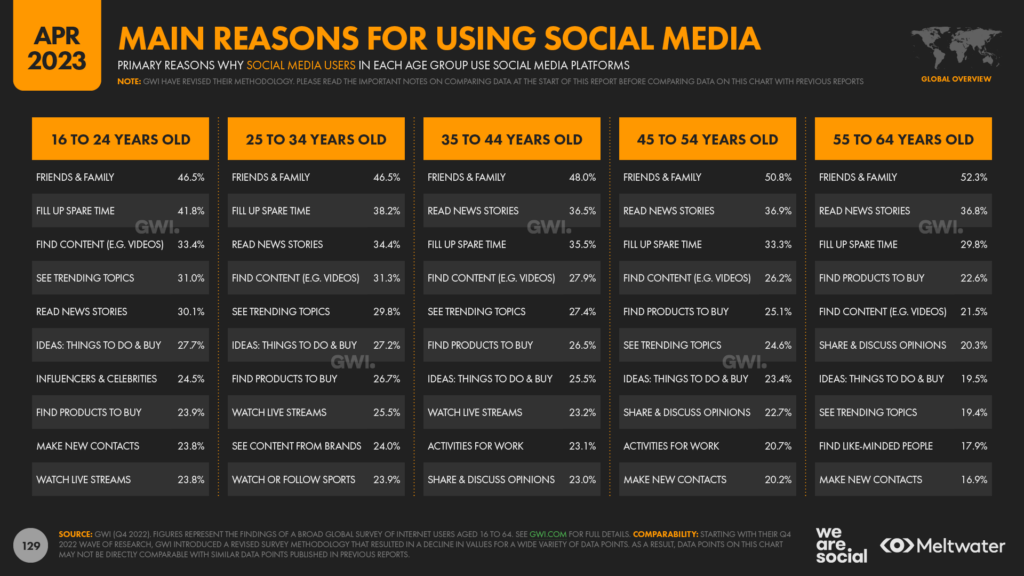

And somewhat surprisingly, this trend appears in people’s motivations for using social media too.

Indeed, in contrast to stereotypes, GWI’s data reveal that it’s not just young people that are influenced by marketing messages on social platforms.

Finding products to buy ranks fourth amongst the reasons why people aged 55 to 64 use social media, whereas this motivation ranks just eighth amongst users aged 16 to 64.

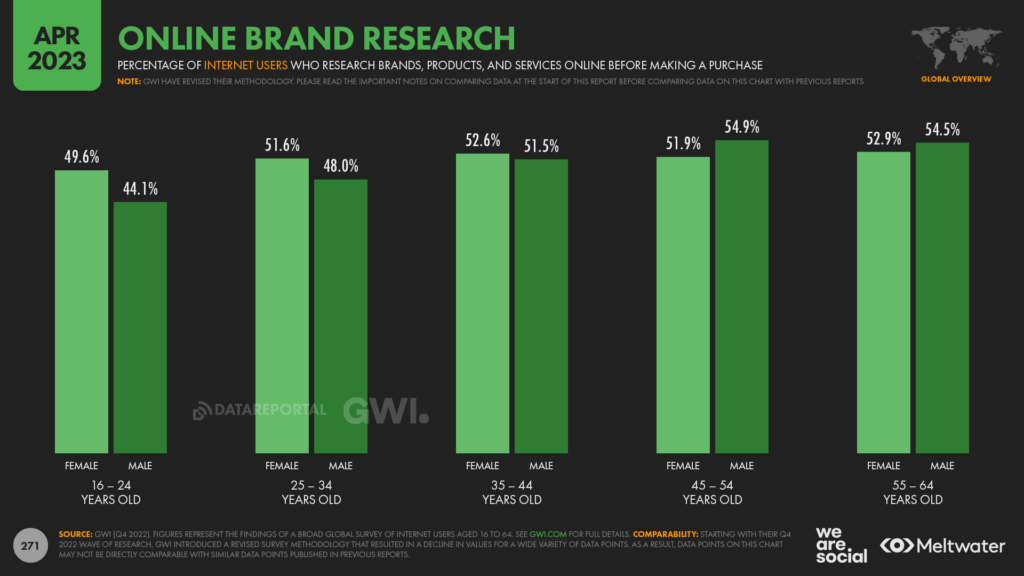

This trend emerges elsewhere in GWI’s survey too, with internet users aged 55 to 64 the most likely to say that they research brands, products, and services online before making a purchase.

So, don’t let stereotypes fool you: online channels are just as valuable for marketing to Boomers as they are for marketing to Gen Z.

But what are the best ways to reach those older generations when they’re looking for information about brands?

Well, we’ve got even more good news for you here: GWI’s data also allows us to see where people go to research brands online, broken down by age.

And one of the most interesting takeaways here is that brand websites are still a crucial source of information for those older age groups.

Sure, TikTok may be all the rage with younger users, but with people over the age of 50 accounting for more than half of all US consumer spend, it’s well worth investing in a diverse marketing mix that caters to the motivations and behaviours of all age groups.

Digital in the workplace

As part of this quarter’s report, we’ve teamed up with GWI to bring you fresh insights into how people around the world use digital in the workplace.

This new data – sourced from GWI’s extensive Work survey – offers powerful insights into how people in different countries and across different age groups use connected tech in the office, and in B2B settings.

So what does this data tell us?

Let’s dive in.

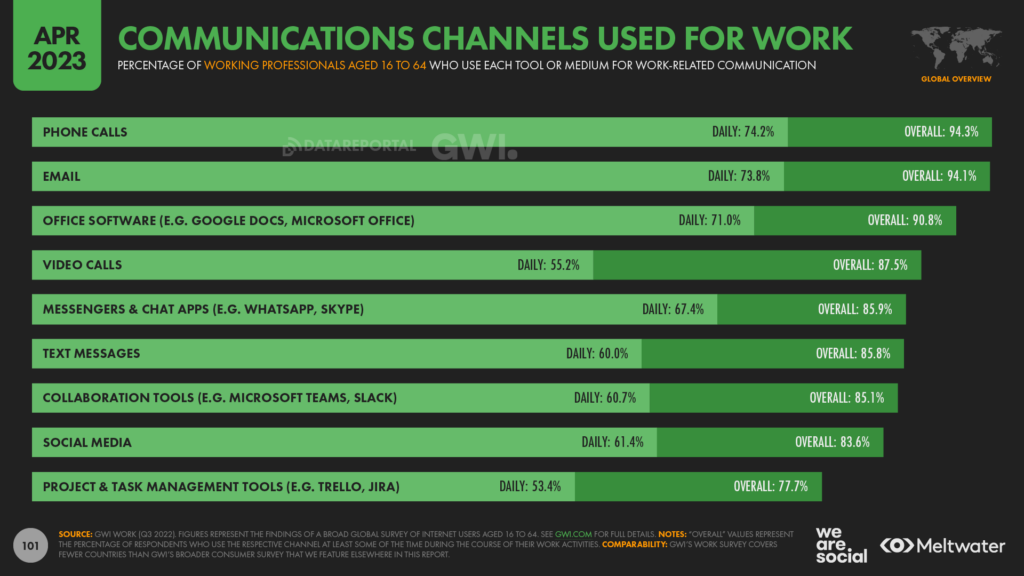

Video calls seem set to stay

The solutions that people turned to during the height of the COVID-19 pandemic appear to have had a lasting impact on digital behaviours in the workplace.

Despite “Zoom fatigue” remaining an enduring memory for many people who worked through lockdown, video calls still rank amongst the most used channels for workplace communication.

87.5 percent of working-age professionals say that video calls are a regular part of their working life, although it’s worth highlighting that just 55 percent say that they attend such calls on a daily basis.

For context, video calls now rank ahead of messenger platforms, text messages, and even collaboration tools like Slack when it comes to workplace comms.

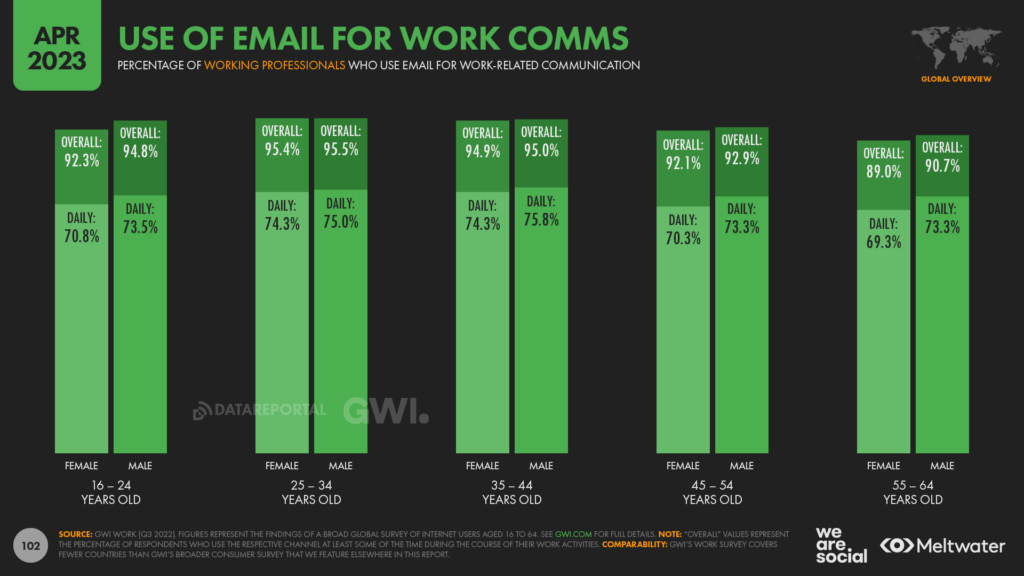

Email use is still near universal at work

The latest data indicate that inbox management is still an everyday reality for almost three-quarters of the world’s working professionals, while more than 94 percent use email at least occasionally.

It’s also interesting to note that email use is largely consistent across age groups, even when it comes to how frequently people use this channel for work comms.

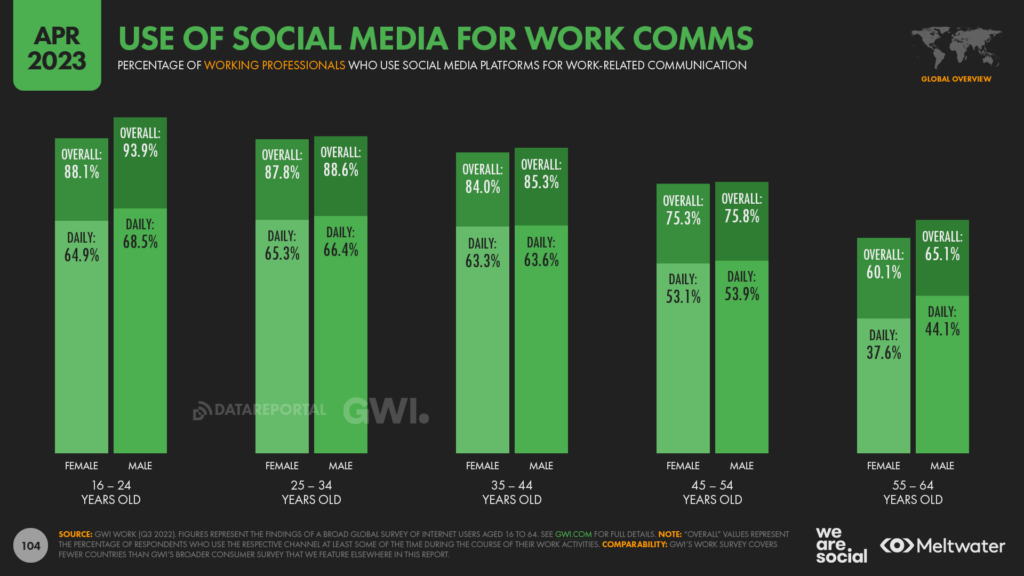

Social media: it’s an age thing

Things look a bit different when it comes to social media use in the office, though.

More than 9 in 10 working professionals aged 16 to 24 say that they use social media for work-related communication, compared with fewer than 2 in 3 professionals between the ages of 55 and 64.

Similarly, roughly 6 in 10 Gen Z professionals say that they use social media for work on a daily basis, compared with just 1 in 3 professionals between the ages of 55 and 64.

Interestingly however, across all age groups, men are more likely than their female peers to use social media for work communications, even though women are more likely to use social media outside of the office.

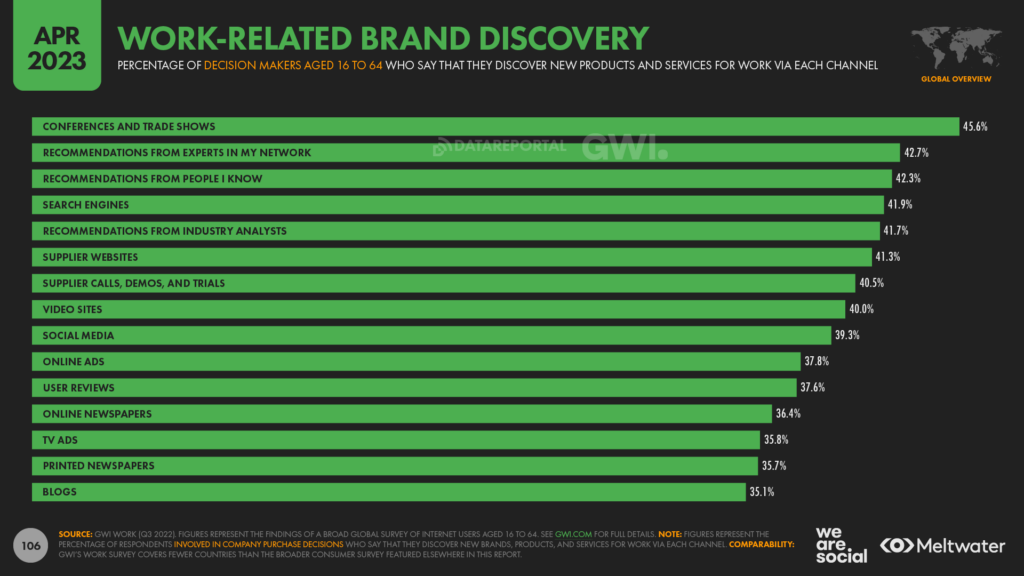

Traditional channels still essential for learning about new B2B brands

Conferences and trade shows are still the primary channels through which B2B buyers learn about new products and services, with 45.6 percent of decision makers citing these events as a key source of B2B brand discovery.

Recommendations from experts in a person’s network ranked second, while broader peer-to-peer recommendations ranked third.

And once again, these findings highlight the importance of a balanced mix of both online and offline channels, even when it comes to B2B marketing.

For example, while word-of-mouth remains a critical channel for discovering B2B solutions, it’s likely that many people turn to internet-powered services such as WhatsApp, Slack, and LinkedIn to chat with peers and seek out the views and recommendations of experts.

Similarly, while many B2B decision-makers stress the continued importance of in-person trade events, B2B marketers will want to maximise returns on these investments by amplifying their on-ground activities via digital channels.

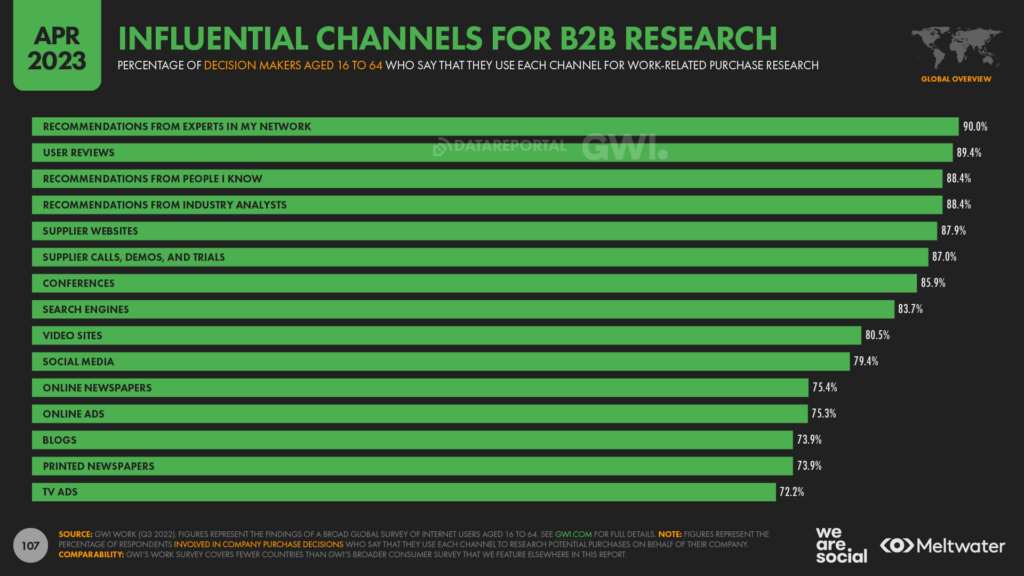

Channels used for B2B research

GWI’s research reveals that word-of-mouth is central to the research phase of the B2B buyer journey too, with fully 9 in 10 business decision makers stating that they seek out recommendations from experts in their network when researching B2B purchases.

Meanwhile, “user reviews”, “recommendations from people I know”, and “recommendations from industry analysts” take the next three places in GWI’s ranking of channels by importance in the B2B research phase.

But websites remain critical too, with almost 88 percent of B2B decision makers saying that they turn to suppliers’ sites when researching potential purchases.

Social media appears lower down the ranking, but roughly four in five B2B buyers say that they turn to social platforms when researching B2B purchases, so social still represents a valuable B2B opportunity.

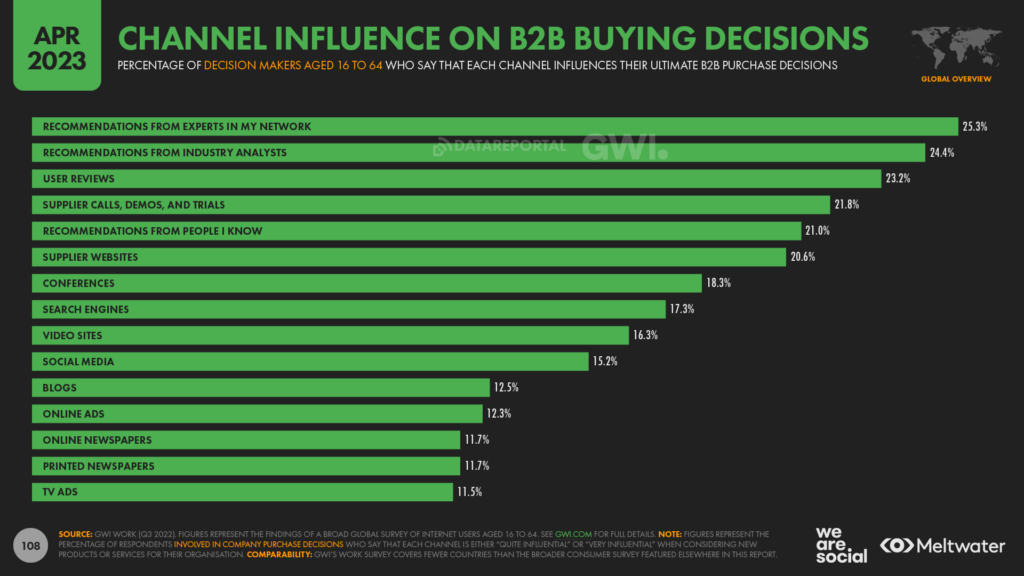

Channels with most influence on B2B decision making

GWI’s data shows that B2B decision makers turn to a wide variety of channels when researching potential purchases, but the data also reveals that these channels have differing degrees of influence over the final purchase decision.

Once again, word-of-mouth comes out top, with “recommendations from experts in my network”, “recommendations from industry analysts”, and “user reviews” cited as the three most influential channels.

But while it’s likely that these top three “channels” comprise a mix of both offline and online conversations, B2B marketers will want to explore how they can use digital activities to amplify the visibility of recommendations and reviews.

For example, you might want to invite experts in your industry to present at your in-person event, upload a video of that presentation to your YouTube channel, and then conduct a live Q&A with your broader audience via a LinkedIn Live livestream.

Similarly, highlighting user reviews on key pages of your website can help reinforce your message and build intent.

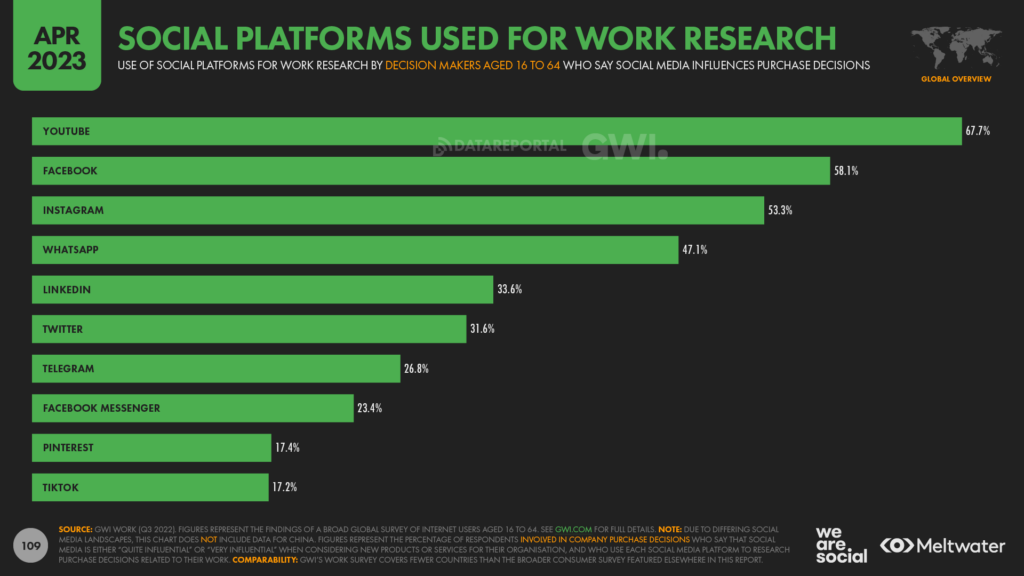

Social media in the workplace

Top social media channels for B2B research

YouTube appears to be the primary social media destination for decision makers exploring potential B2B purchases.

More than two-thirds of respondents outside of China who say that social media influences their purchase decisions say that they watch videos on the platform as part of their research activities.

Interestingly, despite their respective positionings as “consumer” platforms, Facebook ranks second, while Instagram ranks third.

And somewhat surprisingly, LinkedIn only ranks fifth in GWI’s latest survey, although it’s worth stressing that use of the platform varies by industry.

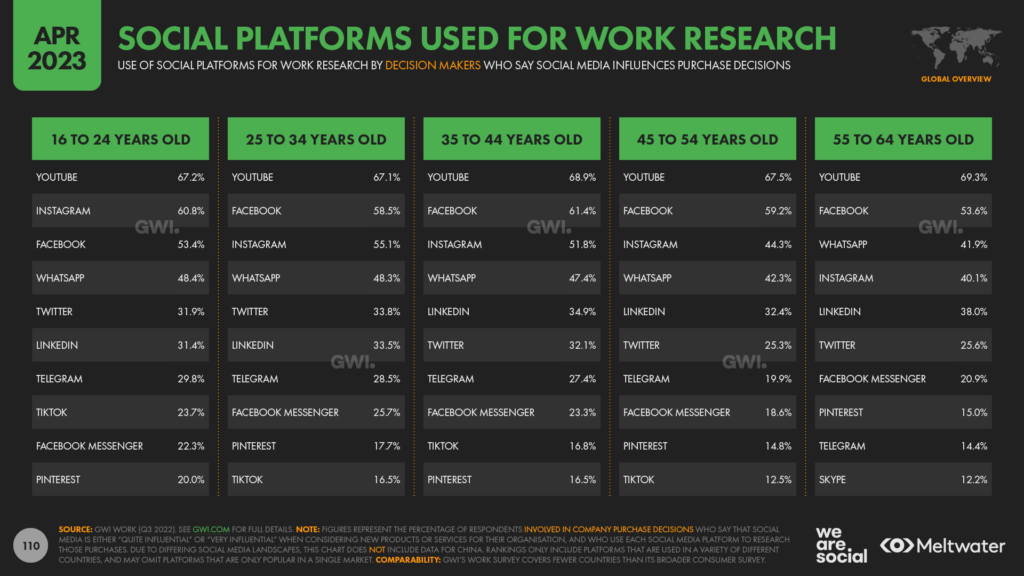

The social media channels used for B2B research also vary by age, although GWI’s latest Work survey shows that YouTube comes out top across all age groups.

Comparatively, Instagram is more widely used amongst younger age groups, while older generations prefer Facebook and WhatsApp.

Meanwhile, in another eye-opening finding, data shows that TikTok has now made its way into B2B research activities too.Almost a quarter of B2B decision makers between the ages of 16 and 24 say that they use the short-video platform to research work-related solutions, although it’s worth noting that the platform doesn’t even appear in the top 10 amongst working professionals over the age of 55.

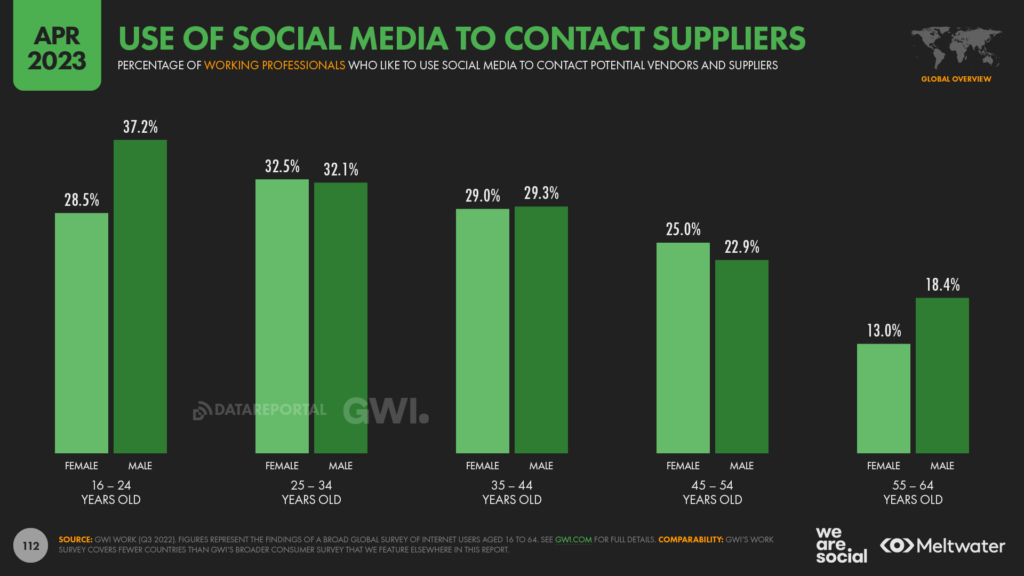

Contacting suppliers via social media

It’s also worth highlighting that social media’s role isn’t just related to outbound B2B marketing.

At a worldwide level, nearly 3 in 10 working-age professionals say that they use social media to contact suppliers, with that figure rising to nearly 4 in 10 in China.

Admittedly, figures are somewhat lower across Europe and the US, but with younger people significantly more likely to use these channels to contact potential suppliers, the importance of social media as an inbound channel looks set to grow.

Social media marketing

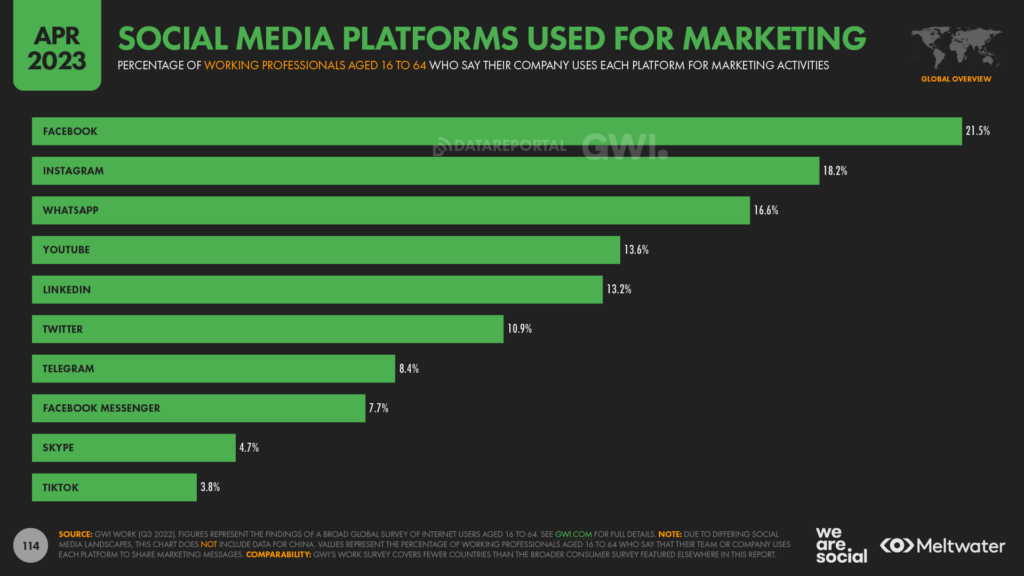

More than half of the professionals surveyed in GWI’s latest Work survey said that their company now uses at least one social media platform to share marketing messages, regardless of whether they’re marketing to B2C or B2B audiences.

However, with just 58.1 percent of respondents answering in the affirmative, the latest data suggest that over 4 in 10 companies do not use social media for any kind of marketing today.

Outside of China, Facebook remains the top choice for marketing activities, but the same data shows that barely 1 in 5 companies – just 21.5 percent – currently uses the world’s most widely used social media platform for marketing.

Instagram ranks second, with 18.2 percent of respondents saying that their company uses the platform for marketing.

However, the biggest surprise for me in this data is how few companies use YouTube for marketing.

Despite being the world’s second most widely-used social platform – as well as the world’s second-most visited website – GWI’s data suggests that just 13.6 percent of companies currently use YouTube to market their offerings.

Meanwhile, despite attracting more than 1 billion active users every month, very few companies appear to have embraced TikTok, and GWI reports that less than 4 percent of companies currently use TikTok for marketing.

So, if your company remains a social media “laggard”, you might want to collect a few of the charts from this quarter’s report, and put together a recommendation for your CMO.

Recalibration of figures for social media use

The changes to GWI’s core survey methodology that I outlined earlier have had a particularly important impact on some of our key metrics for social media use, so it’s worth highlighting the “revised” figures here.

First up, the latest data show a slightly lower average for the time spent using social media compared with the figures that we published in January.

At a worldwide level, the typical social media user now spends roughly 2 hours and 24 minutes per day using social channels, which is 7 minutes lower (-4.4 percent) compared with that January figure.

However, previous trends suggest that most of this change will likely be the result of GWI’s methodology update, rather than an actual drop in social media activity.

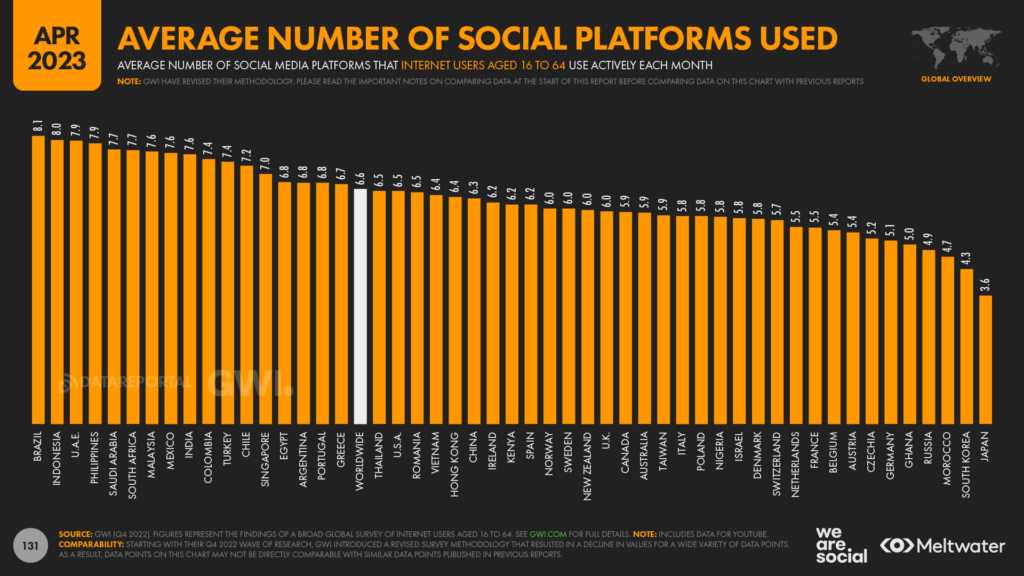

Similarly, GWI’s tools now report a lower figure for the number of social media platforms used per user, per month compared with last quarter’s data.

The latest data indicate that social media users now make active use of an average of 6.6 platforms per month, down from the 7.2 figure that we reported three months ago.

However, analysis by GWI’s own teams suggests that previous figures may have been skewed by a small number of outliers, and this is exactly what the company’s recent methodology changes are designed to recalibrate.

As a result, it’s important to view the differences between the figures for January and April as a revision, rather than as a drop that will be representative of the “typical” user.Given the importance of these two metrics, we’ll update you on trends in these numbers again in our forthcoming July 2023 Global Statshot Report, when we’ll see whether recent changes are purely the result of that methodology update, or if they in fact reveal new changes in people’s online behaviour.

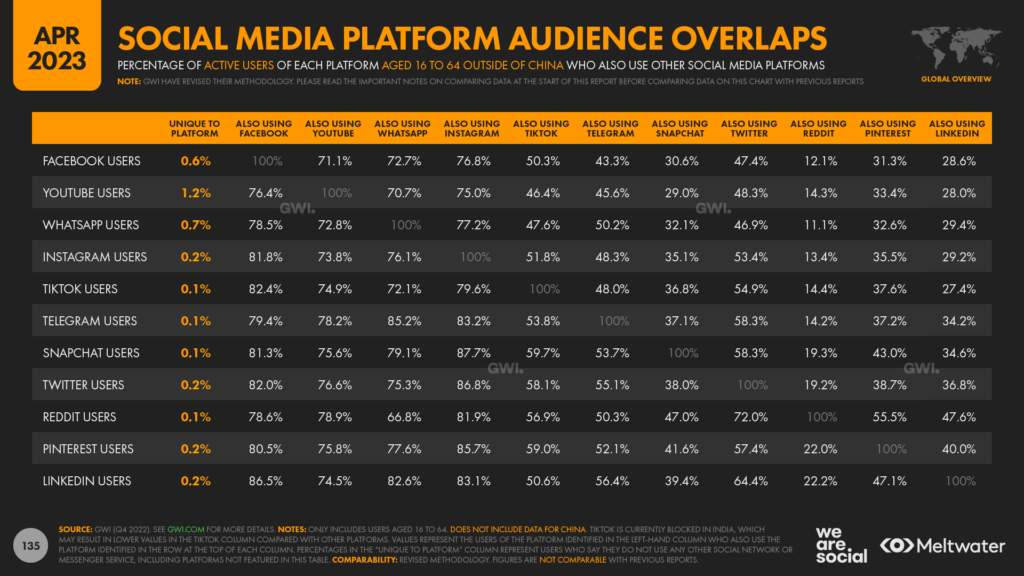

However, I was interested to note that GWI’s methodology changes appear to have had little impact on our popular social media audience overlaps chart.The overlaps for some individual platform pairs (e.g. Facebook and Instagram) have seen drops of a percentage point or two, but the overall takeaway from this data remains the same: marketers can still reach almost 99 percent of the users of any given social media platform on at least one other platform.

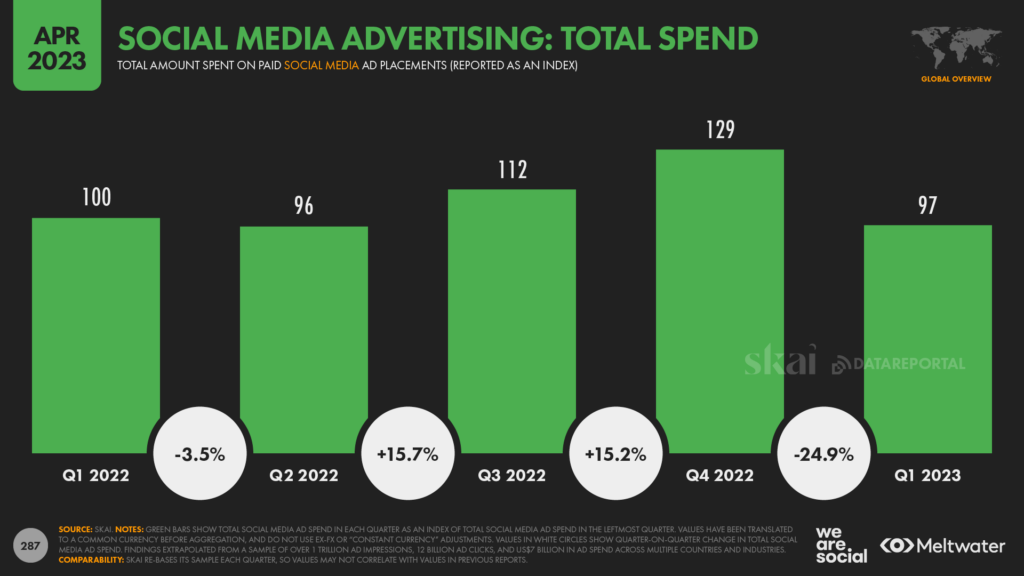

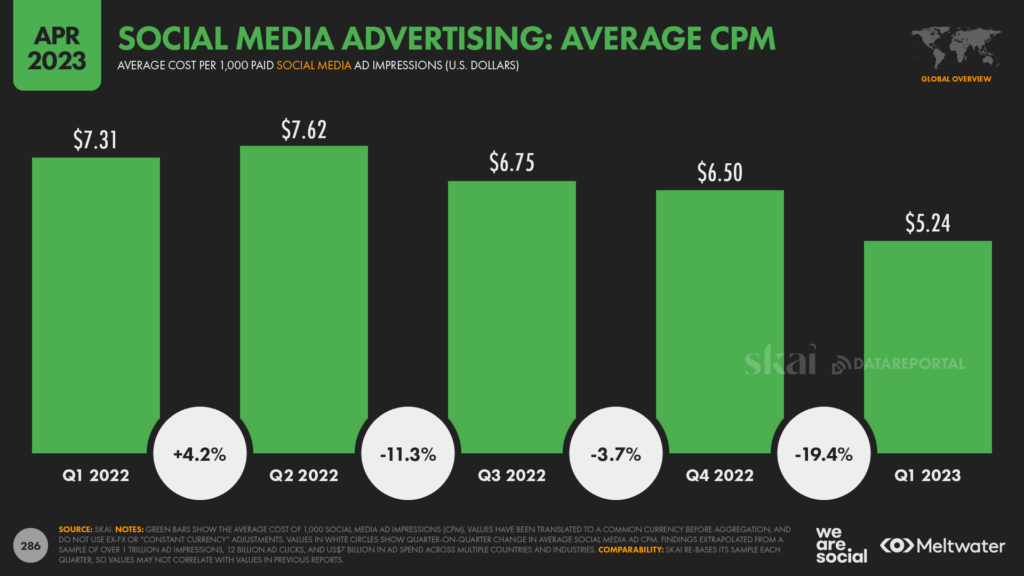

Social media ad spend declines

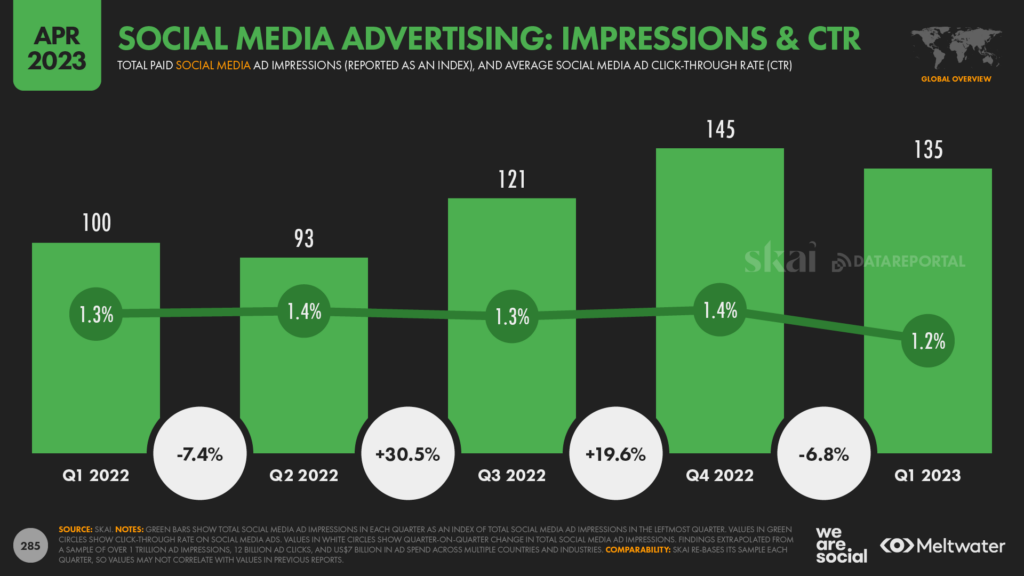

The latest analysis from Skai.io indicates that spend on social media ads has fallen compared with this time last year.The company’s data – which reports activity as an index – reveals a 3 percent decline in global social ad spend in the first quarter of 2023, as compared with Q1 2022.

However, the total number of social media ad impressions served jumped by roughly 35 percent during the same period.

So, as you might expect given the diverging trends in these two metrics, the cost of each social media impression has actually fallen meaningfully over recent months.

For context, it’s not uncommon to see big drops in “CPMs” – i.e. the cost to deliver 1,000 ad impressions – as we transition from the highs of the Q4 “holiday” season into the more conservative first quarter of the following year.

However, Skai’s data also reveals a meaningful year-on-year drop in social media CPMs, with the global average for Q1 2023 almost 30 percent lower than the average for Q1 last year.

But while the total number of impressions served may have increased, it’s worth highlighting that click-through rates actually declined during recent months.

Skai’s data points to a year-on-year drop of roughly 12 percent in average click-through on social media ads.

Balancing that, the sizable drop in average CPMs means that advertisers should still be seeing an improved “cost per click” compared with this time last year, but marketers should keep their eye on these trends, to ensure they can optimise their activities for the most relevant outcomes.

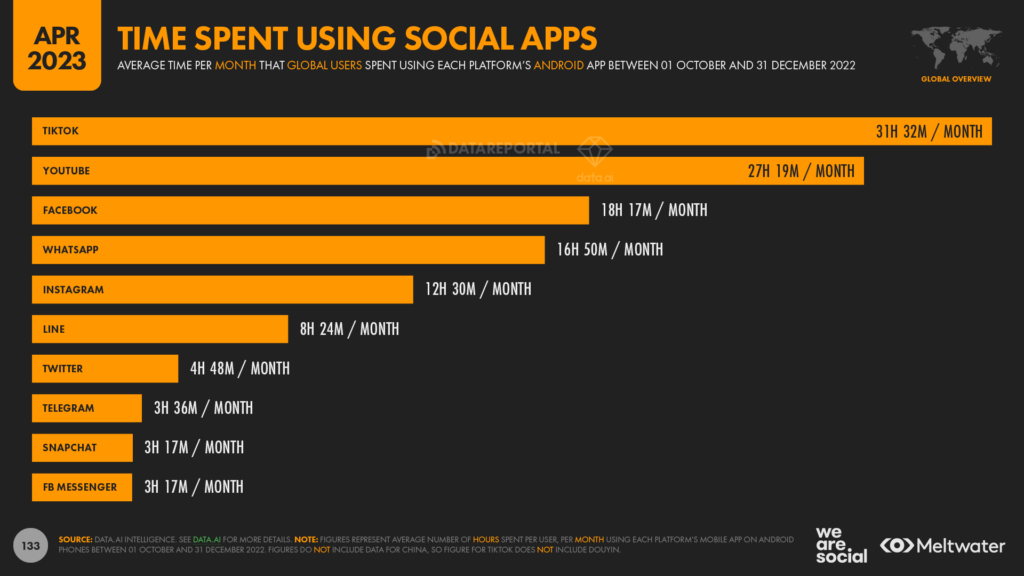

Users spending more time on TikTok

New analysis from data.ai shows that people are spending even more time using TikTok.

Average figures for Q4 2022 show that users spent an average of more than 31½ hours per month using TikTok’s Android app between October and December.

That was more than 4 hours per month more than second-placed YouTube, where users spent an average of 27 hours and 19 minutes per month using the platform’s Android app.

As always though, it’s important to remember that YouTube is still the world’s second most visited website, so it’s likely that YouTube’s overall user average is considerably higher than these app-specific figures suggest.

However, TikTok appears to be growing average time more quickly than YouTube, with data.ai’s figures indicating that TikTok users increased their activity by more than an hour per month in Q4, compared with the previous quarter.

Conversely, the average time spent using Facebook’s Android app showed a modest drop over the course of Q4 compared with the previous three months, but Kepios analysis indicates that this decline has actually reversed over the first three months of 2023.

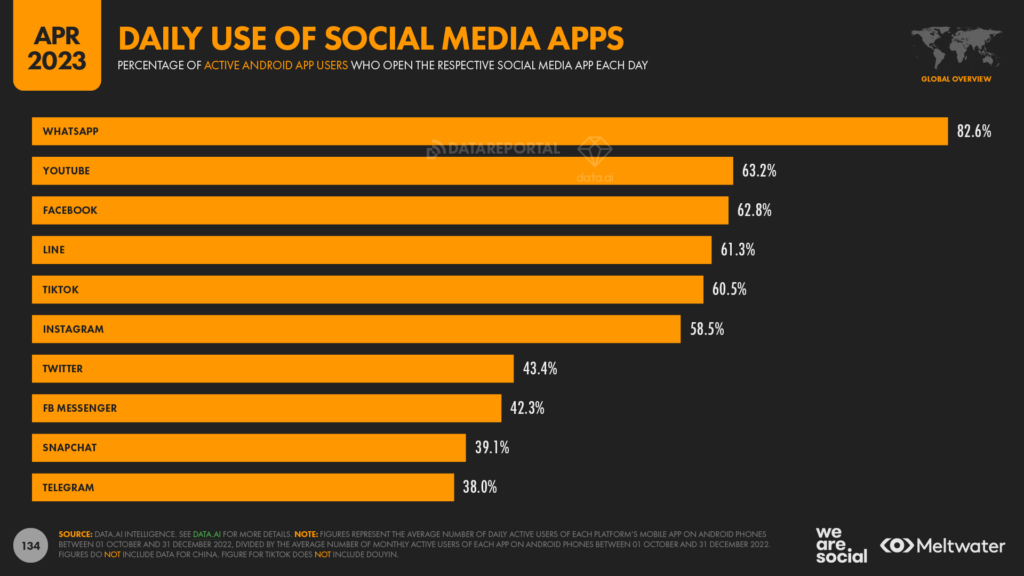

It’s also interesting to note that Facebook also enjoys one of the highest “open rates” of any social media app.

Further analysis from data.ai shows that WhatsApp sees the highest frequency of use amongst the world’s most used social platforms, with a hefty 82.6 percent of the platform’s monthly active Android app users opening the app each day.

YouTube ranks second, with 63.2 percent of active users opening the app on a daily basis.

However, Facebook ranks third, with its 62.8 percent daily open rate putting it ahead of both TikTok (60.5 percent) and Instagram (58.5 percent).

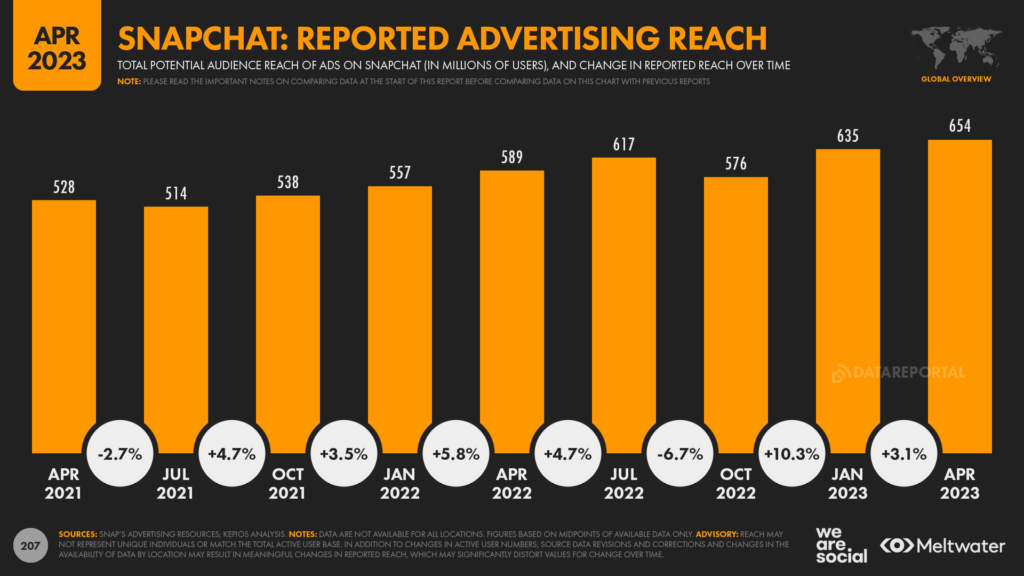

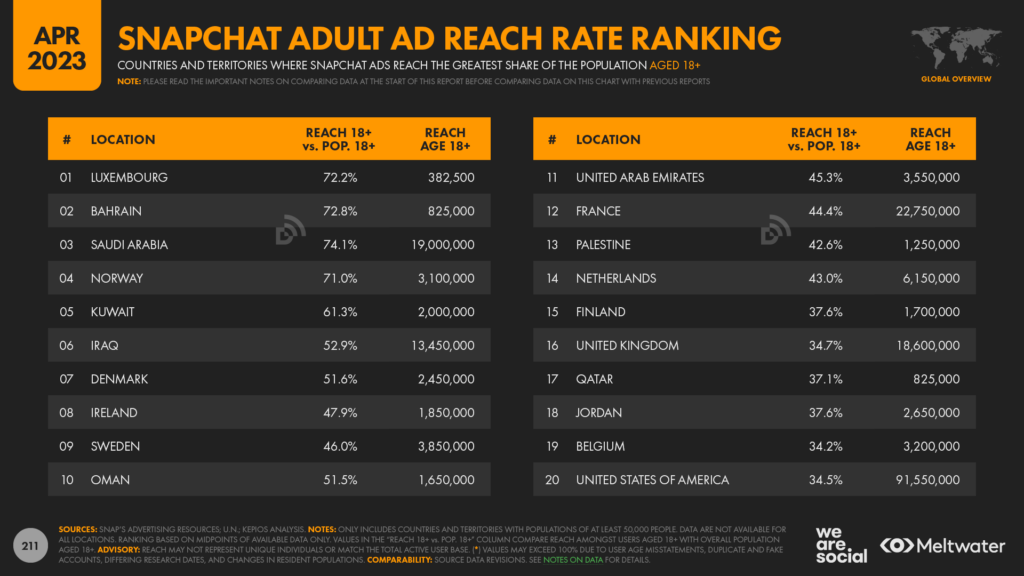

Snapchat is a growing force

Snapchat doesn’t seem to capture as many media headlines as TikTok or Instagram, but data shows that the platform has been growing steadily over recent months, and continues to offer compelling opportunities for marketers.

For example, in February 2023, the company announced that it had reached 750 million global monthly active users.

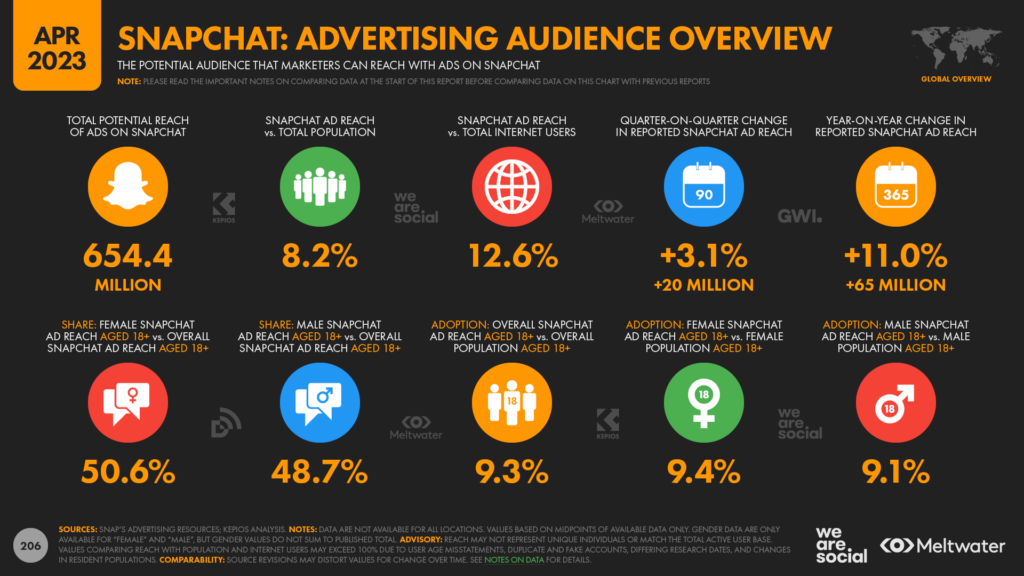

That compares with the 600 million MAU figure that the company reported just 10 months prior, indicating that Snapchat has likely grown its total user base by more than 25 percent over the past year.Meanwhile, the latest figures published in the company’s own ad planning tools show that ads on Snapchat now reach more than 650 million users each month, with that global ad audience growing by a healthy 11 percent over the past twelve months.

This is the highest figure we’ve seen for global Snapchat ad reach, and suggests that more than 1 in 8 of the world’s internet users now see Snapchat ads every month.

The company’s own data indicates that users aged 18 to 24 account for the largest share of that global ad audience, but – as with all social platforms – it’s worth noting that these demographics may be skewed by users “misstating” their age.

The company’s ad data also shows that Snapchat is popular all over the world, but that the platform is a particularly good option for marketers hoping to reach audiences across the Middle East – especially women.

Having said that, the company’s data also suggests that ads on Snapchat now reach 1 in 3 adults in the US and the UK each month, so Snapchat’s opportunities aren’t limited to any one geography.

Twitt… err… what?

The past few weeks have been “interesting” for anyone following developments at Twitter.

Perhaps the biggest story for marketers over recent weeks was the company’s announcement that Twitter accounts will now need to be either a “Verified Organization” or a Twitter Blue subscriber in order to advertise on the platform.

For context, entities need to pay USD $1,000 per month to become a “Verified Organization”, or pay USD $8 per month for a Twitter Blue subscription.

But what advertising opportunities might these subscription fees unlock?

Well, given the ongoing confusion surrounding Twitter, it’s tricky to say for sure.

We’ve collected and analysed a wealth of the latest numbers to try to discern the current “state” of Twitter, but none of these numbers – not even the figures published in Twitter’s own, “official” advertising tools – tells a clear or consistent story.

As a result, we’ve conducted a more detailed study of current Twitter use, in an attempt to help you form something approximating an “informed” decision about the platform, as well as the opportunities it might offer.

You can read that analysis in full in this separate article, but prepare yourself for a rollercoaster ride that’s packed with surprises.

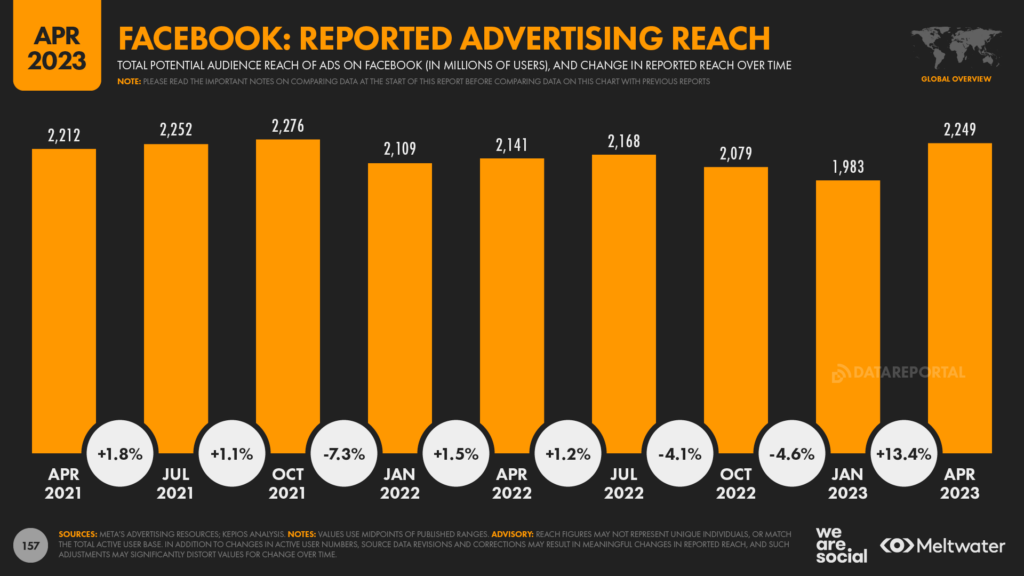

Meta’s tools showing more regular fluctuations

But Twitter isn’t alone in delivering surprising numbers this quarter.

Our ongoing analysis of the data published in Meta’s advertising tools also reveals more frequent – and more dramatic – swings in reported reach figures.

We explored this trend in detail in January 2023 in the context of an 11 percent annual decline in reported Instagram ad reach, and we also reported similar trends at the start of 2022.

However, the latest data reveal some particularly surprising – and somewhat incongruous – trends.

Let’s start by looking at Facebook.

Trends in Facebook’s reported ad reach

Figures published in Meta’s own Ads Manager tool suggest that global Facebook ad reach increased by a hefty 13.4 percent in just the past three months.

Back in January 2023, the same tool reported that ads on Facebook could potentially reach 1.983 billion users around the world, which represented a 4.6 percent decline versus the 2.079 billion figure published in October 2022.

However, in April 2023, that very same tool reported potential global reach of 2.249 billion, equating to a 13.4 percent increase in just three months.

As you can see on the chart below, fluctuations in reported reach aren’t uncommon, but our analysis of data going back to 2013 suggests that the size of these swings has increased over recent months.

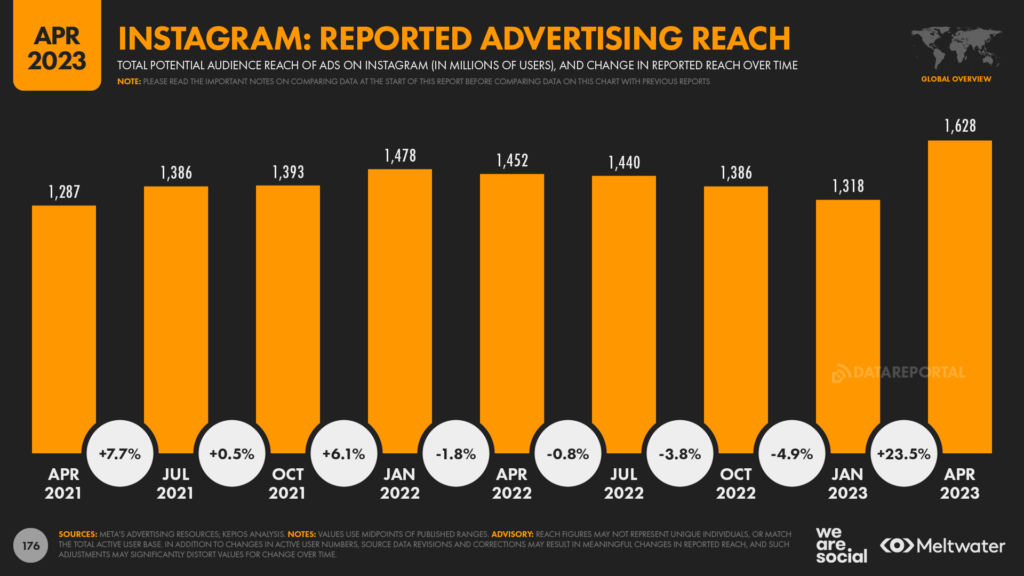

Trends in Instagram’s reported ad reach

But if those Facebook figures caught your attention, hold onto your hat, because the figures for Instagram are even more dramatic.

As you can see in the chart below, Meta’s reported figures for potential Instagram reach dropped by 4.9 percent between October 2022 and January 2023, from 1.386 billion to 1.318 billion respectively.

However, over the past three months, the reported reach figure has changed dramatically.

Meta’s tools now indicate that advertisers can reach a total of 1.628 billion users with ads on Instagram – i.e. 23.5 percent more than they could just three months prior.

For context, Meta’s latest estimate for Instagram reach is more than 10 percent higher than the previous all-time high of 1.478 billion, which the company’s tools reported in January 2022.

Making sense of Meta’s numbers

So what’s going on?

Sadly, Meta hadn’t responded to our requests for comment by “press time”, so we can only offer speculation.

However, the company’s latest numbers do appear to rule out one of our previous hypotheses, which was that recent declines in reported reach might have been the result of more active removal of “false” and duplicate accounts.

It seems very unlikely that Meta would suddenly re-approve hundreds of millions of accounts that it had previously identified as contravening its terms of service, so such purges probably aren’t the primary factor driving ongoing fluctuations.

Meanwhile, given the fact that both Facebook and Instagram are already well established – and that figures for overall internet use haven’t shown any dramatic increases in recent months – it seems even more unlikely that sudden growth in overall active users might be the cause of the recent jump in reported reach.

Changes in Apple’s privacy policies may have played a role, but the bulk of these changes were implemented well over a year ago, so it seems unlikely that they would be the cause of a sudden increase in reported reach now.

Meanwhile, more nuanced changes in users’ everyday platform activities, such as how long people spend using the platform, or which elements of the service they use (e.g. Reels) may also play a role.

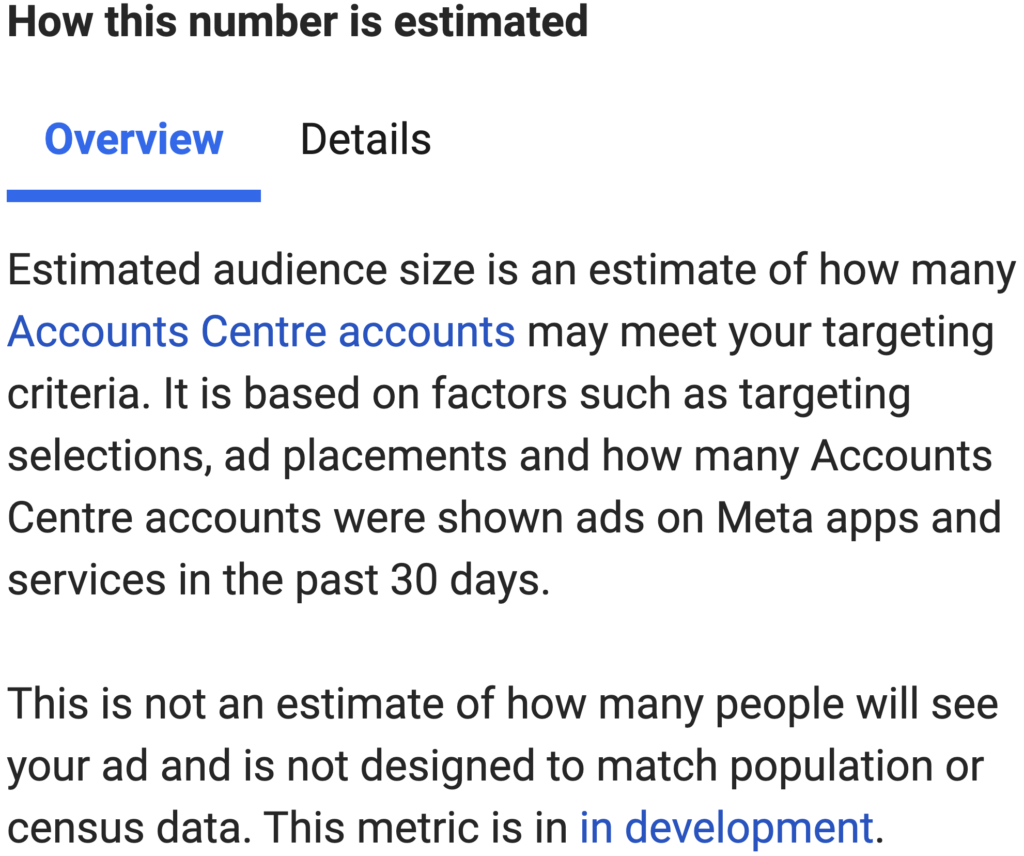

Again though, it seems unlikely that such changes would impact overall reach figures, because – at least as we understand Meta’s own definitions – a user would only need to be shown one ad in any given 30-day period in order to influence the potential ad reach figure:

For reference, Meta’s ad tools state that ad reach estimates are influenced at least in part by “how many… accounts were shown ads across Meta technologies and services in the past 30 days.”

All of which leads me to conclude that these changes are more likely the result of changes in Meta’s reporting methodology, rather than any meaningful change in active use or platform behaviour.

And guidance published in Meta’s own planning tools appears to corroborate that hypothesis.

Is Meta changing how it defines audience reach?

The following pop-up appears next to the company’s estimates for potential ad reach in its Ads Manager tool:

And it’s that last sentence that may hold the key here.

The “in development” hyperlink adds the following detail:

“An in-development metric is a measurement that we’re still testing. We’re still working out the best way to measure something, and we may make adjustments until we get it right.”

But with advertising still responsible for 97 percent of Meta’s revenue, it’s perhaps surprising to learn that the company is still “developing” a way to quantify the size of its ad audience – especially when these “adjustments” result in swings of almost 25 percent over a period of just three months.

A further company note goes on to explain:

“Why metrics are in development: We frequently launch new features and new ways of measuring how those features perform. Sometimes we publish these metrics even when the way we calculate them isn’t final to get more feedback, make them better and figure out the best way to measure performance. Once we’ve completed testing and established the way a metric is calculated, we’ll remove the in-development disclaimer.”

To be fair to Meta, there’s a good chance that actions by third parties (e.g. Apple’s privacy initiatives) have forced the company to change the ways in which it calculates and reports ad reach metrics.

However – somewhat alarmingly – the same note also states:

“Businesses shouldn’t use in-development metrics for… strategic planning or important business decisions.”

In other words, Meta’s own guidance appears to state that businesses shouldn’t use Meta’s own “official” audience reach estimates to inform their marketing plans and budgets.

I confess I’m not sure what to make of that statement, but considering that the entire digital advertising industry does rely on Meta’s ad metrics to inform strategic plans, I thought you should be aware of this guidance too.

Meta restricts demographic targeting

But it’s not just Meta’s reported ad reach figures that are changing.

Another new advisory published in the company’s ad planning tools states that:

“Audiences under age 18 globally, 20 in Thailand or 21 in Indonesia can’t be reached with campaigns that include certain options.”

One of the key consequences of this change is that marketers no longer appear to be able to target ads by gender to users below the age of 18 – at least via the company’s Ads Manager tools.

However, such restrictions were already in place in the ad planning tools of numerous other platforms – including YouTube and TikTok – so it seems that restricting demographic targeting to adult audiences is becoming something of an “industry standard”.

For clarity, marketers can still target ads to users between the ages of 13 and 17 using Meta’s ad planning tools, but they now have fewer options when it comes to identifying more specific audiences within that age group.

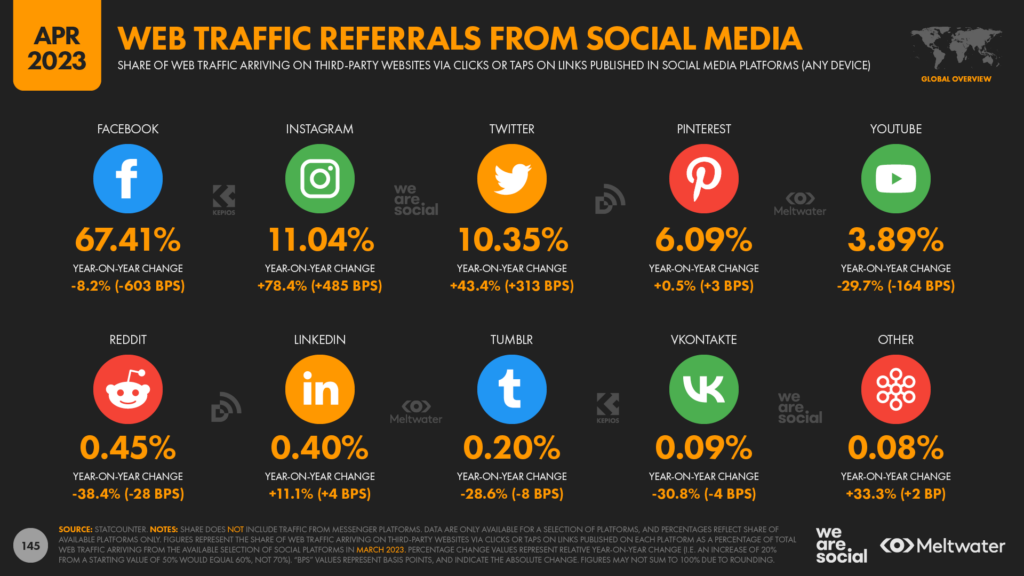

Social media referrals

New data from Statcounter reveals that Instagram has overtaken Twitter to become the second largest source of social media referrals.

Facebook still tops the global ranking, with Meta’s largest platform accounting for more than two-thirds of all web traffic referrals originating from social media.

However, Instagram’s 11.04 percent of total referrals in March 2023 puts it ahead of Twitter’s 10.35 percent in Statcounter’s latest analysis.

Pinterest now ranks fourth with 6.09 percent, while YouTube rounds out the top five, accounting for 3.89 percent of social media web referrals.

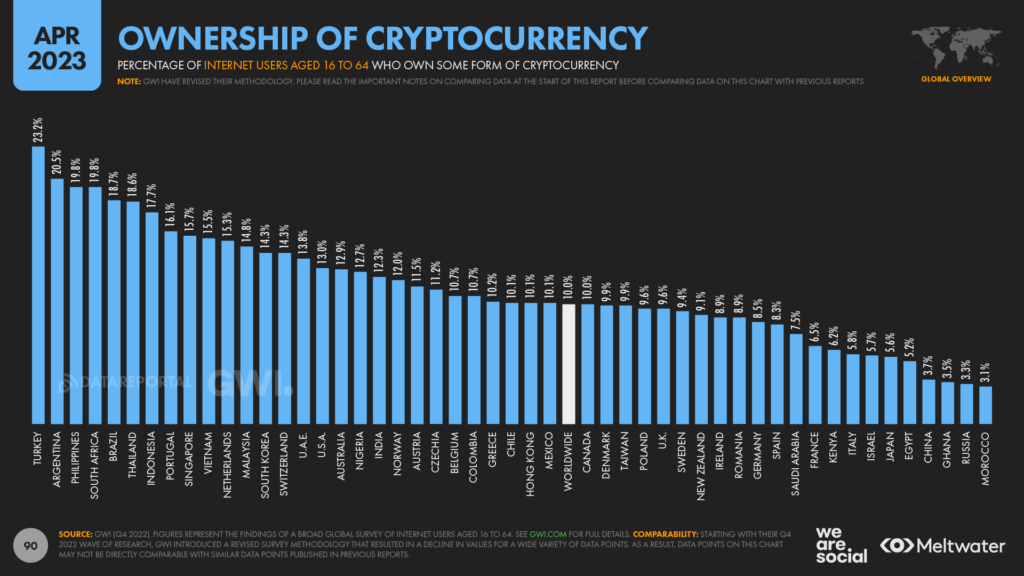

Many people exited crypto markets in 2022

GWI’s latest data shows a meaningful decline in the number of people who hold investments in cryptocurrency during the second half of 2022.

Once again, the changes in GWI’s methodology that I highlighted at the start of this analysis may be an important factor contributing to the latest drops.However, the company’s research shows that the number of working-age internet users who report owning some form of crypto fell from a high of 12.3 percent in Q2 2022, to just 10.0 percent in Q4.

That suggests close to 1 in 5 retail crypto investors may have exited all of their positions in the second half of last year.

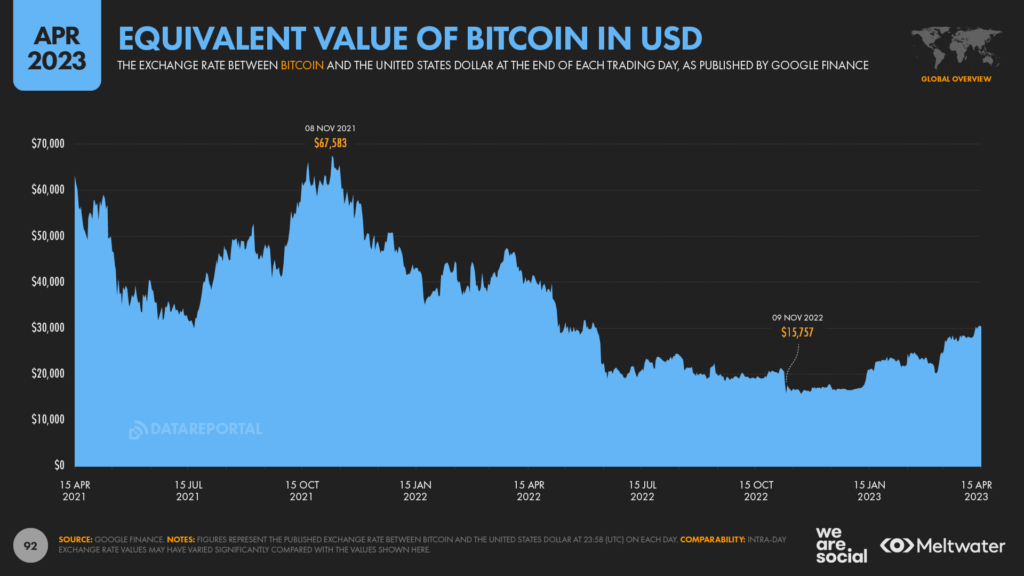

That’s perhaps not surprising when we consider that the “exchange” value of Bitcoin versus the US dollar fell by roughly two-thirds during the course of 2022.

However, in another twist to this ongoing saga, that same exchange rate rebounded by more than 70 percent in the first three months of 2023.

At the start of the year, 1 Bitcoin was worth roughly USD $16,600, but that figure had climbed to more than USD $30,000 by mid-April 2023.Given the sobering experiences of 2022, it’s unclear whether increasing valuations will encourage everyday investors back to crypto markets in 2023, but we’ll keep a close eye on GWI’s ongoing research, and bring you the latest updates to this story in our upcoming Statshot reports.

Looking ahead

As always, you’ll find loads more useful stats and trends in our complete Digital 2023 April Global Statshot Report, which you’ll find embedded in full towards the top of this article.

Alternatively, if you’d like a more “guided” tour of the latest digital trends, you might be interested in our Quarterly Digital Briefings.

Regular readers will also be pleased to hear that we’re already looking forward to our July Statshot report, when we’re hoping to explore findings from the upcoming 2023 edition of Reuters’ Digital News Report.

We’ll also have all of our usual data, insights, and analysis though, so be sure to check back here in a couple of months to explore all of the latest digital trends.

Reports

Reports