The launch of the Digital 2022 Australia report gives us the opportunity to examine the online behaviour of Australians over the past year. If you thought 2020 heralded a shift in how we engaged with social media, online gaming and the internet, 2021 politely requests that you hold its beer.

By the start of 2022, Aussies were spending more time and money online than ever before. If we weren’t indulging in social shopping or challenging our friends to rounds of multiplayer games, we were endlessly scrolling through a variety of social platforms. In fact, our uptake of social media is now disproportionate to the total population growth, driven by another year of pandemic lockdowns and necessary social isolation. As society begins to reopen in the age of vaccine boosters, which behaviours will stay and which return to their IRL analogues remains to be seen.

And now, without further ado, let’s dig up some interesting titbits.

TikTok don’t stop

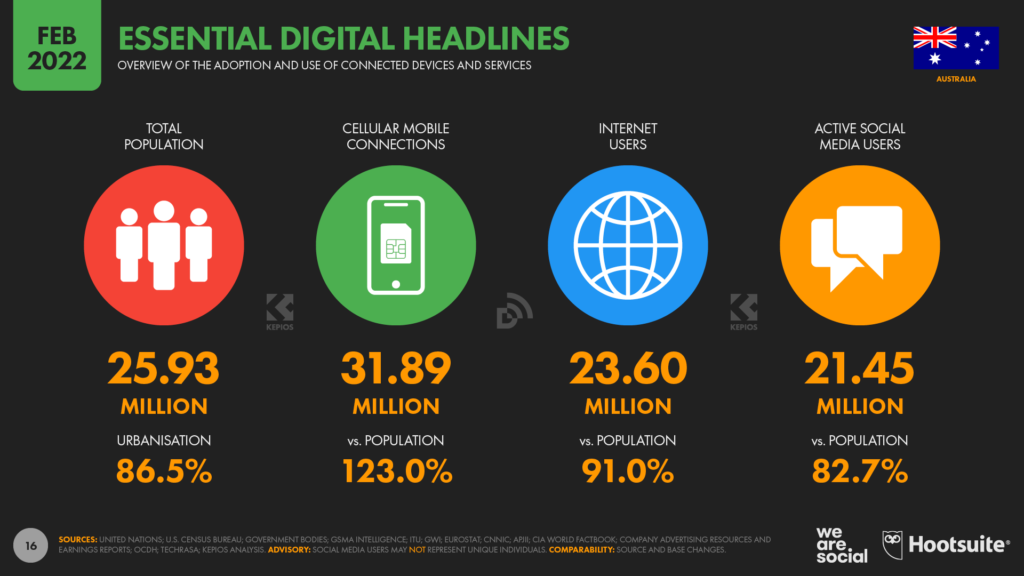

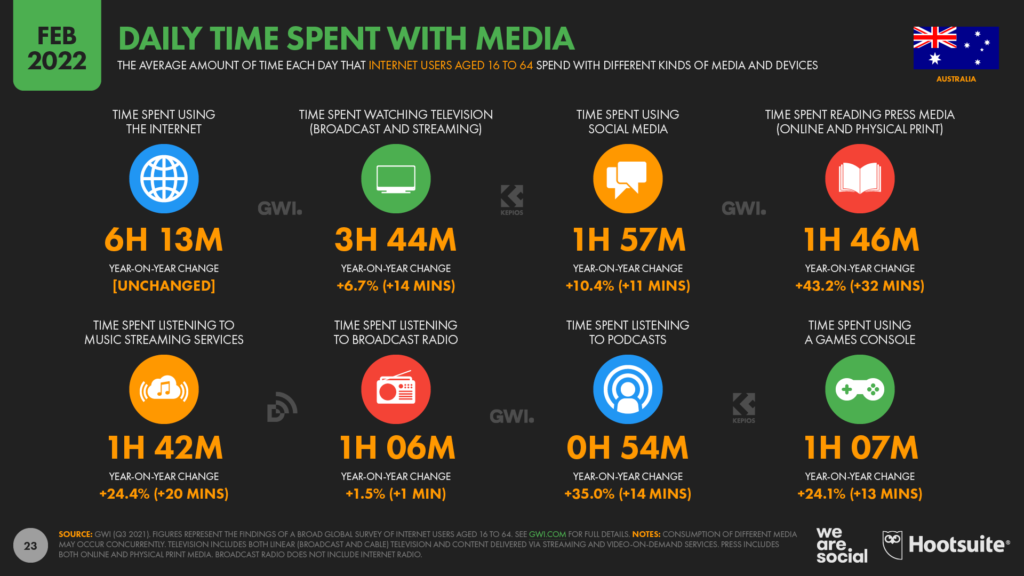

By the end of 2021, 82.7% of Australians were active on social media, an annual growth of nearly 1 million users. As time spent on social media increased to 1h and 57m per day it became the second most popular media activity for Australians after watching television.

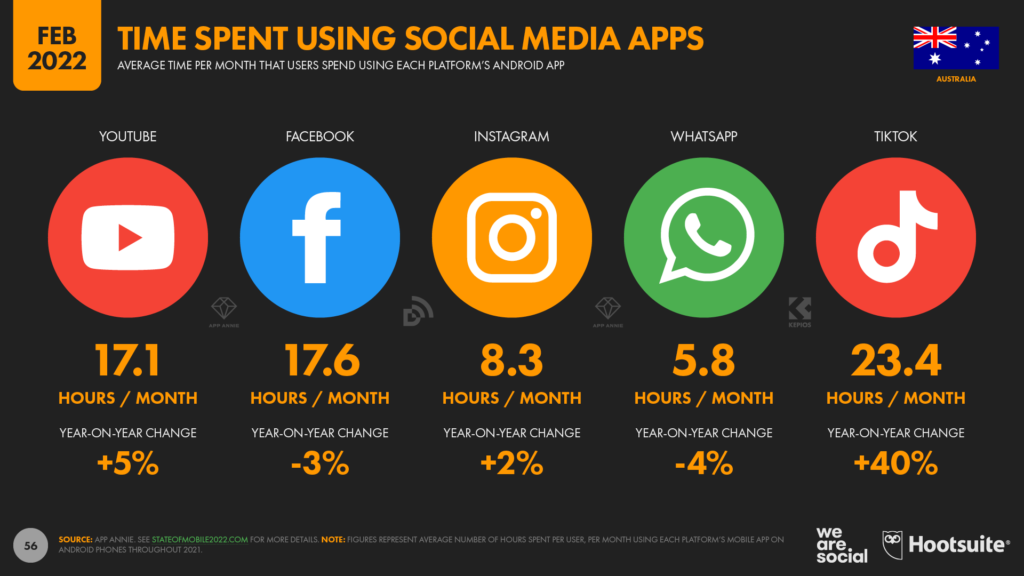

This increase was driven primarily by TikTok, now a social media staple of 32% of the 16-64 set. Australian TikTok users scroll through the app for 23.4 hours per month – a whopping 40% jump since the beginning of 2021. Meanwhile, the Facebook – ahem, Meta – properties either stalled or shrunk their social growth: Instagram grew 3% while Facebook and Whatsapp dropped 3% and 4% respectively.

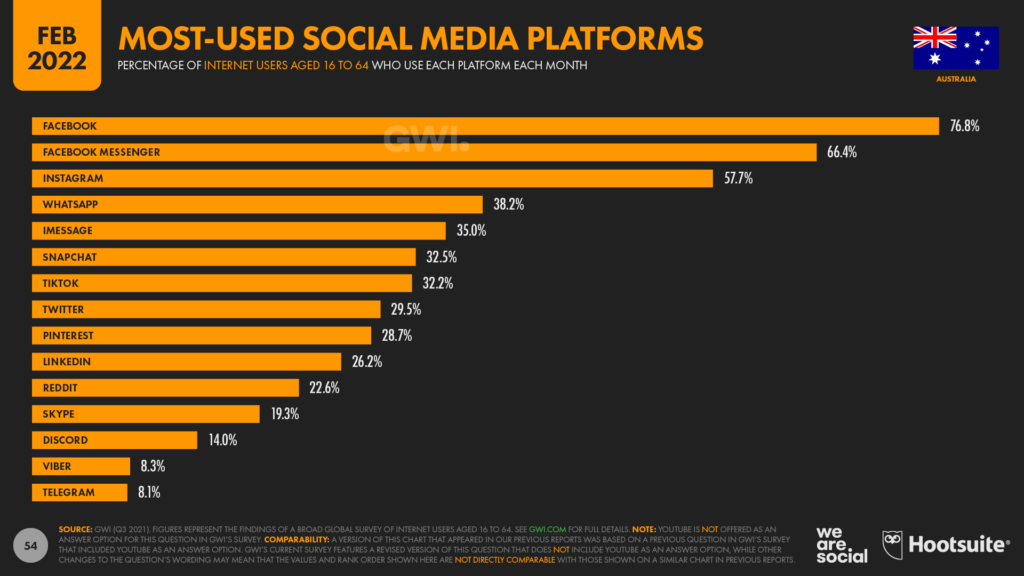

This wasn’t enough to knock Facebook from its throne, though. With 76.8% of social media users still hopping on, it’s the most used platform in Australia, followed by Facebook Messenger in silver position with 66.4% and Instagram taking home the bronze with 57.7%. TikTok now sits comfortably at #8, beating out Twitter, Pinterest and LinkedIn.

The uptake of TikTok speaks volumes to the type of content and interactions users are drawn to. The authenticity of its subcultures and creators’ content is captivating a new audience and keeping them engaged for longer. The rise of the TikTok influencer suggests that there’s no stopping the platform for now.

Gaming away the lockdown days

At the start of 2021, music streaming was up by 20%. Over the course of the year, our entertainment needs evolved to feature an increased focus on interactivity. In short, gaming became king.

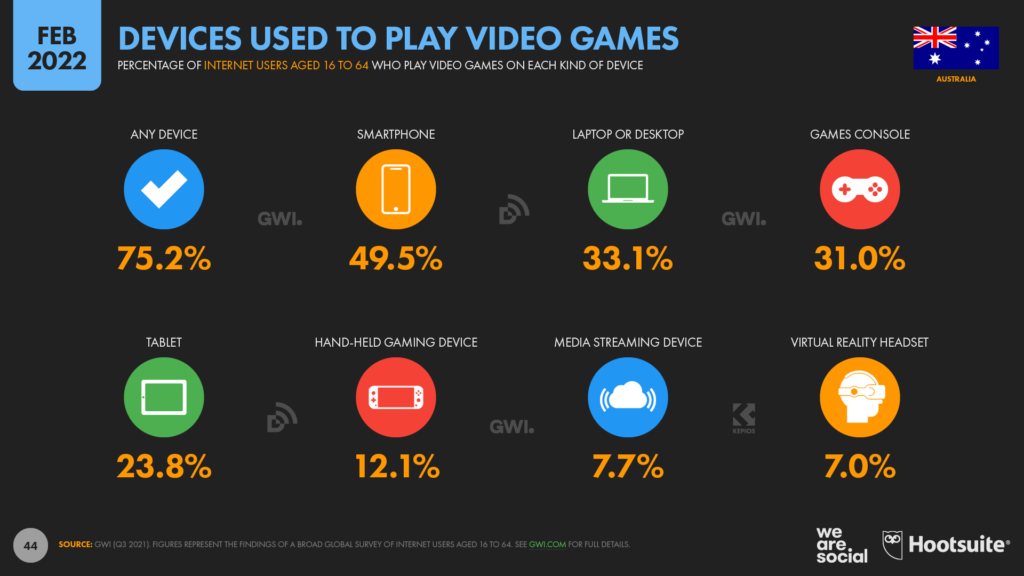

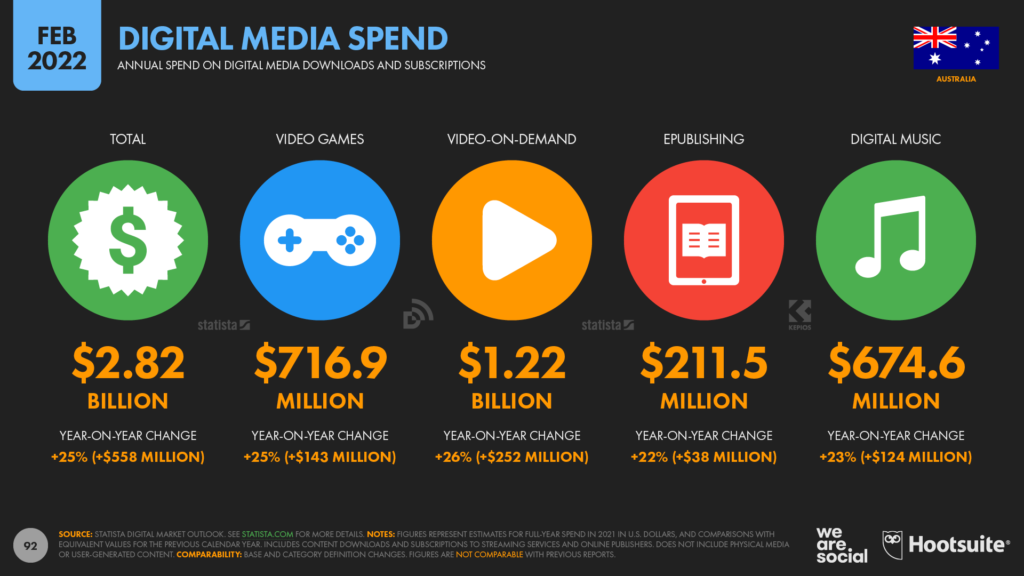

75.2% of internet users play games on any device, but the use of – and demand for – VR headsets and handheld gaming devices all grew, as anyone who tried to buy a Nintendo Switch will tell you. On average, +13 additional minutes was spent gaming on a console. Gaming even became a form of passive entertainment for 18.8% of Australians who spent time watching gaming videos online each week. Spending on video games also increased by +25%, rising to roughly AU$1B (US$717M) per year.

Beyond gaming, digital device ownership continued to grow with smartwatches (+7.3%), streaming devices (+3.0%), virtual reality devices (+9.5%) and feature phones (+22.9%) leading the charge. Of course, since we bought them we aimed to get the most out of them – time spent on all digital activities increased by an average of +15m.

e-Shopping e-Spree

Not only did Australians spend more time online in 2021, but we also splashed more cash on mobile applications and in-app purchases.

Collectively we downloaded 788 million apps during the year and spent AUD$3.24 billion (USD$2.31 billion) both on and in them, a +21% increase year-on-year. We also spent +25% more on subscriptions and downloads across video games, on-demand video, books and music, as we searched for ways to fill the time during lockdown.

67.7% of Australians made a purchase on the internet in 2021, with over half buying something online each week. On average, this worked out to roughly AUD$2,766 (USD$1,968) per person per year, a rise of 19%. As could be expected, e-commerce saw the greatest expenditure increase in food (+64%), personal and household care (+30%) and toys and hobbies (+30%) categories, with COVID isolation protocols driving this growth – when you can’t go to the shops, you get the shops to come to you.

2021’s numbers paint a picture of a society grappling with the second year of COVID-based isolation. Collectively we burrowed deeper into the digital realm, seeking new platforms and media to while away the time and stay connected with friends and family. What remains to be seen is how a return to IRL activities merge with our new digital habits as we gradually gain the upper hand over COVID-19, and how brands will leverage the opportunity.

If you’d like to chat about what this could mean for your brand, and how to gain an advantage over your competition, feel free to drop us a line.

Now if you’d like to get all the delicious data from the Digital 2022 Australia report, check it out below, or find more global stats in the Digital 2022 Global report here.

Reports

Reports