The global digital landscape is still evolving rapidly as we enter the second half of 2020, with the ongoing Coronavirus pandemic continuing to influence and reshape various aspects of people’s daily lives.

Lockdowns may have been lifted across many countries, but many of the new digital behaviours that people adopted during confinement have endured, resulting in meaningful increases in various kinds of digital activity.

For context, Akamai reports that global internet traffic has grown by as much as 30 percent this year, while research from GlobalWebIndex shows that we’re still spending considerably more time using connected tech than we were at the start of 2020.

All of this increased activity has resulted in some important milestones and trends in our new Digital 2020 July Global Statshot report, which we produce in partnership with Hootsuite.

Key headlines this quarter include:

More than half of the world now uses social media

Many digital habits formed during lockdown have endured, despite the easing of restrictions

Global TikTok use has surged, but future growth may be more challenging

Instagram has reached a big new audience milestone

Search behaviours are evolving, with important implications for brands

This is our most comprehensive quarterly report to date, with more than 150 charts of rich data and trends. You’ll find all of those charts for free in the SlideShare embed below (click here if that’s not working for you), but read on below for my in-depth analysis of this quarter’s key stories.

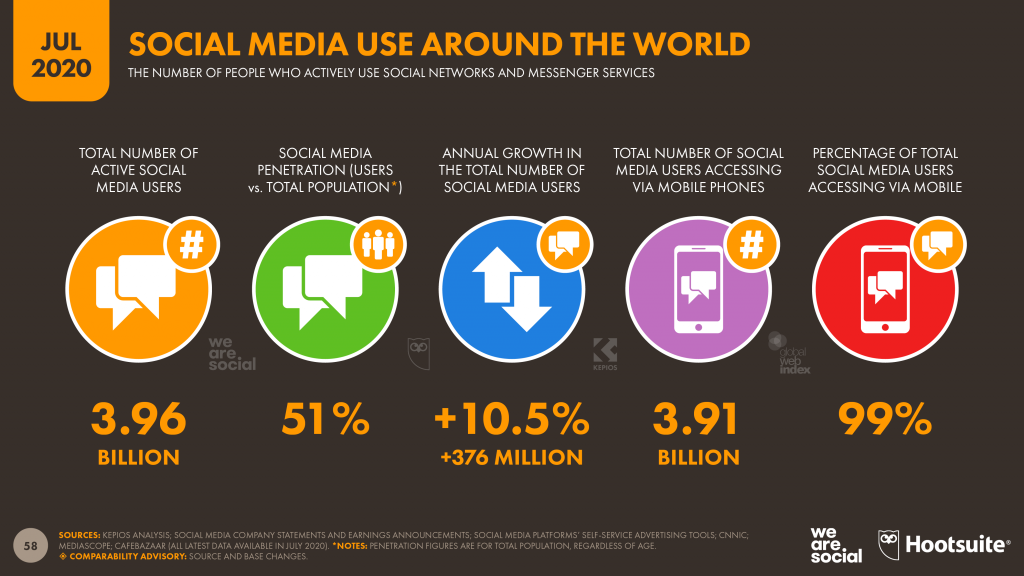

Top story: more than half the world now uses social media

Social media users have grown by more than 10 percent over the past year, taking the global total to 3.96 billion by the start of July 2020.

This means that – for the first time – more than half of the world’s population now uses social media, with more people using social media than not.

Growth trends indicate that an average of more than 1 million people started using social media for the first time every single day over the past 12 months, equating to almost 12 new users every second.

What’s more, the pace of growth appears to have accelerated in recent months, despite the global total having already passed the halfway mark.

COVID-19-related lockdowns may have played a role in this increased adoption, but many of the data points that feed our global total were last updated in Q1, so there’s a reasonable chance that we’ll see rapid growth in our next Statshot report too.

Given the significance of this milestone, we’ve produced a comprehensive analysis of the global state of social media, which you can read in full here.

Essential headlines

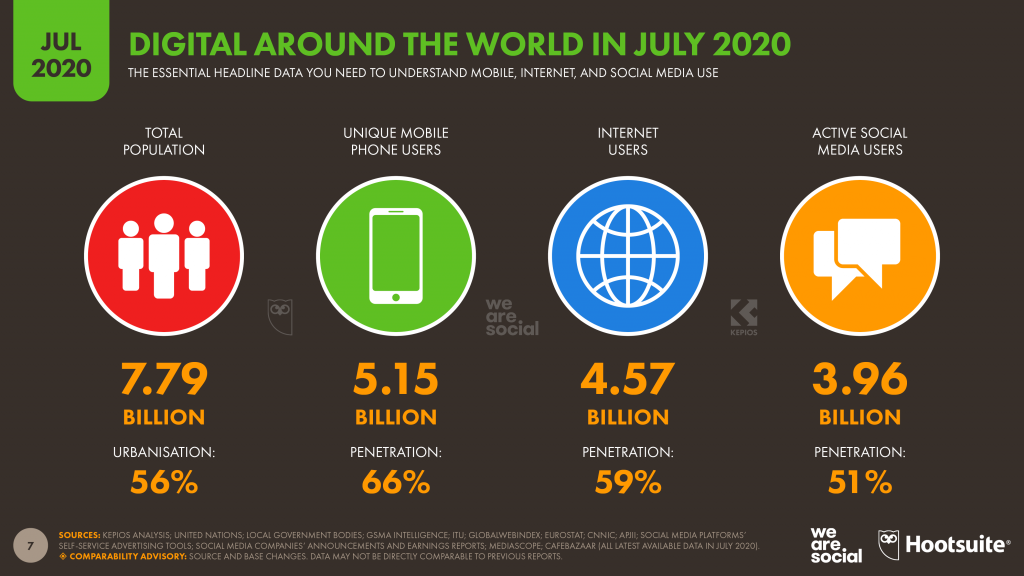

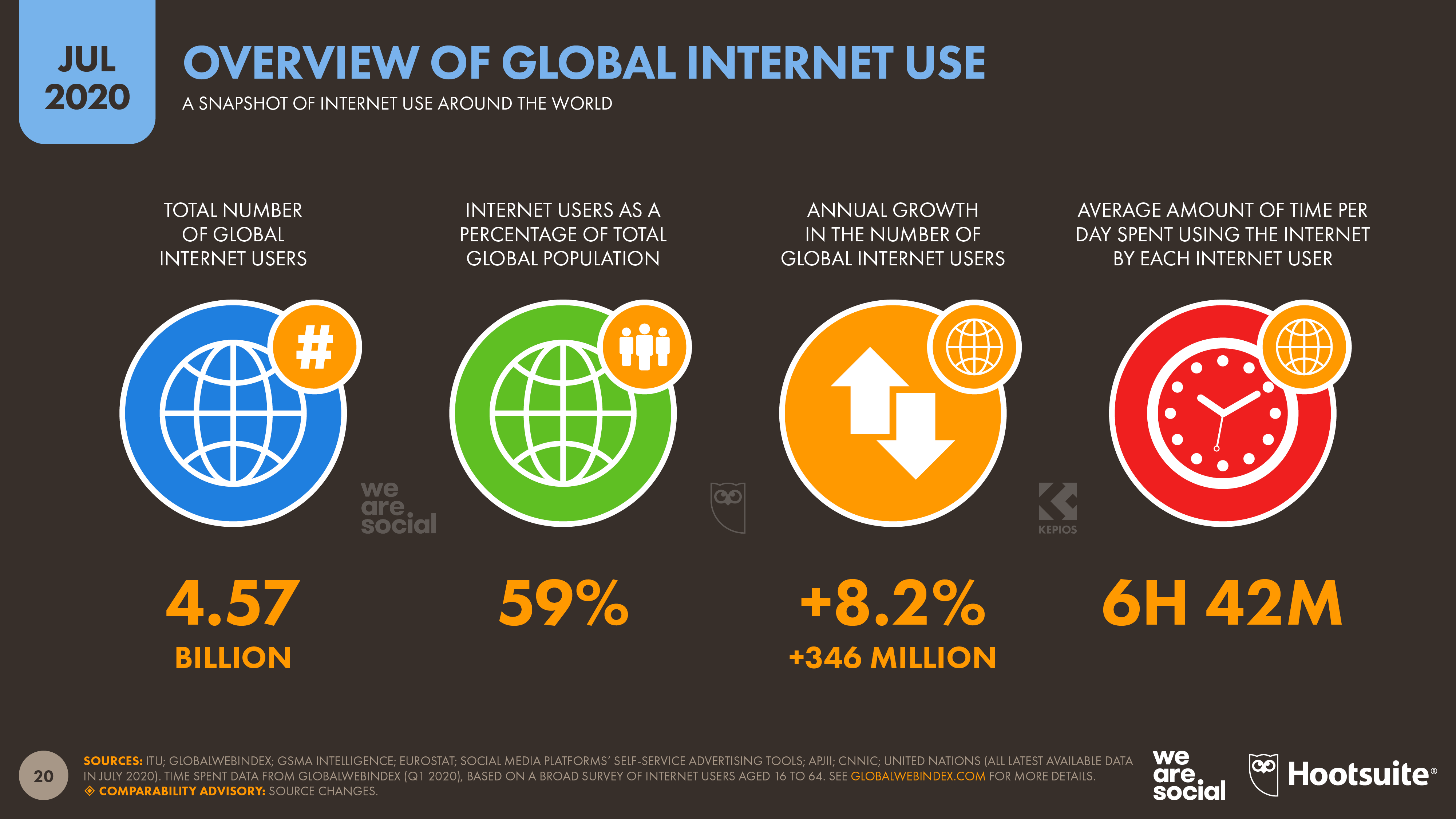

Internet user numbers continue to show strong growth as well, with our latest analysis revealing that 346 million people came online for the first time over the past year.

4.57 billion people around the world now use the internet, accounting for close to 60 percent of the world’s total population.

This is similar to the figure that we published back in April, but following conversations with both the ITU and GSMA Intelligence, we’ve made significant downward corrections to our internet user numbers for a handful of larger countries.

These corrections were triggered by a broader trend we’ve been tracking in internet user numbers, where some reports appear to show unrealistic growth over relatively short periods of time, resulting in figures that seem improbable given the demographic and socio-economic realities within the relevant countries.

However, even once we adjust historical figures for these source corrections, the latest data show that the number of global internet users continues to grow at a similar pace to the rates we’ve reported over our past few reports.

The global total grew by 346 million over the past 12 months, equating to year-on-year growth of more than 8 percent. On average, this means that roughly 11 new users come online for the first time every second since July 2019.

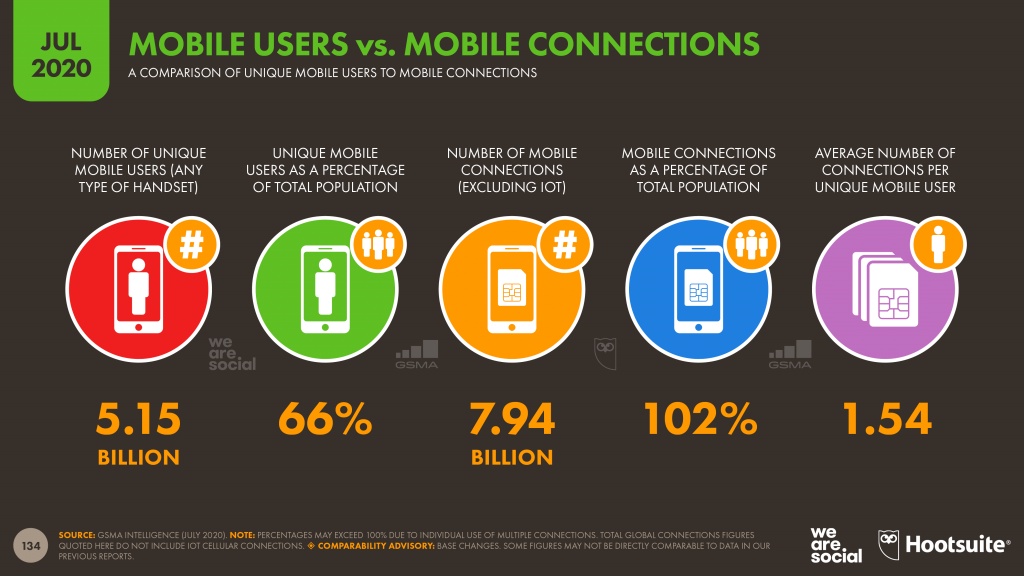

The figures we report for mobile phone users this quarter also appear to have remained static compared to the figures we published in April, but the latest data from GSMA Intelligence show that unique mobile users continue to grow, despite corrections to the overall total.

The organisation reports that mobile users have grown by 2.4 percent over the past year, although the pace of growth slowed in the first three months of 2020 to quarter-on-quarter growth of 0.5 percent.

This slowdown is likely due to the impact of Coronavirus lockdowns, especially in China, which contributes a sizeable share of overall global growth.

Increased use of connected tech continues

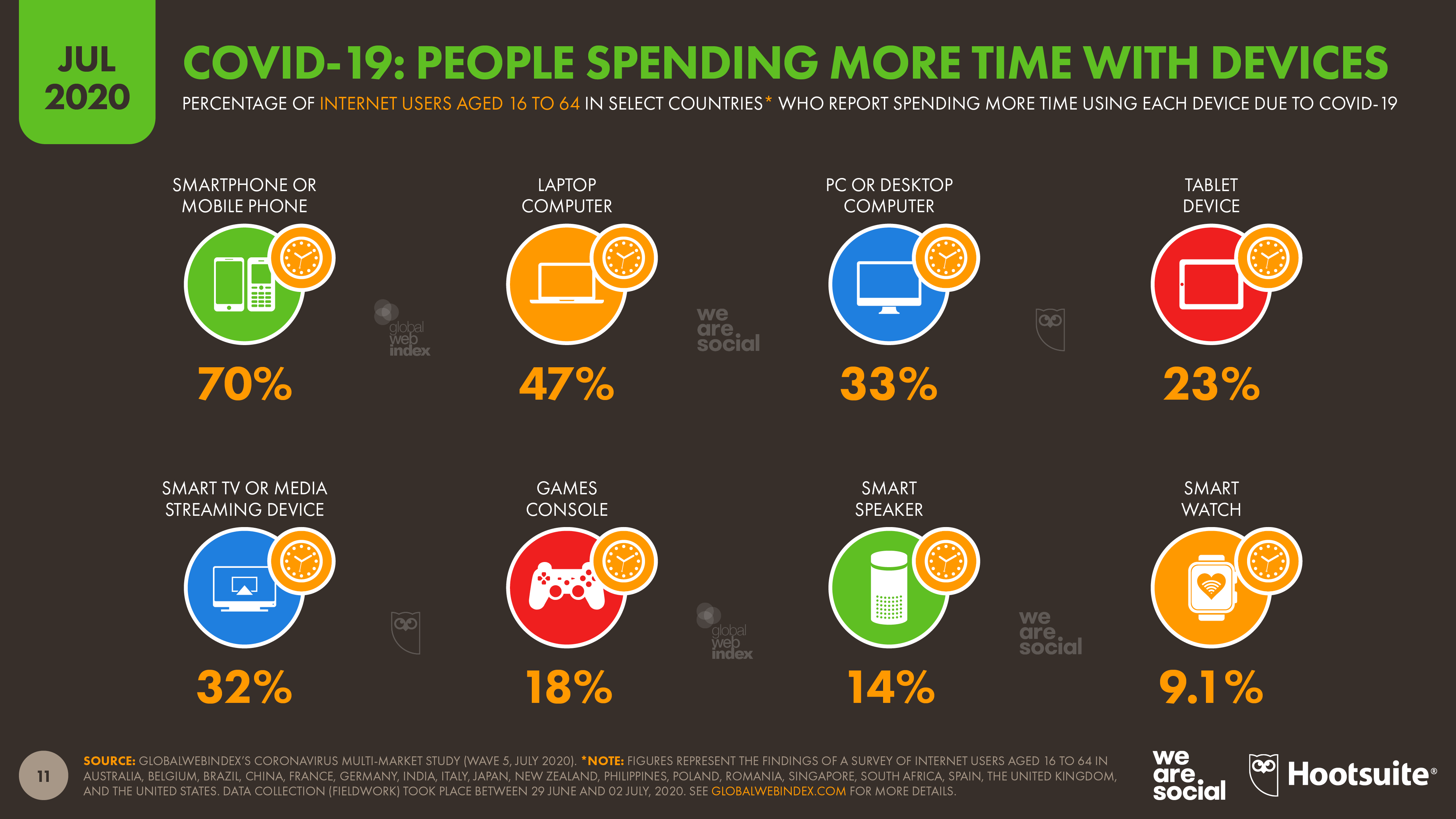

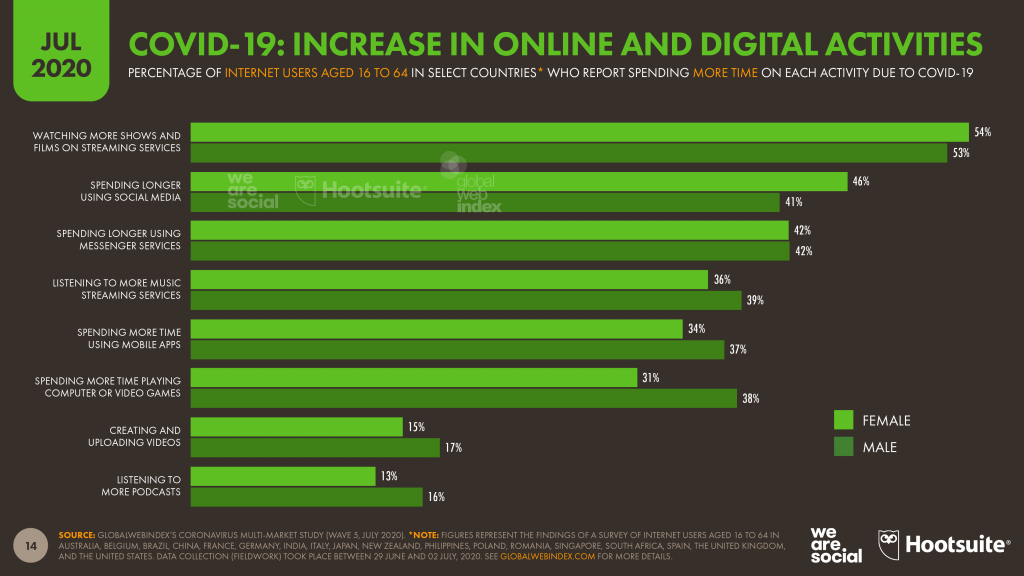

New research shows that the increased use of connected devices we reported in our April report continues today, despite many countries starting to lift the lockdown restrictions that triggered that initial surge in use.

The latest wave of GlobalWebIndex’s Coronavirus Multi Market Study finds that 7 in 10 internet users are still spending more time using mobile phones compared to pre-pandemic levels, while nearly half of us are still spending more time using laptops.

Meanwhile, our love affair with streaming continues, with more than half of GlobalWebIndex’s respondents saying that they’re still streaming more films and TV shows over the internet today than they did at the start of 2020.

Similarly, more than 4 in 10 internet users say that they’re still spending more time using social media, while 1 in 7 respondents say that they’re continuing to create and upload more video content.

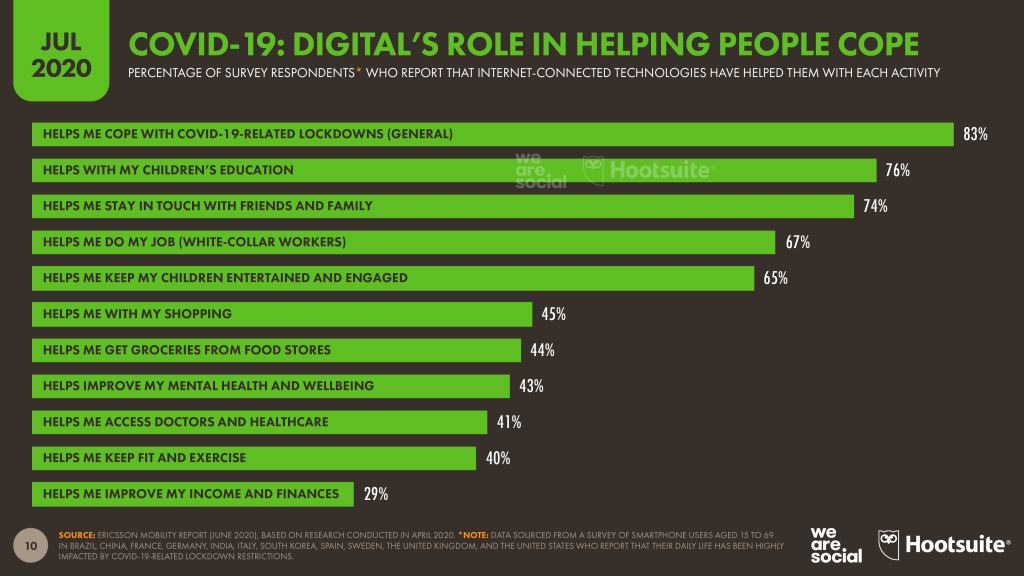

But connected tech hasn’t just been keeping people entertained during lockdown.

More than 8 in 10 mobile phone users surveyed by Ericsson that internet-connected technologies have helped them cope during the pandemic, enabling them to support their children’s education (76 percent), stay in touch with friends and family (74 percent), and even improve their mental health and wellbeing (43 percent).

Indeed, numerous stories have emerged over recent weeks highlighting the role that connected tech can play in combatting issues such as loneliness amongst the elderly.

So, while there’s plenty of evidence that excessive use of connected tech can be harmful, it’s worth remembering that the same technologies can also improve people’s quality of life.

Search behaviours are evolving

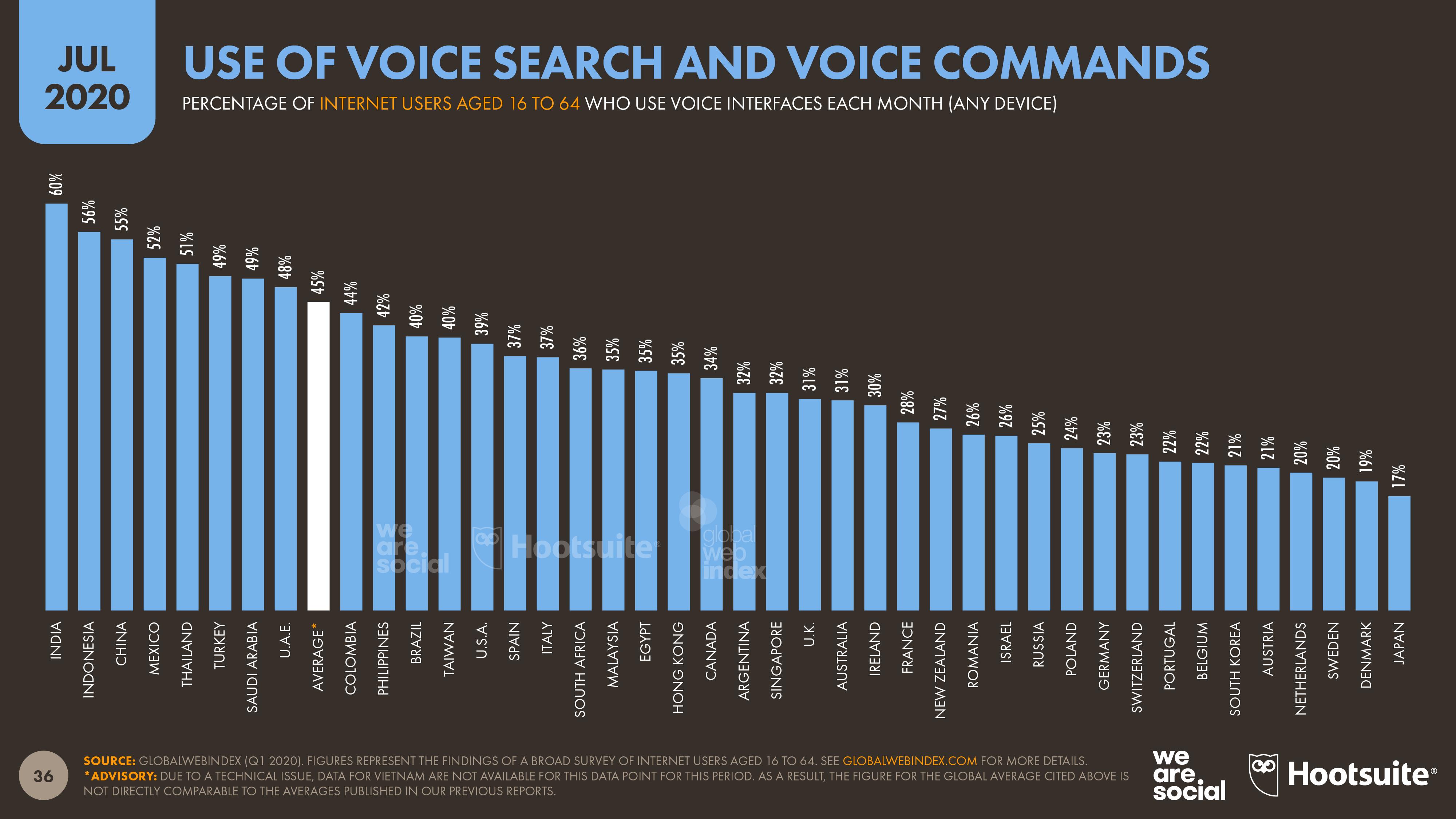

We’ve been tracking the rise of voice search and voice command for some time in our Global Digital Reports series, especially because of the sharp increases in use across some of the world’s fastest growing internet markets.

The latest data from GlobalWebIndex indicate that well over half of the internet users in India, China, and Indonesia now use voice tech each month, with 6 in 10 users in India saying that they used voice interfaces in the past 30 days.

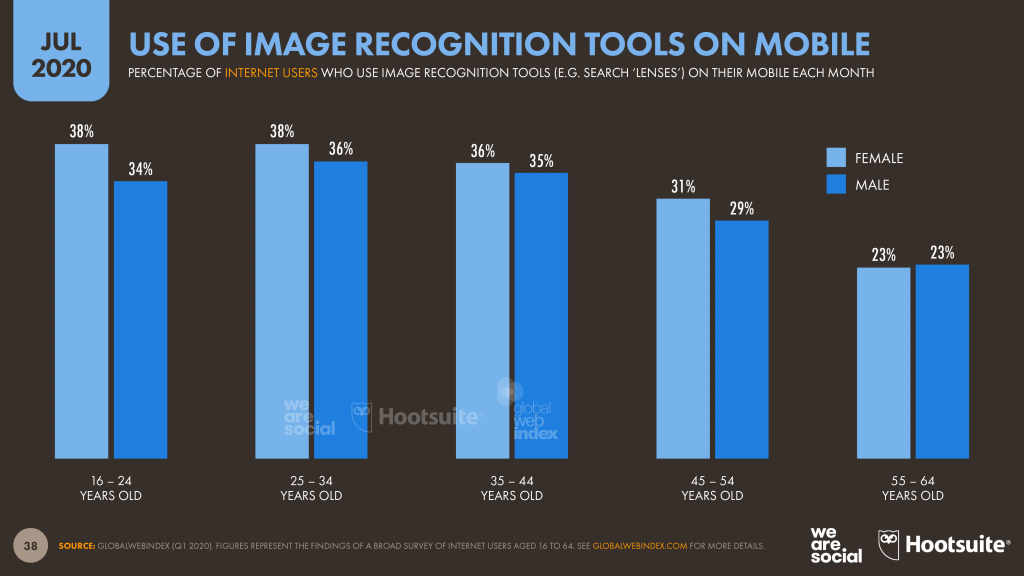

However, voice isn’t the only technology that’s reshaping search. GlobalWebIndex’s research also reveals that image recognition services such as Pinterest Lens and Google Lens have become increasingly important tools for internet users, especially amongst younger audiences.

More than one-third of internet users aged 16 to 64 report using image recognition tools in the past month, but that figure rises to almost 40 percent for women aged 16 to 34.

These tools are especially important when it comes to ecommerce, and have particular value for brands in aesthetically oriented categories such as fashion, home decor, and even consumer technology.

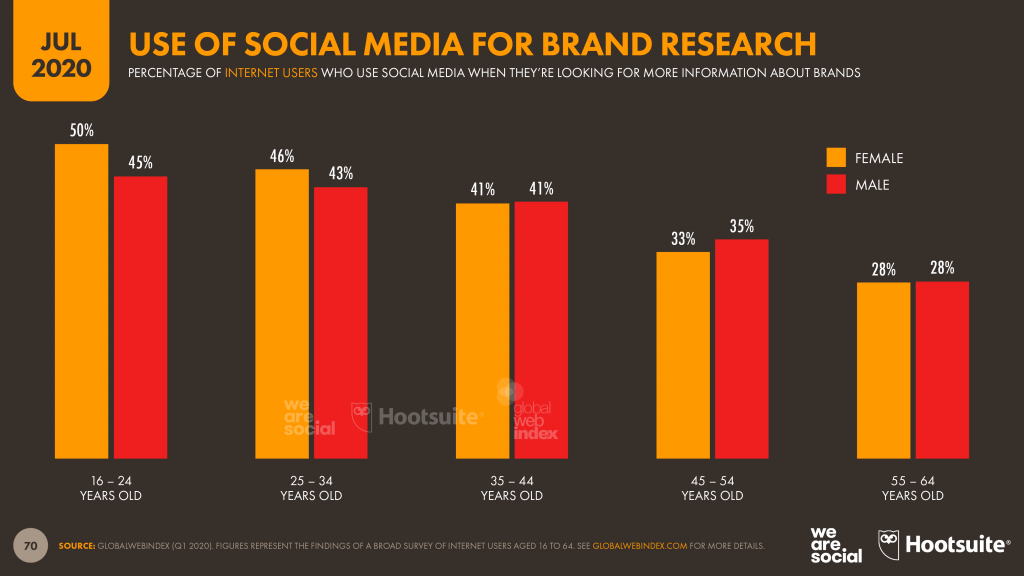

But perhaps the most significant change in search behaviours involves the online platforms that people use when they want to learn more about brands and products.

GlobalWebIndex finds that social networks are playing an increasingly important role in people’s brand research behaviours, and are now second only to search engines.

However, the overall gap between search engines and social networks has been steadily closing over recent months, pointing to an ongoing shift in how people look for information about the things they want to buy.

What’s more, social networks are now the top choice amongst internet users aged 16 to 24 when it comes to brand research – even ahead of search engines – with younger women particularly likely to turn to social media for their research needs.

With roughly 98 percent of internet users across all age groups using a search engine every month, there’s no doubt that these tools continue to play an essential role in people’s online activities. However, the latest data highlights the fact that people are using a wider variety of tools to help inform their purchase decisions.

As a result, it’s essential that marketers think more broadly about how audiences and consumers might want to discover and learn about their brands, and in particular, how they can weave search-friendly elements into their social media activities.

WFH: more evolution than revolution?

As COVID-19-related lockdowns took hold and hundreds of millions of people started working from home, variouspundits predicted the demise of the office.

However, the latest research indicates that tales of the office’s death appear to have been somewhat exaggerated.

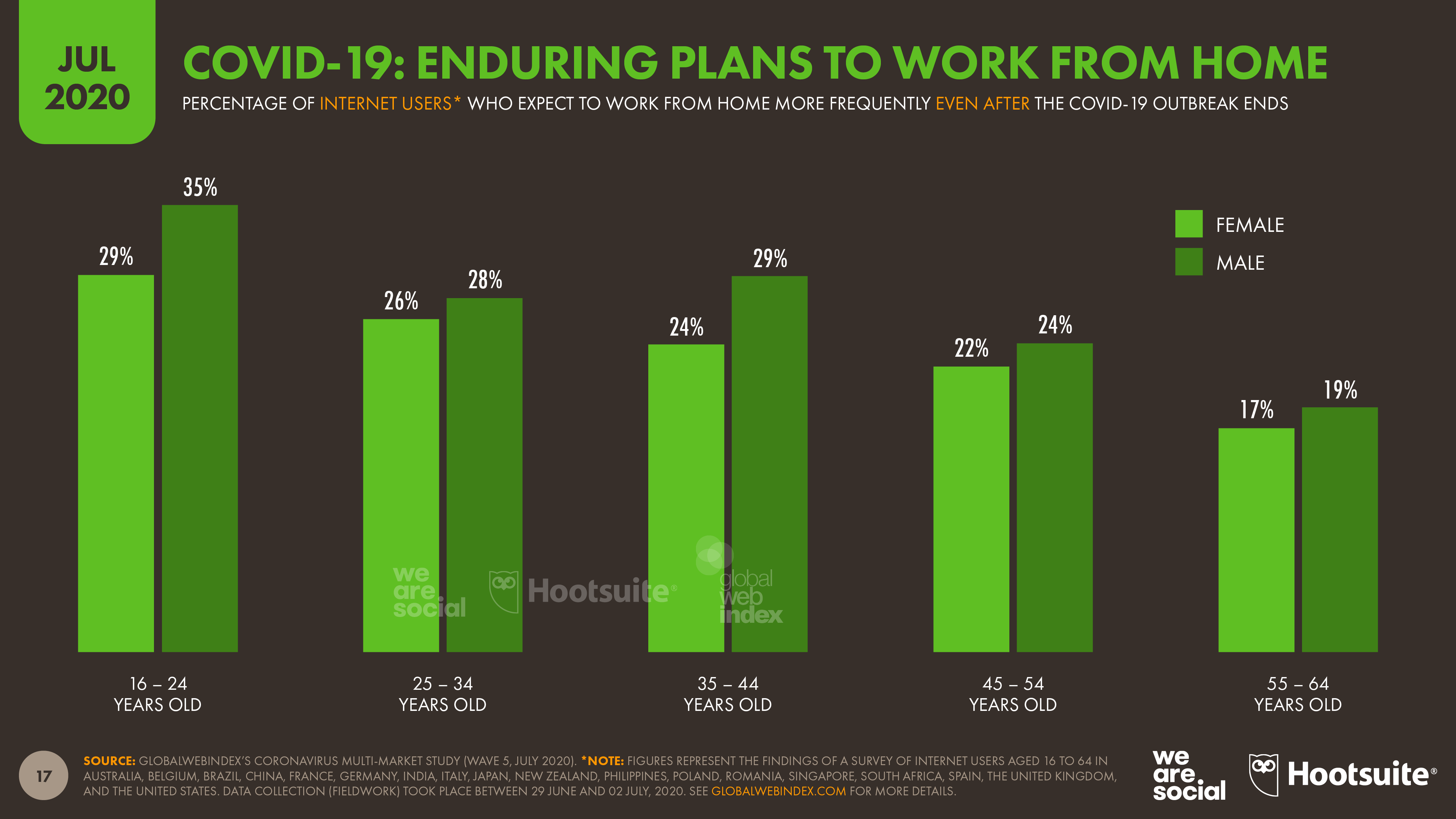

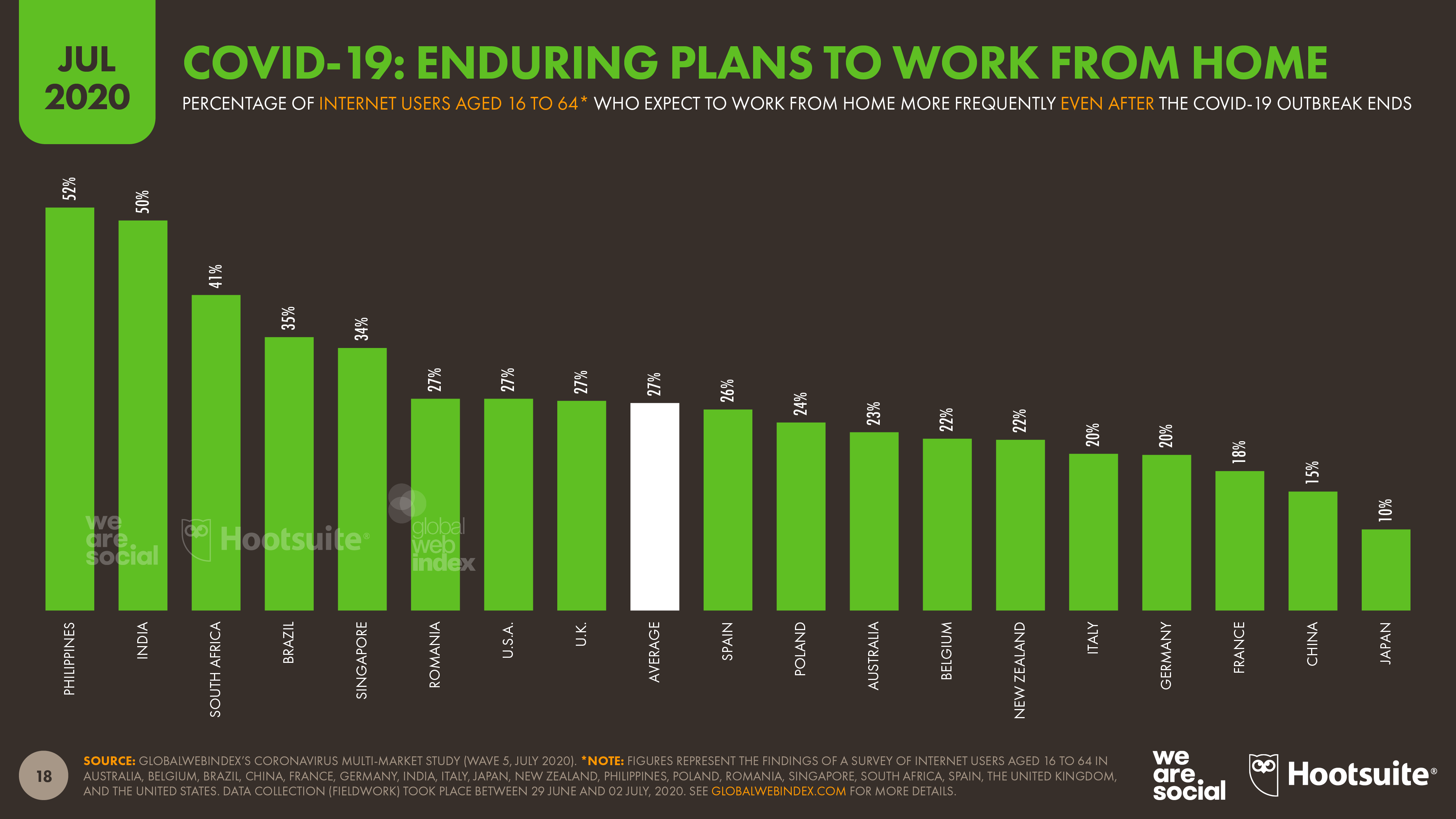

In a study conducted at the end of June, GlobalWebIndex found that just over a quarter of the world’s internet users expect to work from home more frequently after the pandemic has passed, compared to how often they worked from home before lockdown.

That figure varies considerably by country though, with more than half of respondents in India and the Philippines reporting that they expect ‘WFH’ to become a more common occurrence.

However, as with so many aspects of our digital lives, this change in behaviour won’t necessarily involve a binary shift.

In reality, lockdowns have helped many people and businesses understand how to adapt ‘working from home’ to their needs, but once social distancing eases there will still be plenty of occasions when people need to – or choose to – work from more communal settings.

As a result, the future of work is more likely to be ‘WFW’ than ‘WFH’ – i.e. working from wherever makes most sense given the context. In other words, just as “home is where the heart is”, so “work is where the wifi is”.

This evolution will have important implications for brands, especially those in the B2B space.

For example, products and services that enable people to work more efficiently and effectively from home – office chairs, computer monitors, team communication platforms, secure remote connections, etc. – may continue to enjoy increased demand over the coming months.

Similarly, new commercial opportunities may also arise as people’s WFH habits evolve and become more established.

These will vary by country and by culture, however, so be sure to check the latest findings for your country before getting too deep into planning.

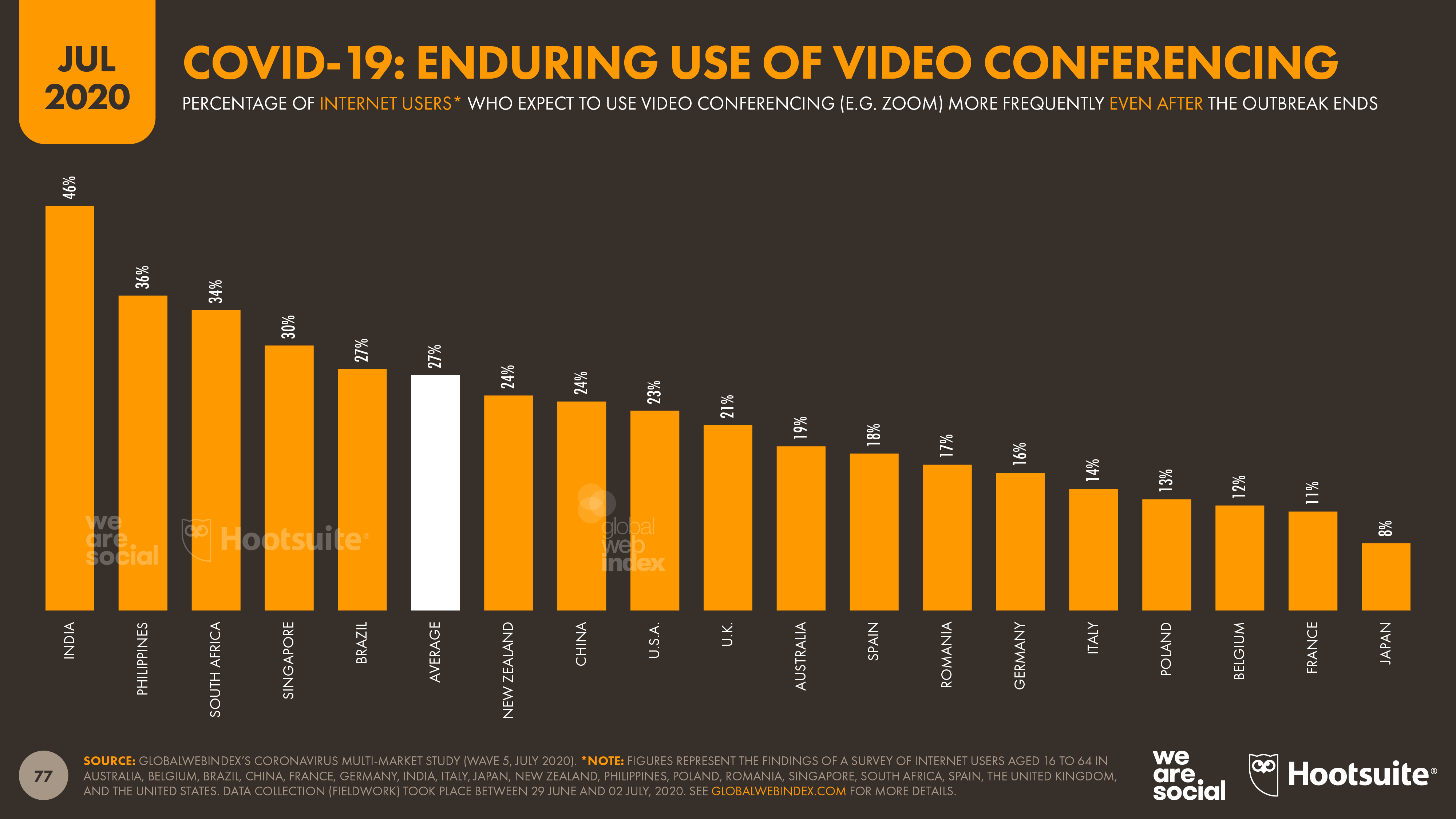

Video conferencing looks set to stay

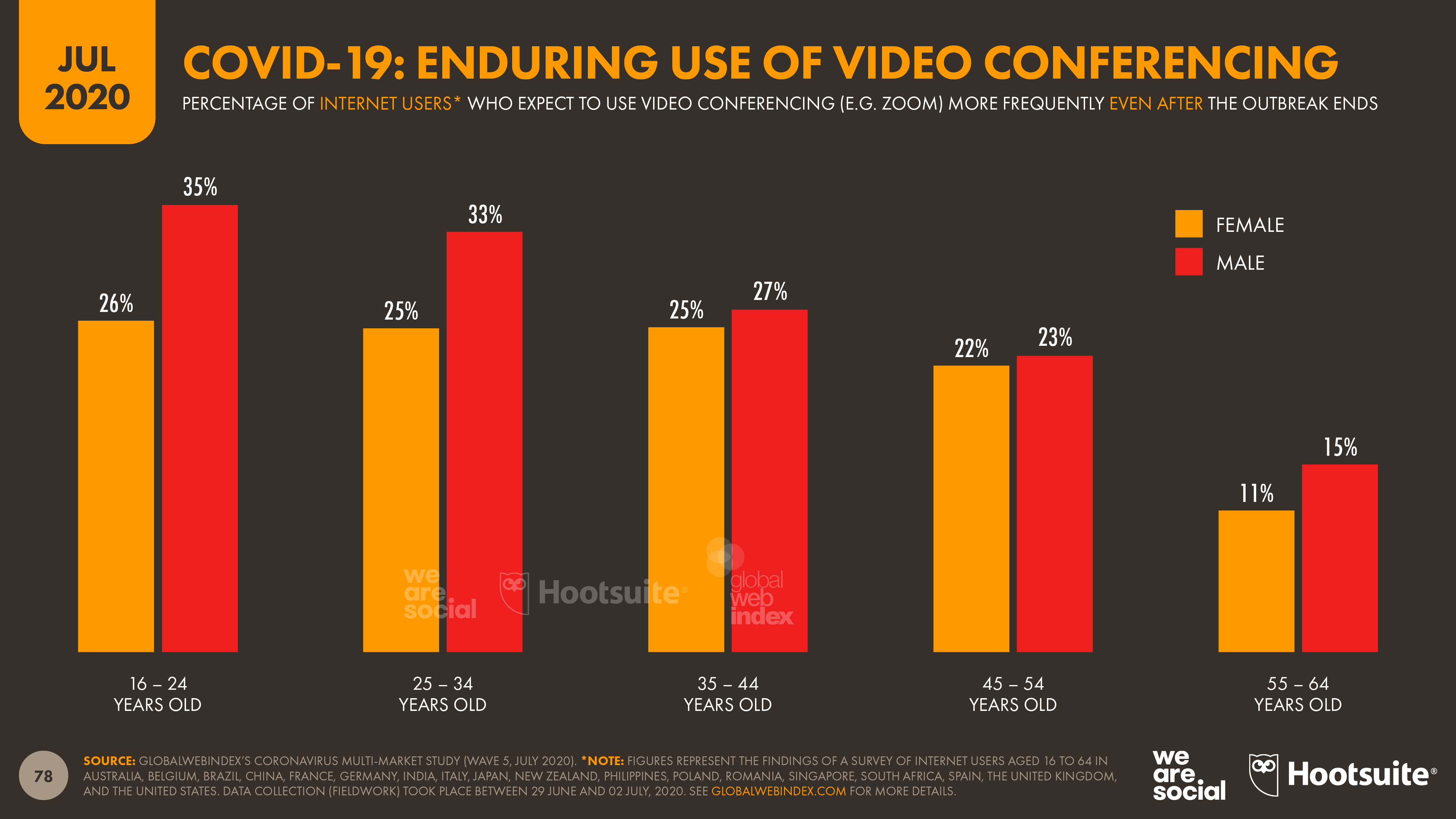

The enduring appeal of video conferencing appears to mirror people’s WFH expectations, with GlobalWebIndex’s research finding that just over a quarter of internet users expect to use these platforms and tools more frequently after the pandemic has passed, compared to their pre-COVID habits.

The research points to a fairly disparate range of expectations though, from less than 1 in 10 internet users in Japan expecting to meet over video in the future, to almost half of all internet users in India.

Interestingly, however, these differences do not appear to be determined by technological factors.

Indeed, Indian internet users seem to have embraced video conferencing and video calling more than users in any other nation, despite the fact that the country continues to be plagued by some of the slowest internet connections in the world.

Our reading of this data suggests that – as is so often the case in connected tech – adoption rates and digital activities are more likely to be determined by people’s age than by infrastructure.

On average, the higher a country’s median age, the less likely that country’s internet users are to foresee major, enduring changes to their digital behaviours as a result of recent events.

We can see support for this hypothesis in the global figures for increased use of video conferencing by age and gender as well, where the data shows a clear difference between the expectations of younger and older users.

Either way, the surge in the use of video conferencing has resulted in a variety of additions to people’s digital platform ‘portfolios’.

As we reported in our April report, Zoom appears to be one of the biggest beneficiaries of these new behaviours, but the platform is by no means the only tech brand that has seen its day-to-day use skyrocket over recent weeks.

While it’s safe to assume that increased use presents an exciting opportunity for these brands to grow their revenues, they may not be the only brands that will be able to capitalise on these new behaviours.

Zoom already promotes a selection of branded virtual backdrops on its website, and we’re guessing it may only be a matter of time before one of the larger platforms adopts an ad-funded video conferencing model for those users who haven’t signed up for paid packages.

Instagram and LinkedIn pass new milestones

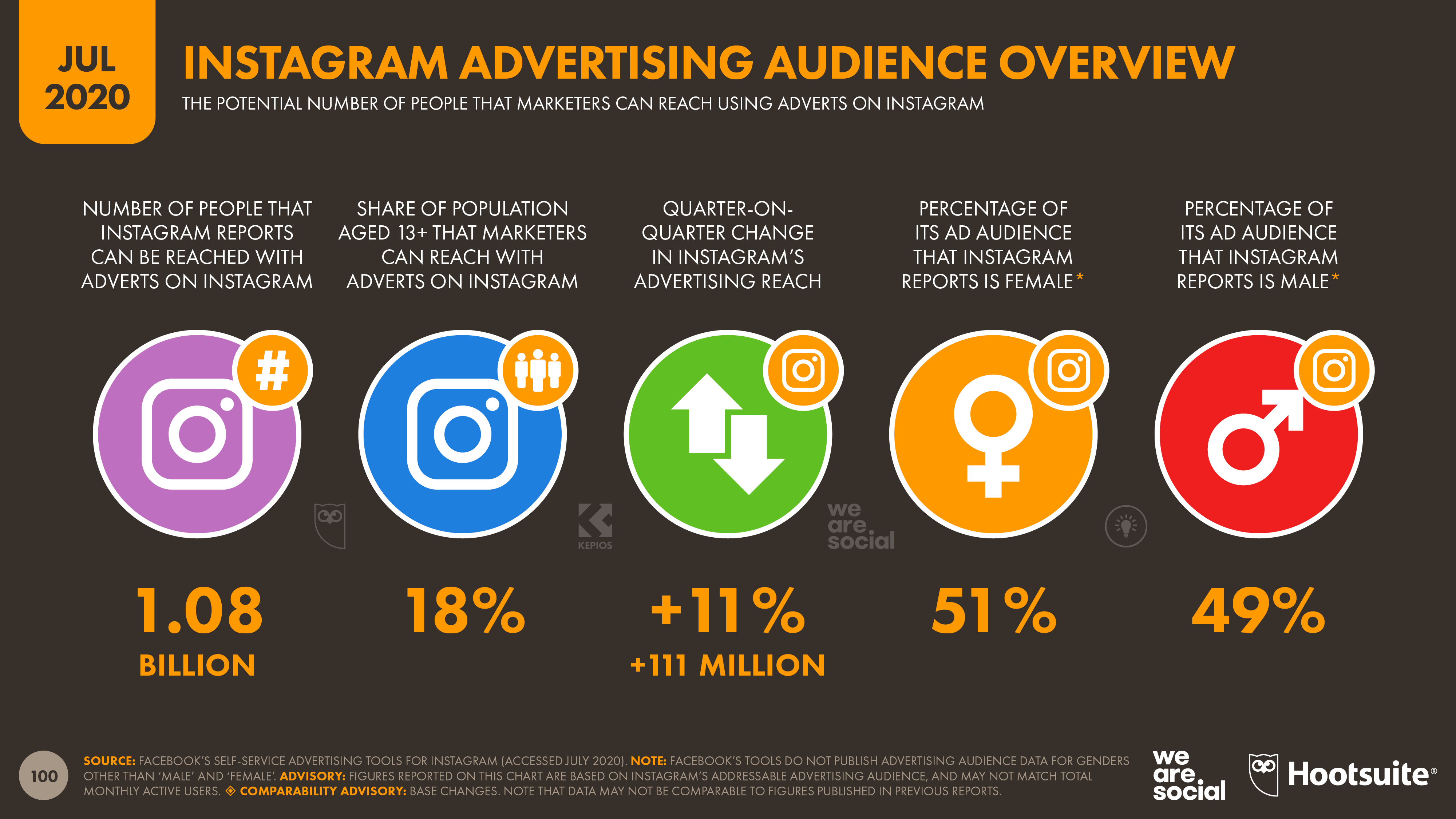

Facebook’s advertising tools show that brands can now reach more than 1 billion people using ads on Instagram.

The company’s latest data indicates that Instagram added 111 million new users to its advertising reach in the past quarter, equating to quarterly growth of more than 10 percent.

The figures mean that Instagram’s ad audience is currently growing at a rate of more than 1 million new users per day, resulting in global reach of 1.08 billion by early July 2020.

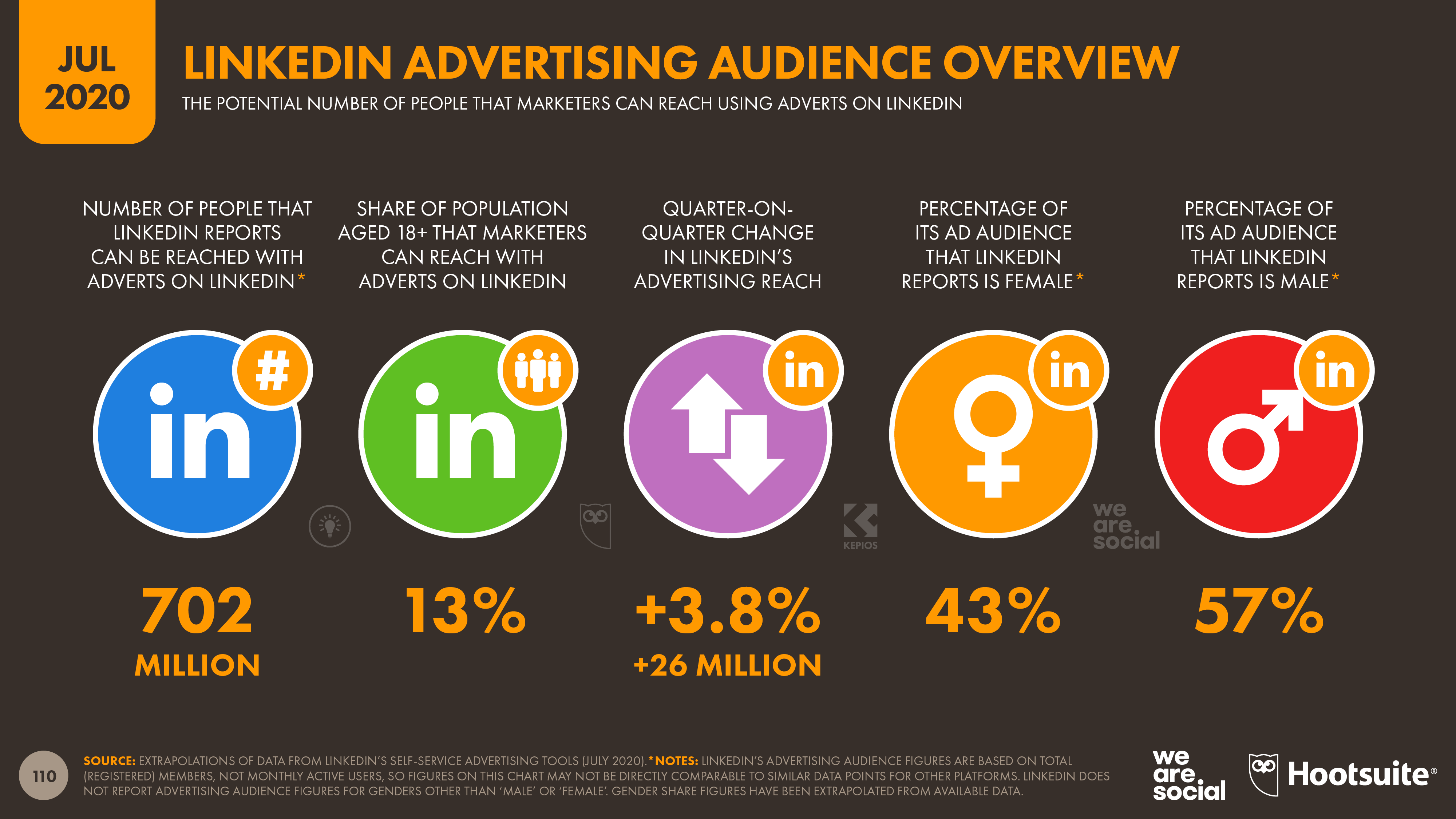

LinkedIn’s tally of total registered users also reached an impressive milestone this quarter, passing 700 million global users.

The platform’s global user base grew by more than 25 million over the past 3 months, equating to quarter-on-quarter growth of almost 4 percent.

It’s important to note that this figure does not represent monthly active users though, so this figure does not compare directly to the figures we report for other platforms in this report.

Sadly, LinkedIn stopped publishing monthly active user figures when it was acquired by Microsoft, but DataReportal analysis suggests that the platform wouldn’t quite make our latest ranking of the world’s most active social platforms.

Twitter appears to have lost the audience gains that it posted last quarter, with the company’s advertising tools suggesting that global advertising reach has now dipped back below the figures those same tools were showing back in January.

However, it is worth noting that the numbers reported in Twitter’s advertising tools are subject to considerable fluctuation, even over relatively short periods of time.

Furthermore, a 90 percent drop in the reported number of Twitter users in Russia played a significant role in this quarter’s reduction.

Twitter’s tools show that the addressable advertising audience in the country dropped by more than 20 million over the past 3 months, accounting for more than a third of the overall global adjustment.

This is particularly noteworthy given the big rise (+149 percent) in Twitter users in Russia that we reported in our April report.

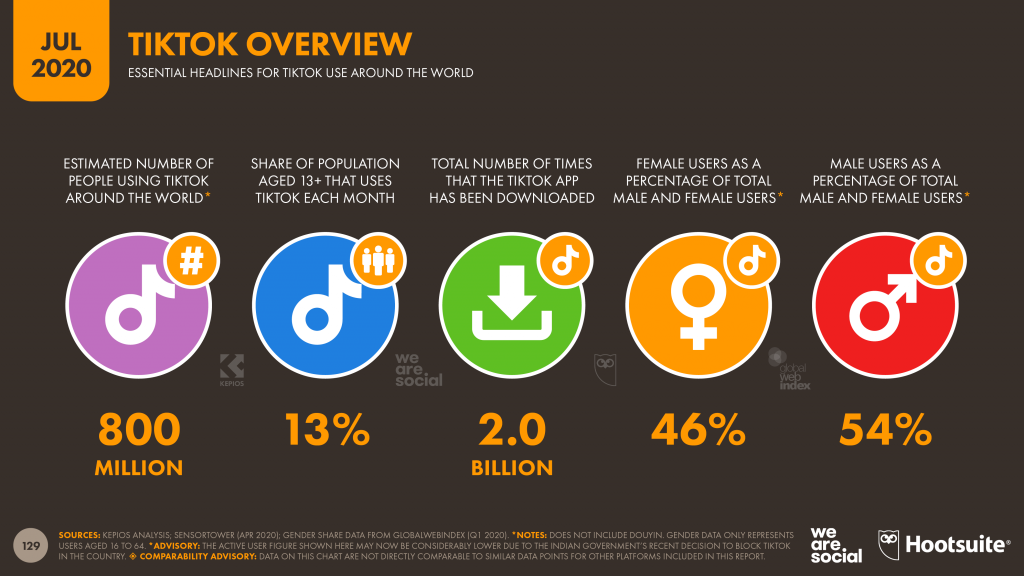

Growth (and challenges) for TikTok

TikTok had been enjoying a stellar quarter, with all signs pointing to impressive user growth all over the world. However, the Indian government’s move to ban the app across the country at the end of June may put a dent in the platform’s future growth trajectory.

Bytedance still hasn’t published any updated figures for global TikTok use, but DataReportal analysis of a variety of data sources indicates that the platform had passed 800 million monthly active users outside of China before the ban in India came into place.

Previously, we reported a combined active user figure for both TikTok and Douyin, but in light of recent events and changes to the company’s structure, we now report them separately.

Had we continued to report the two platforms together, however, the combined monthly active user total would now be roughly 1.2 billion, which would represent growth of 50 percent in just the past year.

It’s unclear whether the Indian government’s decision will result in a permanent ban for TikTok, so we’ve elected to report the unadjusted figures for now, especially because the ban only came into place one day before the end of our reporting period.

However, our analysis indicates that India may account for as much as a quarter of TikTok’s global active user base, so any ongoing restrictions could become a major hurdle for TikTok’s future expansion.

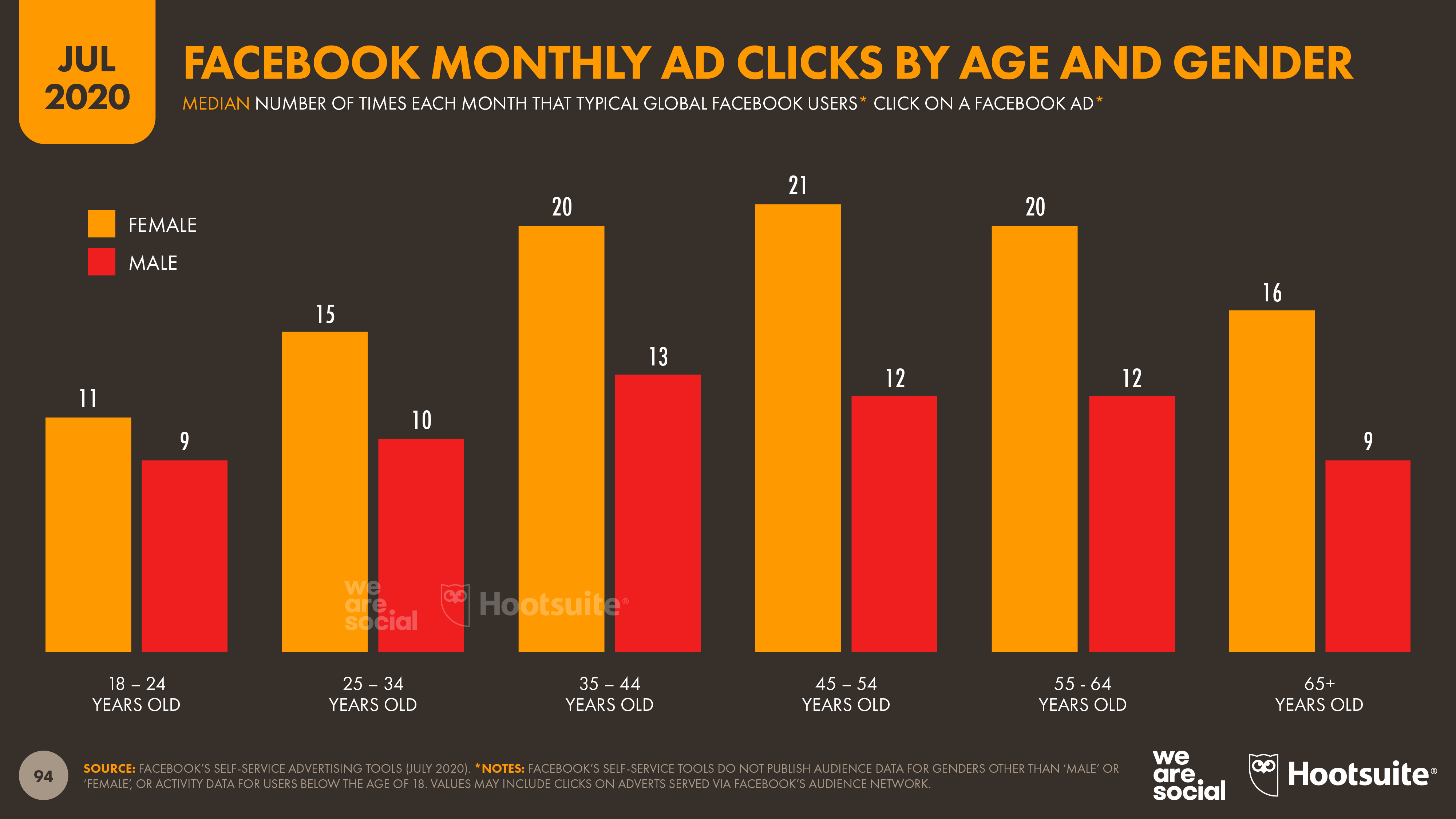

Facebook ad engagement dips

In contrast to the jump in ad engagement that we reported back in April, the latest data suggest that Facebook users clicked on fewer ads in June than they did in March.

The company’s ad tools report that the global median remained steady at 13 ad clicks per user, per month, but closer inspection of the data by age and by gender reveals that clicks actually declined across most demographic groups, compared to the median levels for March.

Facebook ad engagement levels are still higher than they were at the start of the year though, which should offer some level of encouragement for marketers.

Increased ecommerce activity should endure

We’ve collected a wealth of new ecommerce insights for this quarter’s report, all of which point to an increased role for ecommerce even after the COVID-19 pandemic has passed.

Data from Contentsquare shows that overall ecommerce transactions are up by roughly 20 percent in July compared to the start of 2020.

The company reports that the weekly number of online transactions has been declining steadily since lockdowns started to ease – especially now that people are able to return to physical stores – but online conversion rates continue to increase.

Moreover, research from GlobalWebIndex shows that almost half of all internet users expect to make more use of ecommerce even after the outbreak is over, with consumers in some of the world’s largest developing economies most likely to foresee increases in their online shopping activities.

Older shoppers seem to have shown the biggest increases in propensity to shop online compared to our April report, with nearly 4 in 10 internet users aged 55 to 64 now reporting that they expect to make more frequent ecommerce purchases after the pandemic ends.

Even more encouragingly, ecommerce transactions have increased across almost every category, with sports equipment brands and supermarkets seeing particularly strong gains compared to pre-Coronavirus levels.

Tourism transactions continue to be badly affected by safety fears and ongoing travel restrictions, but the encouraging news is that transaction volumes appear to have increased threefold since our previous report three months ago.

Weekly transaction volumes in the tourism sector are still 30 percent lower than they were in the first 6 weeks of 2020 though, and with the number of new COVID-19 cases continuing to rise at the time of writing, it’s likely that conditions will remain tough for travel brands for the remainder of this year.

Making sense of the numbers

So what do all of these new numbers mean for you?

Here are my top 3 takeaways:

1. With more than half of the world’s total population now using social media, now is an ideal time to rethink how we use these powerful platforms. In particular, I’d recommend thinking of social media as a layer that runs through everything that people do – both online and in the physical world – rather than being a series of distinct ‘destinations’ and standalone activities.

2. Try to avoid getting swept up in the hyperbole of binary predictions. Just as digital hasn’t replaced TV, working from home likely won’t replace the office, and ecommerce won’t replace all physical stores. People’s behaviours are evolving though, and it’s important to understand how these changes will impact demand for your brand’s products and services, as well as how you’ll need to adapt your marketing activities to achieve maximum efficiency and effectiveness. My advice would be to adopt a ‘balanced diet’ in all things digital, and to take advantage of every opportunity to learn about what your audience really cares about.

3. Keep an eye on ‘stealth’ trends. Media stories about connected tech often focus on the platforms and the devices, but how people use these technologies is far more important. However, many of these behavioural trends emerge over time, without reaching a sudden ‘tipping point’ that spurs us into action. For example, the changes in people’s search behaviours that we explored above could have fundamentally important consequences for brands across almost every category, but they haven’t replaced search engines (yet). And to make things even more complex, these behaviours are evolving all the time, so there’s no ‘quick fix’ that can deliver a permanent advantage. As a result, as you start to think about 2021, it’s worth investing in plans and tech stacks that can adapt and flex over time – especially given the uncertainty around the ongoing evolution of COVID-19.

And finally…

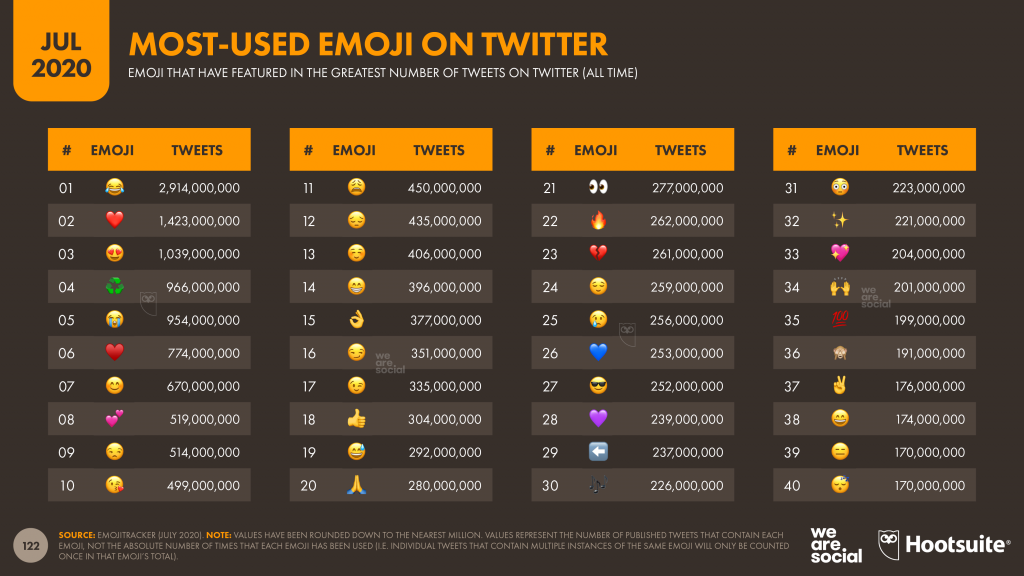

It was #WorldEmojiDay last week 📅, so we’ve produced an update to our chart showing EmojiTracker’s ranking 🏆 of the all-time most-used emoji 📈 on Twitter.

Key findings 🔎 include:

🔥 has been used in more than 70 million tweets over the past 6 months, accounting for more than a quarter of its all-time total. Guess you might say 🔥 is 🔥

😍 has moved above ♻️ to claim the third spot ⬆️ in the rankings

The ⚔️ between ❤️ and ♥️ continues, but 💙 and 💜 are both ⏫.

That’s probably enough nerdiness 🤓 for now, but if you fancy getting involved in a bit of an emoji mystery 🕵️♀️, you might want to check out this intriguing Easter egg 🥚 that I spotted in Apple’s musical notes emoji 🎵🎶.

That’s all for now though – we’ll be back with another Statshot report in October.

Reports

Reports