THE GLOBAL STATE OF DIGITAL IN JULY 2022 | PART TWO

Reports

Last week saw the launch of part one of our Digital 2022 July Statshot. Kepios founder Simon Kemp is back for part two of the report’s analysis, this time taking a look at soaring social media platforms and the rise of mobile gaming.

Time spent on social

There has been a lot of chatter on social media in recent weeks about the amount of time that people spend using social platforms, but – unfortunately – some of the most widely referenced data has been misrepresented.

So, to help make sense of what’s really going on, our Digital 2022 July Global Statshot Report includes two separate charts on the time spent using social media apps: one that uses data from data.ai to show average time per month, and another that uses data from Sensor Tower to show average time per day.

Apart from showing different metrics, note that these two datasets also cover different periods of user activity, so the figures on one chart won’t correlate with those on the other.

Also, for clarity, note that all of the figures in this section – from both data.ai and from Sensor Tower – represent averages for worldwide users outside of Mainland China.

Interestingly, each chart offers a slightly different take on social media behaviours, but both offer hugely valuable perspectives.

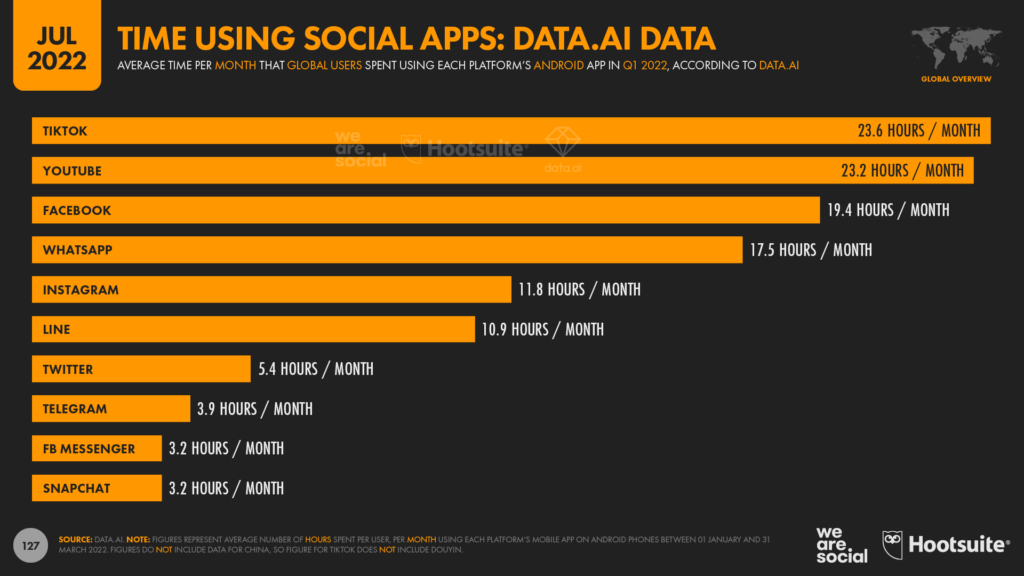

Data.ai’s analysis indicates that the average global TikTok user outside of Mainland China now spends almost a full day (23.6 hours) each month using the platform’s Android app, putting it at the top of the latest rankings.

For context, assuming that the typical person sleeps for between 7 and 8 hours per day, these latest numbers suggest that TikTok users now spend close to 5 percent of their waking hours watching TikTok videos.

YouTube isn’t far behind TikTok though, with the platform’s Android users spending an average of 23.2 hours per month using the YouTube app between January and March 2022.

However, it’s worth remembering that a considerably larger share of YouTube viewing will take place on laptop and desktop computers and connected TVs compared with TikTok.

As a result, there’s a good chance that each individual viewer still spends more time watching YouTube videos across all devices than they do watching TikTok videos. Furthermore, the latest ad reach data shows that YouTube’s adult (18+) audience is roughly 2½ times bigger than TikTok’s adult audience, so YouTube’s total, cumulative time spent is likely still more than double that of TikTok.

Indeed, this hypothesis is backed up by another set of findings from data.ai, which shows that YouTube captures the greatest amount of total, cumulative time spent by all users across all mobile apps.

But this additional context doesn’t detract from the significance of TikTok’s achievement in reaching the top of the rankings for average monthly time spent per user.

It’s also important to highlight that the time users spend in the TikTok app is still growing rapidly, whereas the time users spend in the YouTube app has actually decreased slightly over recent months.

For comparison, in our Digital 2022 Global Overview Report, we saw that users spent an average of 19.6 hours per month using TikTok’s Android app across the whole of 2021, compared with 23.7 hours per month for YouTube’s Android app users.

So, the latest figures show that TikTok’s time per user has increased by more than 20 percent in Q1 compared with full-year 2021, whereas YouTube’s time per user decreased by just over 2 percent.

Moreover, as we’ll see later in this analysis, TikTok’s audience is still growing too, while YouTube has actually revised its audience figures down since our April update (although this revision is most likely due to the effect of ongoing sanctions on Russia).

Looking beyond the top two places, it’s interesting to see that Facebook still claims third spot in the global rankings, at an average of 19.4 hours per month, per user.

But in a finding that’s more likely to worry Zuck and team, data.ai’s data shows that the average Instagram user spends exactly half the amount of time using Instagram as the average TikTok user spends using TikTok.

Instagram users still spend almost half a day per month using the platform’s Android app though, which equates to almost 2½ percent of their waking hours.

Furthermore, while differences in total user numbers mean we can’t simply add up the values for each platform, these latest figures suggest that people still spend more than 2 full days per month using Meta’s various platforms.

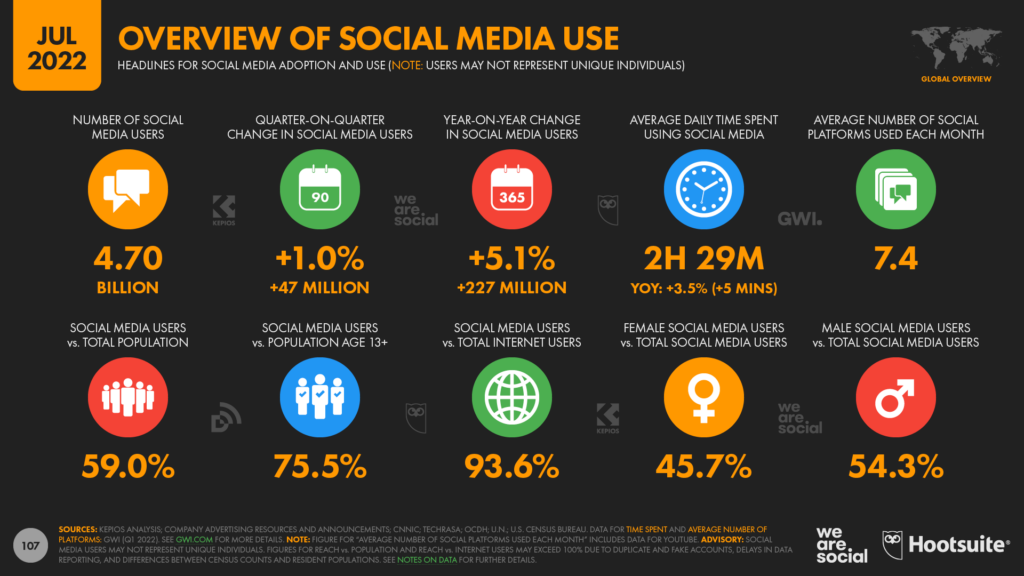

For broader context, GWI reports that the typical social media user now spends 2 hours and 29 minutes per day across all social platforms, which adds up to roughly 75½ hours per month.

That means we now spend more than 3 full days using social media each month, equating to roughly 15 percent of our waking lives.

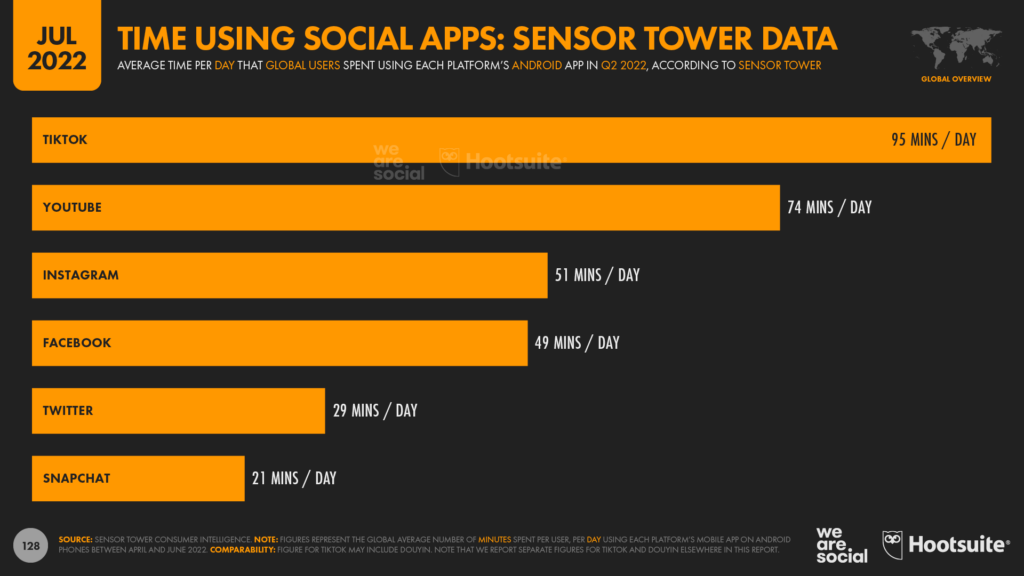

Meanwhile, Sensor Tower’s data for time spent by platform offers equally valuable insights.

The company reports that users who have the TikTok app installed on an Android phone spent an average of more than 1½ hours per day using that app between April and June 2022 – significantly more than the time spent with any other social media platform’s Android app.

This figure suggests that TikTok users now spend more than 2 days – 48 hours – per month using TikTok, which is even higher than the figure identified in data.ai’s Q1 analysis above.

For additional comparison, Sensor Tower reports that YouTube’s Android app users spent 74 minutes per day using the app during in Q2, which equates to 22 percent less time than TikTok’s Android app users spent using the TikTok app during the same period.

Instagram ranks third in Sensor Tower’s latest analysis of daily time spent, with the platform’s Android app users spending an average of 51 minutes per day using the app in Q2 2022.

But the stat in Sensor Tower’s data that’s most likely to grab headlines is that the typical Facebook user now spends roughly half the amount of time using Facebook’s Android app as the typical TikTok user spends using TikTok’s Android app.

As we’ll explore in more detail in the next section, the frequency with which people use each app may help to explain the big differences between the Facebook and Instagram findings in data.ai’s data versus Sensor Tower’s data.

On average though, Sensor Tower reports that global Facebook users now spend 49 minutes per day using Facebook’s Android app, compared with the 95 minutes that global TikTok users spend using the TikTok Android app.

However, it’s worth remembering that Facebook still has significantly more monthly active users than TikTok, so Facebook may still garner more total, cumulative time than TikTok.

Other data suggests that it may only be a matter of time before these two apps reach parity though, as we’ll explore in more detail in the next section.

TikTok ads now reach 1 billion adults each month

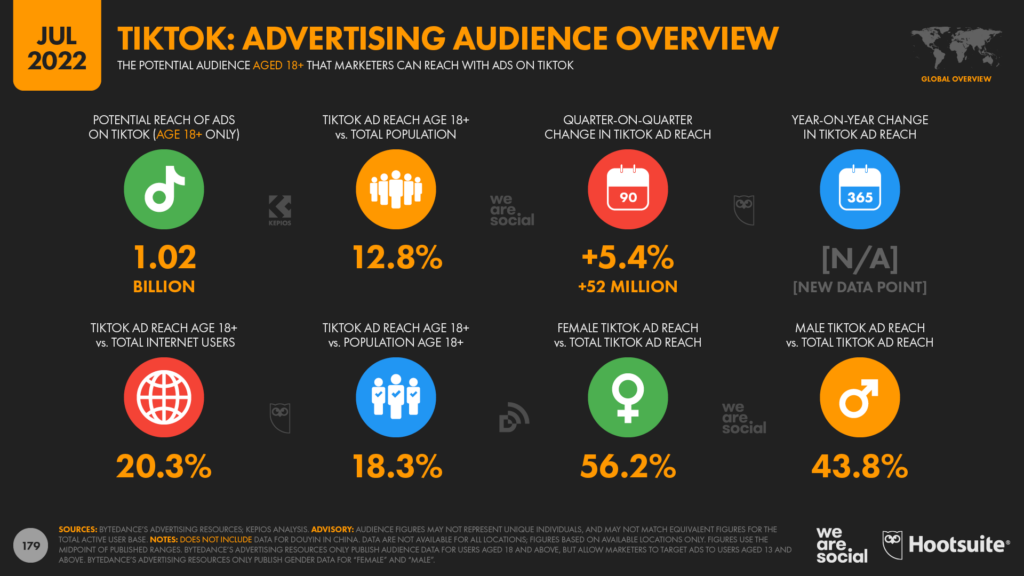

The latest numbers published in Bytedance’s advertising resources reveal that TikTok ads now reach more than 1 billion people aged 18 and above.

For context, that means that TikTok ads now reach 22.9 percent of all adults outside of China each month.

TikTok continues to add new users at an impressive rate too, with its global ad reach increasing by 52 million (+5.4 percent) over the past three months alone.

That’s slightly lower than the rate we saw in last quarter’s report, but still means that TikTok is adding more than half a million new users every day.

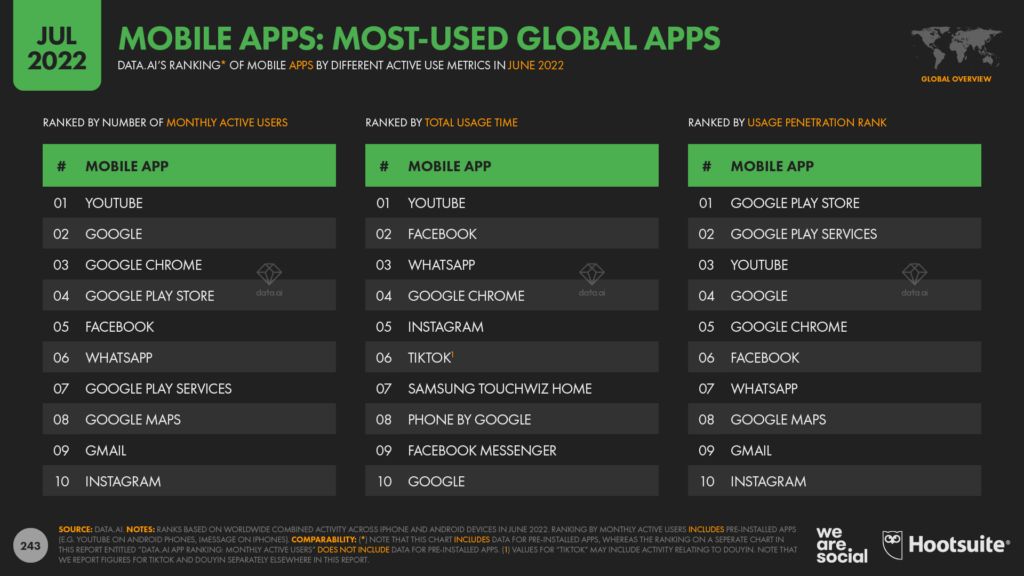

However, it is worth noting that TikTok has slipped down to third place in data.ai’s latest ranking of apps by new downloads, behind both Instagram and Facebook.

Empowering creators

But the ninth position in data.ai’s active user ranking tells what might be an even more interesting story about TikTok’s evolution.

For context, CapCut is Byetdance’s free video editing software, and the mobileapp appears to have been designed specifically to enable TikTok users to create even more compelling videos.

So, the fact that so many people appear to be using this app each month suggests that significant numbers of people are creating – or at least attempting to create – their own videos for TikTok.

And this has particular relevance when we consider TikTok’s role in people’s lives.

Critically, the more content that a user publishes to a platform, the more ‘vested’ in that platform the user is likely to become.

Moreover, when users upload more content, the platform has more content to add to its feed, giving it more opportunities to engage users – and to show advertising.

But beyond its impact on TikTok, CapCut’s growing popularity may also point to a change in people’s broader attitudes towards creativity.

As data.ai’s analysts note in their commentary on CapCut’s rise, “Its presence in the top 10 is a reflection of the democratisation of video production software. What used to be a professional skill is now a hobby and a powerful engine of the new creator economy.”

Create or consume?

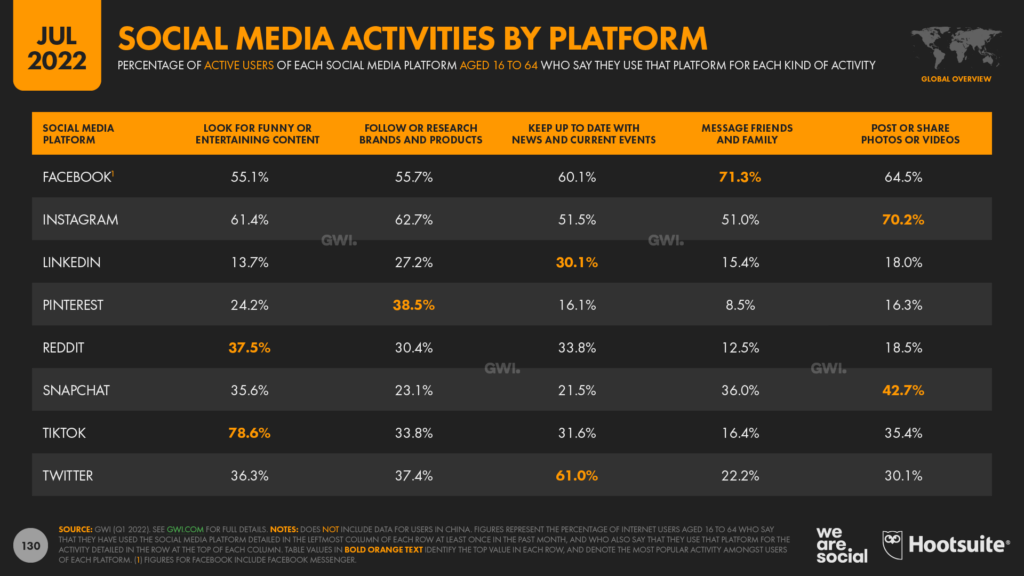

But in apparent contrast to these findings, GWI’s data reveals that consuming funny and entertaining content remains the top activity on TikTok, and just 35.4 percent of working-age adults outside of China say that they post or share their own content on the platform.

That compares with 42.7 percent of Snapchat users, 64.5 percent of Facebook users, and an impressive 70.2 percent of Instagram users.

For now though, this lower publishing ratio doesn’t appear to be much of a problem for Bytedance.

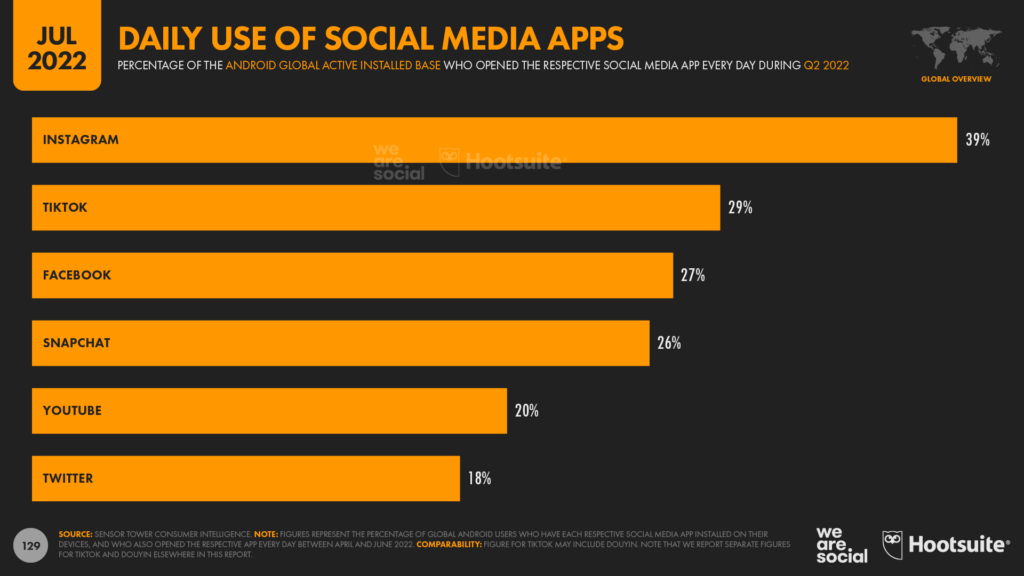

New research from Sensor Tower reveals that TikTok ranks second for frequency of use amongst social media apps, with only Instagram seeing a higher frequency of app use.

Sensor Tower’s analysis indicates that roughly 3 in 10 TikTok users who use the platform’s Android app opened the app every single day between April and June 2022.

This compares with roughly 4 in 10 Instagram users who open Instagram each day, while the figure for Facebook was 27 percent.

Meanwhile, given TikTok’s focus on entertaining videos, it’s particularly interesting to note that just 1 in 5 YouTube users open the app every day.

However, it’s worth remembering that many people will consume YouTube videos via computers and connected TVs as well as via the platform’s mobile apps, whereas TikTok use is more likely to occur within the platform’s mobile apps.

No, Facebook isn’t dead

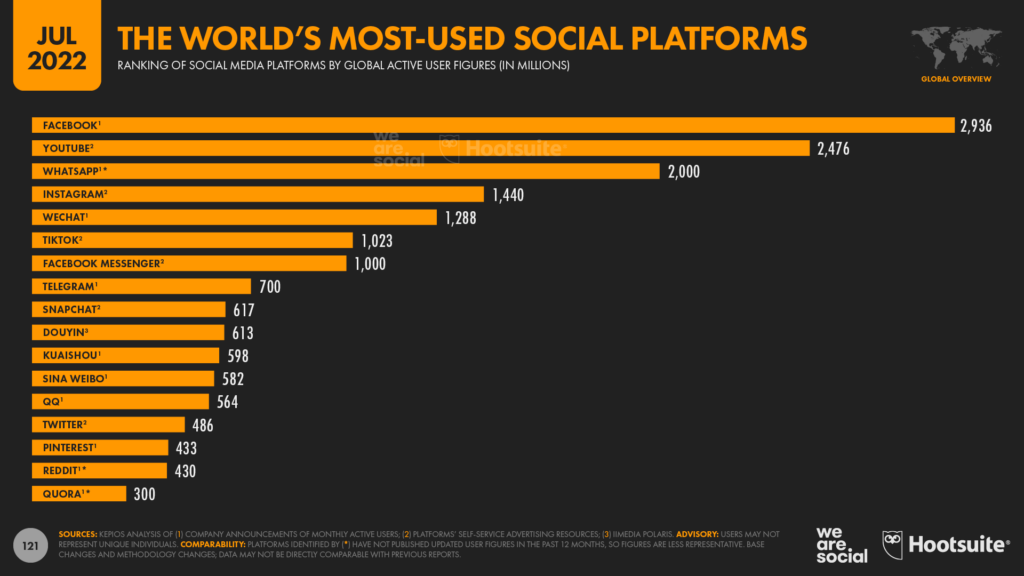

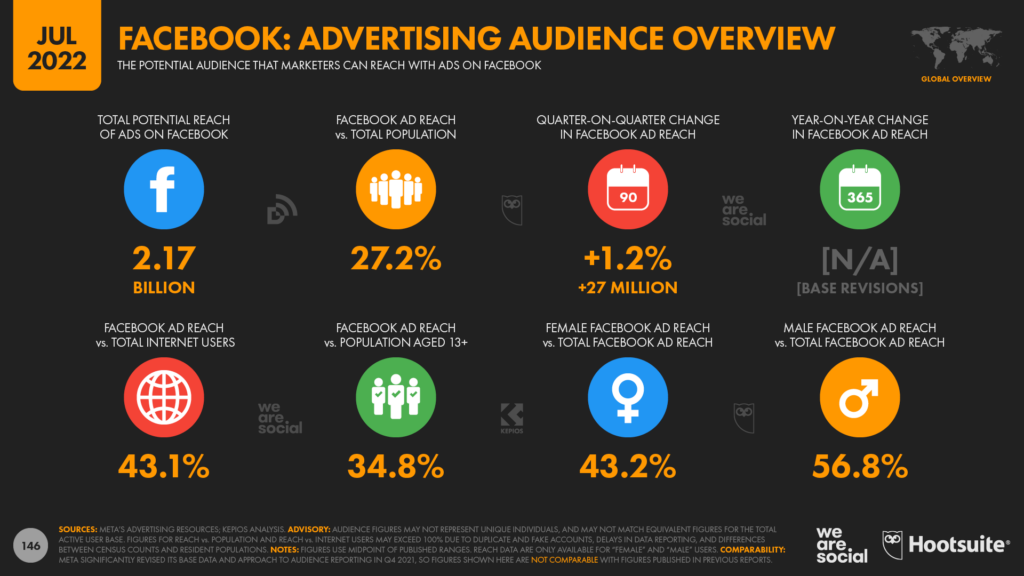

Despite perennial media headlines foretelling the demise of Facebook, Meta’s latest ad-reach data show that tales of Facebook’s death continue to be very much exaggerated. The company’s own resources reveal that global Facebook ad reach actually increased by 1.2 percent between April and June, taking the platform’s total global advertising audience to 2.17 billion.

The platform’s total user base continues to grow too, with the company’s Q1 2022 investor earnings update reporting quarter-on-quarter growth in monthly active users (MAUs) of 0.8 percent [click here to learn why we report different numbers for Facebook’s ad reach and MAUs].

Furthermore, once we factor Facebook’s age limitations and the fact that the platform remains ostensibly ‘blocked’ in Mainland China, Facebook’s latest MAU figures indicate that almost 6 in 10 people (58.6 percent) on Earth who can use Facebook already do.

A mysterious myth

Given these impressive figures, it’s unclear why some media outlets continue to misrepresent the state of Facebook’s health.

Such misrepresentation isn’t a new phenomenon, either; news headlines have been telling us that “Facebook is dying” for well over a decade.

Indeed, a New York Times headline proclaimed a “Facebook Exodus” as early as August 2009, when the platform had fewer than 350 million users.

Facebook’s user base has grown eightfold since then, equating to almost 2.6 billion additional users.

So, my tip would be to wait until Zuck himself says it’s over before you pay too much heed to click-bait.

Compare and contrast

However, there is more to this story than these headline figures suggest.

For starters, Facebook’s recent growth rates are nowhere near as impressive as those of TikTok, whose ad audience has grown over four times faster than Facebook’s audience over the past three months.

But while there’s no denying TikTok’s rapid ascent, it’s also important to put the platform’s growth figures in context.

Just before we do that, it’s worth noting that Bytedance’s advertising tools only report ad reach data for audiences aged 18 and above, so – in order to provide a balanced comparison – we’ll focus on the same cohort for Facebook.

Bytedance also operates a separate platform for Mainland China (Douyin), and while Facebook is technically still blocked in the country, it still reports some nominal ad reach in China, so we’ve removed Facebook’s Mainland Chinese users from the following analysis.

With those caveats in mind, data published in each respective platform’s tools show that:

Facebook ads reach 2.04 billion users aged 18 and above outside of Mainland China in July 2022

TikTok ads reach 1.02 billion users aged 18 and above outside of Mainland China in July 2022

It’s worth acknowledging that TikTok may well have more users below the age of 18 than Facebook does, but because Bytedance’s tools don’t publish audience reach data for users below the age of 18, it’s difficult to know for sure.

Either way though, the big takeaway for marketers here is that Facebook ads still reach twice as many adults as TikTok ads do.

Moreover, if both platforms were to sustain their current growth rates – which is unrealistic for both platforms, but especially so for TikTok given the speed of its current ascent – the data suggest that TikTok’s ad reach wouldn’t catch up with Facebook’s reach for at least another 4 years.

The measures that matter

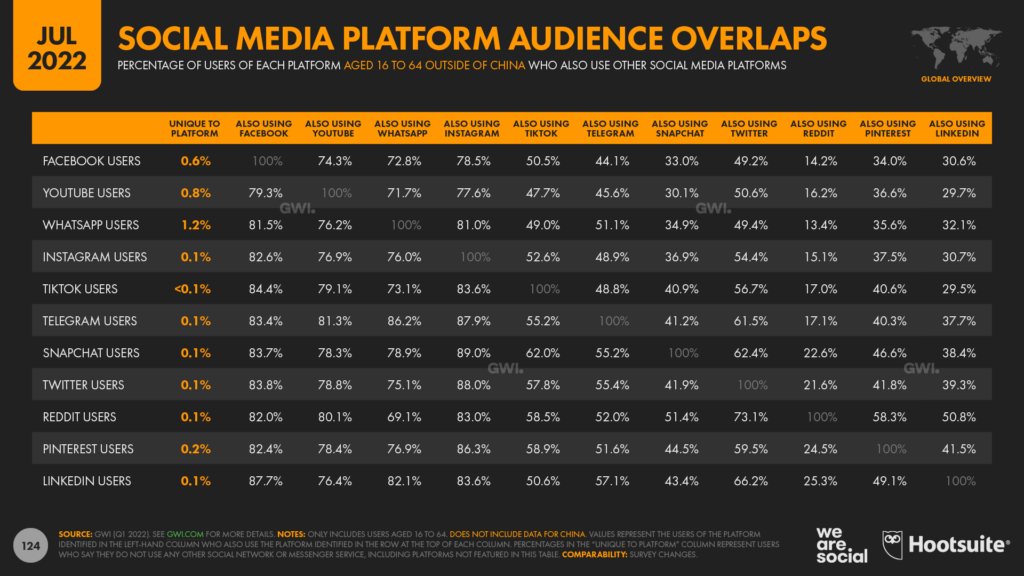

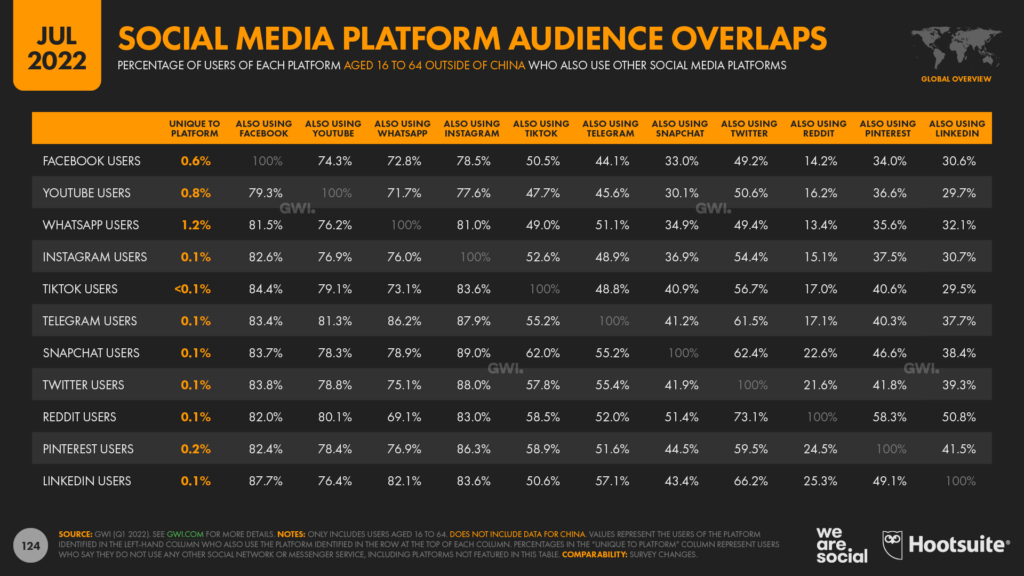

But perhaps the most important finding when comparing these two platforms is that most social media users outside of Mainland China now use both Facebook and TikTok – and many other platforms as well.

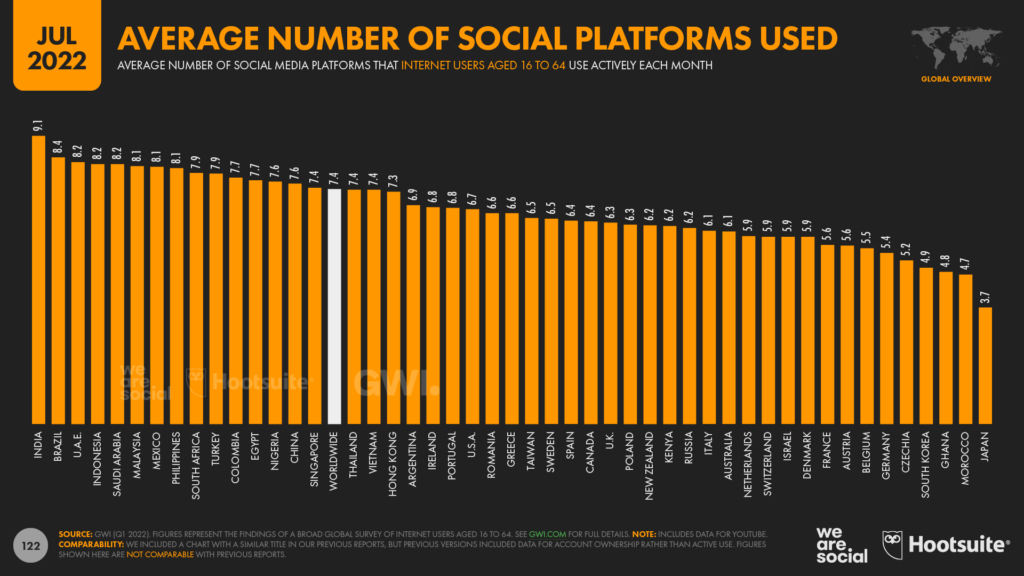

Indeed, the “typical” global social media user now makes active use of almost 7½ social media platforms every month.

Moreover, GWI’s data shows that a hefty 84 percent of TikTok users still use Facebook, while less than 0.05 percent of TikTok users – i.e. fewer than 5 in every 10,000 – surveyed by GWI said that they don’t use any other social platform.

Meanwhile, just over half of all working-age Facebook users also use TikTok – a finding that aligns closely with the various figures that we explored above.

So, perhaps it’s time for marketers to stop pitting these platforms against each other.

Yes, there is still competition for people’s time and attention, and the more of these valuable resources that a platform can attract, the greater that platform’s potential for generating revenue.

However, that consideration likely has more bearing for investors than it does for marketers, especially because marketers should only pay for advertising when their content is actually shown to their chosen audiences.

Sure, marketers still need to decide how to allocate their budgets between different social platforms, but all of the figures above indicate that user numbers alone are a poor basis for that allocation.

So, if you’re looking for some more representative metrics on which to base those allocation decisions, I’d recommend:

Cost per outcome: how much money would you have to spend on each platform to reach your audience and – critically – to achieve your desired objectives? Given that we can now reach almost all of the users of any given social media platform on at least one other social platform, it’s well worth exploring which platforms offer the most cost-efficient opportunities to reach your target audience and deliver your desired outcomes.

Creative opportunities: different platforms offer different media formats, each with their own advantages and limitations. Because of this, it’s well worth exploring which creative formats might offer the most effective and engaging ways of delivering your brand’s message, well before you start thinking about which platform(s) you’ll use to deliver that content.

Usage context and motivations: our audiences use different platforms for different reasons, and they’re likely to be in different settings, mindsets, and emotional states when they use each platform too. Where and when will your brand’s message have the greatest resonance in your audience’s life, and which platforms are most likely to align with those contexts?

And no, the kids aren’t all leaving Facebook either

Continuing a story I touched on in last quarter’s analysis, our July 2022 data may help to dispel another common misconception about Facebook’s current momentum.

Contrary to yet more click-bait mischief, audience reach data do not support the claim that “the kids are leaving Facebook”.

In fact, Facebook’s latest global ad-reach numbers show that teenage audiences are still growing, with the platform adding 1.35 million users between the ages of 13 and 19 between April and June 2022.

For reference, that equates to quarter-on-quarter growth of 0.6 percent.

Sure, that’s nothing like as impressive as the growth we’d expect to see amongst this demographic on a platform like TikTok, but it’s still growth.

In other words, on a net-change basis, the kids are still joining Facebook – not leaving it. It is worth acknowledging that teens now represent a smaller percentage share of Facebook’s total audience, but that’s largely because the number of users in older age groups – especially the over-50s – has increased more quickly in recent months than teenage users have.

For context, in July 2019, Facebook ads reached roughly 115 million Facebook users between the ages of 13 to 17, accounting for 5.9 percent of Facebook’s total ad audience.

At that time, Facebook reported ad reach of 194 million users aged 55 and above, who accounted for 10 percent of the platform’s total audience.

Three years later – in July 2022 – Facebook ad reach amongst 13 to 17s has grown to almost 121 million, but this demographic’s share of Facebook’s total ad reach has slipped to 5.6 percent.

This is partly because Facebook ads now reach 262 million users aged 55 and above, with this demographic now accounting for 12.1 percent of the platform’s total ad reach.

Figures vs. feelings

But looking beyond absolute user numbers, there’s little denying that Facebook’s role in teens’ lives has declined considerably since the heady days of the early 2010s.

For example, GWI reports that Facebook now ranks just fifth amongst the “favourite” social media platforms of women aged 16 to 24, although Zuck and team will be relieved to hear that Instagram is still well out in front for this particular demographic.

Interestingly, Facebook fares better amongst Gen Z males, although the platform still ranks below Instagram and WhatsApp.

However, Facebook is still the “favourite” choice for Millennial males, just ahead of WhatsApp.

Another salient finding in this data is that 48.6 percent of all global social media users – including those in China – still choose one of Meta’s platforms as their “favourite”.

What’s more, if we remove those users in Mainland China – where all of Meta’s platforms remain blocked – roughly two-thirds of social media users identify either WhatsApp, Facebook, Instagram, or Messenger as their favourite platform.

And critically, Meta’s platforms still dominate amongst younger users too.

At a global level (including China), 45.9 percent of female social media users aged 16 to 24 identify one of the company’s four platforms as their favourite, while more than half (51.3 percent) of their male peers do the same.

And if we remove users in Mainland China, those figures rise to 60.6 percent for female social media users aged 16 to 24, and 65.7 percent for male users in the same age group.

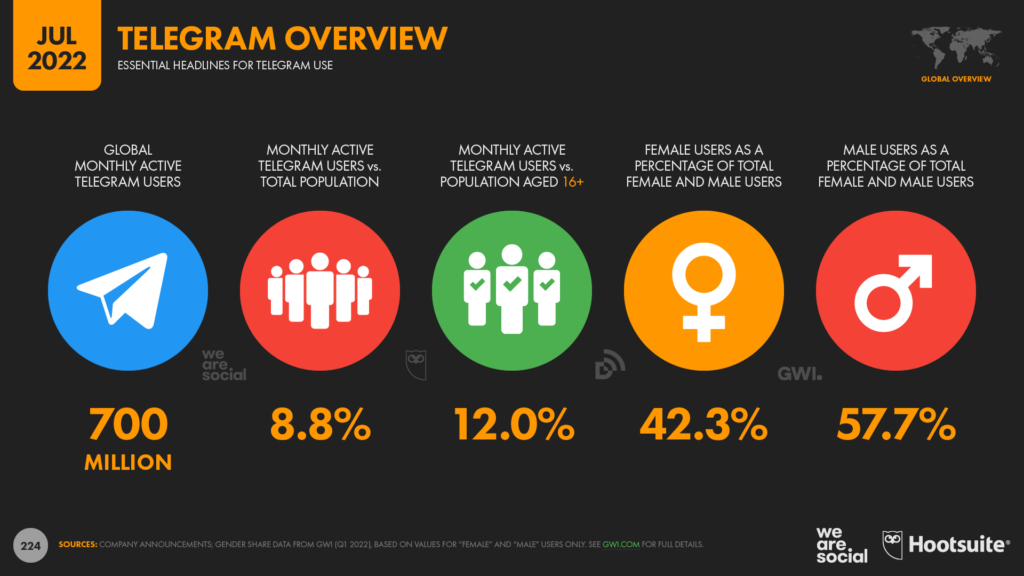

Telegram soars

A recent company blog post reveals that Telegram now has more than 700 million monthly active users, suggesting that that platform has added roughly 200 million active users in just the past 18 months.

The exact dates of the platform’s user milestones remain unclear, but this latest figure suggests that Telegram’s active user base is currently growing at an annualised rate of roughly 25 percent, or close to 6 percent per quarter.

That means Telegram may be growing even faster than TikTok, whose adult ad audience increased by 5.4 percent over the past 90 days.

Telegram’s impressive trajectory isn’t just evident in its own data, either.

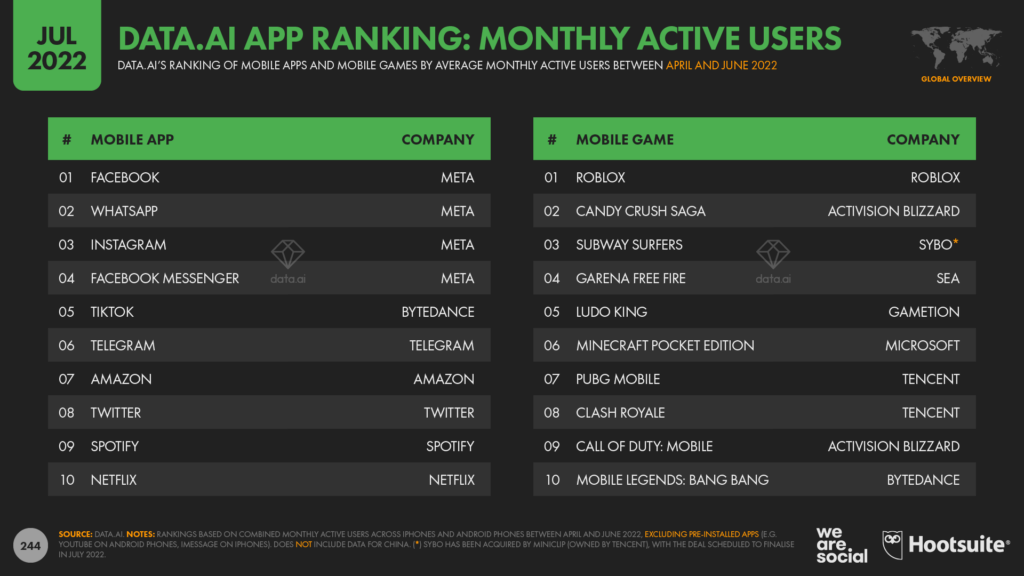

Data.ai’s latest ranking of mobile apps by monthly active users puts Telegram in sixth place – behind TikTok, but ahead of Amazon and Twitter.

Meanwhile, data.ai’s latest ranking of “breakout” apps shows that Telegram ranks second in terms of quarter-on-quarter growth in monthly active users – ahead of all other social media platforms, including TikTok.

Telegram’s app continues to attract new users too, with Sensor Tower reporting 28 million combined worldwide downloads across the Google Play Store and iOS App Store in June 2022 alone.

That’s not quite as high as some of its peers, although download numbers can be misleading.

For context, Sensor Tower’s data suggests that TikTok saw 52 million new downloads across its TikTok, TikTok Lite, and Douyin apps in June 2022, while Instagram attracted 58 million new downloads across Instagram and Instagram Lite during the same period.

However, it’s unclear how many of these new downloads represent actual ‘new’ users, as opposed to existing users simply downloading the app onto a new device.

Moreover, it’s difficult to predict how many of the truly ‘new’ downloads will convert into regular, active users of each platform, so I’d advise caution when interpreting app download figures.

Snapchat jumps too

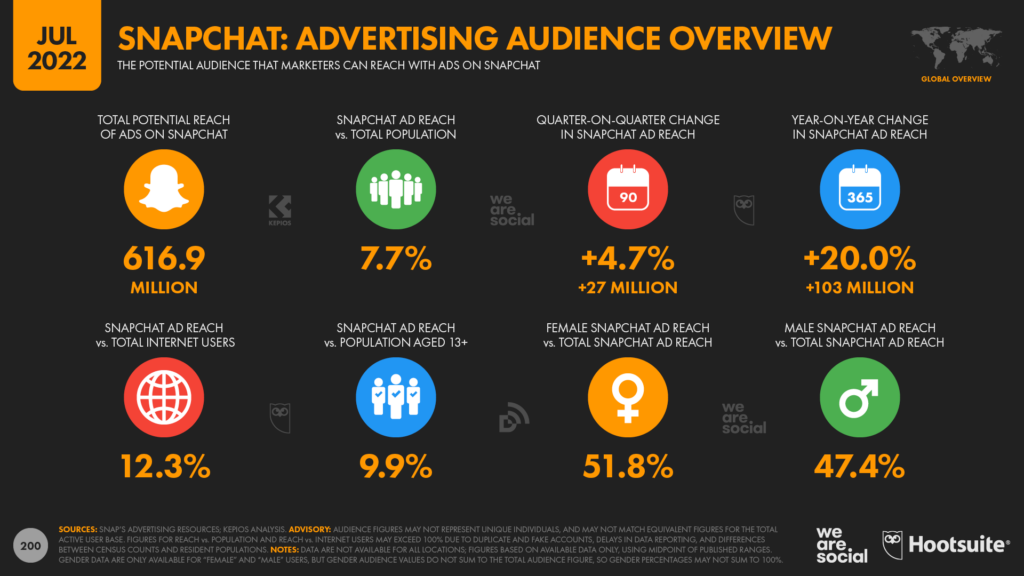

Meanwhile, Snapchat’s latest numbers are almost as impressive as Telegram’s.

According to data published in the company’s own tools, Snapchat’s ad audience has grown by more than 100 million users since this time last year, equating to annual growth of 20 percent.

Snapchat ads now reach almost 617 million users around the world each month, which equates to roughly 10 percent of the ‘eligible’ global audience aged 13 and above.

Snapchat is particularly popular across the Middle East, as well as in countries across Northern and Western Europe.

The rise of Reels

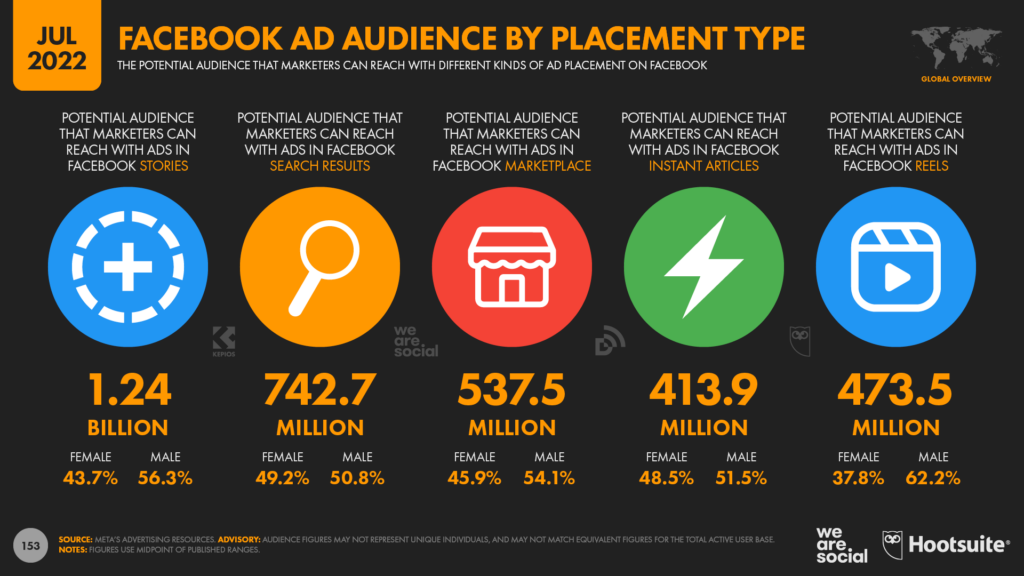

Data published in Meta’s advertising resources indicate that Reels ads have reached a significantly greater number of users over the past 30 days than they did just three months ago.

For reference, in April 2022, Meta reported that ads in Facebook Reels reached 125.0 million users around the world, while ads in Instagram Reels reached 686.9 million users.

Just 90 days later, however, those figures look quite different.

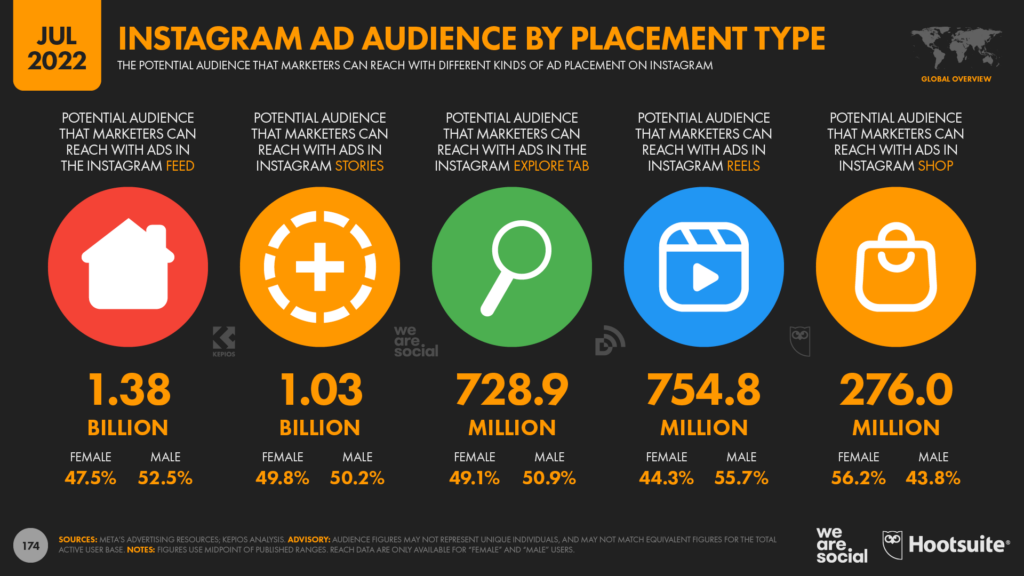

Meta’s tools show that ads in Facebook Reels can now reach 473.5 million users, while ads in Instagram Reels can reach 754.8 million users.

For comparison, that means the Facebook Reels ad audience has grown by almost 350 million users over the past 3 months – a hefty 279 percent increase.

The growth figures for Instagram Reels are somewhat less dramatic, but the format’s audience has still grown by 68 million users (+9.9 percent) since April 2022.

A risk of cannibalisation?

However, the growth of Facebook Reels may have come at the expense of some of the platform’s other ad placements.

For example, Meta’s own data suggests that the number of users seeing ads in Facebook Instant Articles has dropped by 8.4 percent over the past quarter, while the number of users who have been shown ads in Marketplace has fallen by almost 5 percent since April.

But this shift may actually be part of Meta’s plan.

For context, in a recent investor earnings call, Mark Zuckerberg clearly stated that Meta intends to prioritise activities that keep people within Meta’s platform environments:

“We started by building world class ads tools to help businesses reach potential customers and help people discover new products and services that they might like. But what we’ve found is that when [Shops and Marketplace] ads link offsite, you often land on a webpage that’s not personalised or not optimised, or where you have to re-enter your payment information. That’s not a good experience for people, and it doesn’t lead to the best results for businesses either. So our next phase is focused on building out Shops, Marketplace, and business messaging in WhatsApp and Messenger to create more native commerce experiences across our apps.”

This may mean that Meta will start to place less emphasis on ads in Facebook Marketplace and Instagram Shop that direct users to third-party sites, in favour of creating more “on-platform” social commerce offerings.

Despite this potential shift in focus, however, the ad reach of Instagram’s Shop tab still jumped over the past 90 days.

276 million Instagram users were served ads in Shop during June 2022, compared with 197.4 million in March 2022, equating to an impressive quarter-on-quarter growth rate of almost 40 percent.

The demographics of Reels

Returning to Reels, it’s interesting to note that male users tend to over-index in the ad audiences of these formats.

Overall, 47.2 percent of Instagram’s ad audience is female, while 52.8 percent is male.

However, if we focus on the ad audience of Instagram Reels, the imbalance becomes more apparent: 44.3 percent female vs. 55.7 male.

Similarly, while Facebook’s overall ad audience is currently 43.3 percent female and 56.8 percent male, the Facebook Reels audience tilts to 37.8 percent female vs. 62.2 percent male.

Our analysis suggests that this may be because Indian users significantly over-index in the audiences of both formats. For context, India has one of the most significant gender imbalances in the world when it comes to social media use, and men account for a whopping three-quarters of the country’s ad audience across Facebook and Instagram.

Meanwhile, Indian users account for roughly a quarter of the worldwide ad audience for both Facebook Reels and Instagram Reels in July 2022, so the country’s local gender skew will likely play a disproportionate role in shaping the worldwide gender profile of Reels audiences too.

Messengers are the medium

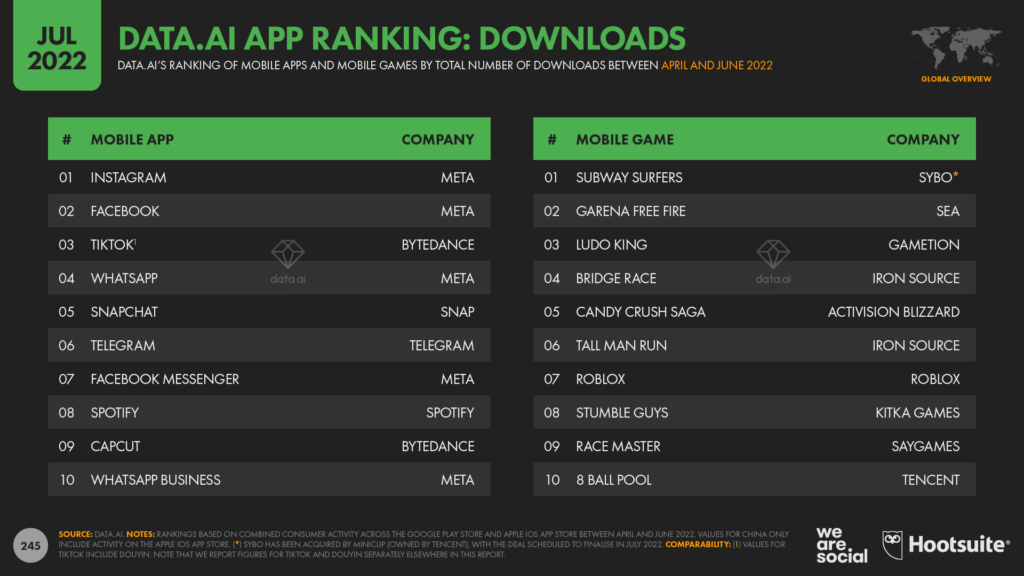

In addition to the impressive growth in Telegram users that we explored earlier in this article, there’s more good news for messaging platforms in this quarter’s data too.The latest insights from data.ai show that WhatsApp Business was one of the 10 most-downloaded mobile apps between April and June 2022, moving up three places versus its ranking in Q1.

This impressive result demonstrates that Meta’s efforts to earn revenue from WhatsApp may be starting to pay off – eight years after the company paid USD $21.8 billion to acquire it.

Furthermore, evidence of this trend isn’t restricted to data.ai’s research.

At its inaugural “Conversations” messaging conference in May, Meta reported that:

“One billion people message with a business each week on WhatsApp, Messenger and Instagram Direct – whether it’s DMing brands, browsing product catalogues, asking for support, or interacting with stories.”

These figures indicate that messaging apps represent a growing opportunity for social media companies and for brands, and we expect to see an increase in messenger-related marketing activities around the world over the coming months.

Mobile gaming levels up

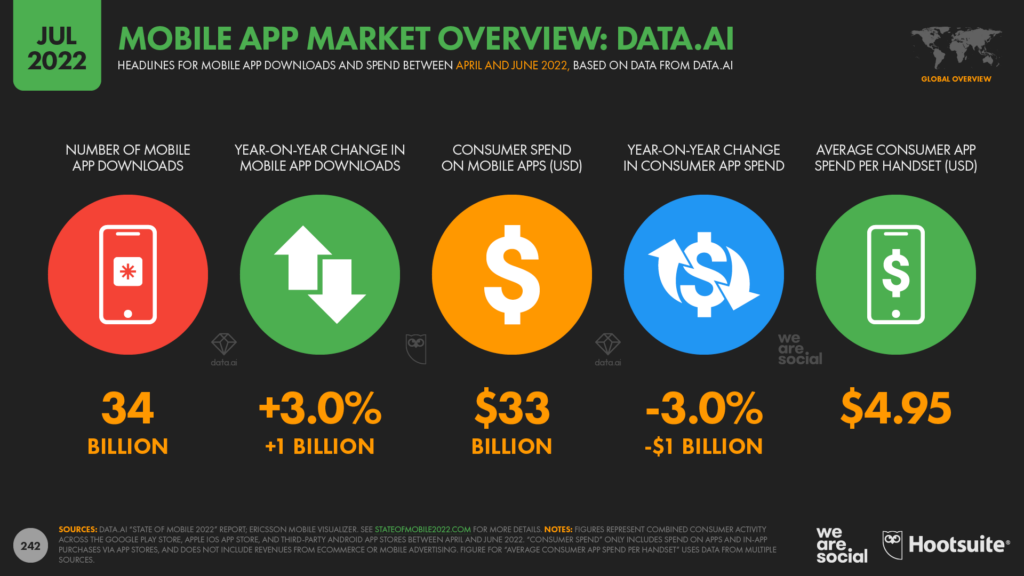

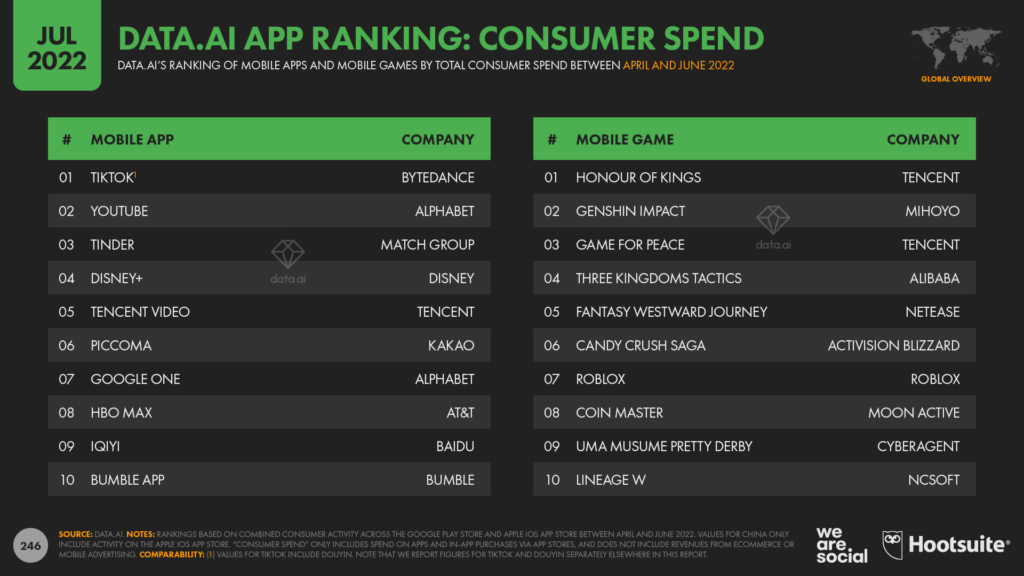

Research from data.ai shows that mobile titles are now responsible for 60 percent of worldwide consumer spend on video games.

The company forecasts that mobile games will generate a total of USD $136 billion in revenue in full-year 2022, compared with USD $42 billion for console games, and $40 billion for PC and Mac titles.

Games also account for the lion’s share of consumer spend across the iOS App Store and Google Play Store:

“Games are set to account for 65 cents of every $1 spent in the twostores in Q2 2022, [contributing] 72 percent of consumer spend on Google Play, and 62 percent on the iOS store.”

In total, gamers spent USD $21.5 billion on mobile games and in-app game purchases in these two stores between April and June 2022, which is 30 percent more than the amount they spent in the equivalent pre-pandemic quarter of Q2 2019.

Spending levels vary considerably by mobile operating system though, and data.ai reports that iOS users typically spend considerably more on mobile games than their Android peers, despite Android accounting for the vast majority of smartphone handsets in use today.

iPhone users accounted for roughly 62 percent of mobile game spending in Q2 2022, with game-related purchases in the iOS App Store reaching USD $13.3 billion, compared with USD $8 billion in the Google Play store.

For context, data.ai reports that consumer spend on mobile apps totalled USD $33 billion across all app categories between April and June 2022.

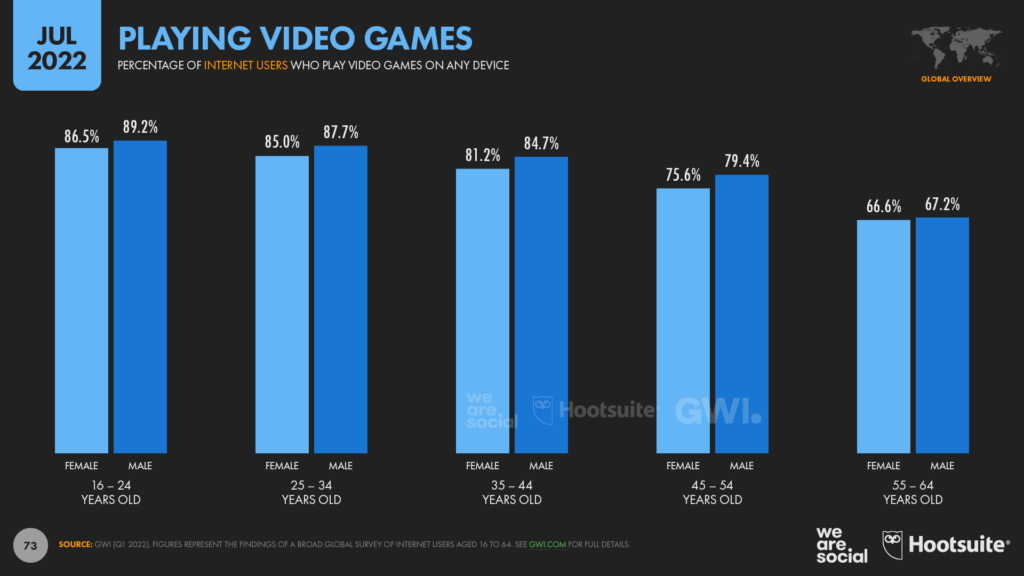

Meanwhile, a report co-published by data.ai and IDC reveals that gaming is now a multi-generational opportunity, with engagement and spend on mobile games increasing amongst older age groups.

The report’s authors note that retirees in particular may represent a particularly appealing gaming opportunity, thanks to higher levels of disposable income, as well as potentially more free time to play games.

GWI’s research adds valuable context to these findings, with the company’s latest data revealing that roughly two-thirds of Baby Boomers already play video games.

The evolving app economy

Beyond games, mobile users have been spending an increasing amount of money on other kinds of apps.

Indeed, Sensor Tower reports that spending in non-game apps has now overtaken spending on mobile games amongst mobile users in the USA.

But it’s particularly interesting to see where this money is being spent.

As we reported in detail in last quarter’s analysis, TikTok accounts for the largest share of consumers’ spend on mobile apps, eclipsing even the top mobile games.

Other video apps attract high levels of consumer spend too, with data.ai placing another 5 video apps – YouTube, Disney+, Tencent Video, HBO Max, and iQiyi – in the top 10 apps by global consumer spend.

Dating apps also generate significant revenues, with Tinder and Bumble both making the global top 10 by consumer spend.

But data.ai’s analysis reveals that people are spending an increasing amount of money in other mobile app categories too.

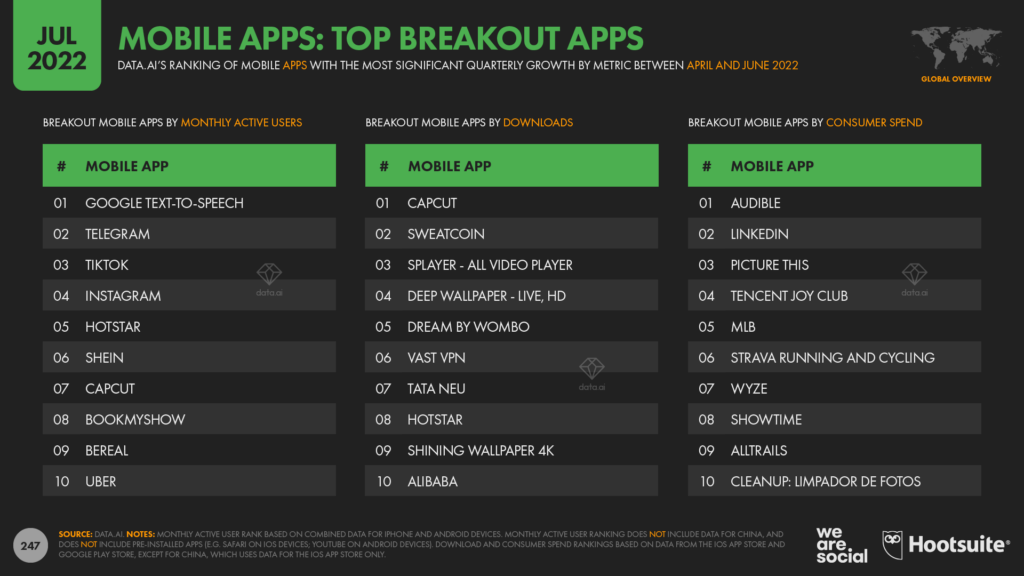

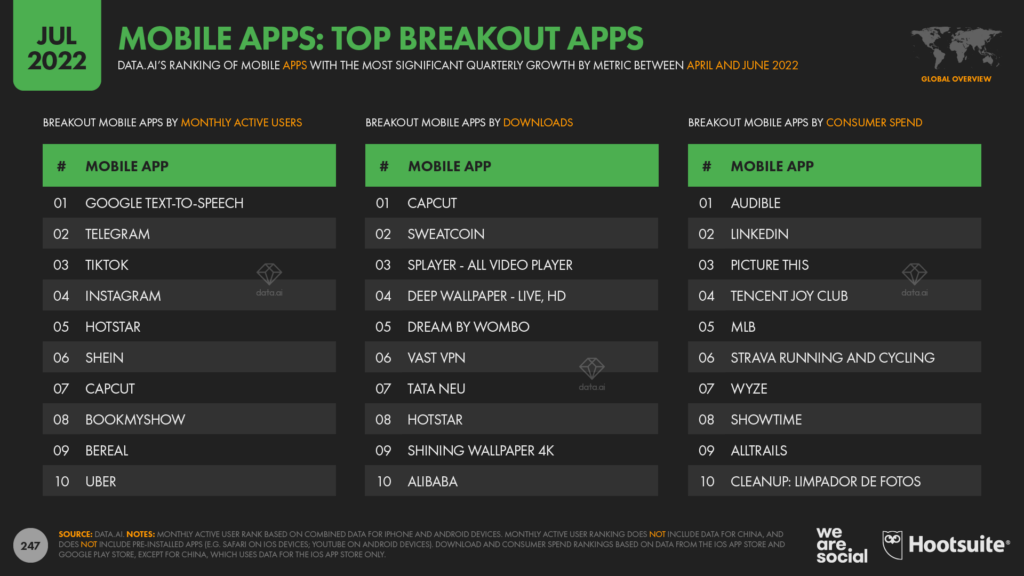

Audio books claim one of the standout stories this quarter, with Amazon’s Audible app delivering the largest quarter-on-quarter growth in consumer spend of any mobile app over the past three months.

Data.ai’s “breakout apps” ranking also shows that there has been a significant increase in the amount of money that end users spend within LinkedIn’s mobile app.

Sadly, the data doesn’t reveal what users are spending this money on, but with LinkedIn advertising already earning meaningful revenue for Microsoft, this increase in consumer spend only goes to consolidate the value of its LinkedIn acquisition.

Meanwhile, people have been spending more money on apps to help them enjoy the great outdoors too, with both Strava and AllTrails seeing a meaningful increase in consumer spend during the course of Q2.

The rise of smart wrists

GWI’s ongoing survey of internet users around the world reveals strong growth in the adoption of smartwatches and smart wristbands over recent months.

Data shows that ownership of smartwatches like the Apple Watch has jumped by more than 60 percent over the past 2 years, while ownership of smart wristbands like the Fitbit has climbed by more than 35 percent during the same period.

For perspective, these latest numbers indicate that roughly 800 million adults now own at least one of these devices.

That means that working-age internet users are now 40 percent more likely to own a “smart wrist” device than they are to own a games console, and nearly twice as many people own one of these wearables as own a TV streaming device like an Apple TV.

Wrapping up

That’s all for this quarter’s analysis, but we’ve already started to research the more forward-looking trends that we’ll share as part of our next Statshot report, so be sure to visit DataReportal for that update towards the end of October.

In the meantime, if you’d like some help making sense of what the latest trends might mean for your 2023 plans, you might be interested in our private briefings, which dig deeper into the stories and context behind all of these numbers, and identify the key implications for marketers.

We’ll also be publishing the latest country-level audience data for a selection of the world’s top social media platforms in a couple of weeks’ time, so head over to our dedicated social media pages for those updates starting in mid-August.

Join us tomorrow over on LinkedIn Live as Simon Kemp and our Global Head of Media Brittany Wickerson take a deep dive into the key headlines featured in the report at 9am (BST).

Reports

Reports