Our latest Global Digital Report is packed with milestones, trends, and our biggest ever collection of data. Here, Kepios founder Simon Kemp takes us through the key headlines featured in Digital 2024.

2024 has only just started, but it’s already shaping up to be a bumper year for digital milestones.

Our huge new Digital 2024 Global Overview Report – published in partnership between We Are Social and Meltwater – reveals a wealth of impressive headlines and trends, including:

A momentous new figure for social media use

An increase in the time we spend online

A change in the world’s “favourite” social media platform

The intensifying rivalry between Instagram and TikTok

A decline in TV viewership

Compelling new milestones for Linkedin, Snapchat, and Weibo

Insights into global digital ad spend

Some truly staggering figures for TikTok hashtags

…and loads more data, insights, and surprises too.

The ultimate collection of digital data

And it’s not just user numbers that have grown this year, either.

At more than 550 pages, this is by far the most detailed Global Overview Report that we’ve ever published, and that’s all thanks to the support and generosity of our wonderful data partners:

There are a few things you should be aware of before you start exploring this latest round of data:

We’ve made significant changes to the way we report social media user identities in individual countries since last year’s report. The good news is that we’ve been able to rebase most of our data for previous periods, so we’re still able to report accurate data for change over time. However, comparisons with social media user figures published in previous reports will deliver inaccurate results, so please use the change values we’ve published in this year’s reports, and don’t try to calculate change values using data from previous reports.

Source corrections to a variety of data points – especially for internet users – may result in figures that look quite different to those we published last year. However, these new numbers rely on the most recent data, and are therefore the most representative and reliable figures.

We continue to see incongruous trends in the data published in the ad tools of various social platforms. We’ll explore some of these anomalies in our full analysis below, but please exercise caution when analysing trends in social media audience data, especially for X (Twitter) and TikTok.

We’ve changed how we collect data for TikTok, so our most recent global figures are not comparable with previous reports. However, the good news is that the data we can report now covers many more countries.

There have been some important changes in the category classifications in our ecommerce datasets, which means the data in this year’s reports is not comparable with seemingly similar data points published in previous years.

Top 10 Takeaways

Need fast insights? This executive summary video delivers the top ten takeaways from this year’s report in just ten minutes:

The complete Digital 2024 Global Overview Report

You’ll find this year’s complete report in the embed below (click here if that’s not working for you), but read on past that to explore my in-depth analysis of what all these numbers actually mean.

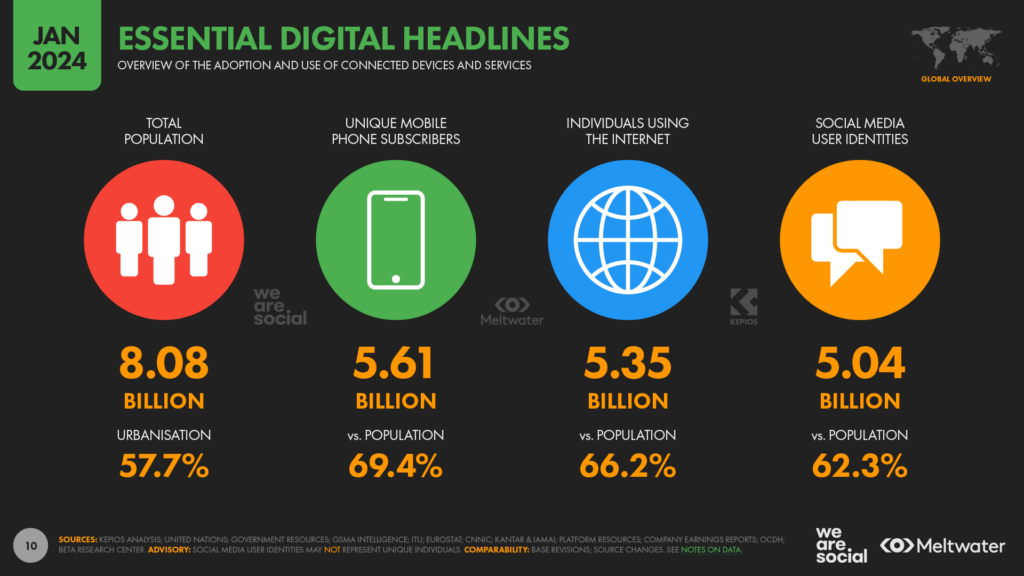

The state of digital in January 2024

Let’s begin with the latest headlines for digital adoption and use around the world:

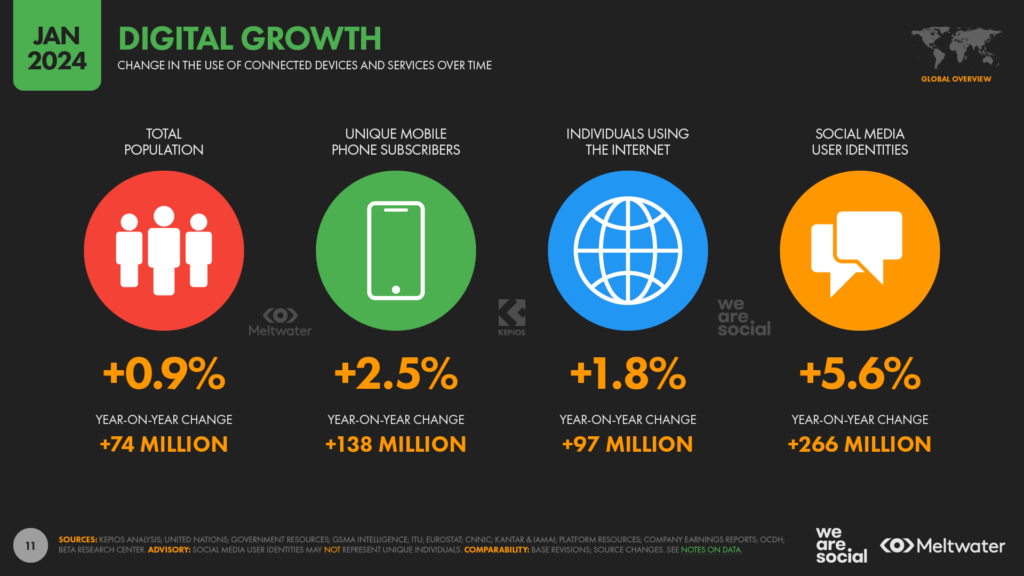

Data from the United Nations World Population Prospects shows that there are now 8.08 billion people living on Earth. The global population has increased by 74 million people since this time last year, equating to year-on-year growth of 0.9 percent.

The number of unique mobile phone users sits at 5.61 billion at the start of 2024. The latest data from GSMA Intelligence reveals that 69.4 percent of the world’s total population now uses a mobile device, with the global total up by 138 million (+2.5 percent) since early 2023.

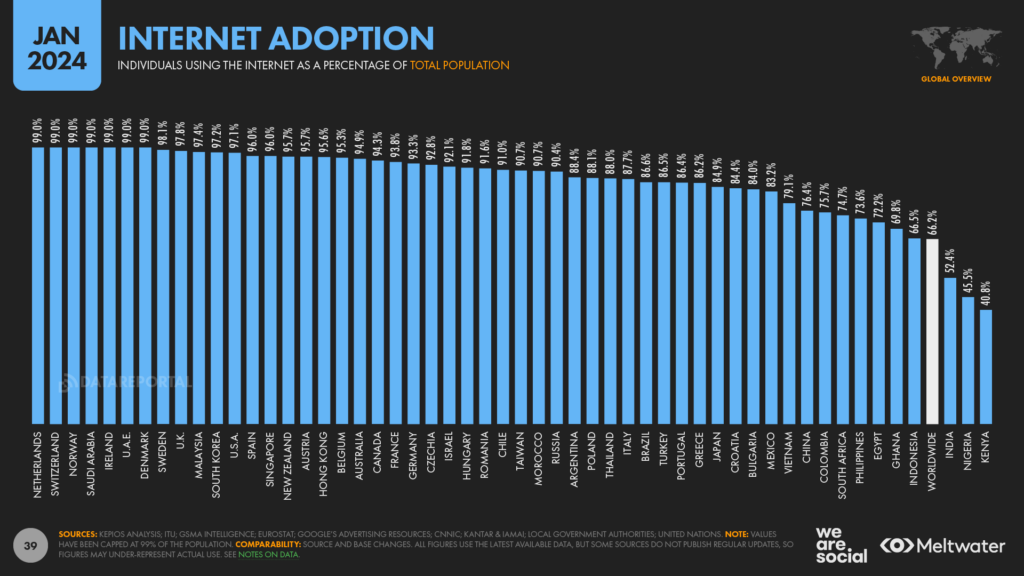

More than 66 percent of all the people on Earth now use the internet, with the latest data putting the global user total at 5.35 billion. Internet users have grown by 1.8 percent over the past 12 months, thanks to 97 million new users since the start of 2023.

Kepios analysis shows that active social media user identities have passed the 5 billion mark, with the latest user figure equivalent to 62.3 percent of the world’s population [note: social media user identities may not represent unique individuals]. The global total has increased by 266 million over the past year, resulting in annual growth of 5.6 percent.

That’s a great snapshot for your social media posts (feel free to copy-paste!), but what can we learn from this year’s bumper collection of data?

Well, the simple answer is “a lot”, so make sure you’re sitting comfortably, and we’ll begin our comprehensive analysis of these Digital 2024 numbers.

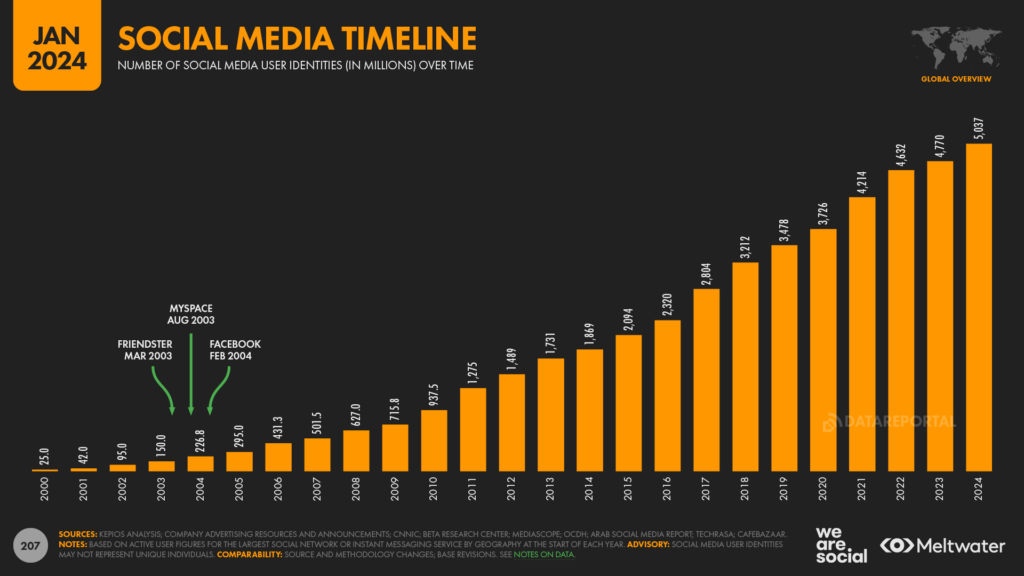

5 billion social media user identities

The top story in this year’s report is that there are now more than 5 billion active social media user identities, with the global total reaching 5.04 billion at the start of 2024.

This huge new social media milestone comes just ahead of Facebook’s twentieth birthday on February 4th, but it’s worth stressing that social media’s history started well before Mark Zuckerberg launched TheFacebook.com from his Harvard dorm room back in 2004.

Indeed, social media’s journey to 5 billion users started more than 50 years ago.

▶ Dig deeper: Explore the complete history of social media – including all the key platforms and milestones – in this special deep dive article.

Social media use continues to grow

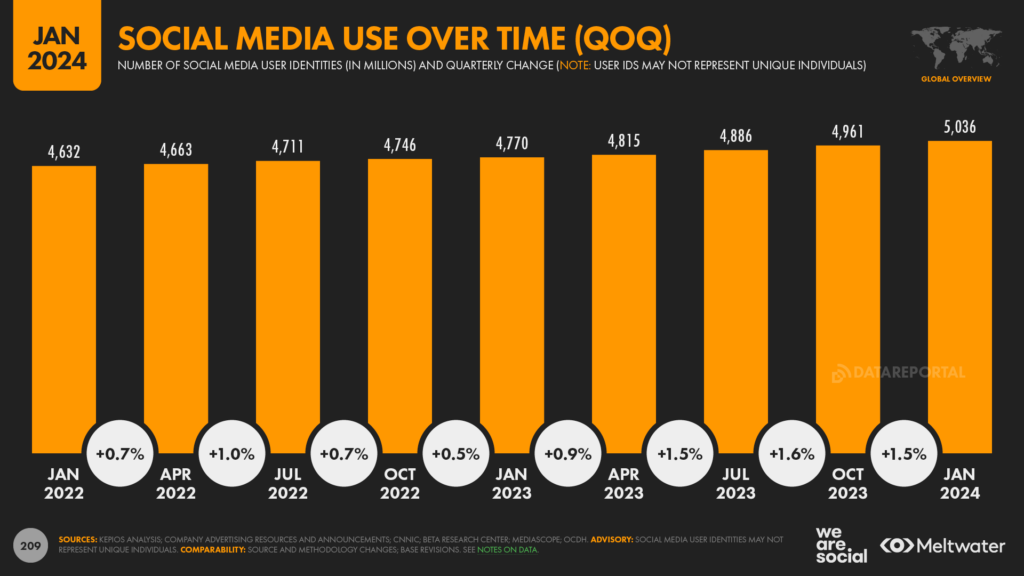

Our latest social media user identities figure has increased by 5.6 percent over the past year, with 266 million new users starting to use social media for the first time over the course of 2023.

This impressive figure means that the world averaged 8.4 new social media users per second over the past year.

What’s more, that adoption rate actually accelerated further in the last three months of 2023, with Kepios analysis putting the average for the last three months of the year at 9.4 new users every second.

Because the same person may manage more than one “user identity”, our 5.04 billion figure doesn’t represent unique individuals, but our analysis indicates that the number of people using social media shouldn’t be massively different from this user identities total.

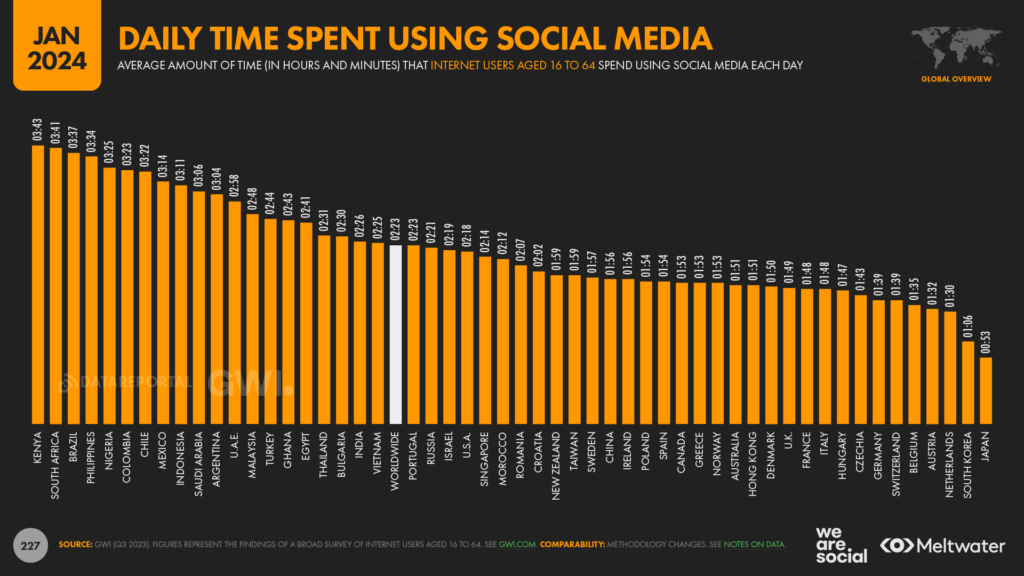

Time spent using social media

But the impressive figures aren’t restricted to user numbers.

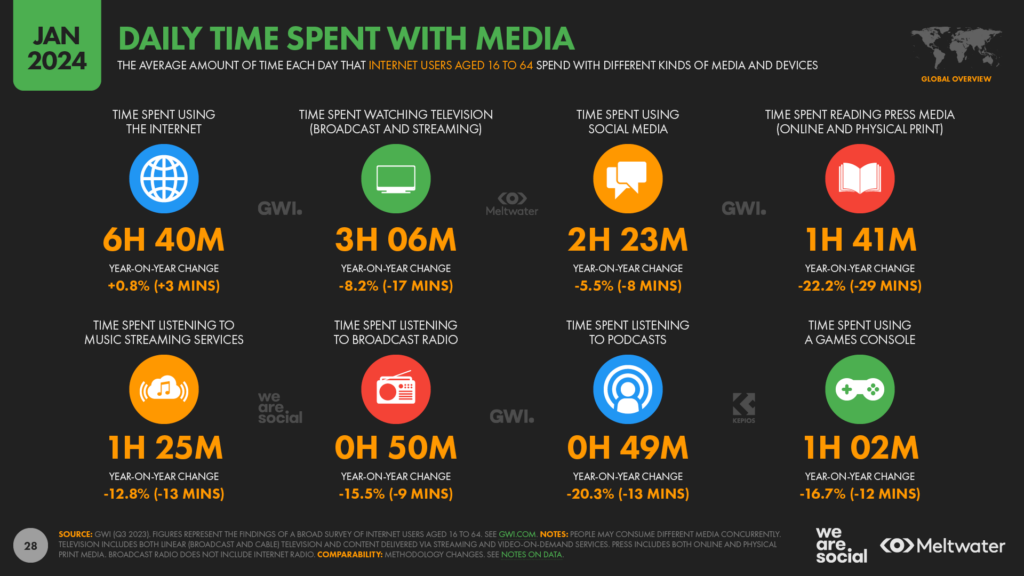

The world spends a huge amount of time using social media too, with the latest research from GWI revealing that the “typical” social media user now spends 2 hours and 23 minutes per day using social media.

That average is 8 minutes per day lower than the one we reported this time last year, but our analysis of the data suggests that a change in GWI’s methodology may be the key factor here, rather than an actual change in user behaviour.

Either way though, these latest figures suggest that humanity will spend a combined total of 500 million years using social media in 2024.

That average is 8 minutes per day lower than the one we reported this time last year, but even then, these latest figures suggest that humanity will spend a combined total of 500 million years using social media in 2024.

▶ Dig deeper: If you’d like to learn more about the time we spend on social media – including how much time we spend on individual platforms – check out our deep-dive article.

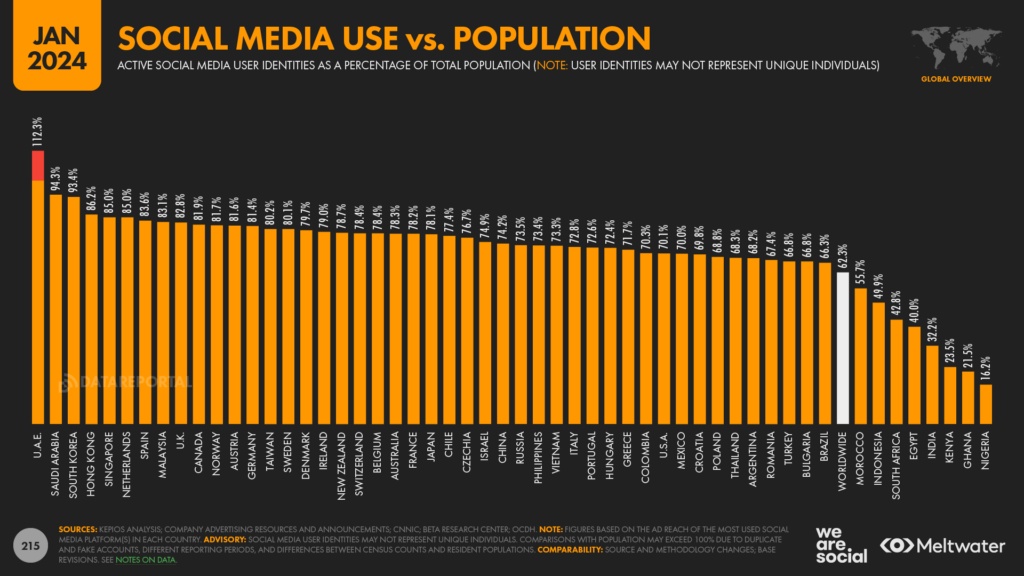

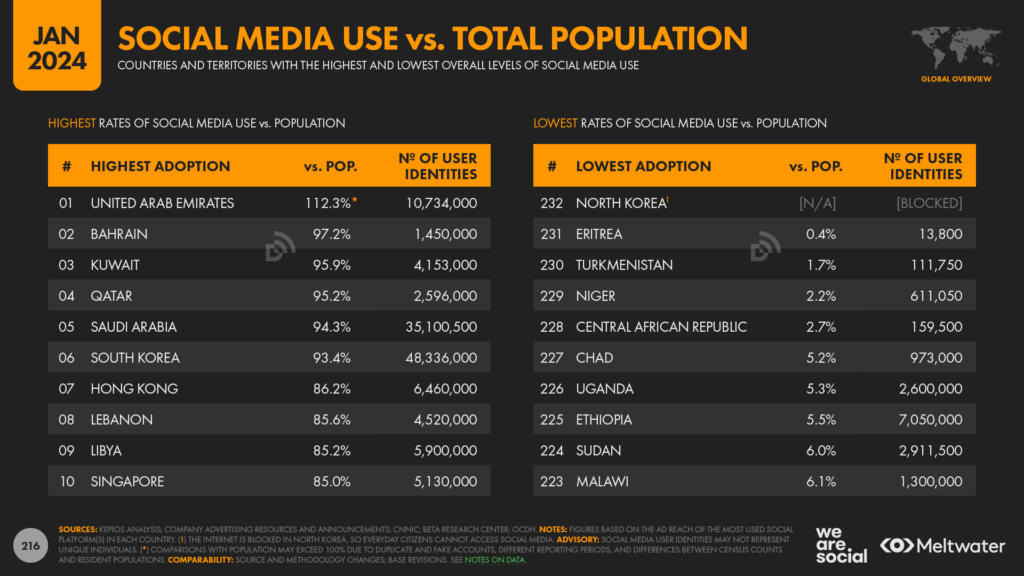

Social media use by country

However, social media adoption and use still vary meaningfully by country.

Countries along the western edge of the Persian Gulf see the highest ratios of social media users to population, although this may be partly because some of these countries are home to large expat communities that are not fully represented in “official” population data.

This phenomenon may also help to explain why some countries in the region have social media adoption figures that appear to exceed figures for population and internet use, although it’s difficult to know whether this is the only cause of these anomalies.

Either way though, the latest data indicate that social media user identities in the United Arab Emirates equate to 112.3 percent of the country’s population.

This figure may seem implausible, but it’s unclear whether this anomaly is caused by social media user identities being artificially inflated by duplicate and “false” accounts, or whether population figures simply under-report the total number of people currently living or working in the country

As a result, we’ve chosen to report these ratios “as is”, so that readers can form their own conclusions.

Bahrain, Kuwait, Qatar, and Saudi Arabia also see particularly elevated levels of social media adoption, with South Korea the first non-Gulf country in our latest ranking.

At the other end of the spectrum, North Korea still suffers from the lowest levels of social media adoption in the world, with the country’s government continuing to impose a total digital blockade that prevents the country’s citizens from accessing the internet.

The governments of Eritrea and Turkmenistan have also imposed tight restrictions on social media use, which explains the markedly low levels of social media adoption in these countries.

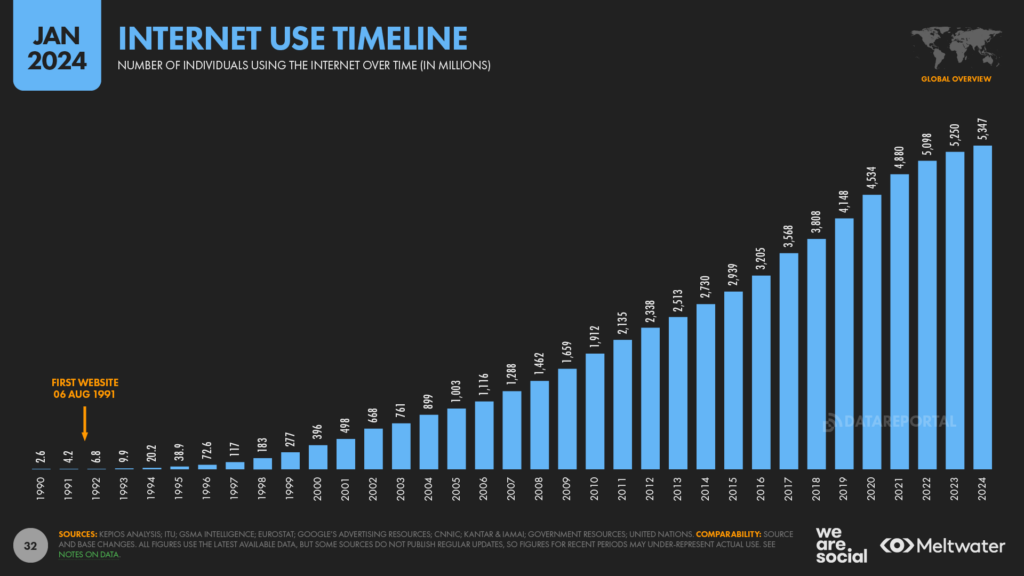

Internet growth continues

The latest data indicate that internet adoption continued to grow in 2023, albeit at a slightly slower pace than we saw in recent years.

However, because internet users are rapidly approaching “supermajority” status – when two-thirds of the world’s population will be online – this deceleration of growth is to be expected, because there is an ever-smaller number of people who remain offline.

Our analysis of the latest data from the ITU, GSMA Intelligence, Eurostat, and various local government bodies indicate that internet users grew by 1.8 percent over the past 12 months, with 97 million new users taking the global total to 5.35 billion at the start of 2024.

However, as we note each year, the complexity of collecting and reporting internet user numbers mean that many countries are yet to publish their most recent numbers, and as a result, our latest figures likely underestimate the actual total, and growth rates for recent months.

For perspective, our latest internet user growth rate is very close to the one that we reported this time last year, but new data published during the course of 2023 indicates that annual growth between 2022 and 2023 was actually closer to 3 percent.

And as a result, we expect that real internet user growth between 2023 and 2024 is higher than the 1.8 percent that the available data currently suggest.

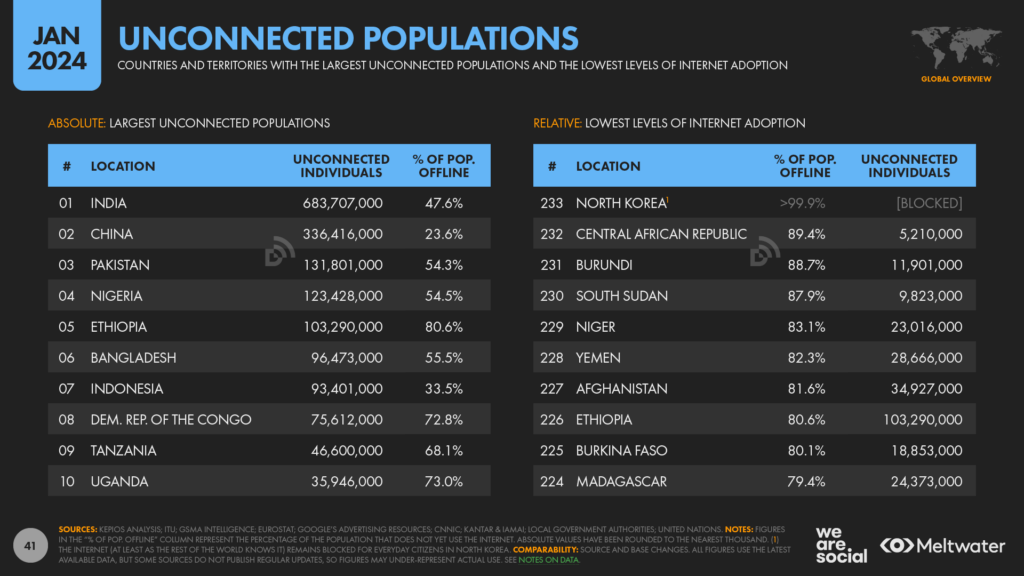

More than 1 in 3 still offline

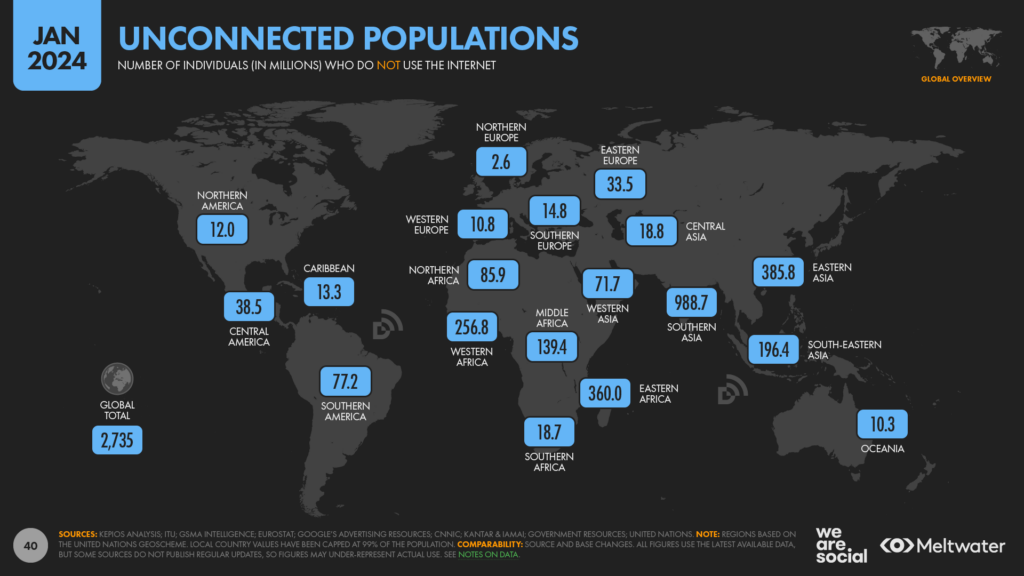

But despite these impressive figures, more than 2.7 billion people remain offline around the world, with India alone home to more than 680 million of the world’s “unconnected”.

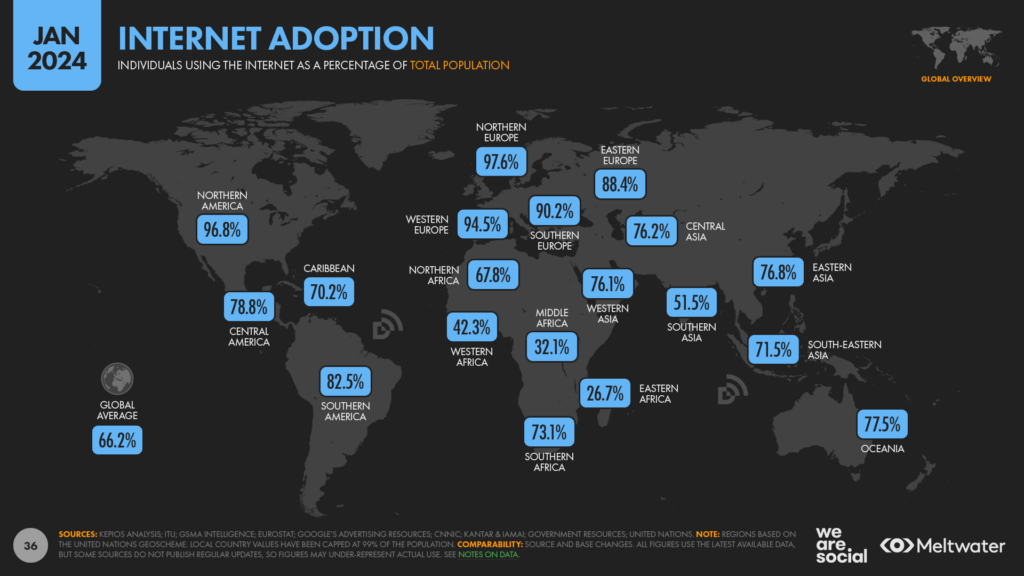

In more encouraging news, the latest data show that internet penetration now exceeds 25 percent in all of the world’s regions, and only central Africa continues to struggle with adoption rates below 50 percent.

As we’ll explore in more detail later in this article, rising internet adoption in India has helped push penetration above 50 percent across Southern Asia this year, but individual country figures tell a more complex story.

As we’ve already seen, North Korea’s total digital blockade means the country continues to languish at the bottom of the internet adoption rankings for yet another year.

African countries account for seven of the bottom ten, with the Central African Republic only just passing 10 percent adoption.

In all, a total of nine countries still contend with internet penetration rates below 20 percent, while 54 countries and territories out of a total of 233 for which we have data suffer from internet penetration rates below 50 percent.

▶ Dig deeper: there’s a lot more nuance to “the unconnected”, especially when it comes to causes and potential remedies. Click here to read our comprehensive analysis of all the latest data and trends.

Connected time creeps back up

This time last year, one of our top stories was that people were spending less time using the internet.

At the time, average daily internet use had declined by 5 percent year on year, and we wondered whether this might signal a fundamental change in how people use connected tech.

However, our latest data reveals that this trend has actually reversed.

Let’s start by exploring overall internet time.

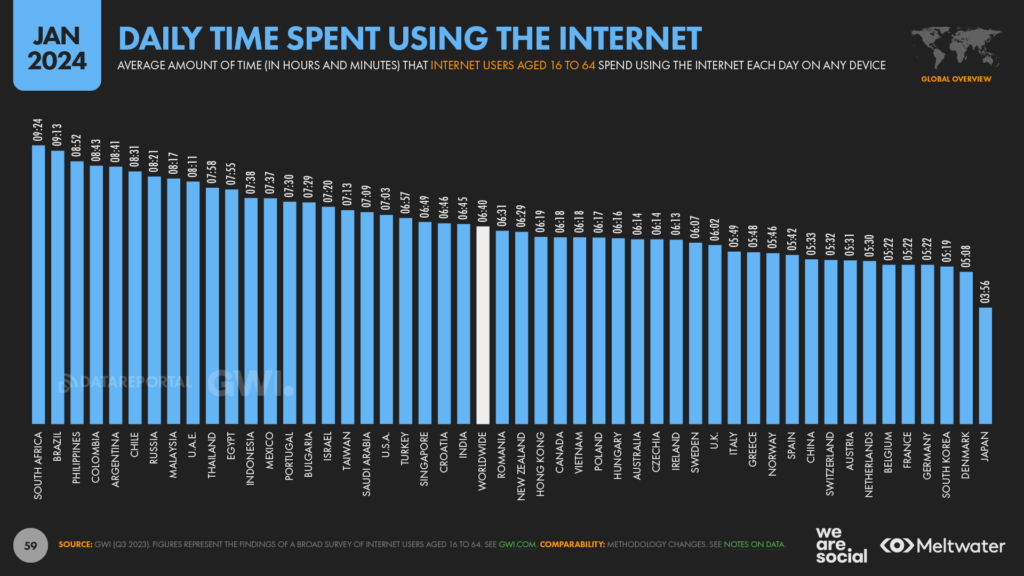

The time we spend online

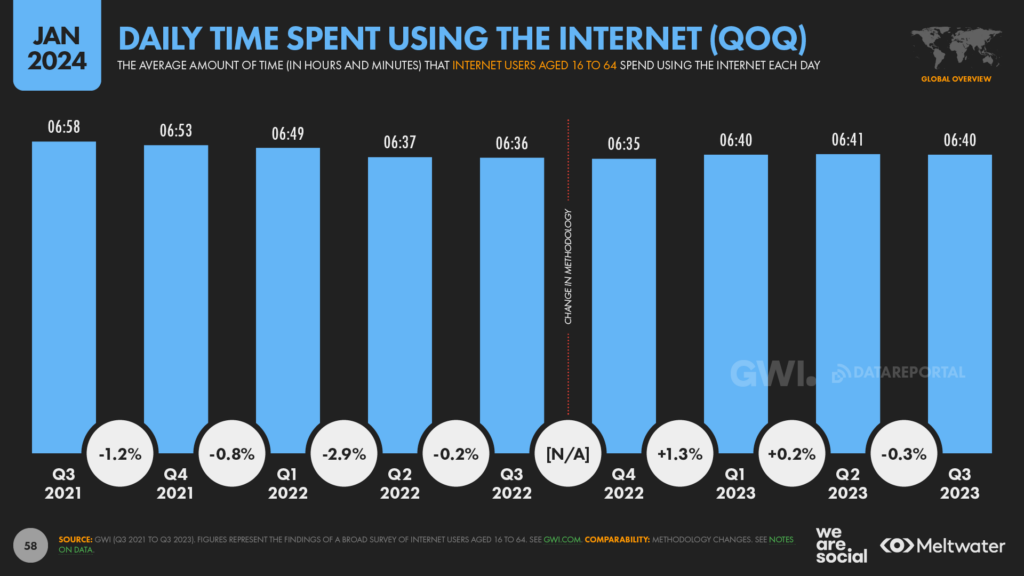

Ongoing research from GWI shows that the typical internet user now spends 6 hours and 40 minutes online each day.

That’s up by almost 1 percent compared with this time last year, when internet users reported spending an average of 6 hours and 36 minutes per day using connected tech [note: time values on the chart have been rounded from more granular data, so while the difference looks like 4 minutes, it’s actually closer to 3 minutes].

It’s important to highlight that revisions to GWI’s methodology over the past year may have affected this change figure, but the fact that these values have remained relatively stable over the past five quarters suggests that this change figure is still representative.

At an average of 400 minutes per user, per day, the world will spend a combined total of 780 trillion minutes using this internet this year, which equates to almost 1.5 billion years of collective human existence.

However, averages vary significantly by geography.

Time online by country

At the upper end of the scale, South Africans still spend the greatest amount of time online, with the typical user in the country reporting that they spend an average of 9 hours and 24 minutes per day using the internet.

If we assume that the average person spends between 7 and 8 hours per day sleeping, that figure suggests that the internet now accounts for close to 60 percent of waking hours amongst South Africa’s connected population.

For perspective, internet adoption in South Africa currently stands at close to 75 percent.

Brazilians rank second by daily online time, with the country’s netizens spending an average of 9 hours and 13 minutes per day using the internet.

And Filipinos close out the top 3, with the typical user in the South-East Asian archipelago spending 8 hours and 52 minutes per day online.

However, it’s a very different story at the other end of the spectrum.

Japanese people say they spend an average of less than 4 hours per day using the internet, which is over an hour a day less than any other nation in GWI’s survey.

Meanwhile, Denmark sits second-to-bottom, with Danes saying they’re online for an average of just 5 hours and 8 minutes per day.

And South Koreans rank third-last, with users spending an average of 5 hours and 19 minutes per day using the internet.

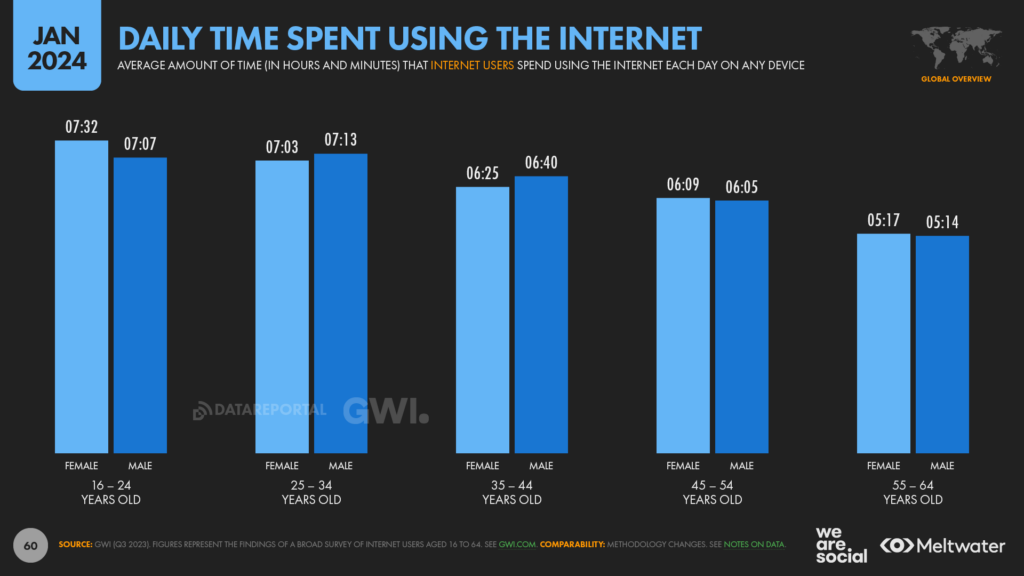

Time online by age

It’s always interesting to explore the reasons why there’s so much disparity in these numbers, but after many years of analysis, I still haven’t found a definitive reason that explains the differences.

In general though, the older the population, the less time the country spends online, because older people tend to spend less time using the internet compared with younger generations.

However, Portugal offers a clear contradiction to this “rule”.

The West-European nation has one of the oldest populations in the world, and yet the country’s internet users also say they spend an average of 7½ hours per day online, which is considerably higher than the global average of 6 hours and 40 minutes.

Culture undoubtedly plays an important role in shaping these averages too, but “culture” is too nebulous a concept to enable objective comparisons between countries.

However, the good news is that we don’t necessarily need to understand the causes of these differences in order to understand their impact.

GWI’s data enables us to see how connected activities vary by geography, age and gender, and that should be more than enough insight for us to build an accurate picture of online time.

▶ Dig deeper: explore how connectivity and online time vary by device in our comprehensive analysis of all the latest data.

But what are people actually doing in their 400 online minutes?

Once again, the story here is one of variety.

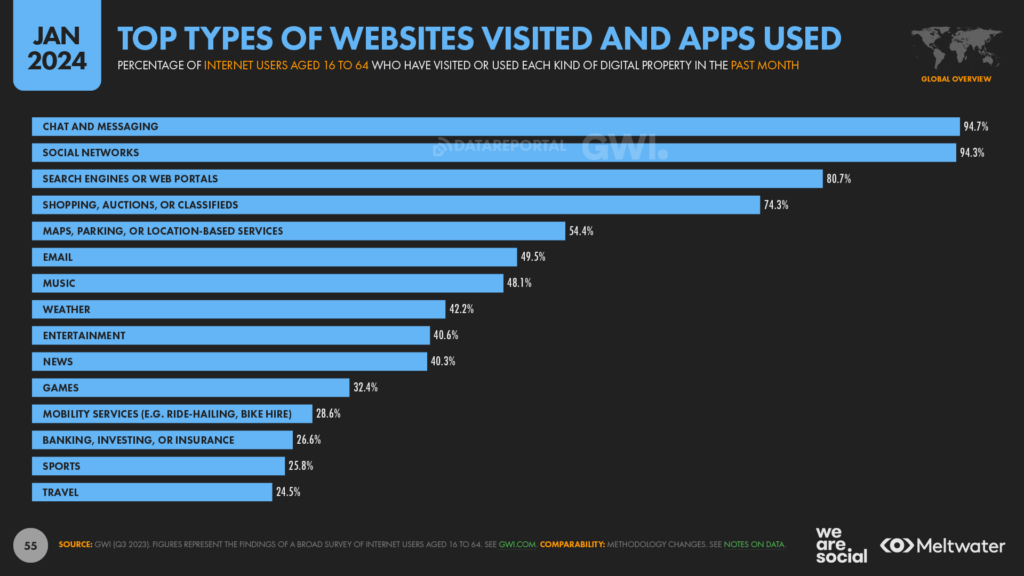

The world’s online activities

Overall, social media remains the most popular connected pastime, with more than 97 percent of working-age internet users accessing social networks or messaging platforms each month.

Across all ages, chat and messaging apps are the slightly more popular choice, with 94.7 percent of all internet users aged 16 to 64 saying that they’ve used at least one of these platforms in the past 30 days.

Social networks aren’t far behind though, with 94.3 percent of the same cohort saying that they’ve used at least one of these services in the past month.

Search engines rank third, with just over 4 in 5 survey respondents (80.7 percent) saying that they use services like Google and Bing on a monthly basis.

Shopping ranks fourth, with just under three-quarters of all internet users engaging in some kind of ecommerce activity each month.

And location-based services such as maps and parking apps round out the top 5, with just over half of GWI’s respondents saying that they’re regular users of these sites and apps.

Generational Differences

However, there are some subtle differences in these rankings when we cut the data by age.

For example, younger people are more likely to use online music platforms than they are to use maps and location-based services.

On the flip-side, music platforms only rank ninth for users aged 55 to 64.

Meanwhile, older generations are more likely to use email compared with today’s youth, but it’s worth pointing out that almost half of all internet users aged 16 to 24 still say that they use email on a monthly basis.

But perhaps the most noteworthy difference across the ages is that younger people are actually more likely to use social networks than they are to use chat and messaging apps.

This order is reversed across all other age groups in GWI’s latest survey results, and I confess I was surprised to see social networks at the top of this younger cohort’s activities.

As we saw in the overall data though, the difference between the two is only very slight, and the key takeaway here is that both activities are hugely popular across all ages.

Why we go online

Beyond the specific types of website and app that people use, it’s also interesting to explore the reasons why people go online.

And in particular, we see something of a contradiction in this data.

Almost 61 percent of GWI’s working-age survey respondents say that “finding information” is one of the top reasons why they use the internet, making this the most common motivation at a worldwide level.

Meanwhile, “staying in touch with friends and family” ranks second, with 56.6 percent of respondents citing this as primary motivation.

However, this rank order seems to contradict the findings of the dataset we explored above, which puts social media well ahead of search engines when it comes to the connected services that we use most often.

The answer to this quandary may lie in the various reasons why people use social media.

Perhaps unsurprisingly, “keeping in touch with friends and family” ranks top in the social motivations dataset, with almost half of working-age social media users saying that this is one of the primary reasons why they use social platforms.

However, the fact that roughly half of this cohort doesn’t choose this option is perhaps more revealing.

Similarly, the fact that 38.5 percent of respondents say that they use social media to “fill spare time” is particularly telling.

Overall, a key takeaway from this data is that social media is now just as much about entertainment as it is about social connection, as the rise of platforms like TikTok attests.

Returning our attention to the main reasons why people use the internet, “watching videos, TV shows, and movies” ranks third, with 52.3 percent of respondents selecting this answer.

And we see parallels to that trend in the social media motivations data, with 30.2 percent of social media users saying that they visit social platforms to “find content” like articles and videos.

However, these two things are inherently linked.

While many people certainly find intrinsic value (i.e. pleasure) in watching content for its own sake, it’s also true that entertainment content is one of the primary topics of conversation amongst friends and family.

And this may help to explain why entertainment content finds such a wide audience on “social media”, and why platforms like TikTok have gained so much momentum.

“Content isn’t king. If I sent you to a desert island and gave you the choice of taking your friends or your movies, you’d choose your friends – if you chose the movies, we’d call you a sociopath. Conversation is king. Content is just something to talk about.”

Is internet use getting less “purposeful”?

But this brings us neatly back to another of the trends that I highlighted in my 2023 analysis.

When trying to make sense of the decline in online time that we’d seen towards the end of last year, one of the hypotheses I explored with GWI’s Trends team was that people might have been becoming more “purposeful” and “considered” in their online activities.

“There are only so many hours in the day, and people want to know their online time isn’t being wasted.”

I still believe that’s a solid conclusion, but if this was indeed the primary motivation for that erstwhile change in our online behaviour, we might conclude that people have been happy to waste a bit more time online over the past year.

But then again, a less cynical perspective might be that people tried to achieve more online during 2023.

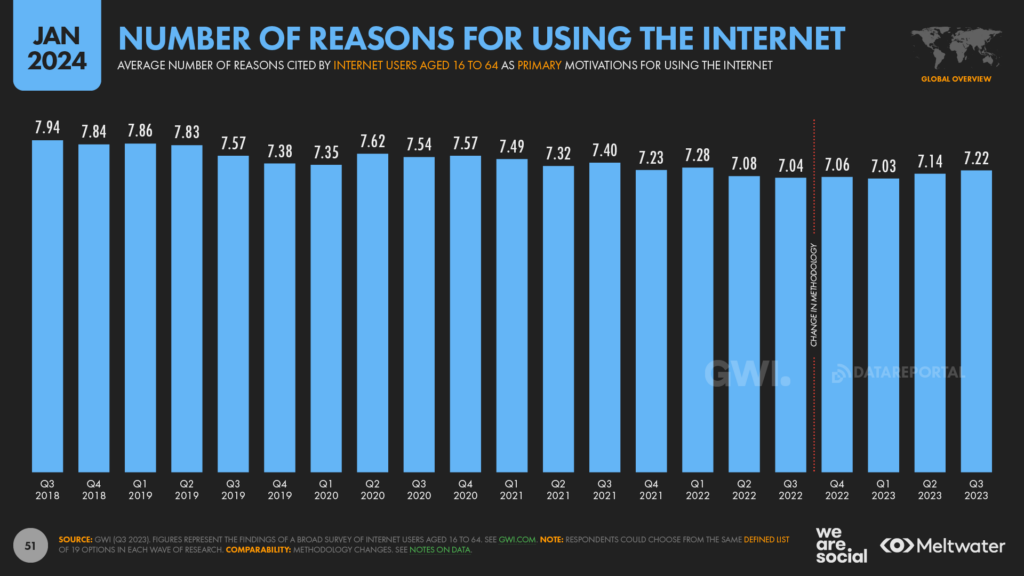

Either way, GWI’s data reveals that the average number of reasons for going online has crept back up again over the past year, from a low of 7.04 in Q3 2022, to 7.22 in the most recent round of data (Q3 2023).

[Side note: this average is largely determined by the options that people can select from in GWI’s survey. In the chart below, respondents could choose from the same 19 options in each survey “wave”, so the variation in the average represents a like-for-like comparison over time.]

Interestingly, out of the available options, the top categories also saw the largest relative increases over the past year, with “finding information”, “staying in touch with friends and family”, and “watching videos, TV shows, and movies” all seeing the strongest growth.

But despite that increase in the overall average, we did see some categories decline this year, with gaming the most notable.

Gaming remains a hugely popular activity of course, but the number of people who say that gaming is one of the primary reasons why they use the internet has dipped by almost 4 percent over the past year.

▶ Dig deeper: want to learn more about what people are really doing online – including their more “sordid” online activities? Click here to read our comprehensive analysis.

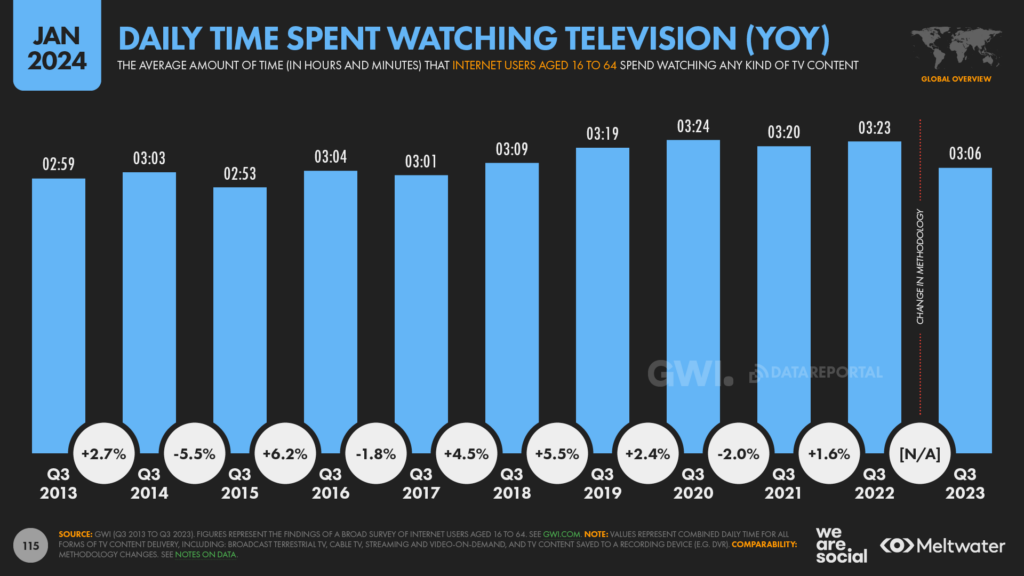

Decline in TV time

Despite the slight increase in the amount of time that internet users spend online each day, the latest data from GWI shows that connected populations are actually spending less time watching TV.

The company’s Q3 2023 wave of research shows that the typical internet user now spends 17 minutes per day less watching TV content than they did this time last year, with that dip equal to a year-on-year decline of 8.2 percent.

Note that this total figure covers all kinds of TV viewing, including broadcast, cable, and streaming.

It’s worth highlighting that changes to GWI’s methodology may have contributed to this change, but our analysis of data from both before and after that methodology change indicates that it isn’t the primary driver of these declines.

As a result, it appears as though people are indeed watching less television than they were this time last year.

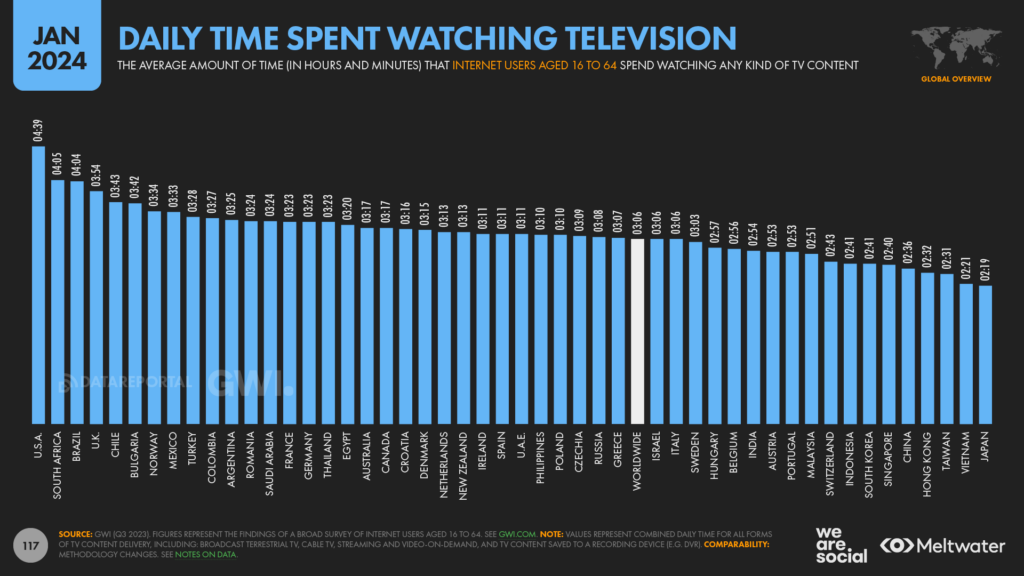

Figures to watch

Moreover, GWI’s data suggests that average daily TV viewing time has now returned to a level that we last saw in 2017.

However, the change in overall averages doesn’t tell the whole story.

At a worldwide level, people are now spending roughly the same amount of time streaming TV content over the internet as they were in Q3 2019, just before the Covid-19 pandemic took hold.

But over that same four-year period, viewing time for “conventional” TV – i.e. linear, broadcast content – has declined by 14 minutes per day, from an average of 1 hour and 58 minutes in Q3 2019, to 1 hour and 44 minutes in Q3 2023.

However, at more than three hours per day, it’s essential to highlight that TV is still a fundamentally important part of internet users’ days.

On average, working-age internet users still spend more time watching TV content than they do using social media, and – despite the recent decline – we can expect TV to continue playing a central role in people’s everyday lives for many years to come.

So, my counsel is to stop treating media activities as somehow “competing” with each other.

Beware of “media buckets”

Yes, you still need to decide how to allocate your marketing budgets across different channels.

However, robust research shows that marketing campaigns which make use of multiple different kinds of media tend to deliver the best results.

Ultimately, our audiences don’t care whether we label what they’re consuming as “TV”, “social media”, or some other arbitrary industry term.

People simply want to be entertained, stimulated, inspired, and feel a sense of connection.

These are the things that will capture their attention, so that’s what we should focus our attention too.

Meanwhile, India’s internet population is also growing rapidly.

It’s tricky to identify exactly how rapidly, because the sheer scale of the country makes it difficult to conduct the research required to identify internet use across the nation as a whole.

Different research also offers quite different findings – even when it comes to things like the size of India’s total population.

However, a highly regarded study conducted by Kantar and the IAMAI indicates that India’s connected population grew by 9.7 percent between 2021 and 2022.

Meanwhile, our analysis of data from a variety of different organisations shows that more than half of India’s total population is now online, with the country home to more than 750 million users.

India’s internet adoption rate still lags the global average of 66.2 percent, but recent studies show that the country is steadily closing this gap.

India’s internet adoption rate still lags the global average of 66.1 percent, but recent studies show that the country is steadily closing this gap.

That’s obviously excellent news for Indians, but these increases will likely have important implications for internet users outside of the country too.

In particular, I expect to see India play a significantly greater role in shaping online culture over the coming years, especially as Indian content gains momentum on global platforms like Netflix and Spotify.

Making sense of this trend requires significantly more context though, so click the link below to explore the full story.

▶ Dig deeper: learn how a more connected India may reshape global culture in this detailed analysis

TikTok vs. Instagram

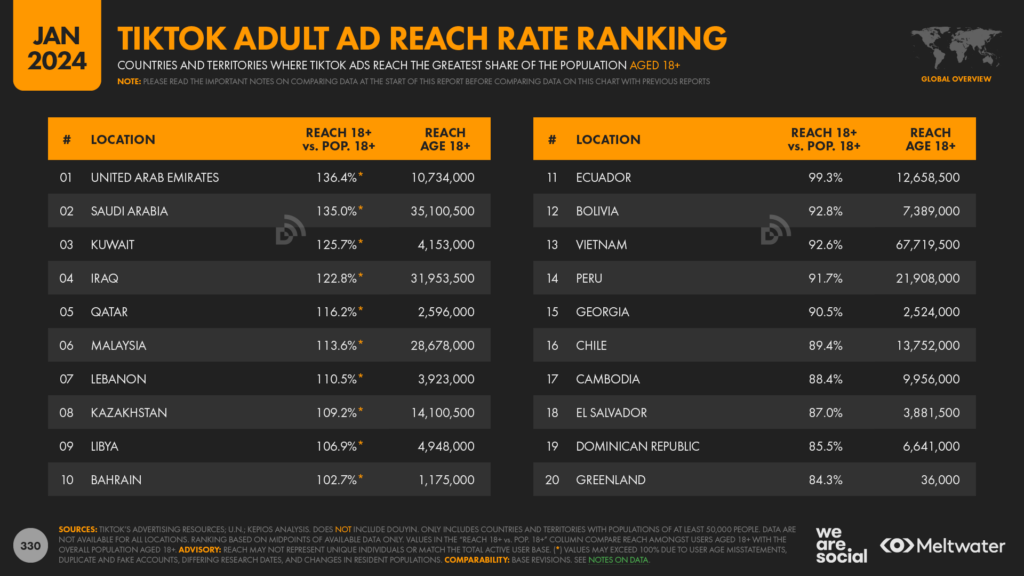

We’ve been able to access a significantly expanded dataset for TikTok this year, which has enabled us to report data for many more countries than before.

This data still comes directly from Bytedance, so it will still be just as representative as our previous dataset, but it covers a much wider range of markets.

It’s worth highlighting that we continue to see anomalies in this data – especially in terms of elevated ad reach across the Middle East – but this is the data that Bytedance reports to marketers through its own resources, so we’ve chosen to report it “as is”, in order to let readers form their own conclusions.

So what does this new data tell us?

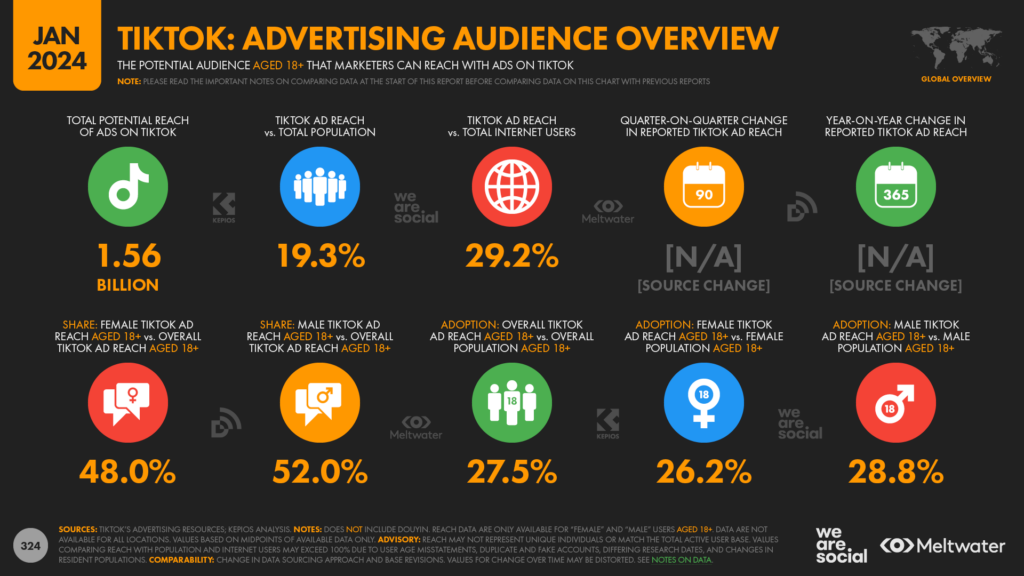

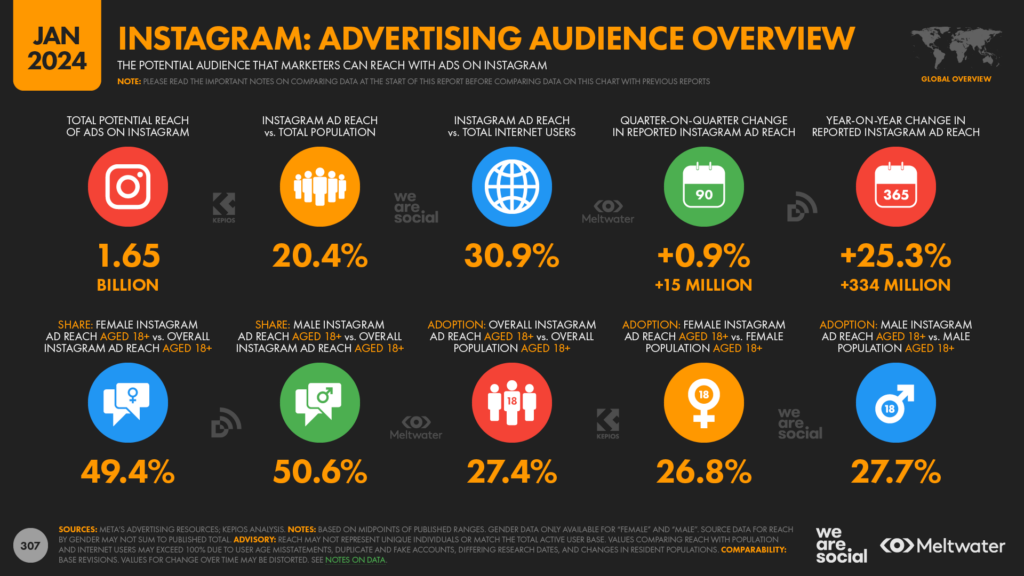

Well, perhaps one of the most striking takeaways from this new data is that TikTok’s total global ad audience is now almost as large as Instagram’s.

Figures reported in Bytedance’s own advertising resources show that TikTok ads now reach a global audience of 1.56 billion users each month.

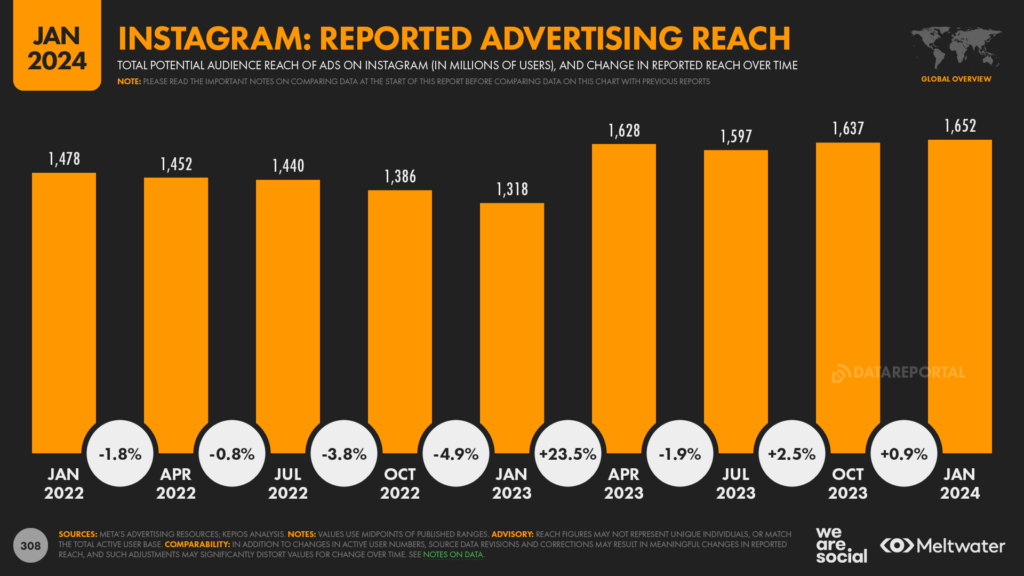

That’s only 5.5 percent lower than the latest Instagram figure published in Meta’s advertising resources, which put the platform’s global ad reach at 1.65 billion at the start of 2024.

However, as with our previous dataset, Bytedance only reports ad audience data for users aged 18 and above.

And if we limit our comparison of these two platforms to users in that adult cohort, the reported ad reach for both is eerily similar: 1.56 billion.

But there’s another crucial difference between these companies’ data: Bytedance’s reported audience data doesn’t cover all countries, whereas Meta’s does.

And if we limit our comparison to only those countries for which TikTok data is available, these platform-reported figures indicate that TikTok ads may now reach a larger audience than Instagram ads.

Indeed, the available data suggest that – on a like-for-like basis, comparing adult audiences across available countries – TikTok’s reported ad audience may be as much as 30 percent larger than Instagram’s ad audience.

However, there’s much more to this story than these headline figures suggest.

It’s complicated…

First up, some important differences.

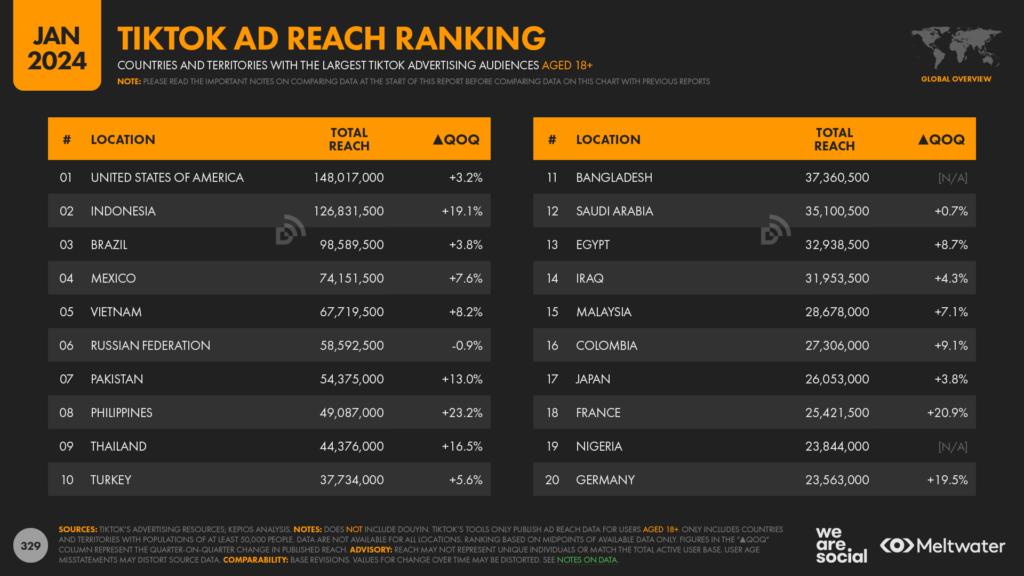

TikTok remains blocked in India, so the platform has no reported ad reach in the country.

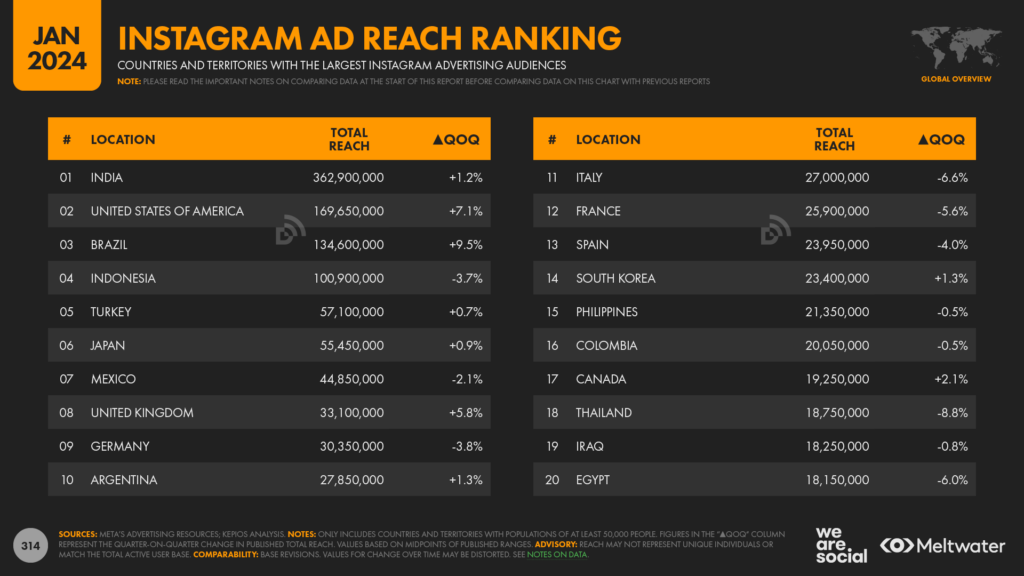

However, India remains Instagram’s largest market, and Meta’s latest data show that Instagram ads reach a total audience of close to 363 million in the country.

On the other hand, Instagram doesn’t report ad reach for Russia due to US sanctions, whereas TikTok continues to report reach of more than 58 million users in the country.

Next up, if we focus solely on users over the age of 18, Instagram’s reported ad reach in the United States still exceeds that of TikTok (162 million vs. 148 million, respectively).

And we see a similar story across Western and Northern Europe, with Instagram’s combined ad reach across the region (126 million) considerably ahead of TikTok’s reported total (100 million).

However, data suggests that TikTok’s adult audience is significantly larger than Instagram’s in other parts of the world.

For example, across Western Asia, TikTok reports adult ad reach of 149 million, which is more than 20 percent higher than the 122 million reported by Instagram.

Similarly, TikTok’s reported ad reach across the African continent is 72 percent higher than Instagram’s (144 million vs. 84 million, respectively).

And finally, TikTok reports ad reach of 345 million users across South-Eastern Asia, whereas Instagram only reports reach of 154 million for the region.

So – as is so often the case – different platforms may offer different benefits and advantages, depending on what the marketer is trying to achieve.

Even more options

For me, the most important takeaway from all of this data is that marketers now have even more compelling options to choose from.

And what’s more, the data shows that both platforms continue to grow at impressive rates.

The Instagram reach figures reported in Meta’s resources suggest that the platform’s global reach has increased by 334 million over the past year, resulting in year-on-year growth of 25.3 percent.

And while we’re unable to provide an exact figure for global TikTok growth due to our recent change in datasets, our comparison of same-country data shows that TikTok’s reach has increased by 26.4 percent.

But should we take these platforms’ own numbers at face value?

Let’s take a look at what some independent data tells us.

Third-party perspective

First up, our analysis of mobile app intelligence from data.ai tells quite a different story to the companies’ ad reach figures, although there are some important similarities too.

By the end of Q3 2023, data.ai reports that TikTok’s active user base was already larger than Instagram’s across key Northern American markets, albeit only by a very small margin.

TikTok was also significantly ahead of Instagram across top economies in South-Eastern Asia.

However, Instagram still led TikTok by a considerable margin across larger economies in Europe, and it was also well ahead across primary markets in Southern America.

Overall, data.ai’s figures suggest that Instagram still leads TikTok, but reduced data availability for lower- and middle-income countries likely skews this finding in Instagram’s favour.

However, another key takeaway from data.ai’s intelligence is that both these platforms have each added more active users than any of the other top social platforms over the past few months.

And data.ai’s nuanced usage data provides even more valuable perspectives.

Comparing time and frequency

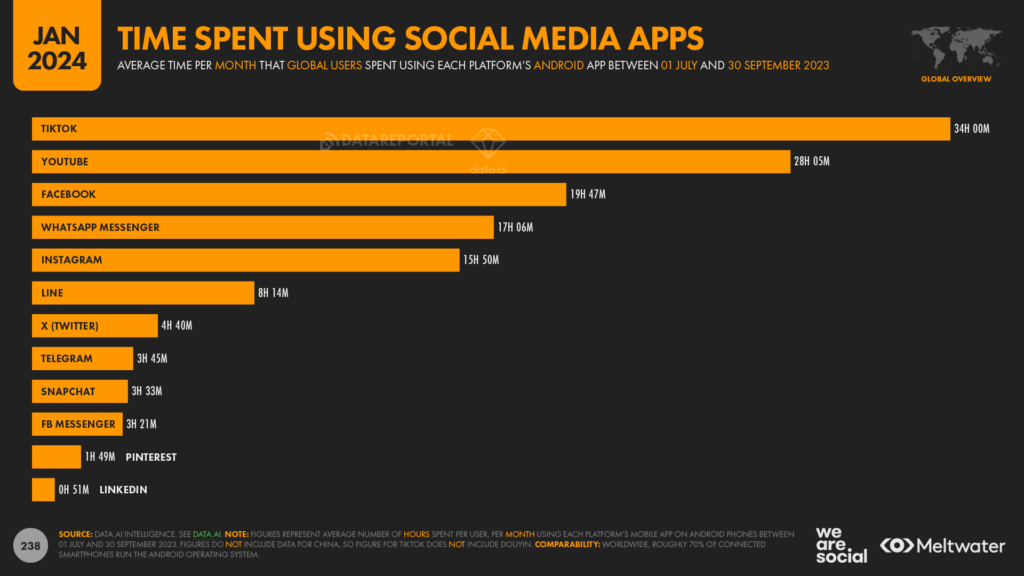

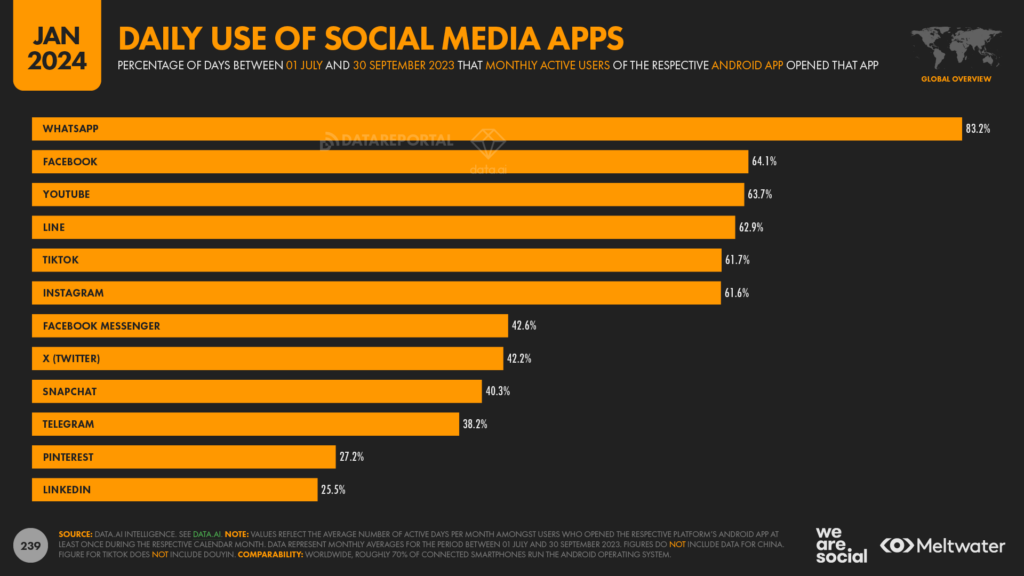

The company’s analysis shows that TikTok had the highest average time per user of any of the top “social” apps between July and September 2023, with the platform’s typical Android user clocking in at 34 hours per month.

In other words, at a worldwide level, the typical TikTok user now spends an average of more than an hour per day using the platform.

That’s almost 6 hours per month ahead of second-placed YouTube, which sees an average of slightly over 28 hours per month, per user for its Android app.

However, as always, it’s important to remember that a significant proportion of YouTube activity takes place in web browsers, and even based on app activity alone, YouTube still accounts for the greatest total amount of time across these top social apps (thanks to its larger user base).

But the more striking comparison is with Instagram, with data.ai’s insights revealing that the typical Instagram user spends less than half as much time using the platform’s Android app as TikTok users spend using the TikTok app.

data.ai’s analysis suggests that Instagram users spend an average of 15 hours and 50 minutes per month using the app, which equates to an average of roughly 31 minutes per day.

However, the same data reveals that both apps have seen considerable increases in average time per user over the past year.

Average TikTok time has increased by 3 hours and 46 minutes per user, per month (+12 percent), while average Instagram time has grown by more than 4 hours per user, per month (+34 percent).

Interestingly though, both apps see the same daily use ratios, with just over 6 in 10 users opening the app every day.

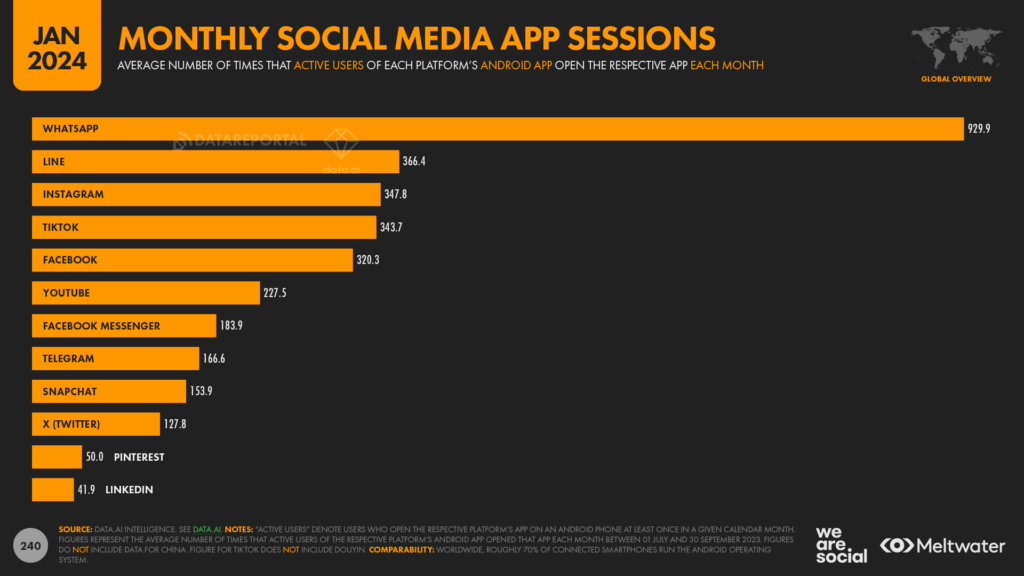

Interestingly though, Instagram users tend to open the app slightly more frequently than TikTok users.Data for Q3 2023 shows that Android users opened the Instagram app an average of 347.8 times per month, compared with an average of 343.7 times per month for TikTok

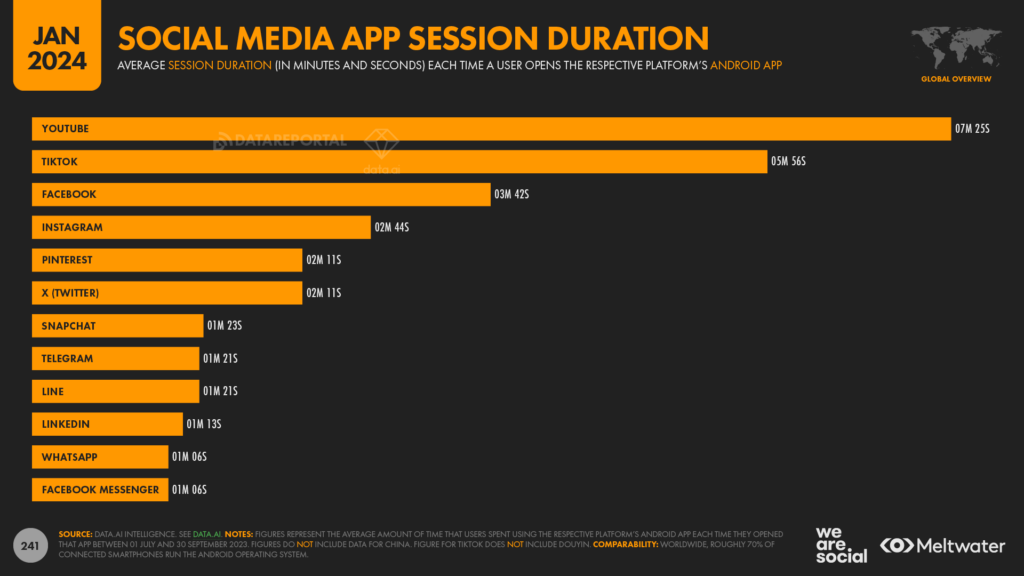

As you’ve probably guessed by now though, the typical TikTok session lasts considerably longer than the typical Instagram session.

data.ai reports that TikTok sessions lasted an average of 5 minutes and 56 seconds in the third quarter of last year, which is more than twice as long as the Instagram average of 2 minutes and 44 seconds.

A complex web

With Instagram and TikTok both heavily oriented towards their native mobile app experience, it’s perhaps less representative to compare traffic to their websites, especially given their differing demographic appeal.

However, such comparisons provide another valuable angle, so let’s take a look at what this data tells us.

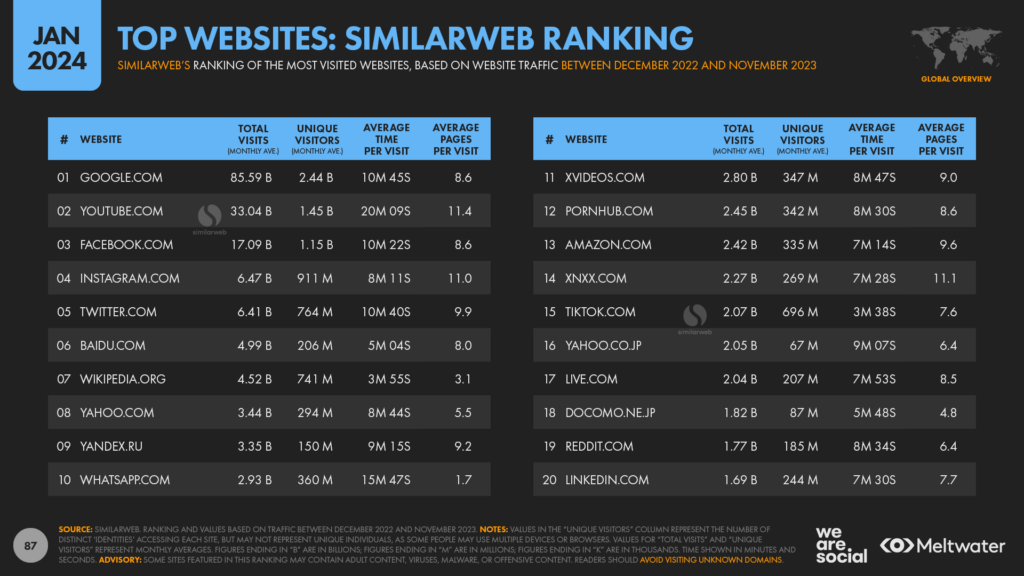

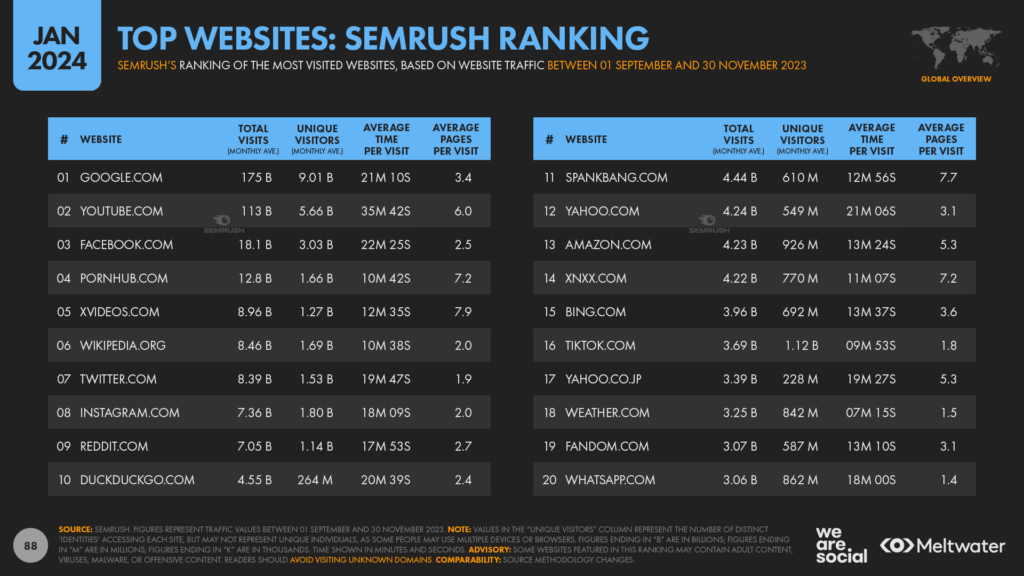

First up, analysis from Similarweb shows that Instagram attracts meaningfully more traffic to its website than TikTok does, with Instagram attracting an average of 30 percent more unique monthly visitors than its rival during 2023.

Similarweb also reports that Instagram.com attracts 3 times as many total monthly visits as TikTok.com, with those visitors spending considerably more time on Instagram’s website too.

Meanwhile, Semrush’s data tells a slightly different story, although the outcome is the same.

The company’s latest analysis suggests that Instagram.com attracted roughly 60 percent more unique visitors than TikTok.com did between September and November 2023, and almost twice as many total monthly visits.

Semrush’s data also shows that people spend significantly longer on Instagram’s website than they do on TikTok’s dot-com domain.

Once again though, data from both Similarweb and Semrush shows meaningful growth in web traffic to both websites over the past year.

So, given the complexity of this story, let’s take a look at two last data points, before drawing some conclusions.

Search your feelings

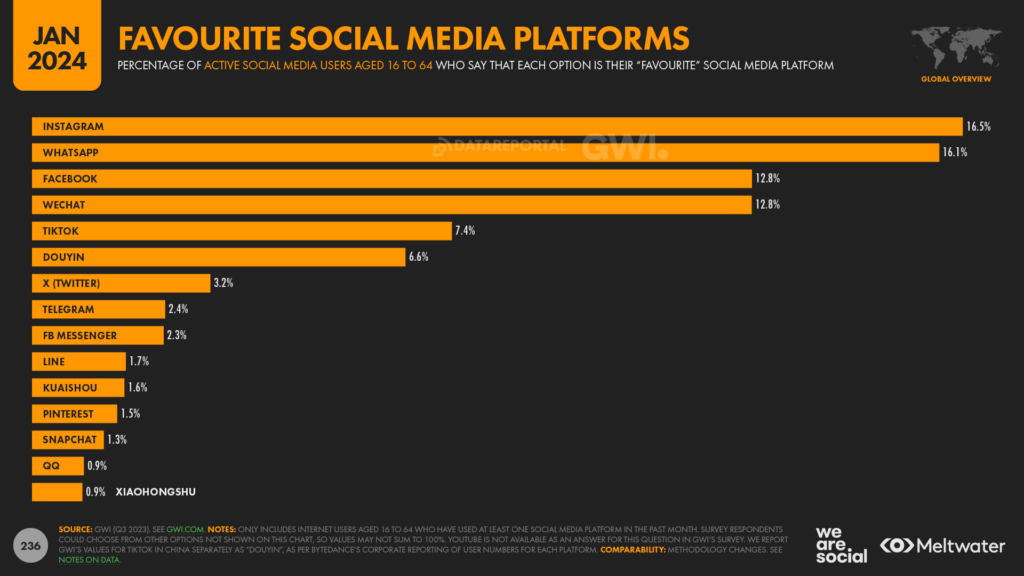

But despite the continuing surge in TikTok use, Instagram is still comfortably ahead of Bytedance’s platform in one key metric: audience affinity.

The latest data from GWI reveals that Instagram is now the world’s “favourite” social media platform, with 16.5 percent of internet users between the ages of 16 and 64 selecting the platform above all others.

That’s more than twice as many as the 7.4 percent that chose TikTok.

And just for perspective, it’s worth highlighting that this cohort still has greater affinity for Facebook than they do for TikTok, with Meta’s largest platform still the preferred choice amongst 12.8 percent of the world’s working-age internet users.

TikTok is gaining preference though, and the platform’s current 7.4 percent has increased by a relative 21 percent (+1.3 percentage points) since this time last year.

So, after all that analysis, what’s the conclusion?

Yes and…

In reality, both Instagram and TikTok offer highly compelling opportunities for marketers, so the easy answer is that you should actively consider both of them.

The “best” choice will depend on various factors such as your audience, your objectives, and the kinds of message you want to communicate, but both Instagram and TikTok offer marketers the ability to reach over 1.5 billion users with an array of creative opportunities.

But just before we wrap up this section, let me leave you with one last tidbit.

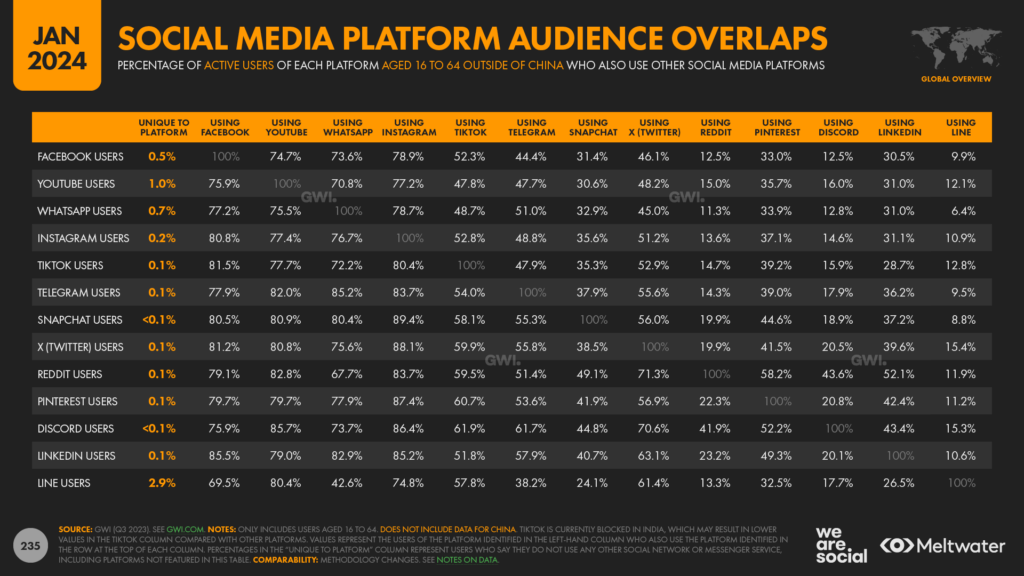

More great data from GWI reveals that over half of Instagram users also use TikTok each month, while more than 80 percent of TikTok users also use Instagram.

In other words, users’ most common behaviour is to use both platforms each month, which means that you’ll likely end up reaching many of the same people on each platform.

As a result, if you do decide to use them both, I’d recommend taking a different approach on each one, in order to maximise your effectiveness.

But with Instagram and TikTok both growing so quickly, does this finally mean that “Facebook is dead”?

Ummm… no.

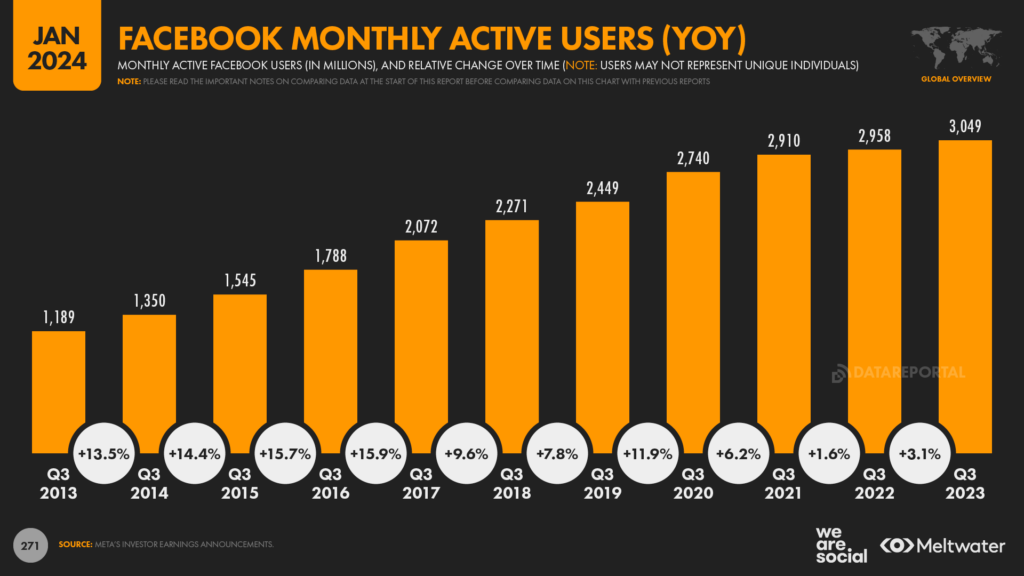

Facebook in 2024

The change in Facebook’s reported ad reach over the past year may not be quite as impressive as the changes we saw above for TikTok and Instagram, but Meta still reported healthy growth for Facebook over the course of 2023.

The company’s latest data indicates that global Facebook ad reach grew by more than 200 million over the past 12 months, delivering year-on-year growth of 10.5 percent.

Moreover, Facebook’s reported ad reach still exceeds that of Instagram and TikTok by a considerable margin.

Meta’s business resources report that marketers can now reach close to 2.2 billion users with ads on Facebook each month, which equates to more than 40 percent of all the world’s internet users.

But when we consider that Facebook is still blocked in China, it’s perhaps more representative to show that Facebook ads now reach more than half of all internet users outside of China every month.

Whichever way you look at it, that’s an impressive achievement, and Zuck and team will doubtless be celebrating this as part of the festivities to mark Facebook’s twentieth anniversary on February 4th.

That ad reach number doesn’t tell the whole story though, and it’s worth stressing that Facebook ads don’t reach everyone that uses the platform.

Plenty of room for Facebook to grow

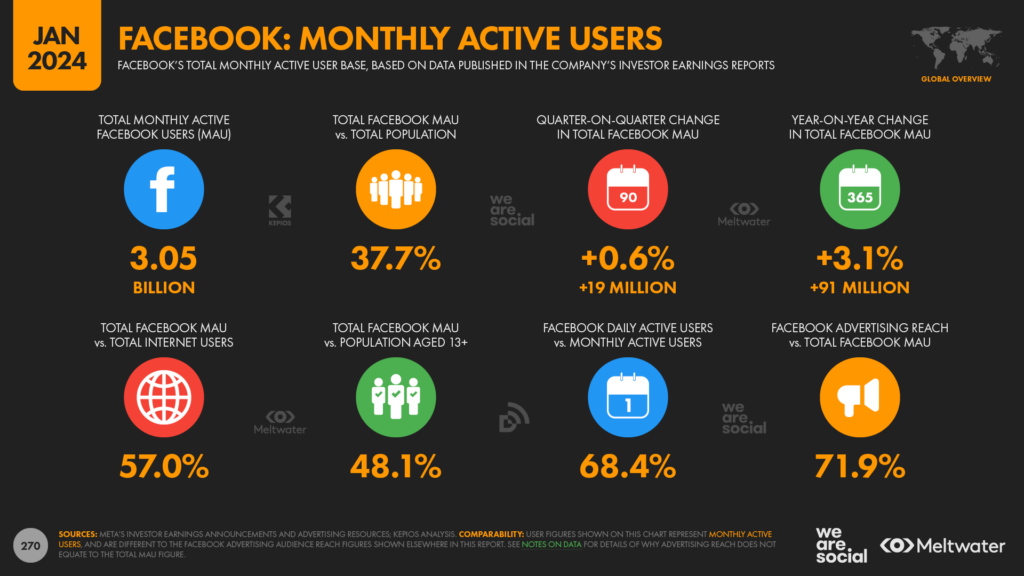

Comparing the latest ad reach figures with the monthly active user figures published in Meta’s Q3 2023 Earnings Presentation, the company’s own data indicates that Facebook ads only reach 71.9 percent of the platform’s active user base.

It’s unclear from this data alone why more than 850 million of Facebook’s 3.05 billion monthly active users didn’t see any ads on the platform last month, but it’s important to remember that Facebook doesn’t show ads in the Notifications feed of its mobile app, nor does it show ads on people’s profiles.

So, even from these numbers, it’s clear that Facebook still has plenty of potential to grow its business, even when it comes to monetising existing, active users.

And moreover, that active user base continues to grow too.

The latest data show that monthly active Facebook users have increased by 91 million over the past year, delivering year-on-year growth of 3.1 percent.

The current total of 3.05 billion is already equal to 48 percent of all people aged 13 and above living on Earth today, but if we remove China again, the data indicate that a massive 59.6 percent of all those people who can use Facebook already do so – every month.

And just to reiterate, that figure is still growing.

So no; Facebook is not dying.

However, the mainstream media still seems to be peddling this ridiculous narrative, and – while we all know it’s incorrect – this inaccurate clickbait may influence how your leadership views your digital strategy.

So, we’ve produced a comprehensive response to help you dispel this misinformation – click the link below to learn more.

▶ Dig deeper: find all the latest data, trends, and insights you need to correct people who claim that “social media is dying” in this deep-dive article.

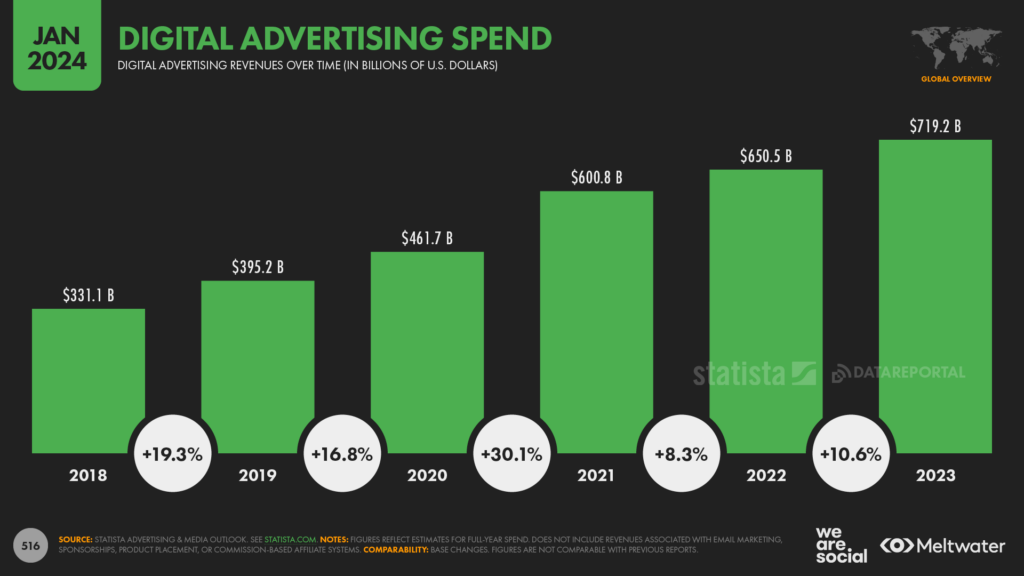

Digital dominates ad spend

The latest data show that the world’s marketers spent a combined total of almost USD $720 billion on digital ads in 2023, which was more than 10 percent higher than the equivalent figure for 2022.

Statista reports that digital ad spend has more than doubled over the past 5 years, with the latest total roughly 117 percent higher than the figure reported for 2018.

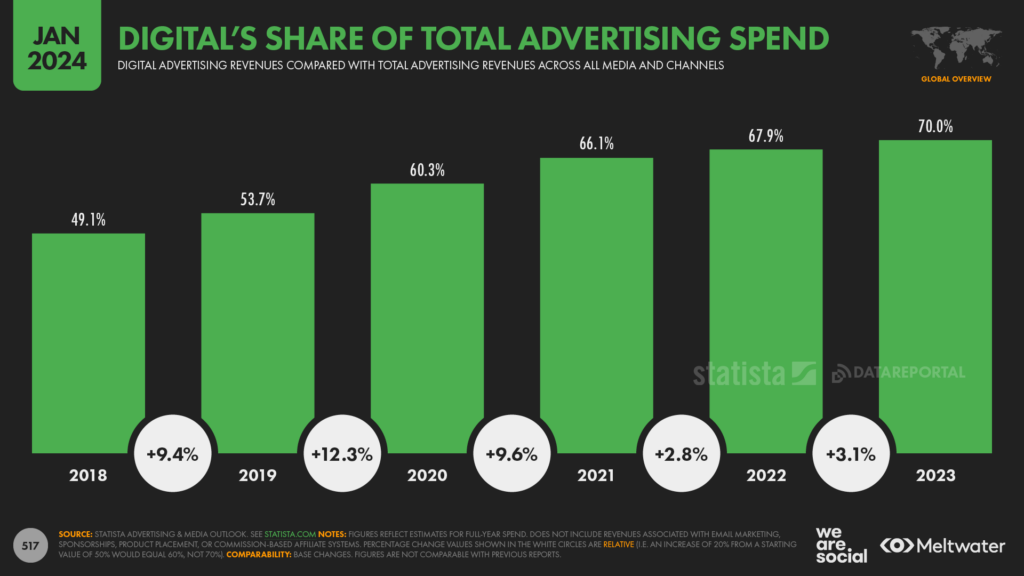

Statista also reports that digital’s share of ad spend continues to grow.

The company’s latest analysis indicates that 70 percent of total ad spend went to digital channels in 2023, up from 67.9 percent in 2022.

Note that Statista has revised its estimates for previous years though, so these figures will not correlate with those we published in last year’s reports.

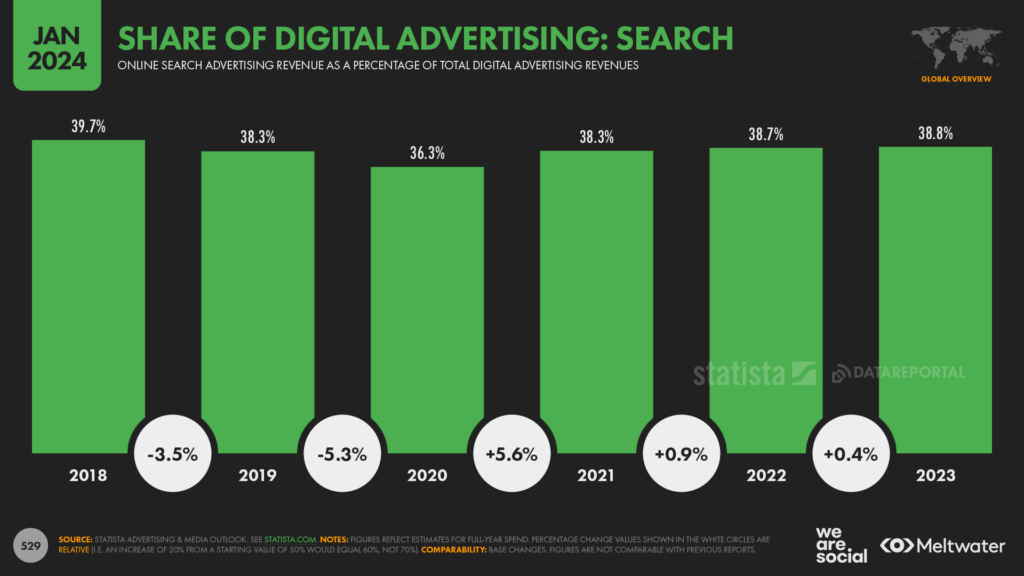

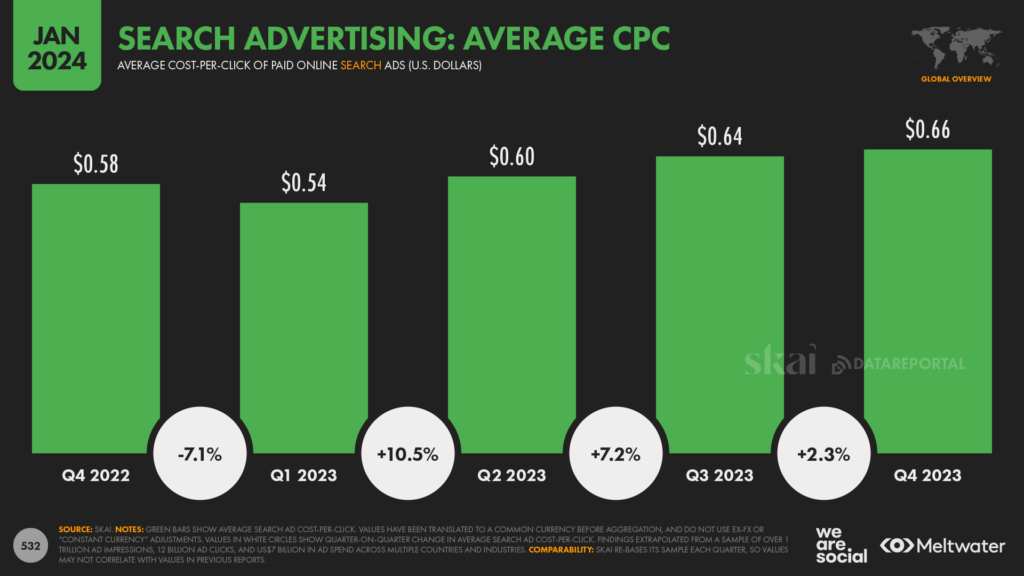

Search accelerates

Search ads still account for the greatest share of digital ad spend, capturing close to USD $280 billion over the course of 2023.

For perspective, that figure was 11 percent higher than marketers’ spend on search ads in 2022, while search increased its share of total ad spend last year too.

In all, 38.8 percent of advertisers’ 2023 digital budgets went to search advertising, up by a tenth of a percentage point compared with 2022’s 38.7 percent.

Meanwhile, analysis from Skai shows that advertisers spent roughly 4 percent more on search ads in the final three months of 2023 than they did in the same period the year before.

However, the average cost per click (CPC) of search ads increased by almost 14 percent year on year, resulting in a meaningful decline in the total number of search impressions served compared with the last three months of 2022.

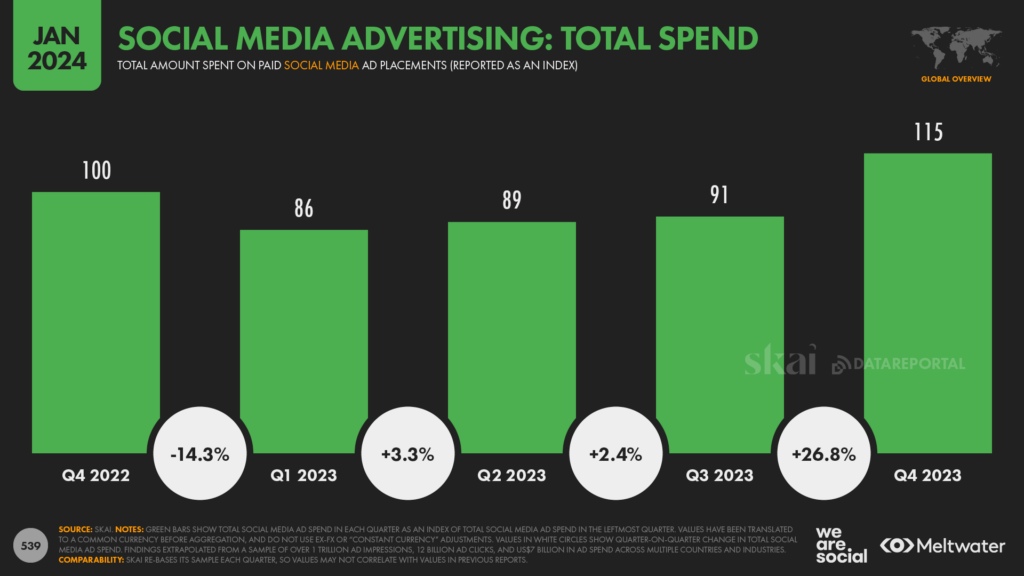

Social media ad spend increases

Meanwhile, despite ongoing economic headwinds, marketers also spent more money on social media advertising in the final quarter of 2023 than they did in the same period of 2022.

Data from Skai reveals that advertisers increased “holiday” social media ad spend by roughly 15 percent year on year, while spend was up by 26.8 percent quarter-on-quarter compared with the July to September period.

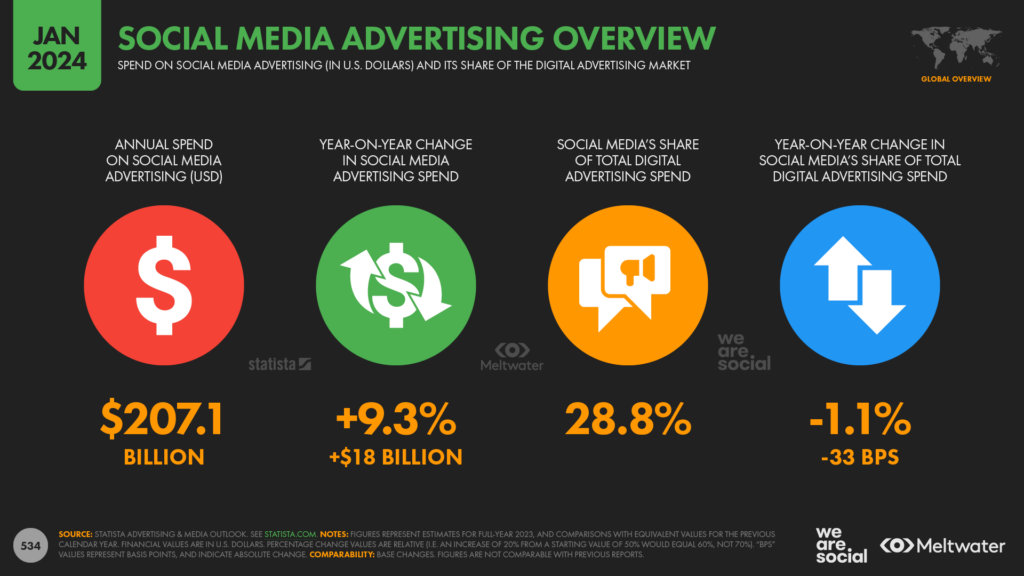

More broadly, Statista reports that social media ad spend for 2023 as a whole was up by 9.3 percent compared with 2022, reaching a total of USD $207 billion.

However, the company’s analysts also found that social media’s share of overall digital ad spend actually declined slightly last year.

Paid social media placements accounted for 28.8 percent of all online advertising in 2023, which was down by a relative 1.1 percent (-33 basis points) compared with 2022 social ad spend.

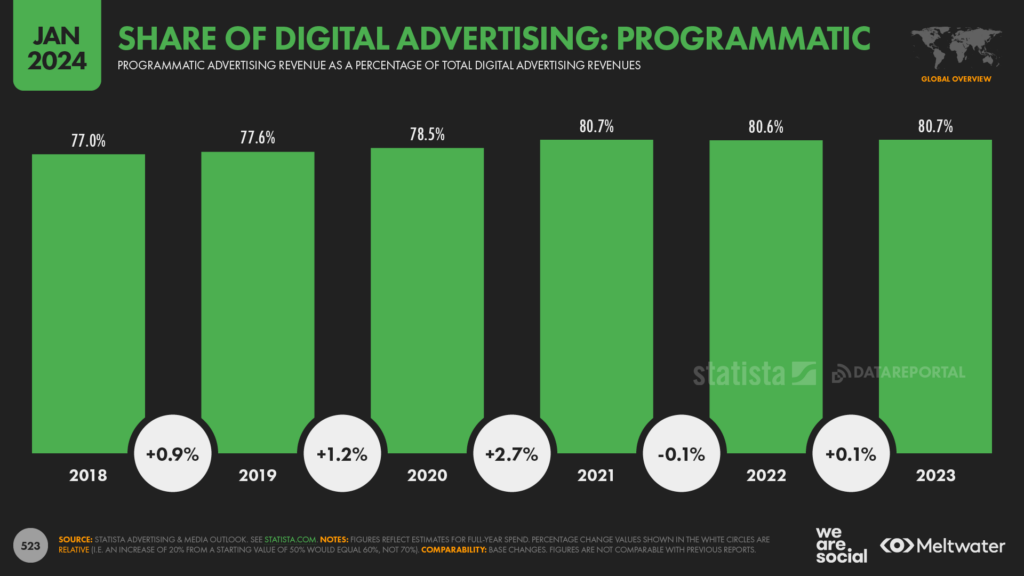

The robots rule

More broadly, over80 percent of digital ad budgets were spent programmatically in 2023, although that share has remained relatively consistent over the past three years.

Statista reports that USD $580 billion was spent on programmatic advertising last year, with that total increasing by 10.7 percent ($56 billion) compared with 2022.

LinkedIn members pass 1 billion

Figures published in LinkedIn’s business resources reveal that marketers can now reach more than 1 billion LinkedIn “members” using the platform’s ad products.

This figure likely represents LinkedIn’s total registered member base though, and the 1 billion figure should not be confused with the monthly active user figures that we report for other social platforms.

That clarification does nothing to diminish the significance of this milestone though, and these latest figures firmly cement LinkedIn’s position as the world’s preeminent professional network.

LinkedIn still growing

LinkedIn’s ad reach continues to grow too, with data published in the company’s advertising resources pointing to a year-on-year increase of almost 14 percent.

For perspective, that suggests that roughly 1 in 8 LinkedIn members only joined the platform within the past 12 months.

And furthermore, LinkedIn adoption appears to have accelerated in 2023 compared with the year before, with the platform attracting an extra 33 million new users last year compared with its additions for 2022.

LinkedIn’s audience is still heavily centred on the United States though, with data indicating that almost a quarter of the platform’s total member base is located in Northern America.

The company’s advertising reach figures point to 220 million registered members in the USA, compared with 120 million in India, and 68 million in Brazil.

A network of young professionals

It’s also interesting to note that more than half – 51.6 percent – of LinkedIn’s advertising audience is aged between 25 and 34.

Meanwhile, the company’s data suggests that members aged 18 to 24 actually outnumber users above the age of 35.

Figures reported in LinkedIn’s ad resources suggest that the younger cohort accounts for 24.7 percent of the total audience, compared with 23.7 percent for the over-35s.

However, it’s important to stress that LinkedIn’s active user base is considerably smaller than these “member” figures suggest.

Indeed, our analysis of third-party data from companies including data.ai, Similarweb, and Semrush suggests that just 1 in 3 LinkedIn members is active on a monthly basis.

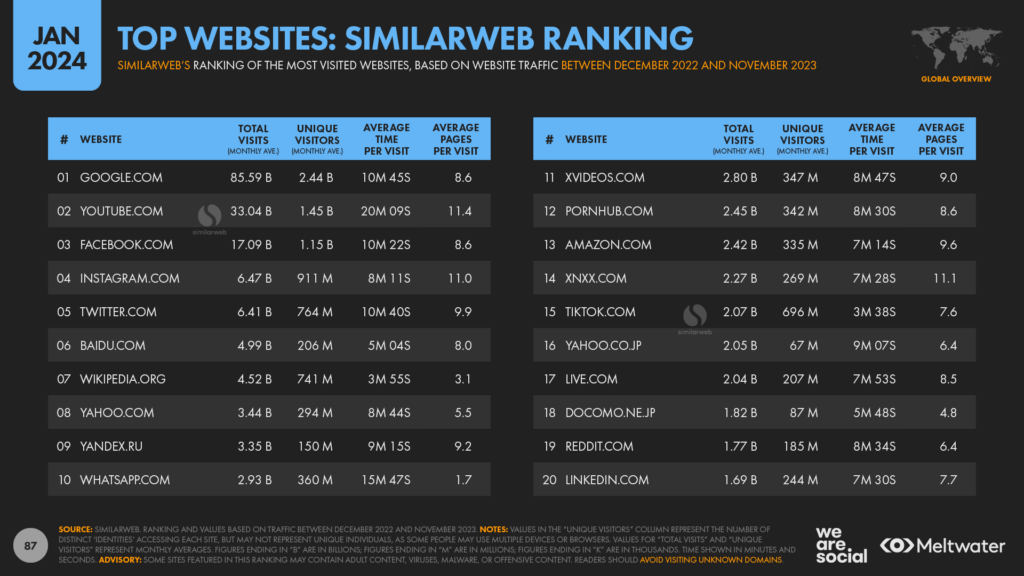

That estimate puts LinkedIn MAUs at roughly 330-350 million, although this level of usage is still enough to place LinkedIn.com in Similarweb’s latest ranking of the world’s top 20 websites.

It’s also worth highlighting that “less active” LinkedIn users may still represent a valuable marketing opportunity, because these irregular users most likely visit the platform when they’re actively exploring a change of employer or career.

This “need state” has obvious appeal to brands in the recruitment industry, but people who are considering a change in one of the most important aspects of their lives may also be more open to making changes in other aspects of their lives too – or at least be more receptive to new marketing messages.

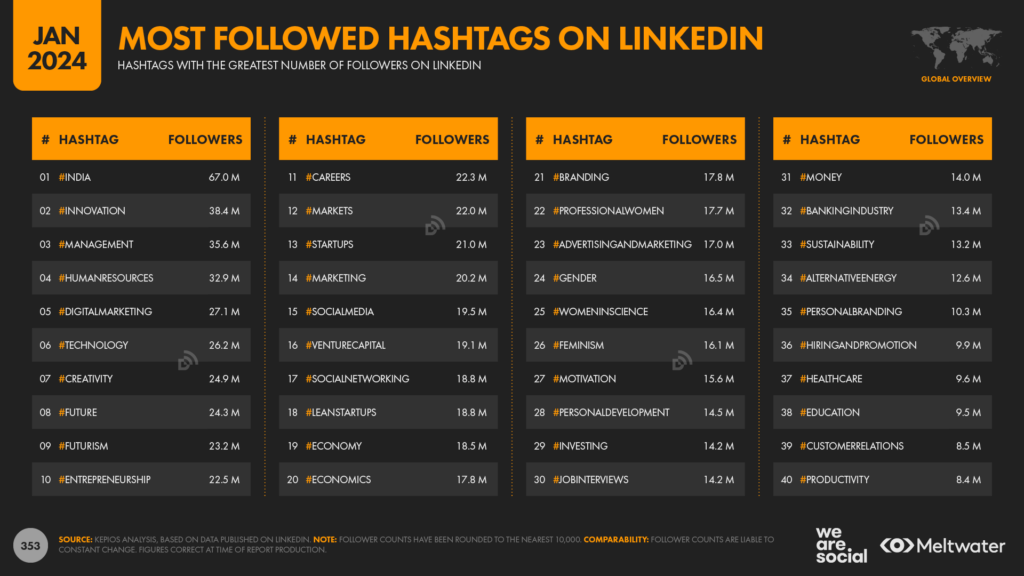

LinkedIn hashtags losing favour

However, we did notice that hashtags appear to be losing impact on LinkedIn.

A comparison of follower numbers in this year’s ranking with the follower numbers for the same tags that we published last year shows that all of the top tags have been losing followers.

It’s unclear whether this represents an active downgrading of hashtags in the LinkedIn algorithm, or whether it’s the result of users growing tired of “hashjacking” and spam.

Either way though, marketers may want to rethink how they use hashtags on LinkedIn, and avoid depending on them too heavily in order to drive visibility.

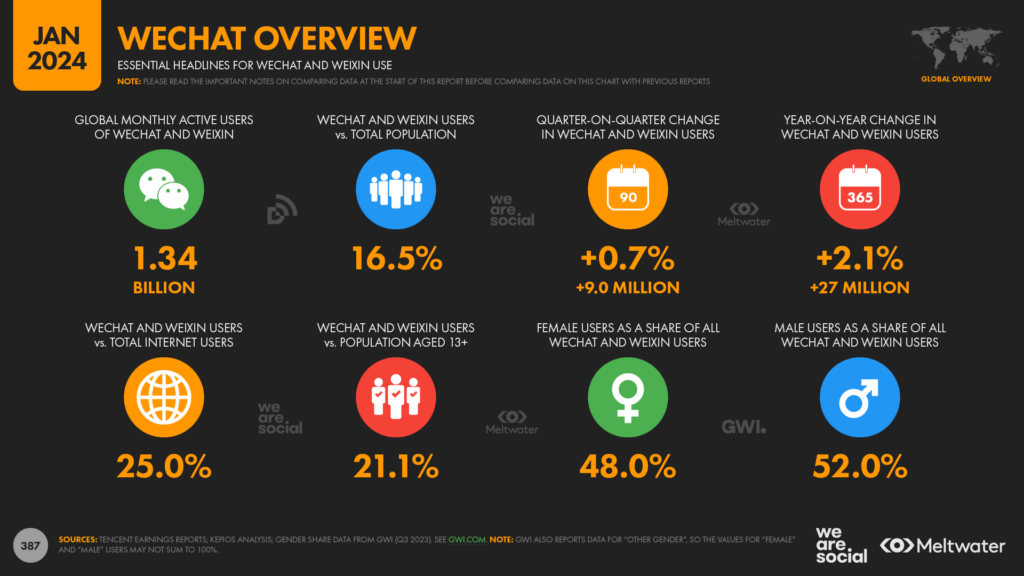

The state of WeChat

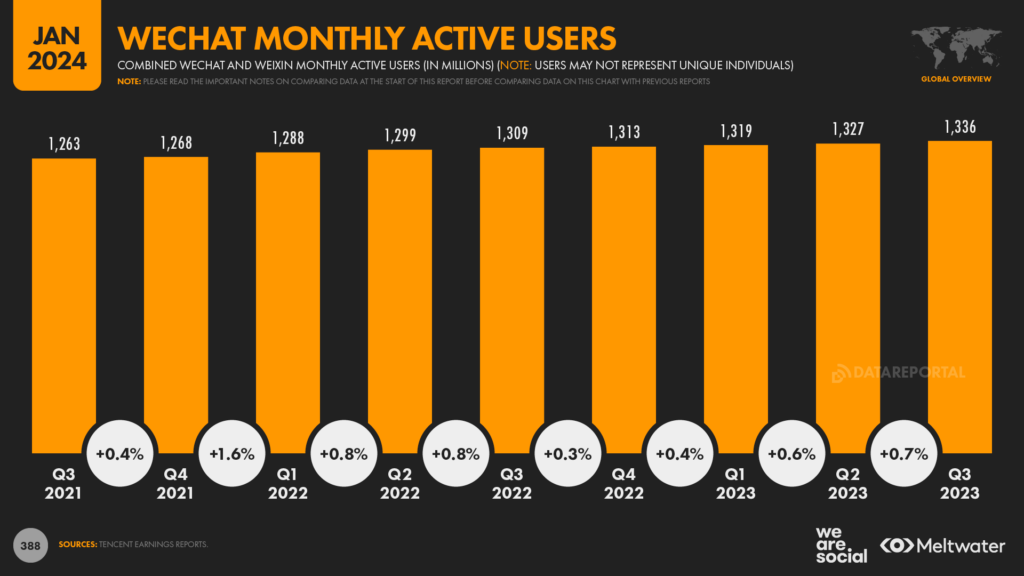

WeChat became China’s largest social media platform around the end of 2016, but data shows that the platform continues to grow.

Tencent’s latest investor earnings announcement reveals that WeChat and Weixin now reach a combined audience of 1.34 billion monthly active users, which is 2 percent higher than the MAU figure that the company reported this time last year.

That growth figure might seem quite small in comparison to the ones that we reported above for Instagram and TikTok, but it’s important to remember that the vast majority of China’s internet users already use Weixin.

Data from CNNIC (in Mandarin) shows that more than 97 percent of the country’s connected population uses instant messaging, and while there are other messaging options in China, Weixin is by far the most popular choice.

However, therein lies the importance of the distinction between WeChat and Weixin.

While Tencent groups the two apps together in its reporting, the apps offer quite different benefits.

Weixin is closely integrated into almost every aspect of everyday life in China – both online and offline – to the extent that foreign visitors can often find it difficult to pay for things or get around without it.

However, without the benefits of these “network effects”, WeChat has struggled to gain the same level of momentum outside of its domestic market.

Indeed, the latest data from GWI suggests that more than 87 percent of the world’s WeChat users are located in China, and less than 5 percent of the working-age internet population outside of the country says that they use WeChat in any given month.

But despite these challenges, WeChat continues to grow, and even if its success remains limited to China, at least that success is concentrated in the world’s largest connected market.

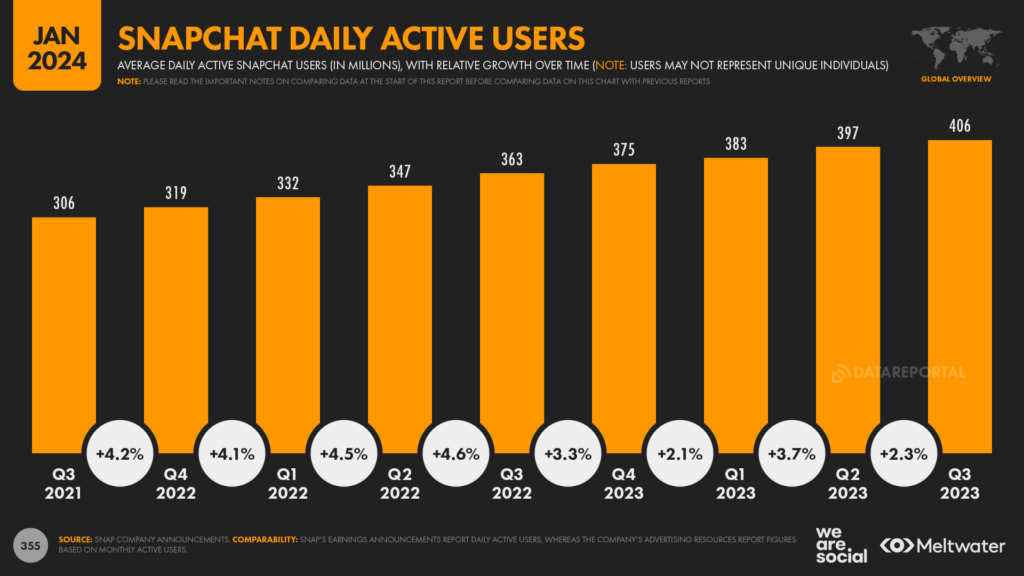

Snapchat still growing

And we’re sticking with social media growth for our next trend too.

Following last year’s news that it attracts more than 750 million monthly active users, Snapchat has delivered another impressive milestone in our latest round of data, with the platform now boasting more than 400 million daily active users.

The company’s most recent investor earnings report reveals that the platform has added 100 million daily active users over the past two years, to reach the current total of 406 million.

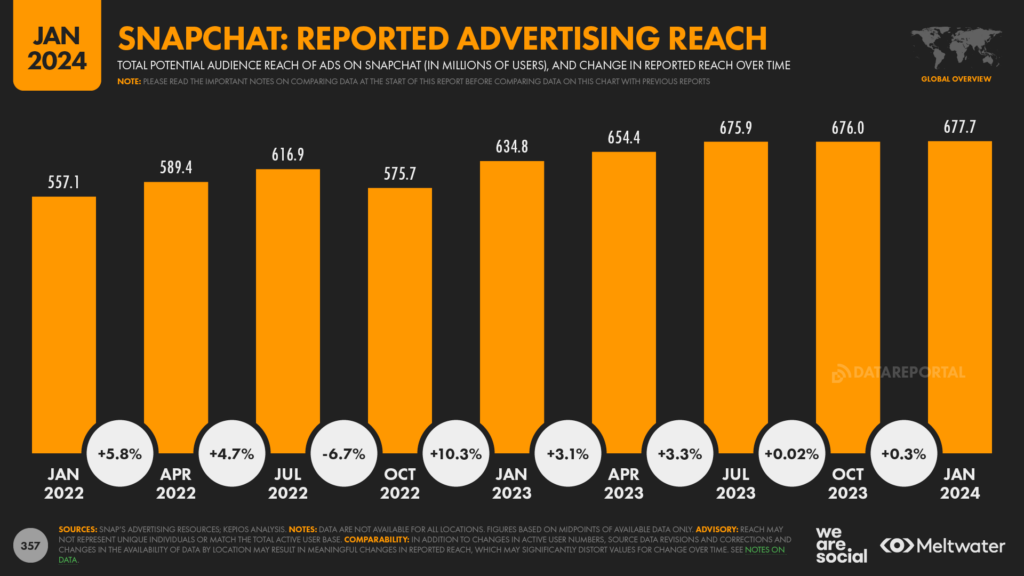

Meanwhile, Snapchat’s advertising reach has also seen meaningful growth over the past year.

The latest figures reported in Snap’s advertising resources indicate that marketers can now reach more than 677 million users via ads on the platform each month, which is 6.8 percent higher than the figure we reported this time last year.

The reported data suggests that Snapchat’s audience growth has remained relatively flat for the past six months, so we’ll be keeping an eye on these figures over the coming quarters.

However, 677 million is already an impressive audience, and Snapchat is still very much a compelling option for marketers.

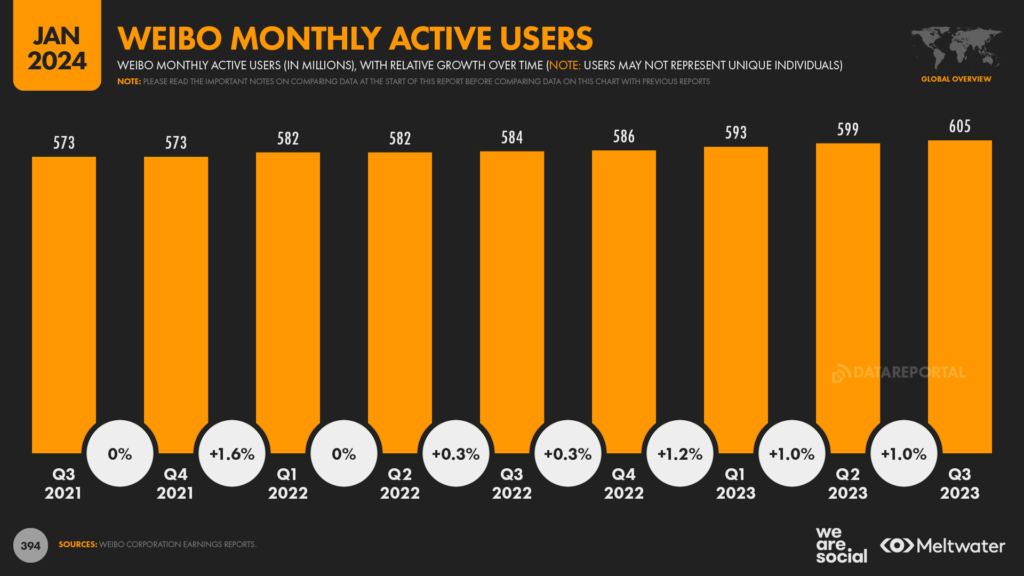

Weibo breaks 600 million

Returning to China, Weibo’s audience has been inching up over recent months, and the company’s latest earnings report reveals that the platform now has more than 600 million monthly active users.

The platform’s total active audience stood at 605 million at the end of Q3 2023, with that figure 3.6 percent higher than the total for the same period one year prior.

Weibo appears to be even more reliant on domestic users than WeChat is, but the company’s latest MAU figures suggest that more than half of China’s internet users may already use the platform each month.

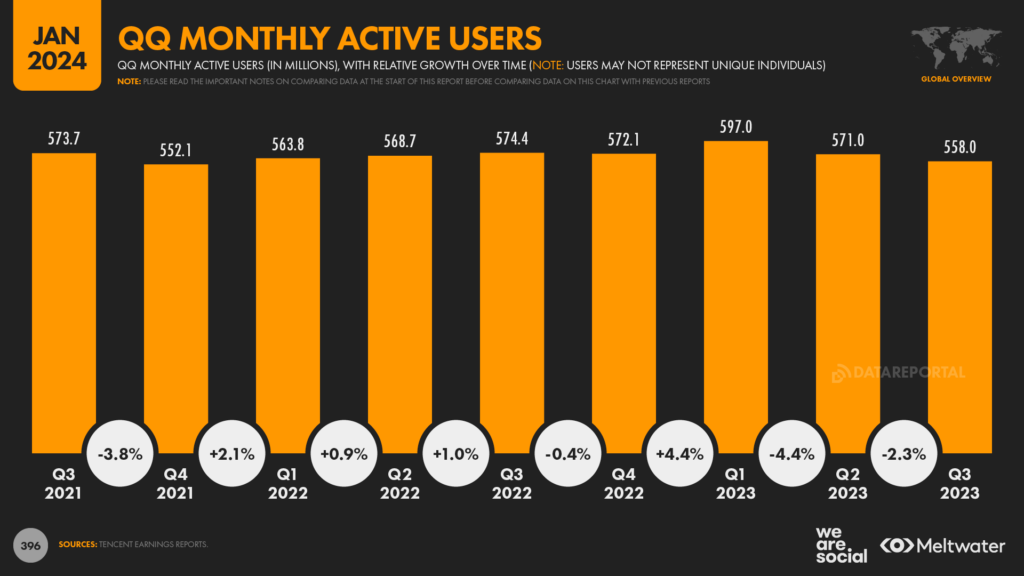

Moreover, the latest data suggest that Weibo is now comfortably ahead of QQ.

QQ used to be China’s dominant social platform, but the platform has lost 16 million active users over the past year, whereas Weibo’s active audience has grown by 21 million during the same period.

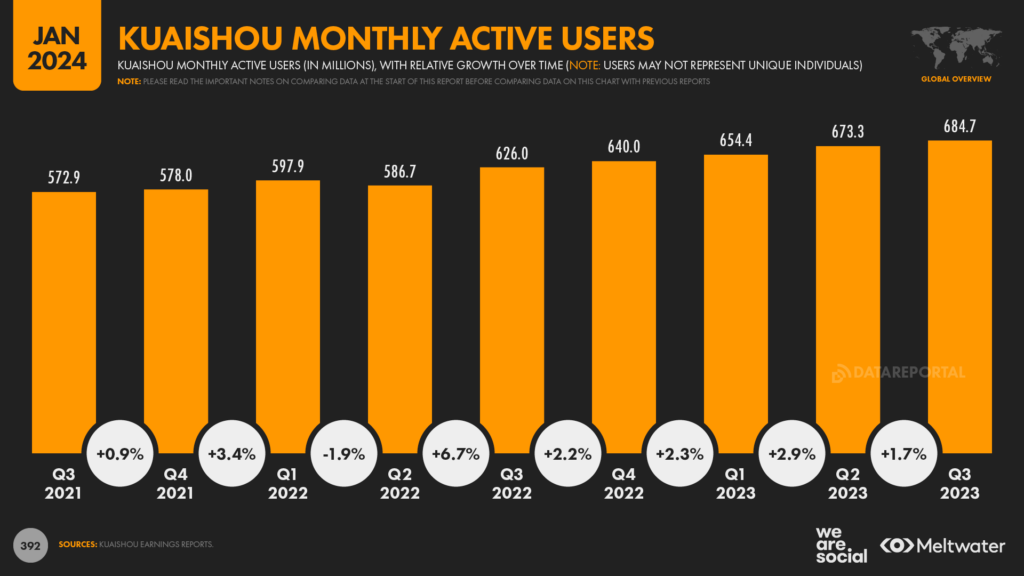

Kuaishou use increasing

Meanwhile, Kuaishou is another platform that has gained significant momentum over recent months, and the platform now boasts more than 680 million monthly active users around the world.

The platform’s domestic market remains its most important, and GWI’s latest research suggests that China is still home to more than three-quarters of Kuaishou’s total user base.

However, the “Kwai” app has built a sizeable audience in Brazil, while its “Snack Video” sibling – which is ostensibly the same platform, but with a different “wrapper” – has built meaningful momentum in Indonesia and Pakistan.

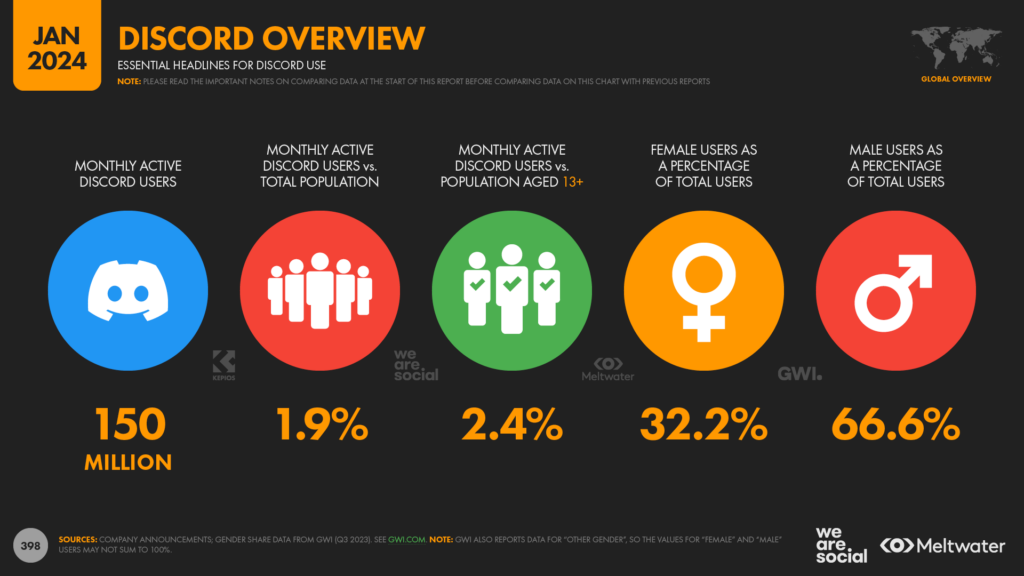

Discord striking a chord

Community platform Discord hasn’t published an updated user total during the past year, but our analysis of third-party data suggests that the platform’s active user base has grown significantly over recent months.

The company’s website still states that Discord has 150 million monthly active users, but Kepios analysis of data from reputable third parties including data.ai, Semrush, and Similarweb suggests that Discord may attract well in excess of 300 million active users each month.

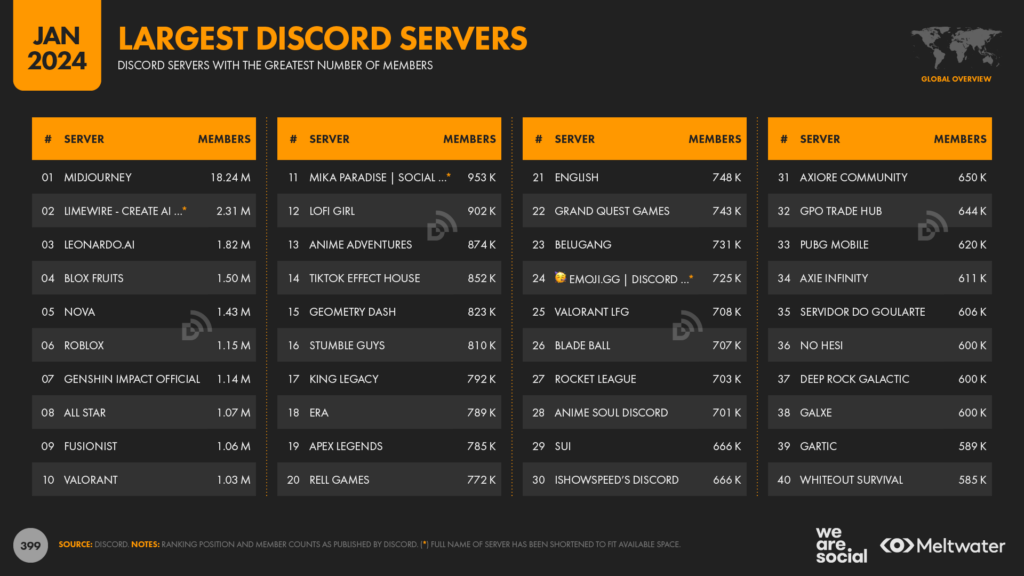

Alongside its continued popularity amongst gaming communities, the platform’s rapid ascent over recent months has also been fuelled by its association with Midjourney, which has grown to become one of the world’s most popular AI image generation tools.

Indeed, Discord’s own ranking of its many millions of “servers” puts Midjourney firmly at the top, with the AI tool claiming more than 7 times as many members as second-ranked Limewire, which also happens to be AI focused.

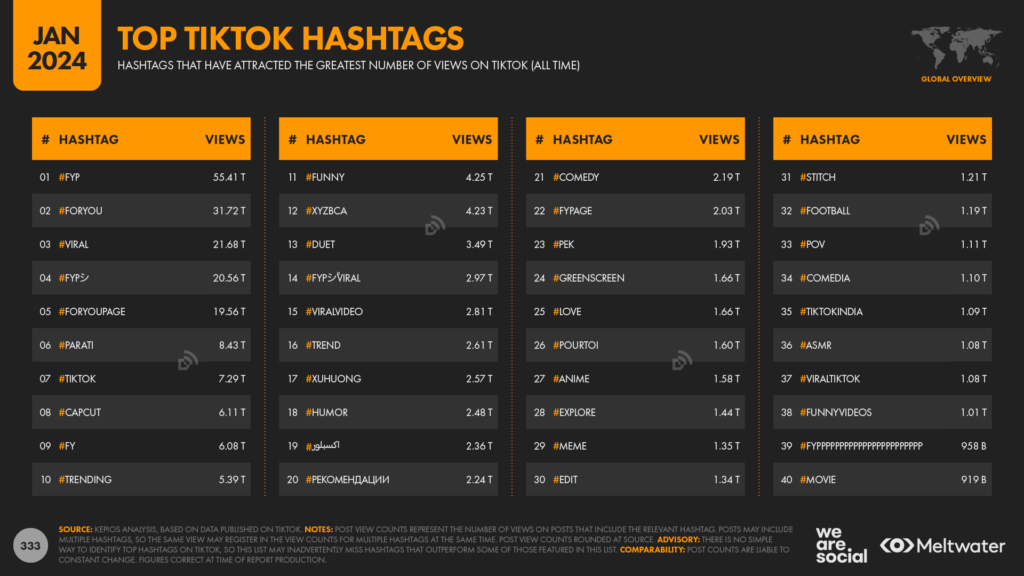

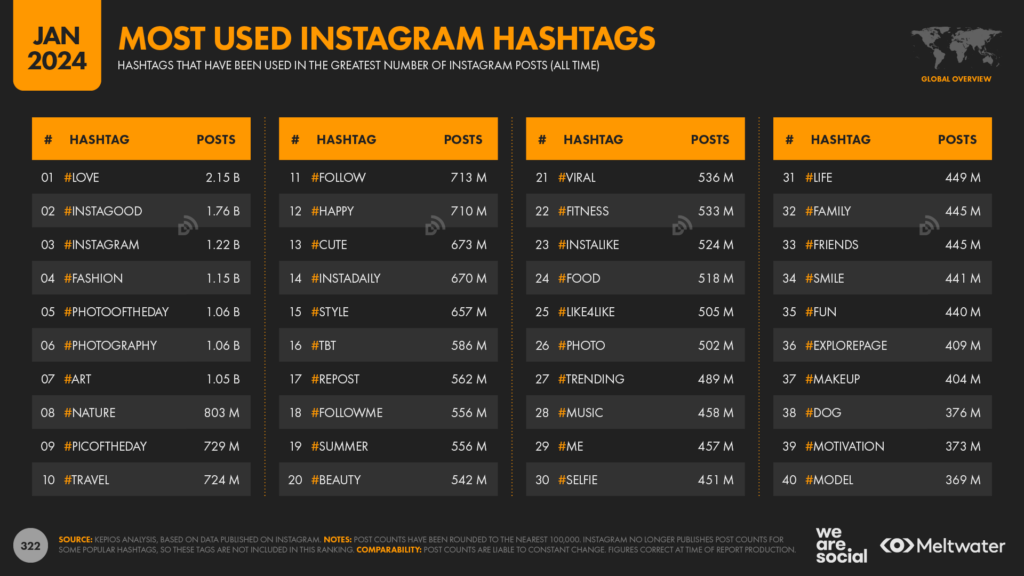

The wonderful world of TikTok hashtags

One of the most fascinating – and perhaps perplexing – datasets in this year’s report relates to TikTok hashtags.

Just before we dive into the data, it’s important to highlight that there’s no “official” list of the platform’s top tags, nor is there any easy way to identify which ones garner the most attention.

As a result, this research required an incredibly laborious, manual trawl, and there’s every chance that we’ve missed one or two hashtags that should have featured in this ranking (side note: if you know of one that’s missing, please let me know).

Caveats aside though, this data offers a real treasure trove of insight and inspiration for cultural observers and marketers alike.

It’s all for you

First up, the obvious winner: #fyp.

This initialism of “for your page” has long been the most popular hashtag on the platform, and is still used by TikTokers everywhere in the hopes of getting their clips featured in the platform’s main feed.

And this ubiquity has resulted in some truly staggering results.

Data published on the platform itself suggests that TikToks tagged with #fyp have amassed a total of 55½ trillion views.

Yes, you read that correctly: trillion.

For perspective, even if each of those views only lasted for one second, the combined total would equate to 1.76 million years.

But #fyp isn’t the only hashtag delivering eye-watering view counts.

TikTok’s top tags

All of the hashtags in our top 10 have attracted more than 5 trillion views, and tags will soon require more than 1 trillion views in order to qualify for the top 40.

Many videos feature a combination of these tags though, so adding them all up doesn’t offer a representative total.

However, just for perspective, the combined view count across the top 10 tags comes to a massive 182,000,000,000,000.

But endless strings of zeros aside, what can we learn from this data?

It’s not all in English…

Well, one of our most interesting discoveries is that many of the top hashtags use languages other than English.

Interestingly, we’ve not seen this phenomenon gain nearly as much traction on other platforms, and it appears as though all of the top hashtags on Instagram are still in English.

Moreover, none of the TikTok hashtag guides that we read across the internet whilst preparing this research even mention this tendency to polyglotism.

So, let’s take a closer look at which non-English tags have gained the most momentum on TikTok so far.

…but it’s still (almost) all for you

First up, the Spanish-language equivalent of “for you” – #parati – is the most widely used non-English hashtag on TikTok today, garnering a hefty combined view count of 8.43 trillion.

[Side note for the pedants: it could be argued that the use of the Japanese katakana character, “ツ” – pronounced “tsu” – in #fypツ qualifies that hashtag as the top “non-English” entry, but this character’s popularity stems from its resemblance to a smiling face, and there’s no obvious use of the Japanese language in this particular instance, so I decided to ignore it].

Next up is #xuhuong, which likely relates to the Vietnamese words “xu hướng”, meaning “trend” (note that #trending and #trend both appear as English tags within the top 40 as well).

For context, TikTok reports close to 68 million users in Vietnam, making it the platform’s fifth-largest country audience.

#Xuhuong is particularly popular amongst users in South-East Asia, and posts featuring this tag have amassed an impressive 2.57 trillion combined views.

However, our analysis shows that use of the #xuhuong tag isn’t limited to Vietnamese users.

The third-most popular non-English tag on TikTok is the Arabic #اكسبلور.

However, this tag is an interesting one, because it’s a phonetic transliteration of the word “explore” in English, and isn’t actually a “standard” Arabic word.

It’s also worth highlighting that this Arabic rendering of “explore” has had more success than the English-language #explore has, with the Arabic version attracting almost a trillion more views.

And for added context, it’s worth noting that #اكسبلور has also gained meaningful momentum on Instagram, where it has been used in more than 125 million posts.

Next up in our TikTok tag ranking is the Cyrillic #рекомендации, closely followed by its derivative form, #рек.

The longer tag is the Russian word for “recommendation”, and posts with this tag had attracted 2.24 trillion views by the time we compiled this list.

And for added perspective, TikTok’s latest data indicate that the platform has 58.6 million users in Russia, placing it sixth in our TikTok country ranking.

#Рек literally translates to “rivers” in English, but in this case, TikTok users are likely using it as an abbreviation of “рекомендации”.

However, use of this particular abbreviation may also reflect a subtle nod to the “flow” – or “feed” – of content on TikTok’s “For You Page” [I may be reading far too much into that of course, but the nerd in me can’t resist].

Next in our ranking of the most popular non-English tags is #pourtoi, which is the French-language equivalent of “for you”, while #comedia – the Spanish-language word for “comedy” – rounds out this list of non-english tags.

But there are still a few more tags in the top 40 that are worthy of our attention.

Make me famous

For the uninitiated, one of the most confusing tags in this list might be #xyzbca.

With a total of 4.23 trillion combined views, the tag has clearly been used a huge number of times, but the characters themselves don’t actually have any meaning.

Analysing the potential origins of this tag is probably a bit cringe – it’s quite probably entirely random – but for a Gen Xer like me, it’s vaguely reminiscent of cheat codes from old video games.

But if that sounds like a stretch, remember why people are using these tags: to “go viral”.

And if me writing “go viral” also sounds cringe, take a look at tags 3, 14, and 15 in our top 40 list.

Oh, and #goviral has also amassed more than 880 billion views, so – while it doesn’t quite qualify for the top 40 – it’s not far off it.

Moreover, the likelihood of “going viral” on TikTok today is somewhat akin to winning the lottery, so perhaps a “cheat code” isn’t a bad analogy.

However, the standout entry for me in this ranking of top TikTok tags is #fyppppppppppppppppppppppp.

No, I didn’t fall asleep with my finger on the keyboard; that hashtag really is “fy” followed by 23 Ps, and yes, it really has attracted more than 958billion views.

But why 23 Ps and not 22 or 24, you ask?

Beats me.

If you know, I’d genuinely love to know the answer. Drop me a note.

Wrapping up

That’s almost all for this year’s analysis – thanks for making it through 10,000+ words so far! – but you might like to know that we’ll start publishing our Digital 2024 local country reports towards the end of February.

We’ll share those as soon as they’re ready, but if you’re worried you might have missed something, head over to our complete Global Digital Reports library, where you’ll be able to find everything you need.

And just in case you want even more analysis, be sure to check out our complete collection of Digital 2024 Deep Dive articles – you can find all of those here.

But just before you go…

And finally…

We spent a lot of time earlier in this analysis exploring the ongoing battle for supremacy between Instagram and TikTok.

However, a far more storied battle has been taking place across the internet over the past 12 months.

Unlike that social media story though, this battle has a clear winner… at least for this year.

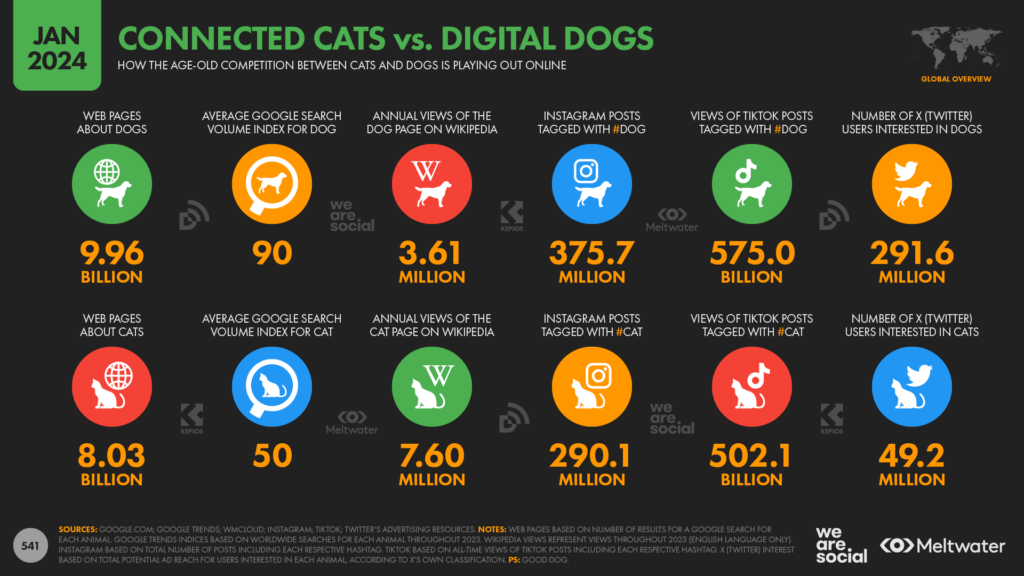

When it comes to digital today, it’s all about the dogs.

Some people may tell you that the internet was invented for cats, but – even if that assertion might have held water back in the 90s – canines are well and truly top dog as we enter 2024.

Even a cursory glance at Google search results will tell you that dogs are ahead, with the world’s top search engine returning close to 10 billion pages for “dog”, compared with just 8 billion for “cat”.

You might pawsit that cats could simply do with better SEO, but it turns out that ranking on the first page of Google probably isn’t felines’ top frustration.

Indeed, our careful analysis of data published by Google Trends reveals that today’s internet users are 80 percent more likely to search for Dogs than they are to search for Cats.

And yes, for the G-Trends nerds out there, we used broad search terms for this analysis rather than specific keywords, and we also took a worldwide view across the past 12 months as our base.

Cats appear to have the upper hand paw when it comes to Wikipedia though, and the number of people visiting the main page for Cats outnumbers those visiting the main Dog page by a ratio of more than two to one.

It appears as though supporters of Felis catus have been hard at work too, with the genus’s Wikipedia page now available in 262 languages, compared with Canis lupus familiaris’s 260.

Editors have also made significantly more lifetime edits to the Cat Wikipedia page, outnumbering edits to the Dog page by 15,170 to 12,535.

Perhaps surprisingly though, the Dog page appeared on Wikipedia before the Cat page did – by a whole 34 days.

However, Wikipedia was the only triumph for cats in 2023, and when it comes to social media, dogs win – hands paws down.

For context, Instagram users have published almost 376 million posts to the platform tagged with #dog, compared with just 290 million tagged with #cat.

And the #DogsOfTikTok are winning too.

TikToks tagged with #dog have garnered a massive 575 billion views, compared with 502 billion for TikToks tagged with #cat.

And just as an aside, this data reveals that the world has collectively viewed posts tagged with either #dog or #cat more than 1 trillion times.

Yes, you read that right: it’s ’rillion, with a “T”.

Meanwhile, the dogs are even winning on X.

We’re fully expecting raucous claims of bot activity and accusations of political bias here, but the numbers don’t lie: the platform-formerly-known-as-Twitter’s own advertising resources reveal that a hefty 291.6 million X users are “interested in” dogs, compared with a meagre 49.2 million users who are “interested in” cats.

So, what’s the overall conclusion here?

Well, if you represent #TeamDog, it’s perhaps time to freshen up that Wikipedia page, and convert your social media presence into tangible traffic and results.

However, if you’re on the side of #TeamCat… well, it may be time for a new agency. If you need any ideas, I have the purrfect suggestion.

That’s all from me for this year’s flagship analysis, but I’ll be back on your screens in just a few short weeks to bring you the first of our Digital 2024 Quarterly Statshot Reports.

Reports

Reports