Kepios founder Simon Kemp takes us through the key headlines featured in our Digital 2022 April Global Statshot.

63 PERCENT OF ALL PEOPLE ON EARTH ARE NOW ONLINE

DataReportal’s new Digital 2022 April Global Statshot report – published in partnership with We Are Social and Hootsuite – reveals that more than 5 billion people around the world now use the internet.

This impressive total marks another important milestone on our journey towards universal internet accessibility, and means that 63 percent of the world’s total population is now online.

There’s much more to this story than a headline user figure though, and this article offers extensive analysis to help you understand the implications of this milestone.

But there are plenty of other big stories in this quarter’s report too, including:

A big new milestone for social media use in China;

A remarkable new record for TikTok;

A change in momentum for social media user growth;

Further increases in the cost of social media ads;

The role of digital in the workplace and B2B marketing; and

A jump in cryptocurrency ownership across developing economies.

Executive summary

You’ll find a handy summary of this quarter’s top stories in the video embed below (click here if that’s not working for you), but read on below for the full report, and for my in-depth analysis of this quarter’s data.

Digging deeper

This is by far the biggest Statshot report that we’ve produced to date, and – in addition to our usual quarterly insights – you’ll also find a wealth of new data in this update.

So, just before we dig into all of the numbers, I’d like to extend a very special thank you to the data partners who’ve made this “wealth of data” possible:

You may also want to grab a coffee and a notepad and get comfortable before you dive in – at almost 300 slides and more than 10,000 words, there’s a lot (!) to digest in this update.

Full report

The SlideShare embed below contains the complete Digital 2022 April Global Statshot Report (click here if that’s not working for you), but read on past that to understand what all these numbers mean for you.

The global state of digital in April 2022

Let’s begin with the essential headlines for the adoption and use of connected tech around the world in April 2022:

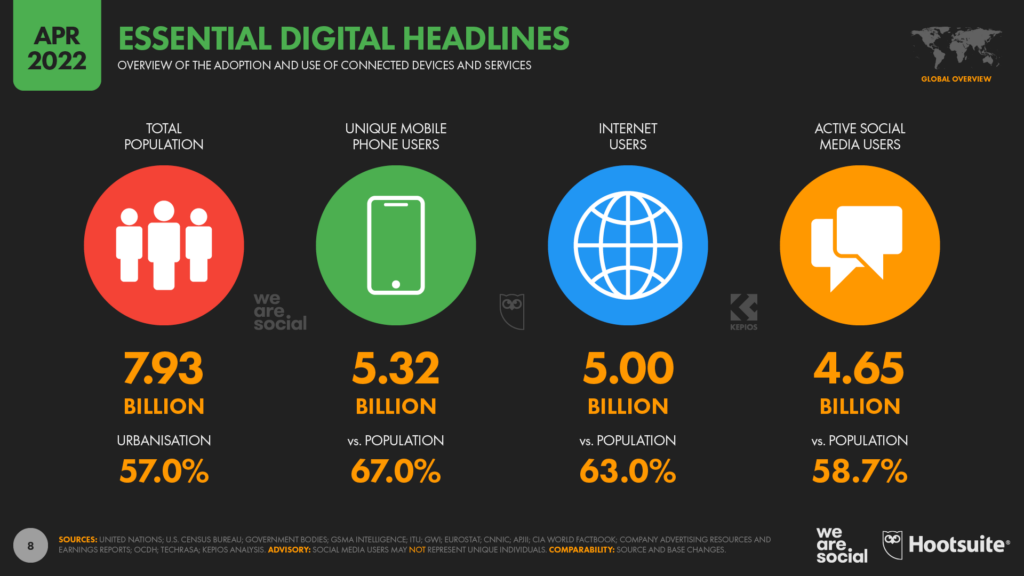

World population: there are 7.93 billion people living on Earth in April 2022, with 57 percent of those people residing in urban areas.

Mobile users: 5.32 billion people around the world now use a mobile phone, equating to 67 percent of the total global population. Smartphones account for roughly 4 in 5 of the mobile handsets in use today.

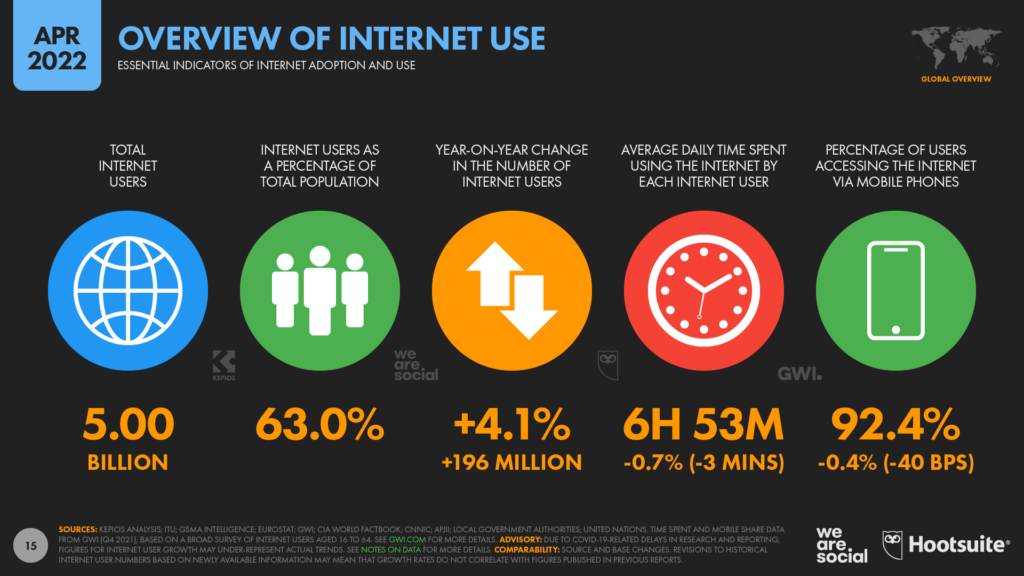

Internet users: 5.00 billion people now use the internet, with the global total increasing by almost 200 million over the past year. 63 percent of the world’s population is now online, but there are still important differences in the “quality” of internet access around the world.

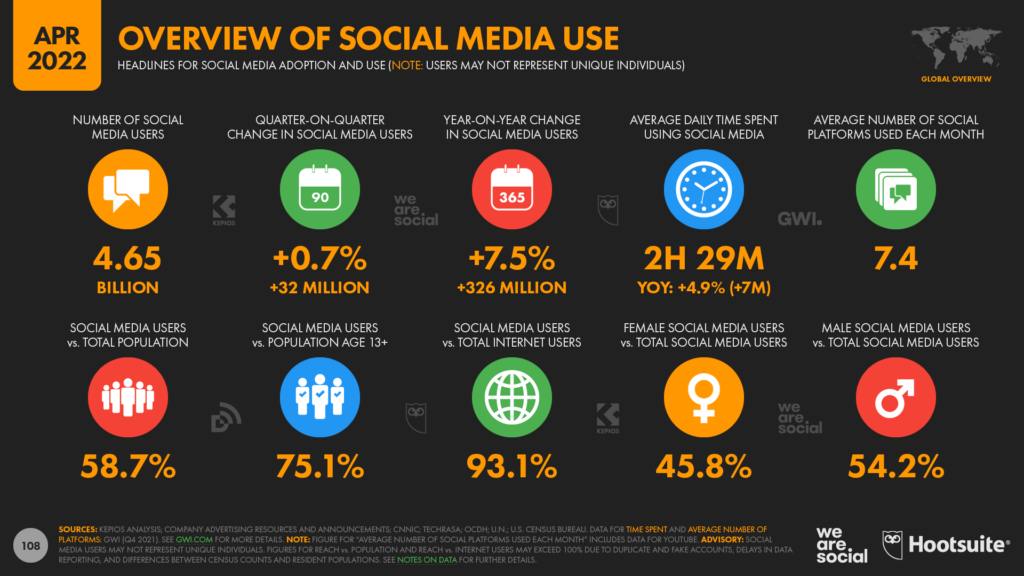

Social media users: there are 4.65 billion social media users around the world today, which equates to 58.7 percent of the total global population. However, if we focus just on ‘eligible’ audiences aged 13 and above, data suggests that roughly three-quarters of all those people who can use social media already do.

Those numbers offer some great context to get us started, but in order to make sense of the underlying trends, we need to dig deeper into the stories behind the headlines.

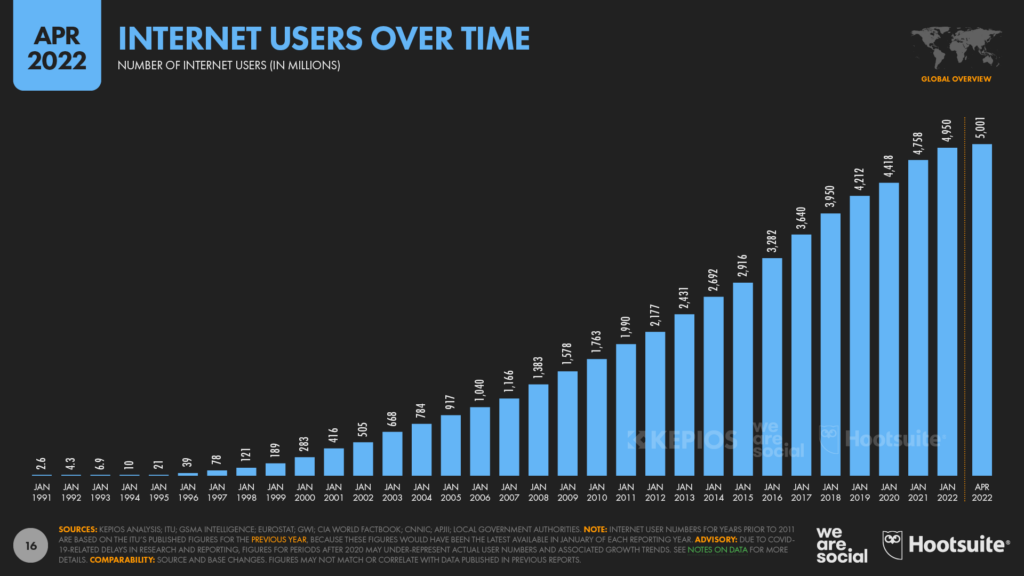

Internet users pass the 5 billion mark

Ongoing analysis by the team at Kepios reveals that there are now more than 5 billion internet users around the globe, marking a momentous milestone on the world’s journey towards universal access.

That journey only began about 50 years ago, with the first transmission of data via an internet-like network taking place in October 1969.

Email followed in the early 1970s, but it wasn’t until Tim Berners-Lee developed the World Wide Web some 20 years later that adoption of the internet really started to gain momentum.

When the first website went live in August 1991, fewer than 4 million people around the world used the internet, but internet users grew quickly over the following decade.

The global user total passed 50 million shortly after the removal of commercial internet restrictions in 1995, and by the turn of the millennium, well over a quarter-of-a-billion people were already online.

The billionth internet user likely came online sometime in 2005, but it only took another 6 years for that global user figure to double to 2 billion.

Less than 5 years later, in early 2015, the global figure passed the 3 billion mark – a milestone that we covered in our Digital 2015 Global Overview Report (however, note that we’ve revised some of our historical numbers – and our reporting methodology – since publishing that report).

By early 2017, more than half of the world’s total population was using the internet.

The global user figure passed the 4 billion mark in early 2018 – a story that we explored in detail in our Digital 2018 Global Overview Report.

That means it has taken roughly four years for the global internet user total to grow from 4 billion to 5 billion.

These trends indicate that internet user growth rates have slowed in recent years, but that’s perhaps to be expected now that more than 6 in 10 people are online.

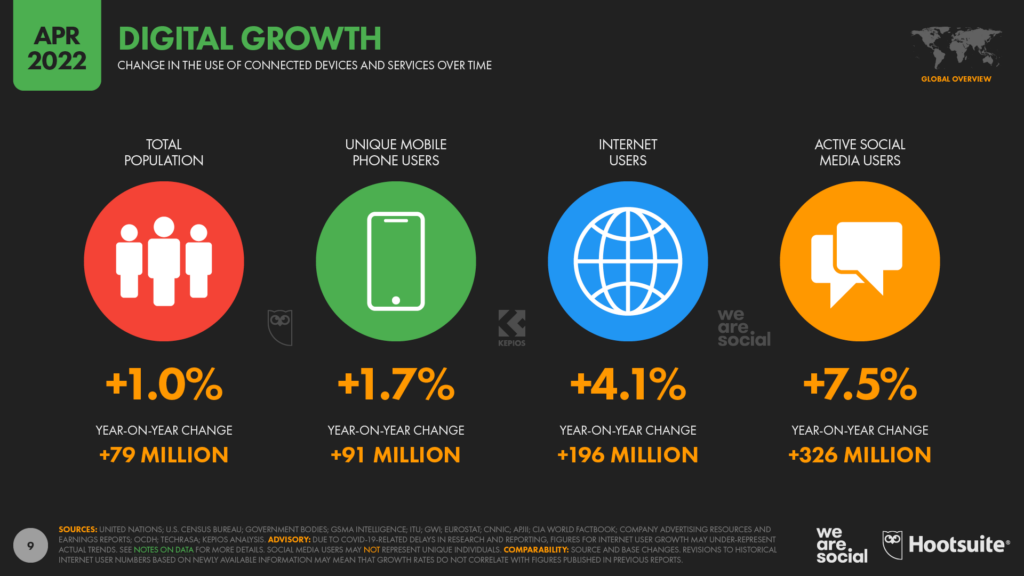

The latest data show that internet users have still increased by almost 200 million over the past 12 months though, representing year-on-year growth of slightly over 4 percent. Moreover, there’s a good chance that the ongoing COVID-19 pandemic continues to impede research into adoption of connected technologies, and the actual number of internet users may be higher than these published totals suggest.

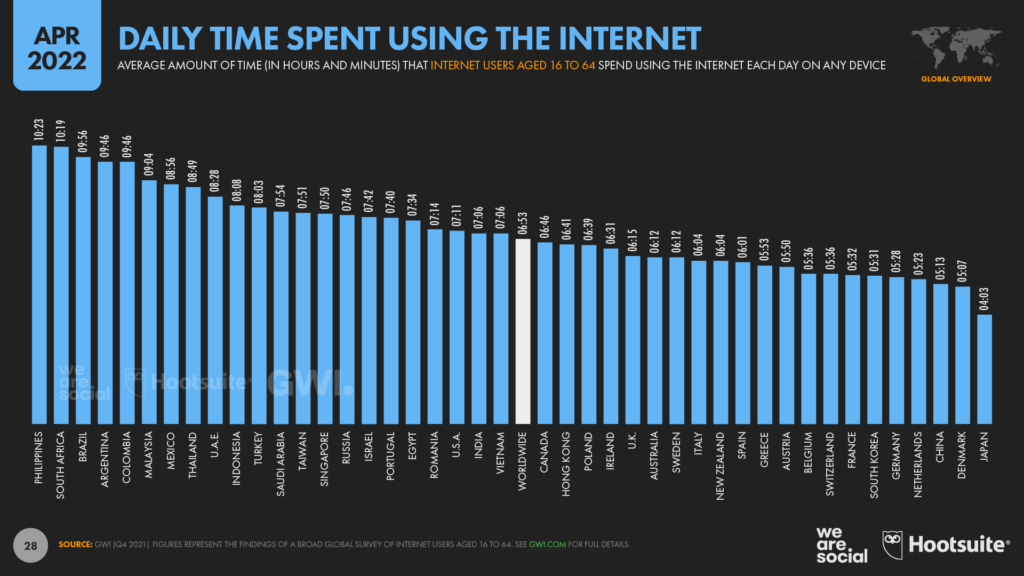

Online time

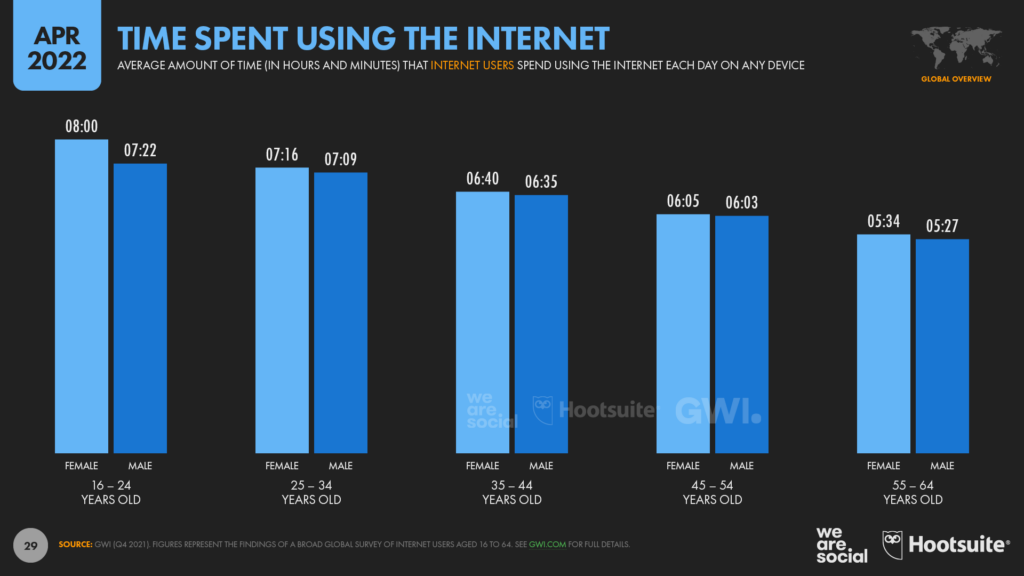

The latest wave of research from our partner GWI reveals that the world’s internet users now spend an average of 6 hours and 53 minutes online each day.

That’s down slightly from the start of the year, when survey respondents reported spending an average of 6 hours and 57 minutes per day on connected activities.

However, the latest figures mean that the world’s 5 billion internet users still spend a combined total of more than 2 trillion minutes online every single day.

For context, the typical internet user now spends more than 40 percent of their waking life online.

And what’s more, with the typical user spending more than 48 hours online each week, billions of people now spend more time using connected devices than they spend at work.

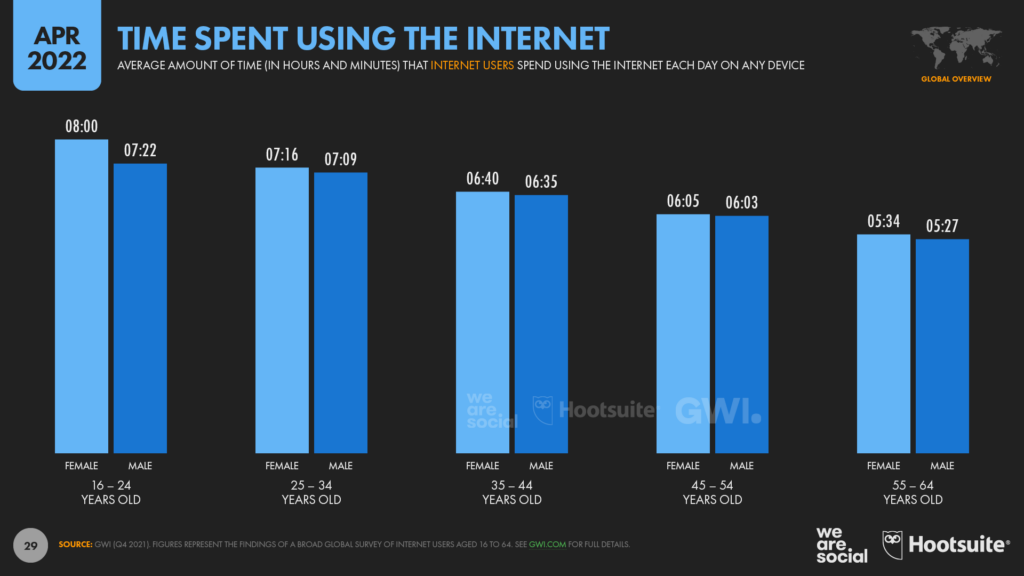

On average, younger people tend to spend more time online than older generations do, with young women spending the greatest amount of time using the internet.

GWI’s research reveals that women aged 16 to 24 now spend an average of 8 hours per day online, meaning that many women in this demographic now spend as much time using the internet as they do sleeping.

At the other end of the spectrum, men in the Baby Boomer generation say that they spend just under 5½ hours per day online, but that still equates to roughly a third of their waking hours.

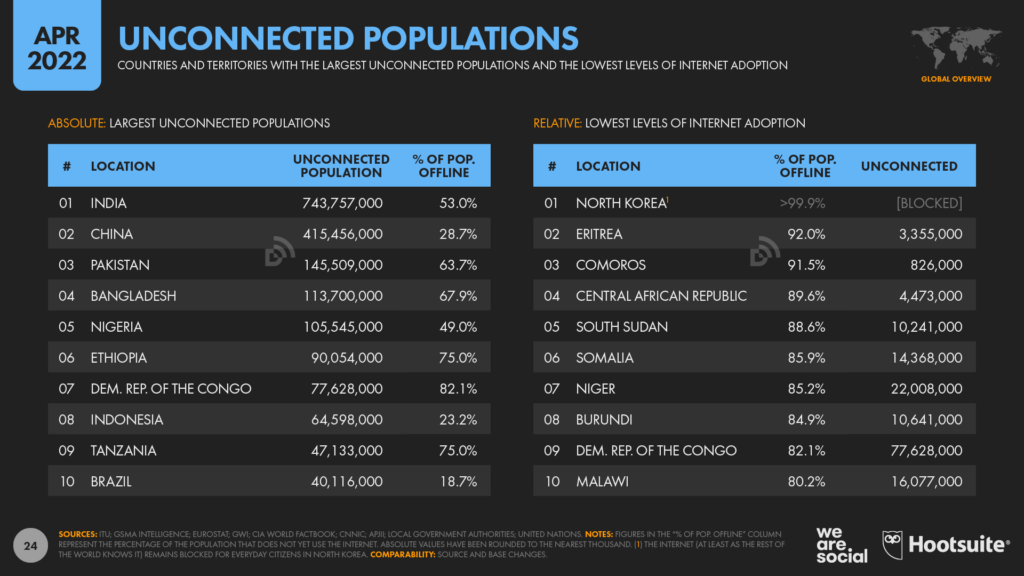

Billions still offline

Despite these impressive figures, however, there are still 2.9 billion who do not use the internet in April 2022, representing 37 percent of all the people on Earth.

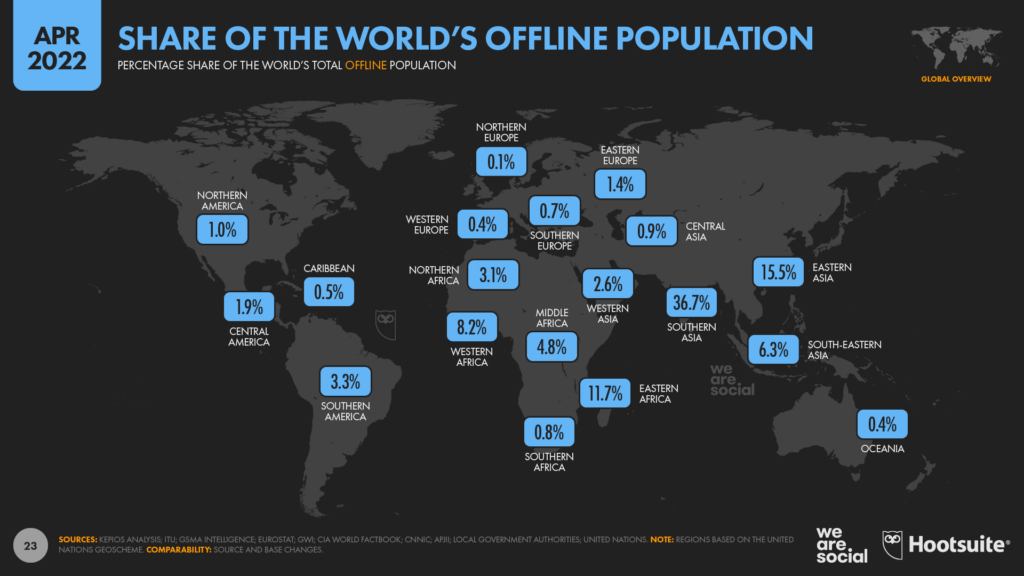

Southern Asia is home to the largest offline population, with more than a third of the world’s “unconnected” living in the region.

744 million people remain offline in India, equating to more than half (53 percent) of the country’s population, and more than a quarter of the world’s unconnected.

Meanwhile, 145 million people in Pakistan do not currently have internet access (63.7 percent of the population), and 114 million people remain offline in Bangladesh, equating to more than two-thirds of the country’s population (67.9 percent).

China still has a large unconnected population too, despite the country’s internet users now numbering well over 1 billion.

Data from CNNIC indicates that roughly 415 million people remain offline in China, equating to 28.7 percent of the country’s total population.

For context, China’s offline population accounts for just over 14 percent of the world’s unconnected in April 2022.

Connectivity in context

Back in 2003, William Gibson posited that, “the future is already here; it’s just not evenly distributed.”

Almost 20 years later, such “uneven” distribution remains a fundamental problem when it comes to internet access around the world.

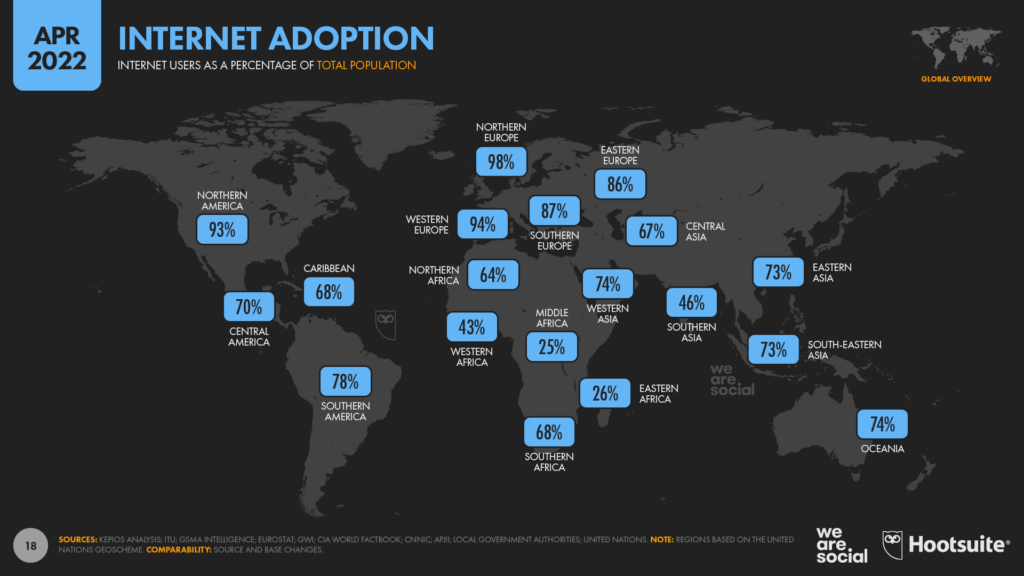

Kepios’s analysis indicates that 63 percent of the world’s population is now online – a figure that aligns closely with the latest estimates published by the ITU.

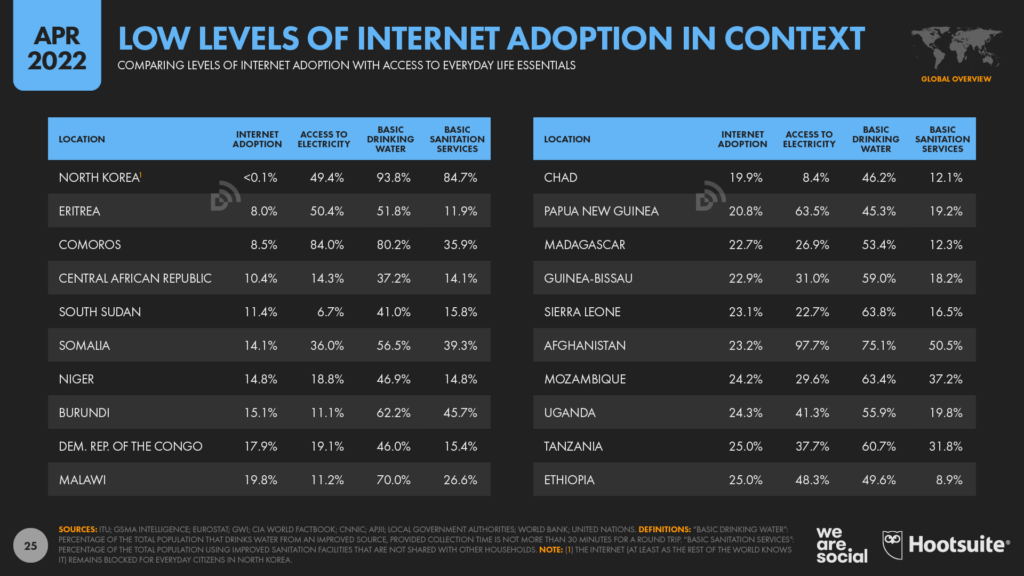

However, data also shows that internet penetration remains below 10 percent in three countries – North Korea, Eritrea, and Comoros – while less than a quarter of the population has access to the internet in a total of 18 countries.

15 of these 18 countries are situated in Africa, where the region-wide internet penetration rate currently sits at just 39.9 percent.

As we’ll explore in more detail in the next section, economics play an important role in determining how likely a country’s citizens are to access the internet, but cost isn’t the only factor we must address in order to achieve the goal of universal accessibility.

In some countries – such as North Korea – unusually low levels of internet access appear to be largely the result of political decisions to “block” public access.

Meanwhile, low levels of digital connectivity are often symptomatic of broader infrastructure challenges.

For example, rates for internet adoption only exceed rates for access to electricity in 6 countries around the world.

This finding is perhaps unsurprising given that all internet-connected technologies rely on electrical power, but this data still provides useful context when analysing current levels of internet access.

Furthermore, in 6 of the 18 countries where internet penetration remains below 25 percent, the World Bank reports that less than half of the population currently has access to basic drinking water services.

Similarly, in 16 of those 18 countries, less than half of the population has access to basic sanitation services.

Interestingly, however, internet access either matches or exceeds levels of access to basic sanitation services in 8 of these countries, and we see a similar situation in a total of 28 countries around the world.

Meanwhile, GSMA Intelligence reports that nearly a quarter of adults in lower- and middle-income countries are still not even aware of mobile internet and its benefits.

In other words, hundreds of millions of people across developing economies may not know that the internet exists.

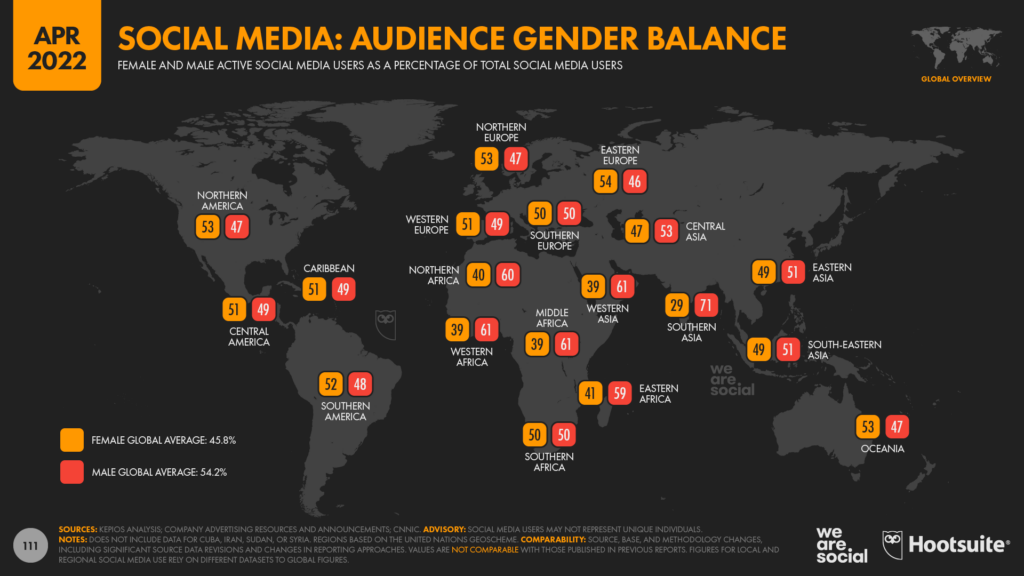

Adding context to these numbers, GSMA Intelligence reports that lower awareness and adoption is more common amongst older, less educated women in poorer countries.

And this gender imbalance is apparent in other data too, such as the share of social media users by gender.

At a global level, men account for 18 percent more social media users than women. However, across Southern Asia, men account for almost 2½ times as many social media users as women.

This “digital gender gap” is perhaps the most troubling aspect of uneven digital distribution, because various data points demonstrate that – when they have equal access – women tend to use the internet more than men do.

As we saw earlier, the time that people spend using the internet is a clear example of this.

As a result, it seems clear that the digital gender divide is – quite literally – “man made.”

It’s the result of sexism.

For context, if women had the same level of internet access as men currently do, we estimate that the global internet user total would already have reached almost 5.4 billion – equal to 68 percent of the world’s total population.

But this isn’t just about internet access; continuing to restrict women’s access to the internet exacerbates other problems too.

“When women and girls are empowered through information and communication technologies (ICTs), societies overall benefit. With access to the Internet and skills to use digital technologies, they gain opportunities to start new businesses, sell products in new markets, and find better-paid jobs; pursue education and obtain health and financial services; exchange information; and participate more fully in public life.”

Critically, closing the digital gender divide doesn’t require any large-scale investment in infrastructure, nor does it require any new technology.

It simply requires men to stop restricting women’s access to the internet.

The cost of internet access

The affordability of access is also a primary consideration when analysing levels of internet adoption.

The Alliance for Affordable Internet (A4AI) publishes a number of datasets that explore various aspects of internet accessibility, all of which provide valuable context into rates of internet adoption around the world.

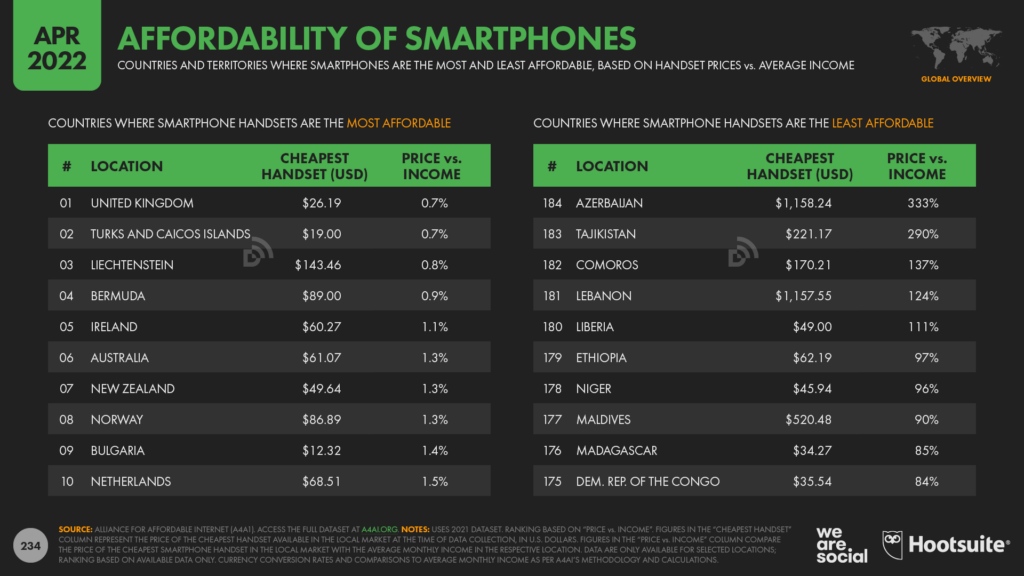

For example, A4AI reports that there are currently 5 countries around the world where the price of the cheapest available smartphone handset is currently greater than average monthly income, and that cost-to-income ratio remains above 50 percent in a total of 20 countries.

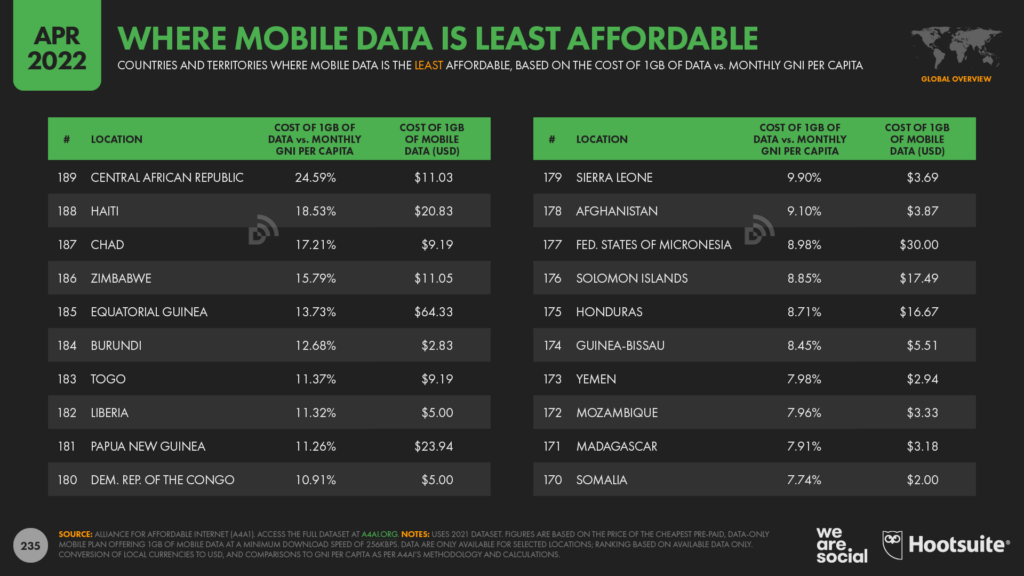

The cost of mobile data is also prohibitively expensive in a number of countries.

Amongst those countries where internet adoption remains below 25 percent of the population, A4AI reports that the cheapest prepaid mobile data plan offering 1GB of mobile data still costs more than 5 percent of average monthly income.

For context, 5 percent of average monthly income in the United States would be equal to roughly USD $270.

In the most extreme case – the Central African Republic – 1GB of mobile data currently costs almost a quarter (24.59 percent) of the country’s average monthly income.

For comparison, 1GB of mobile data costs just 0.07 percent of the average monthly income in Macau and Liechtenstein, and 0.7 percent of the average monthly income in the United States.

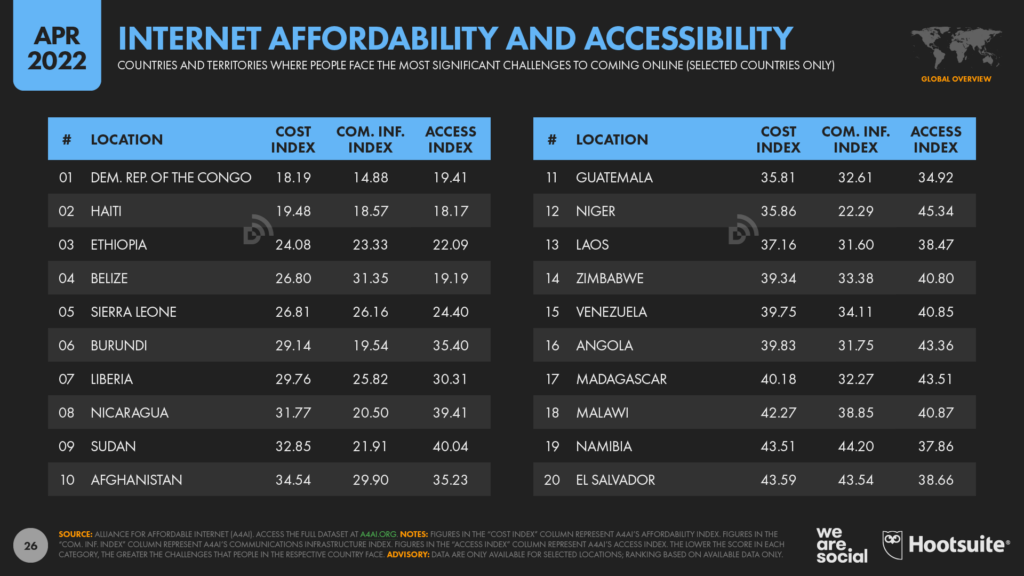

In addition to publishing these individual metrics, A4AI also produces an overall “affordability index”, which facilitates broader comparisons across countries.

The latest updates to this index indicate that people in the Democratic Republic of the Congo face the greatest challenges to going online, although it’s worth noting that the current rankings don’t include data for every country.

So, despite the encouraging progress we’ve made towards universal accessibility, it’s clear that we’ve still got a long way to go before everyone who wants to use the internet is able to do so.

Meaningful connectivity

It’s also important to stress that our journey towards “universal accessibility” isn’t just about ensuring basicaccess to the internet.

Two recent studies have revealed important differences in how people around the world “experience” the internet.

An excellent new report from the A4AI titled “Advancing Meaningful Connectivity” highlights how issues such as the cost of mobile data and internet connection speed can have a dramatic impact on the extent to which internet connectivity can improve people’s lives.

The report’s authors assert that:

“For an individual, meaningful connectivity can mean the difference between access to education, banking, and healthcare – or none of them. For a society, it can determine how realistic and how impactful digitalisation programs will be.”

They go on to note that, by failing to make the critical distinction between “basic” and “meaningful” internet access,

“…we mask the true nature of the digital divide, which lies not only between the connected and the unconnected, but in the starkly varied online experience people have.”

As a result, we need to go beyond looking solely at the quantity of people using the internet, and place greater emphasis on the quality of access and connected experiences.

But what does “meaningful” connectivity look like?

A4AI proposes the following framework:

Daily internet access, which ensures that the internet can facilitate advances in work, education, and communication;

Appropriate connected devices – especially smartphones – which enable people to experience the full power that today’s internet has to offer;

A connectivity “plan” or package with sufficient data – ideally unlimited – that enables people to access the content that they want, wherever and whenever that content has the greatest relevance in their lives; and

Connections that are fast enough to deliver stable and satisfactory internet experiences, especially when it comes to critical services like education and remote healthcare.

Meanwhile, the comprehensive 2021 edition of GSMA Intelligence’s State of Mobile Internet Connectivity (SOMIC) report also explores these issues, alongside more systemic challenges such as literacy and infrastructure.

For example, GSMA Intelligence reports that just 6 percent of the world’s population now lives in areas without the infrastructure required for mobile internet access, but this still equates to 450 million people, or more than 15 percent of the world’s unconnected.

Furthermore, the organisation reports that various challenges remain even when the necessary infrastructure exists.

Overall, GSMA Intelligence identifies six key areas that act as primary barriers to internet adoption and meaningful use:

Knowledge: whether people are aware of the internet, especially in terms of mobile internet and its potential benefits;

Access: the availability of the necessary network infrastructure, as well as associated enablers such as access to electricity, possession of the forms of official identification required to gain network access, and the availability of relevant end-user devices (e.g. smartphones);

Skills: the extent to which people have the necessary levels of literacy and digital “savviness” to make meaningful use of the internet;

Affordability: the costs associated with buying or accessing connected devices, the cost of data plans, and other associated service fees and expenses (e.g. the cost of electricity);

Relevance: the extent to which people can find and consume content, services, and connected products that they can understand and that meet their needs; and

Safety and security: how worried people are about the potential risks and negative experiences that they may be exposed to via the internet, such as harmful content, harassment, fraud, and personal data protection.

We cover a variety of these topics in our recently published Digital 2022 country reports – all of which are available to read for free on DataReportal – so if you’re looking for data to help you assess meaningful connectivity at a local level, head over to our complete report library.

We’ll also take a closer look at some of those key indicators below, but before that, let’s explore the reasons why the world’s 5 billion internet users go online today.

Reasons for using the internet in 2022

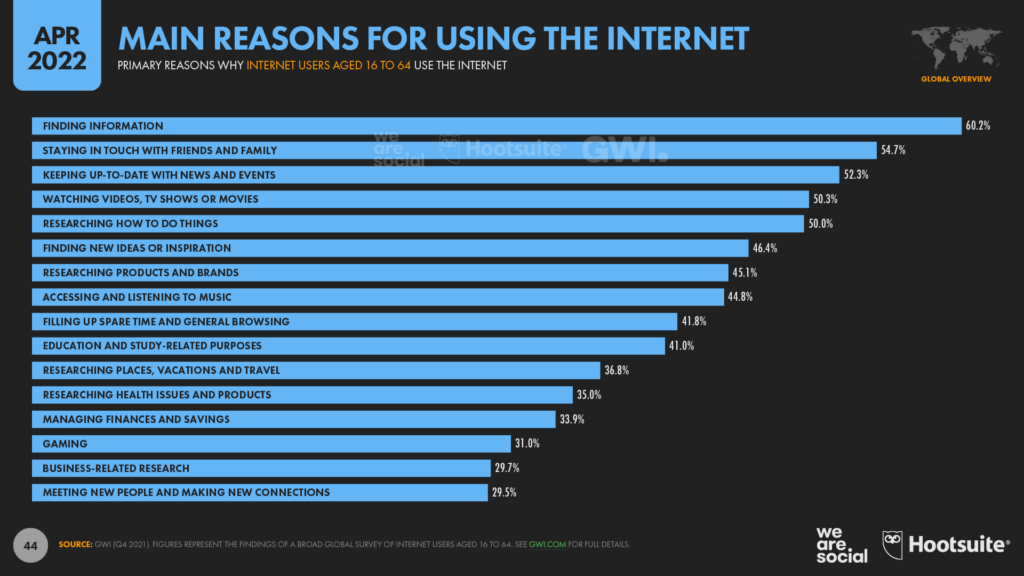

New research from GWI confirms that “finding information” is still the top motivation for using the internet.

More than 6 in 10 internet users (60.2 percent) between the ages of 16 and 64 cited this as one of the primary reasons why they went online in Q4 2021.

“Staying in touch with friends and family” ranked second, at 54.7 percent.

Finding and consuming news was the third most common reason for going online, with 52.3 percent of the world’s working-age internet users citing this as a top motivation.

And more than half of us (50.3 percent) said that we go online to find entertaining video content, placing this activity fourth in the latest global rankings.

Various other reasons bring people online though, with commercial activities such as searching for products and services also placing relatively high in GWI’s latest rankings.

It’s also worth highlighting that education, healthcare, and finance all feature in people’s top motivations for using the internet.

However, given their relative importance – as highlighted in the A4AI’s Advancing Meaningful Connectivity report – these activities merit more in-depth investigation.

Digital empowerment

As connected technologies advance and connection speeds improve, the internet is increasingly expanding beyond its initial focus on information and communication.

For example, the rise of “connected entertainment” is already clearly apparent in the widespread popularity of video games, and video and audio streaming.

However, digital innovation in education, healthcare, and financial services will likely have the greatest impact on the next phase of the internet’s “value evolution”.

Just before we explore each of these areas in more detail though, it’s worth noting that current data limitations may impact our ability to fully determine digital’s potential role in each of these industries.

For example, age-related restrictions governing the use of social media mean that there’s considerably less data available on young people’s online activities, making it harder to assess online education.

Similarly, privacy and security considerations make it more difficult to track and report online activities relating to healthcare and financial services.

And lastly, conducting research – especially surveys – can be a costly affair, so commercial research tends to focus on wealthier nations where companies are able to pay for insights.

Fortunately though, the available data still offer valuable insights into people’s online attitudes and behaviours as they relate to education, healthcare, and financial services, and they also point to how we might expect these attitudes and behaviours to evolve in the future.

Online healthcare

More than 1 in 3 internet users aged 16 to 64 surveyed by GWI across the world’s larger economies say that “researching health issues and healthcare products” is one of the main reasons why they go online today.

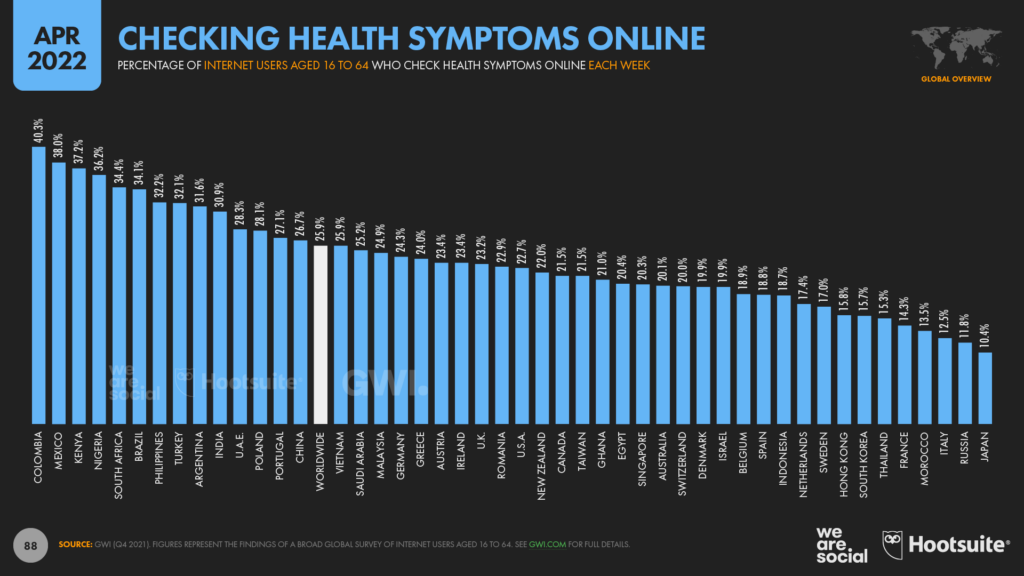

However, this figure is considerably higher across countries in Latin America, with more than half of Colombia’s working-age internet users citing health-related issues as a primary motivation for using the internet.

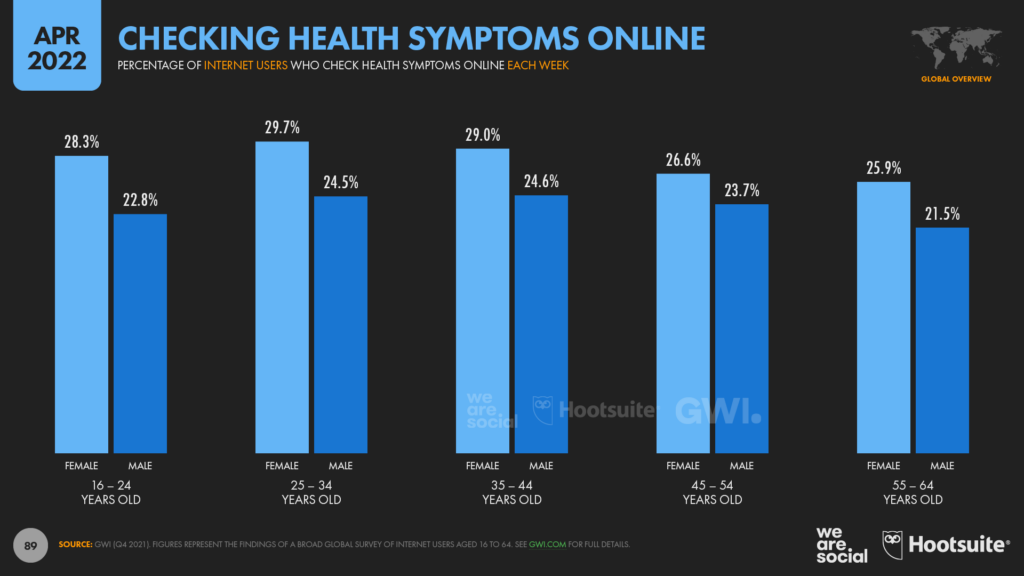

GWI’s survey also finds that more than a quarter of working-age internet users (25.9 percent) now check health symptoms online every week, and once again, that figure tends to be higher across countries in Latin America and Africa.

Data also reveal that women are more likely to turn to the internet for health-related concerns than men are, especially amongst younger age groups.

This finding will have particular significance for policymakers and healthcare professionals, especially when it comes to considerations relating to the availability and accuracy of online information and advice.

The adoption of telehealth services has also jumped since the outbreak of the COVID-19 pandemic.

Management consultancy Bain reports that the use of telemedicine by the public more than doubled across selected countries in the Asia-Pacific region between 2019 and 2021, and the company projects that more than 7 in 10 people in APAC will use these services by 2024.

However, progress in digital healthcare appears to be much slower across countries in Africa.

Despite accounting for 17.6 percent of the world’s total population and 11.2 percent of the world’s internet users, Statista reports that Africa is currently home to just 7.6 percent of the people currently using digitally enabled services to access healthcare, treatment, and medicines.

Online financial services

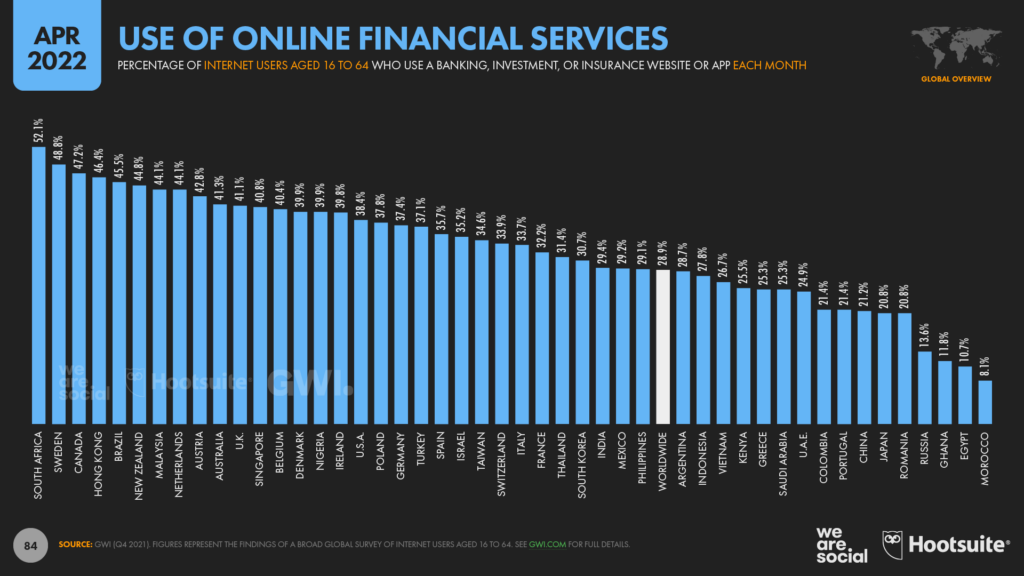

GWI’s research also highlights the important role that connected devices can play in delivering financial empowerment, while simultaneously challenging stereotypes of who’s using online banking today.

For example, the company’s latest wave of research (Q4 2021) reveals that South Africa has the highest rate of adoption of online financial services amongst internet users of any nation in its 47-country survey.

More than half (52.1 percent) of South Africa’s working-age internet users say that they have interacted with a banking, investment, or insurance website or app in the past 30 days, which is significantly higher than the equivalent figures for the United States (38.4 percent) and the United Kingdom (41.1 percent).

For context, internet penetration in South Africa currently sits at 70 percent, compared with 92 percent in the USA, and 98 percent in the UK.

But South Africa isn’t the only “developing” economy where the level of adoption of online financial services is higher than it is in the world’s largest economy.

At 45.5 percent of working-age internet users, Brazil also sees relatively high rates of online banking adoption, as does Malaysia (44.1 percent).

Various factors may contribute to these differences, but one of the clear takeaways from this data is that – provided the necessary infrastructure is in place and relevant services are available – a country’s economic standing isn’t the only determinant of whether its citizens will embrace online financial services.

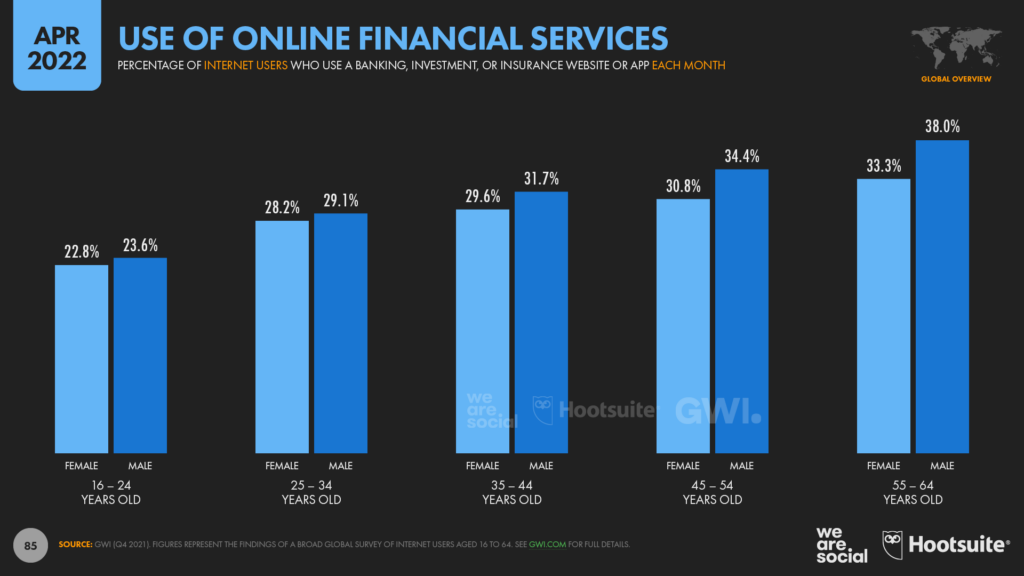

However, perhaps surprisingly, GWI’s data does reveal that older internet users are considerably more likely to use online banking, investment, and insurance services than younger users are.

Once again, there may be various reasons for these differences, but these findings provide valuable reference and context for policymakers hoping to address issues relating to financial empowerment.

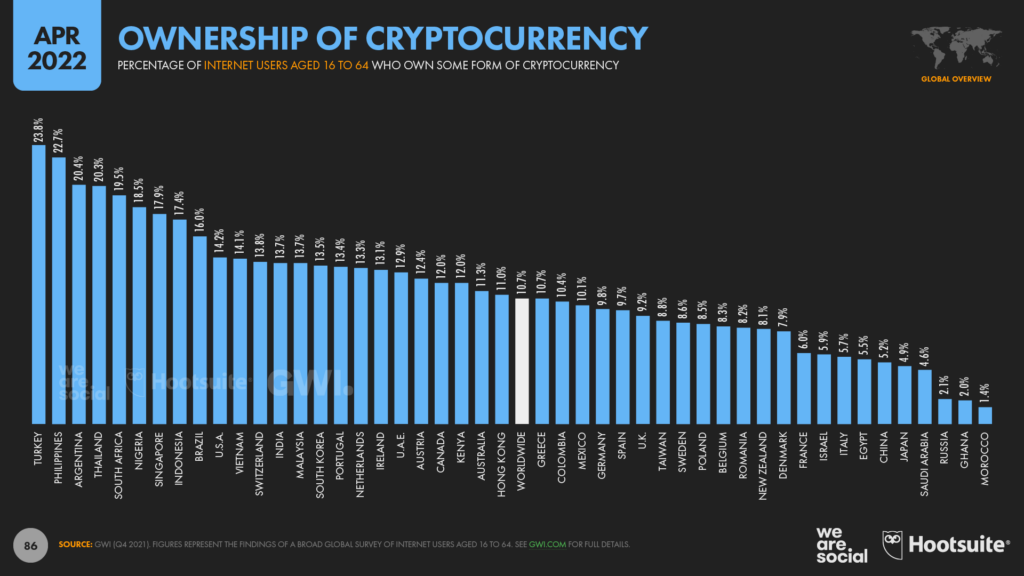

Cryptocurrency

Turning to more innovative financial products, it’s interesting to note that people in developing economies are considerably more likely to have embraced cryptocurrencies than their peers in more economically developed countries are.

Overall, GWI reports that 1 in 9 working-age internet users around the world now owns some form of “crypto”, but this figure jumps to almost 1 in 4 in Turkey.

The rapid decline in the value of Turkey’s fiat currency over recent months likely played an important role in this trend, and may help to explain why ownership of crypto in Turkey has jumped by roughly 28 percent in just the past 3 months.

However, cryptocurrencies are also increasingly popular across South-East Asia, with more than 1 in 5 working age internet users in the Philippines (22.7 percent) and Thailand (20.3 percent) saying that they now own some form of crypto.

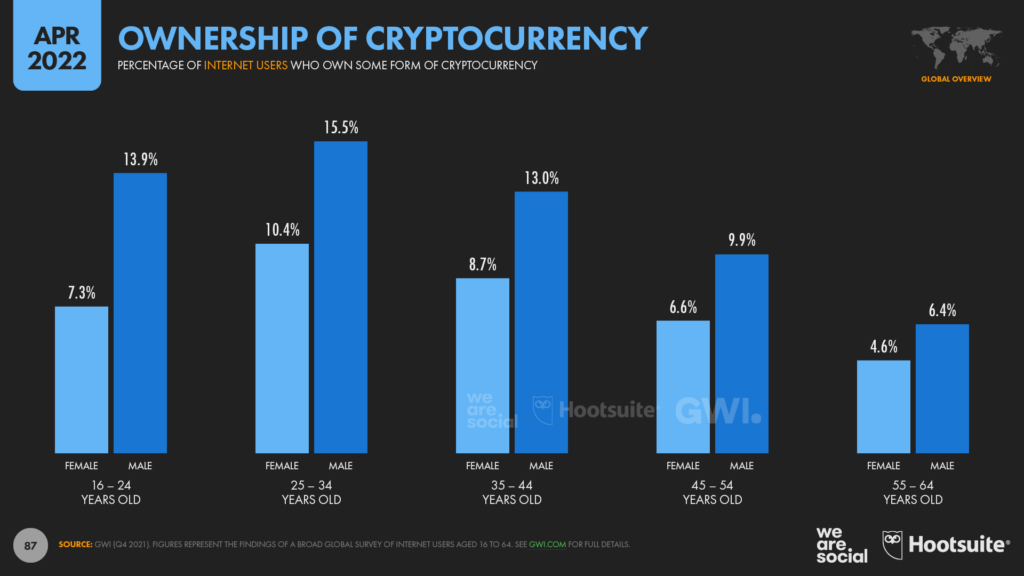

Ownership of digital currencies is significantly skewed towards male internet users though, with GWI’s data indicating that – at a global level – men are almost 60 percent more likely to own crypto than women are.

Online education

With the exception of the highest-level metrics like internet adoption, most of the data we feature in our Global Digital Reports focuses on audiences aged 13 and above, especially working-age adults.

As a result, we’re currently unable to offer many insights into digital’s role in the education of younger children.

However, the data we do have indicate that “education” remains an important driver for internet use amongst adult audiences too, and there are still plenty of important takeaways from this research.

For example, GWI reports that half of all working-age adults go online to “research how to do things”, revealing that continuous learning is an important consideration for internet users everywhere.

“Learning how to do things” need not necessarily involve the acquisition of a major new skill or academic qualification though, and in many cases, it may simply involve addressing everyday challenges such as how to tie a tie, or how to fix a dripping tap (or faucet, if you prefer).

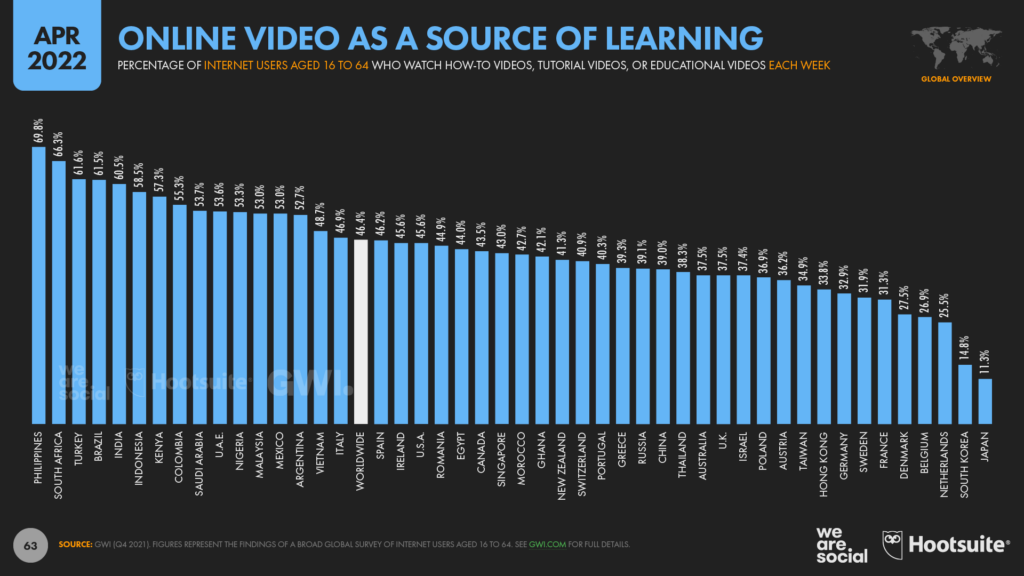

However, the huge popularity of “how-to” videos all across the internet demonstrates just how much we rely on the internet to learn the everyday skills that we need. Indeed, GWI reports that 46.4 percent of working-age internet users around the world now watch online tutorials, “how-to” videos, and educational content every week.

However, this figure soars to almost 70 percent in the Philippines, while figures across other developing economies are consistently higher than the figures for more economically developed nations.

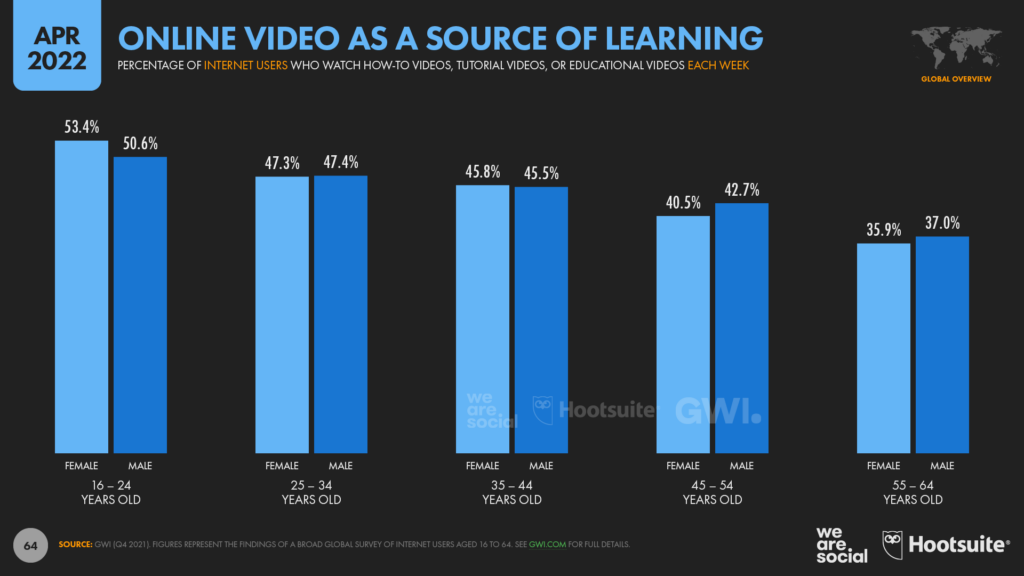

GWI reports that more than half of all Gen Z internet users currently develop their knowledge and skills online each week, with young women the most likely to turn to the internet for learning.

More than a third of Baby Boomers still go online for learning each week though, which may be of particular interest to researchers and brands hoping to address challenges associated with neurodegenerative diseases like dementia.

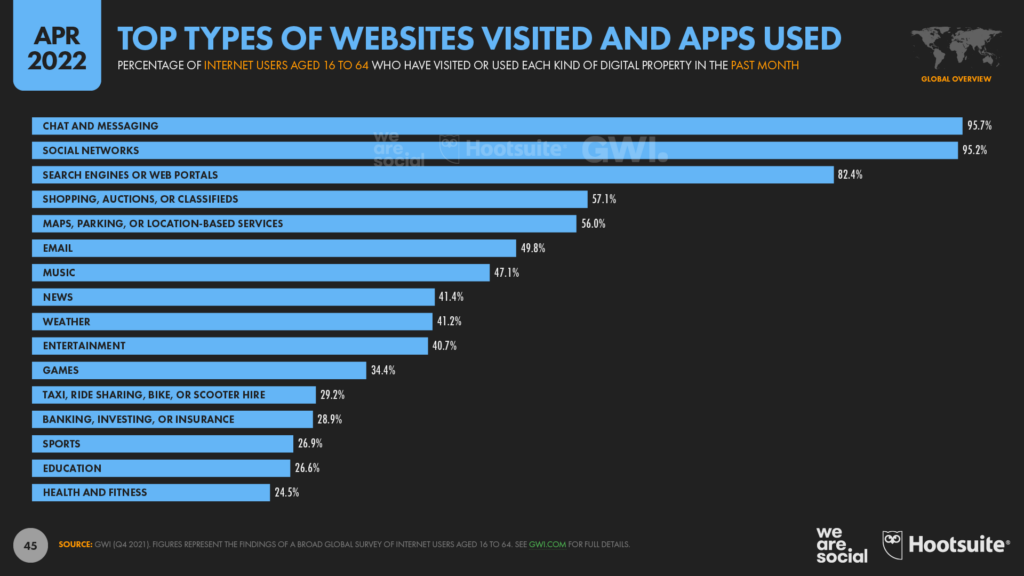

Online activities

When it comes to the kinds of online properties that people visit and use, GWI reports that social activities such as chat and social networking come out top, with 95 percent of working-age internet users saying that they’ve used at least one of these properties in the past 30 days.

Search engines and web portals rank third in terms of popularity, with more than 4 in 5 respondents in GWI’s survey saying they’ve visited at least one of these sites in the past month.

Meanwhile, 57 percent of respondents say that they’ve done some form of online shopping in the past 30 days, demonstrating just how important ecommerce has become for the world’s internet users.

Once again though, this dataset demonstrates the diversity of the world’s online activities, reinforcing the idea that digital connectivity has become a “layer” that runs through almost every aspect of our daily lives.

The world’s top websites

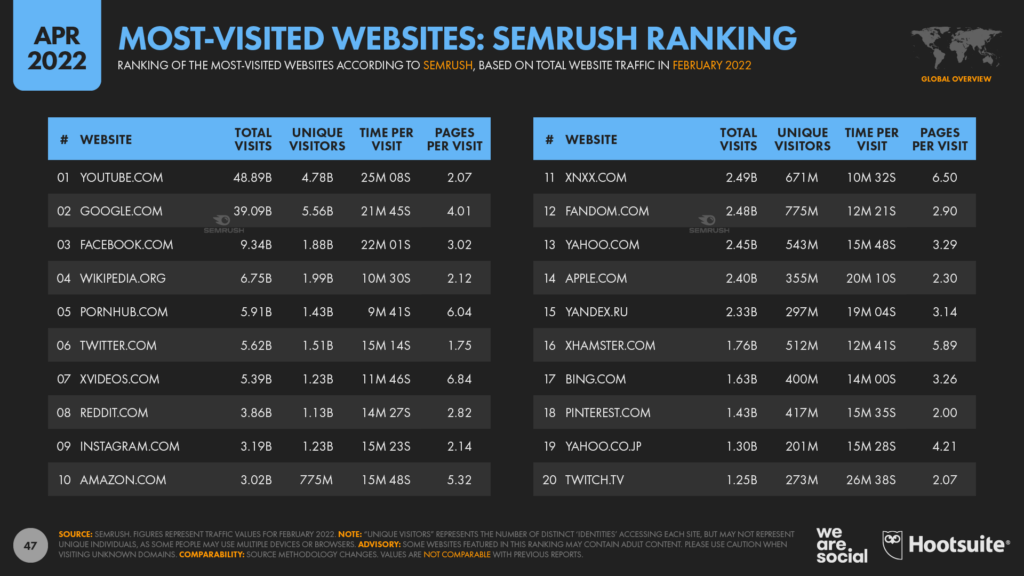

This diversity is visible in the latest rankings of the world’s most visited websites too.

Our partner Semrush reports that YouTube was the most visited website in February 2022, making this one of the rare occasions when Google.com hasn’t topped the global traffic charts.

Semrush’s data indicates that YouTube’s website hosted almost 50 billion distinct user “sessions” in February, with visitors spending an average of more than 25 minutes on the site.

This suggests that people spent more than 20 billion hours on YouTube.com in February 2022 alone, which equates to more than 2.3 million years of combined human existence.

However, it’s worth noting that this only represents activity on YouTube’s website, and doesn’t include time spent using the platform’s native mobile apps.

But Semrush reports that Google.com still attracts the greatest number of unique “visitors” of any website in the world, attracting more than 5.5 billion unique visitor identities during February 2022 [note: the same person may use multiple devices to access the same website over the course of a month, so this figure does not necessarily represent unique individuals].

And despite the huge amount of time that people spend on Facebook’s native mobile app, the platform’s website still attracts significant activity too.

Meanwhile, Wikipedia.org remains one of the world’s most-visited websites, reinforcing the importance of the role that “finding information” plays in the world’s internet activities.

Shifting to ecommerce, Amazon.com saw more than 3 billion visits to its website in February, which was enough to place the world’s most-visited ecommerce site in the overall top 10.

Apple’s primary web domain also makes an entrance in top 20 websites for February 2022, with Semrush’s analytics indicating that the site attracted 2.4 billion visits over the course of the month.

New readers may be surprised to learn that Yahoo! continues to be a top force in online media, with the platform continuing to attract hundreds of millions of visitors to its web properties.

Semrush reports that Yahoo!’s primary “.com” domain ranked 13th in terms of global web traffic in February 2022, and its Japan-focused “.co.jp” domain ranked 19th.

But we’d be remiss not to acknowledge that “adult” sites also account for four of the top 20 places.

These properties attracted a combined total of 15.5 billion visits in February 2022, and accounted for more than 2.8 billion hours of online time in that one month alone – the equivalent of 322,000 years of combined human existence.

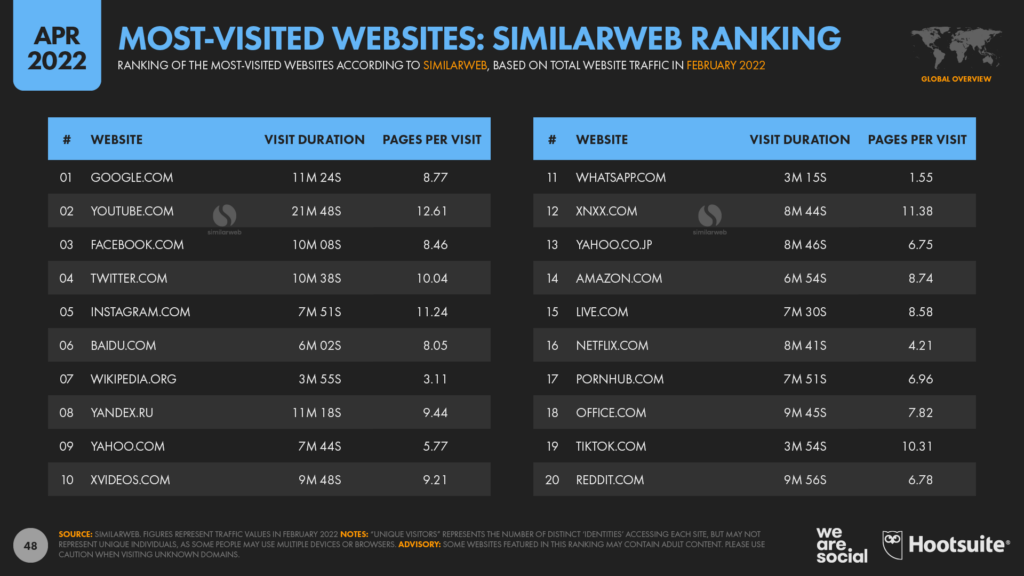

SimilarWeb has a slightly different take on the world’s top 20 websites, although many of the themes that we see in Semrush’s data are also present in SimilarWeb’s data.

However, one of the more notable differences in SimilarWeb’s rankings is the position of Twitter, which SimilarWeb ranks fourth overall.

SimilarWeb also places TikTok.com – i.e. the platform’s website – in 19th place in the global ranking for February 2022.

This finding is all the more impressive when we consider that the vast majority of TikTok activity will likely take place within the platform’s native mobile app, which isn’t included in this data.

Devices used to access the internet

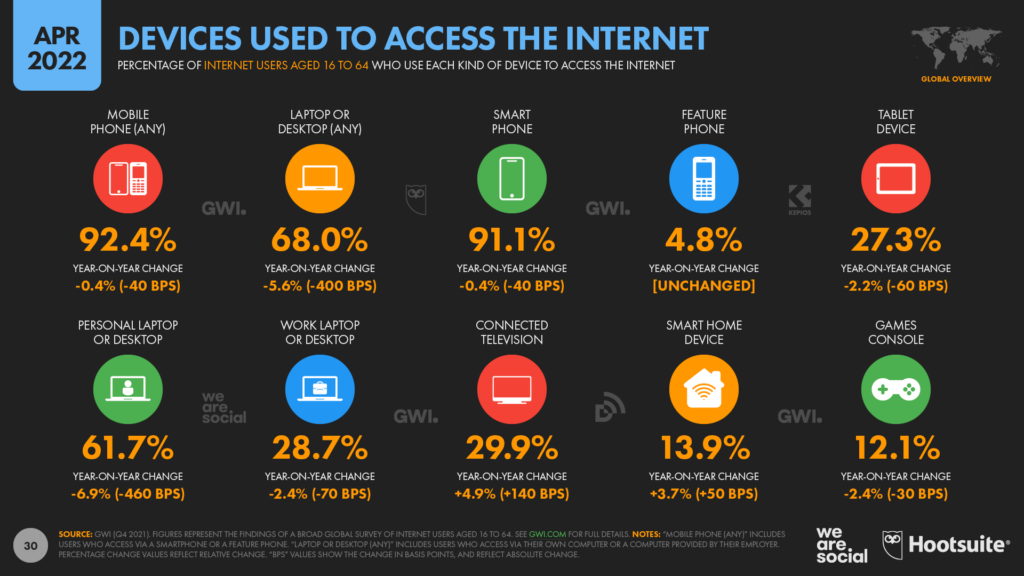

Cell phones continue to be the world’s most-used connected devices, with GWI reporting that more than 92 percent of working-age internet users go online via mobile devices.

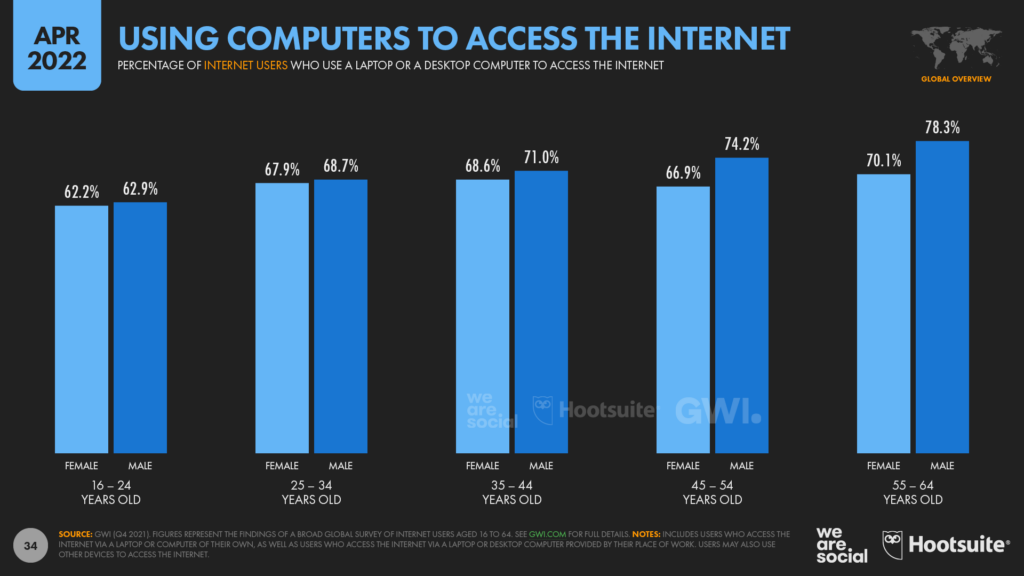

However, more than two-thirds (68 percent) of the world’s internet users still go online via laptop and desktop computers, although it is worth noting that this figure has fallen from 72 percent this time last year.

3 in 10 people also connect to the internet via their television, and more people now go online via televisions than go online via tablet devices.

But mobile phones aren’t just the most widely used devices.

GWI’s latest research also reveals that mobile phones now account for almost 55 percent of the time we spend online, and that figure rises to almost 60 percent across Thailand, Indonesia, China, and India.

Age plays an important role in shaping device preferences though.

For example, Gen Z users are considerably less likely to go online via a computer than users in their parents’ generation are.

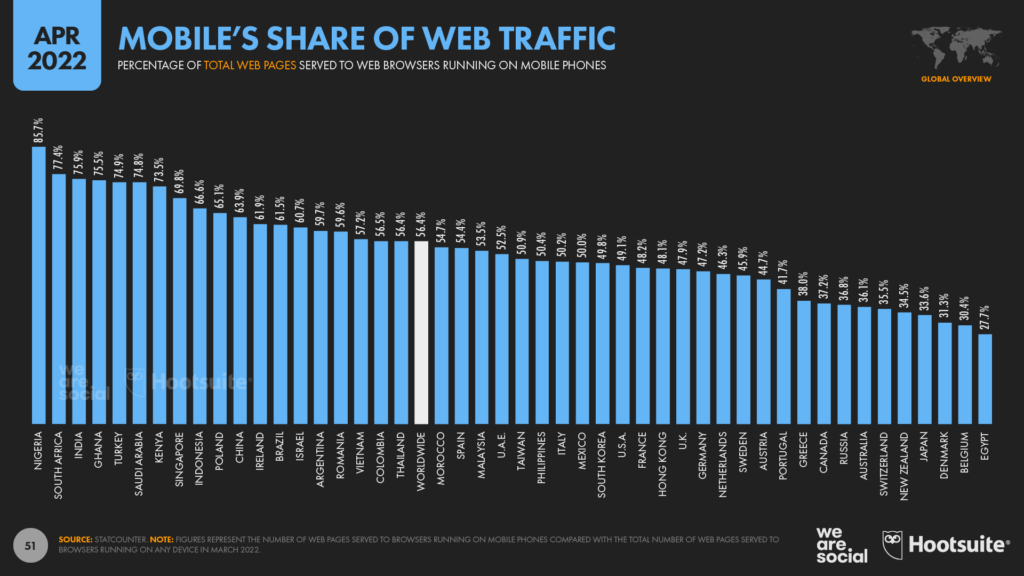

Meanwhile, the latest data from Statcounter shows that mobile phones accounted for more than 56 percent of global web traffic in March 2022, up from 54 percent this time last year.

However, mobile’s share is considerably higher in countries across Africa and Asia, with Statcounter reporting that mobiles accounted for almost 86 percent of total web traffic in Nigeria in March 2022.

Internet connection speeds accelerate

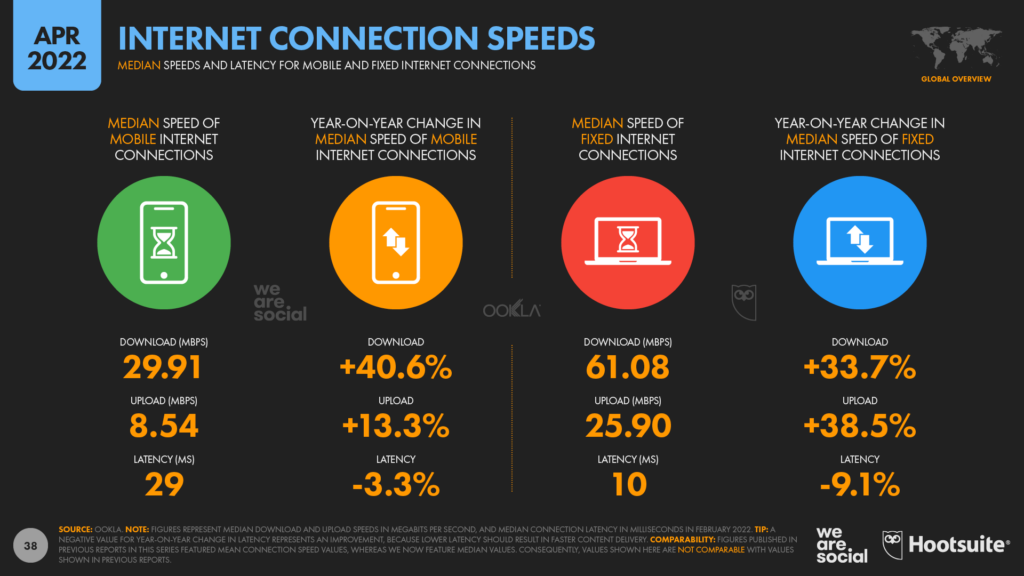

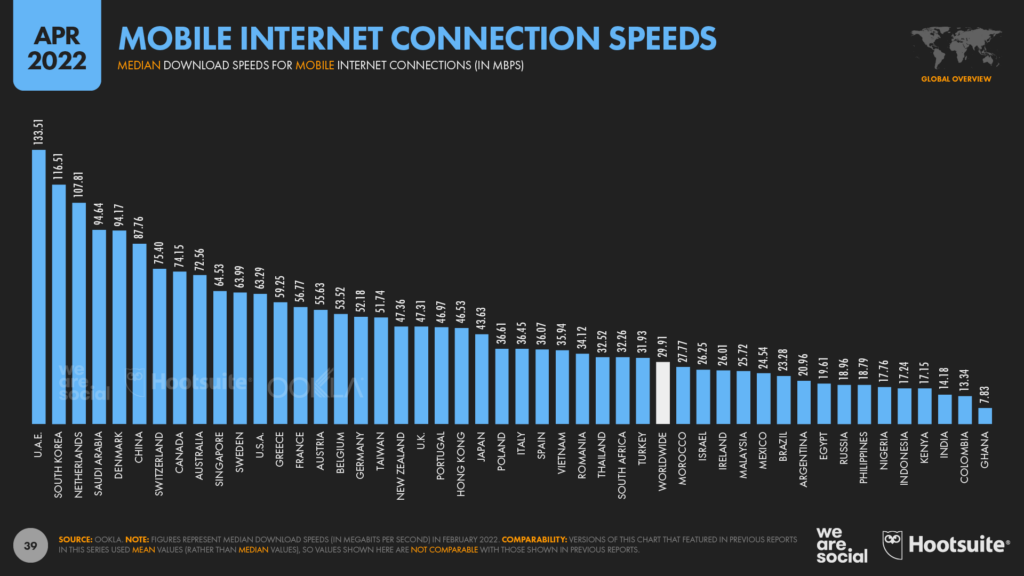

The latest data from our partner Ookla reveals that internet connection speeds have surged over the past 12 months.

The world’s mobile internet users now enjoy a median download rate of 29.9Mbps, which means that well over half of all the world’s mobile internet users should now be able to stream 4K video over their mobile data connection without any buffering or loss of image quality.

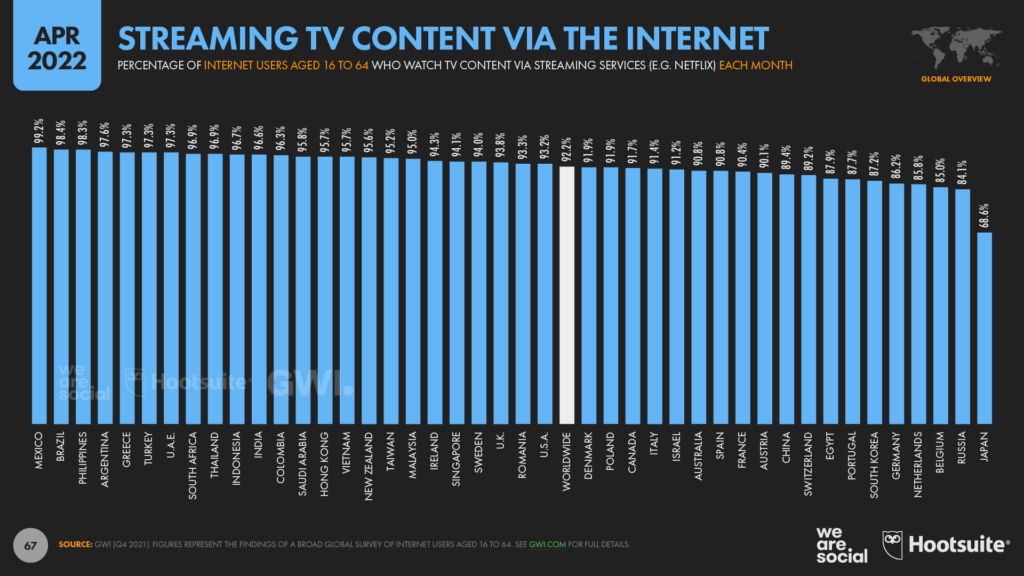

This has particular relevance when we consider the latest research from GWI, which reveals that a whopping 92 percent of working-age internet users now stream movies and TV shows via the internet.

Encouragingly, Ookla reports that median mobile data speeds have increased by more than 40 percent since this time last year, with median download bandwidth now 8.6Mbps higher than the equivalent rate for this time last year.

However, the median fixed internet connection still delivers data twice as quickly as the median mobile connection, with half of all internet users with fixed connections now enjoying downloads speeds in excess of 61Mbps.

Fixed download speeds have increased by more than a third over the past year too, resulting in an additional 14.5Mbps of download bandwidth compared with equivalent figures from 12 months ago.

However, echoing the findings of A4AI’s “Advancing Meaningful Connectivity” report, connection speeds vary significantly from country to country.

Internet connection speeds by geography

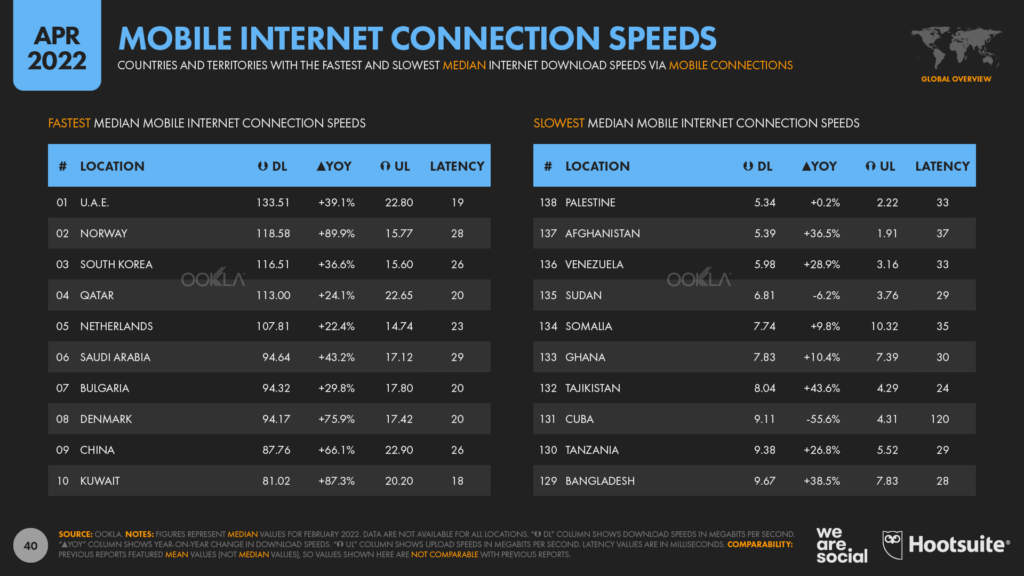

Ookla’s latest analysis reveals that networks in the United Arab Emirates currently offer the fastest median mobile data speeds in the world, at 133.4Mbps.

Mobile connections in the UAE continue to accelerate too, with the median download speed in February 2022 clocking in at 39 percent higher than the figure for February 2021.

However, the company also reports that median download speeds are still stuck below 10Mbps in eleven countries around the world.

Mobile users in Palestine currently suffer from the slowest mobile connections, with median download bandwidth in the country languishing at just 5.34Mbps in February 2022.

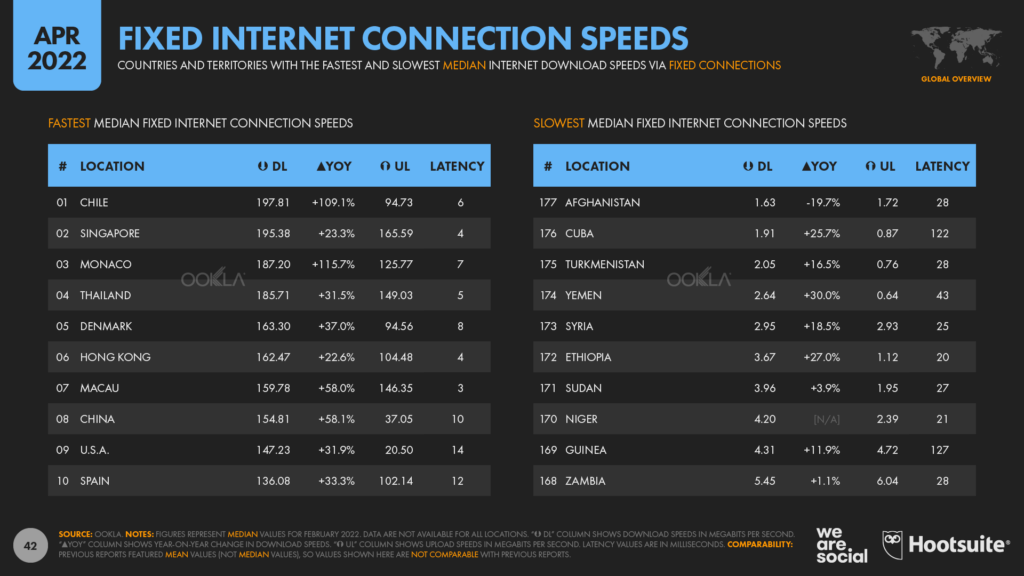

Meanwhile, Ookla’s data shows that Chile has overtaken Singapore to take top spot in the fixed connection speed rankings.

Median fixed-connection bandwidth has more than doubled in Chile over the past year, reaching close to 200Mbps in February 2022.

However, a very different picture emerges at the other end of the spectrum.

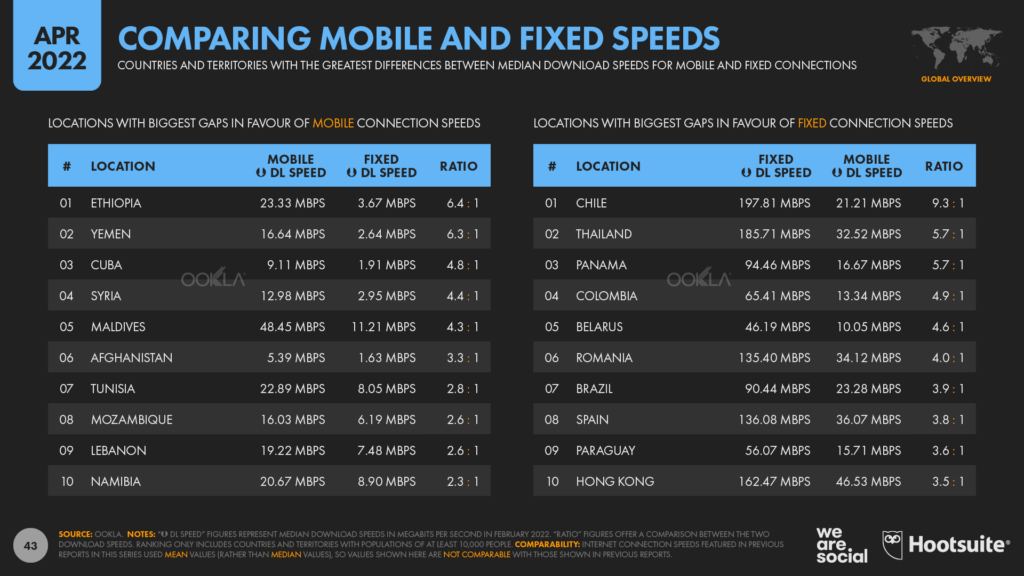

Users with fixed internet lines still struggle with median connection speeds below 10Mbps in a total of 38 countries around the world, with half of all users in Afghanistan enduring speeds of less than 1.63Mbps.

Interestingly, the median mobile internet connection in Afghanistan is now more than 3 times faster than the country’s median fixed connection.

This situation isn’t unique to Afghanistan either, with Ookla’s data revealing that median mobile connection speeds now outpace median fixed connections in a total of 51 countries.

The mobile-to-fixed-speed ratio is greatest in Ethiopia, where mobile internet connections are typically 6 times faster than fixed connections.

Meanwhile, median mobile download speeds are more than double the median fixed download speeds across a total of 16 countries.

Content accessibility

Even when audiences have access to connected content, however, that content may not necessarily be accessible to them.

Issues such as literacy may pose fundamental barriers to content accessibility, while the ability to speak, read, and write languages other than one’s native tongue may also determine the extent to which online content is “accessible”.

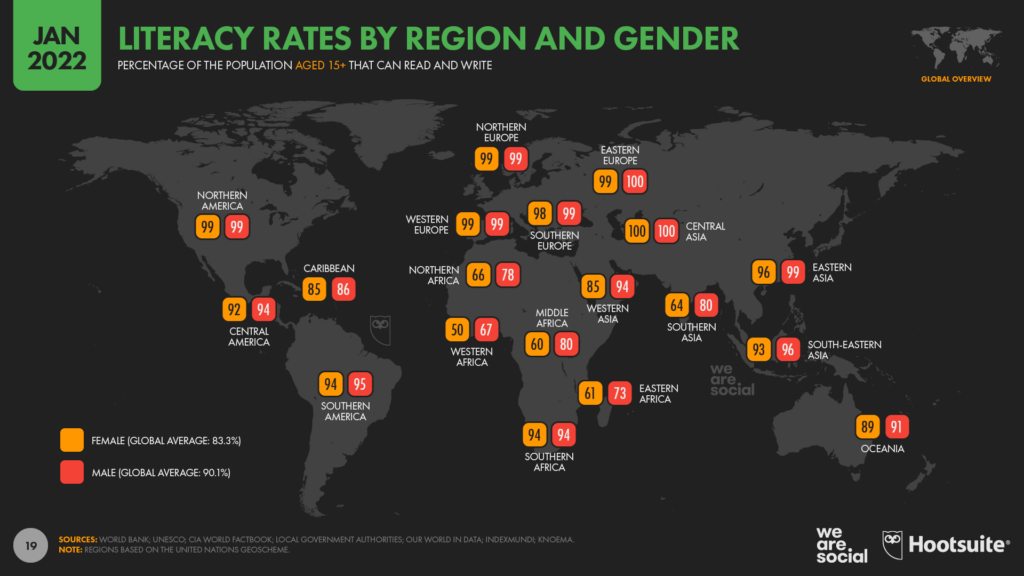

Global literacy rates have improved dramatically over the past few decades, but there are still 13 countries around the world where less than half of the adult population is literate.

Alarmingly, literacy rates amongst women are often even lower, and reports suggest that less than half of the female population is literate in a total of 19 different countries [note: you’ll find the chart below in our Digital 2022 Global Overview Report].

However, literacy in a local language may still not be enough to unlock the full value of the content available on today’s internet.

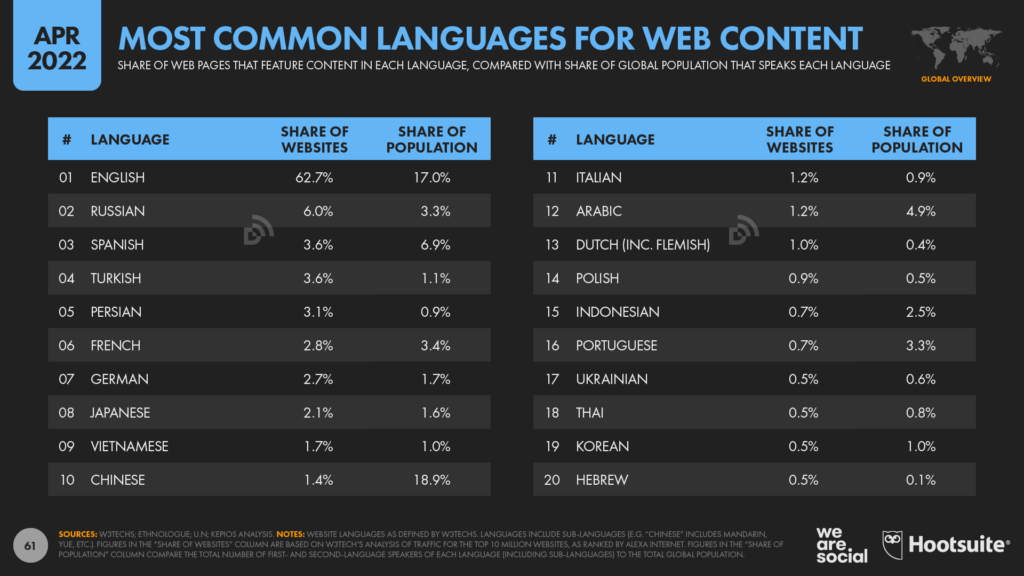

Data from W3Techs suggests that more than 6 in 10 websites are written in the English language, even though English speakers only represent 17 percent of the global population.

The company’s rankings reveal that English isn’t the only language that “over indexes” when it comes to online content either, with Russian, Turkish, and Persian all appearing high up in the content rankings.

Conversely, W3Techs’ data reveals that a number of languages – notably Spanish, French, and Chinese (in its various forms) – are all under-represented in web content when compared with the number of people who speak those languages.

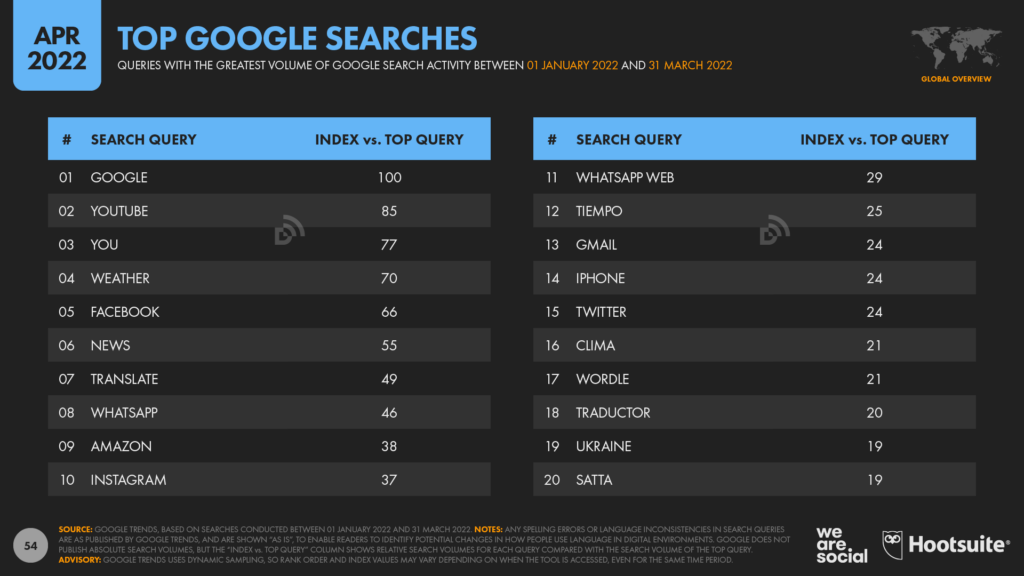

But there’s also some good news when it comes to language accessibility, with the use of online translation tools gaining momentum around the world.

Data from Google Trends reveals that “translate” was one of the top-ten most searched queries around the world in the first three months of 2022, and related queries in other languages (e.g. “traductor”) also see high levels of interest.

Research from GWI reinforces these findings, with the company’s global survey revealing that 3 in 10 internet users now make use of online translation tools every week.

Use of these tools is considerably higher in developing economies though, especially across Latin America.

Meanwhile, video formats may help to make content more accessible to people with lower levels of literacy, as well as to people with certain disabilities.

Similarly, the use of voice interfaces and image recognition tools to search for content on the internet without the need to type queries and read results may also help to make online discovery more accessible.

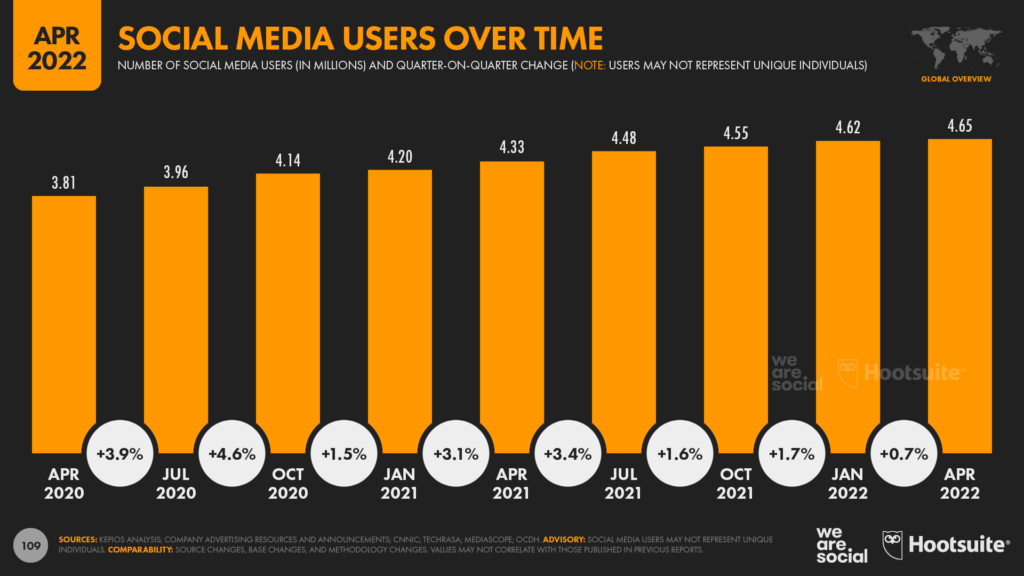

Social media growth slows

As we’ve been anticipating for some time now, social media user growth rates have slowed over the past three months compared with the quarterly growth rates we’ve been seeing since the start of the COVID-19 pandemic.

Kepios analysis reveals that global social media users have only increased by 32 million since the start of 2022, equating to quarterly growth of 0.7 percent.

The global total has still increased by 7.5 percent year on year though, with an additional 326 million new users over the past 12 months taking the global count to 4.65 billion by the start of April 2022.

As always, it’s worth stressing that this figure may not represent unique individuals, but it does indicate that well over 9 in 10 internet users now visit social media platforms every month.

Moreover, if we focus on “eligible” audiences aged 13 and above, the data also suggest that more than three-quarters of all the people on Earth who can use social media already do so, which may in part explain why growth rates have started to slow.

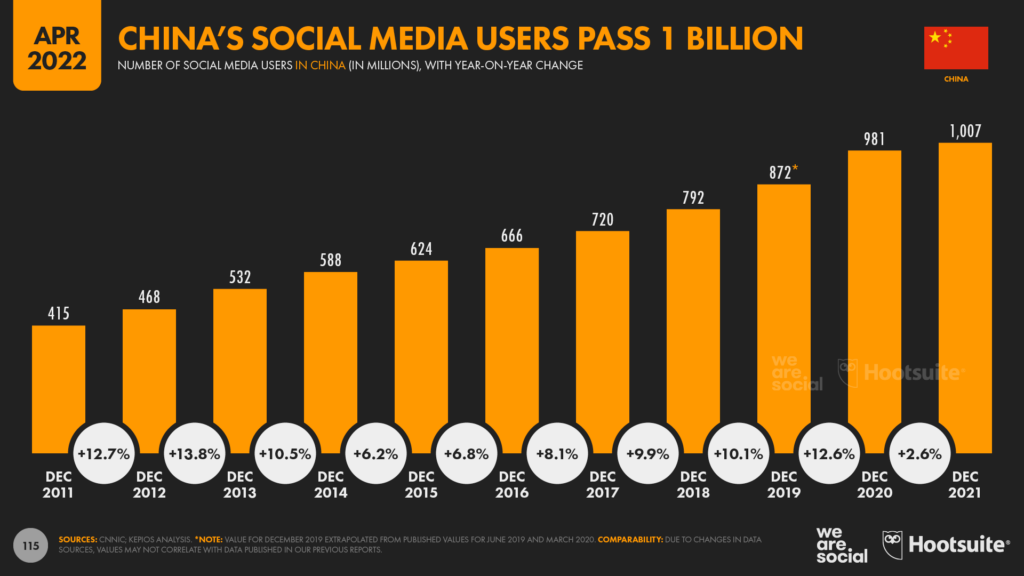

China’s impressive social media milestone

The latest report from the China Network Information Centre (CNNIC) reveals that more than 1 billion people in China now use social media and messenger platforms.

CNNIC’s data shows that the number of social media users in the country grew by 2.6 percent during 2021, reaching 1.007 billion by the end of the year.

CNNIC’s reports indicate that it has taken just over 8 years for the number of social media users in China to double.

The latest figures suggest that roughly 70 percent of the country’s total population now uses social media on a regular basis, but a massive 97.5 percent of the country’s internet users are already active on social platforms.

For context, China is now home to 21.6 percent of all the world’s 4.65 billion social media users.

However, data also reveal that there are 440 million people in China who do not currently use social media, so there’s still plenty of room left for growth in the country’s social media population.

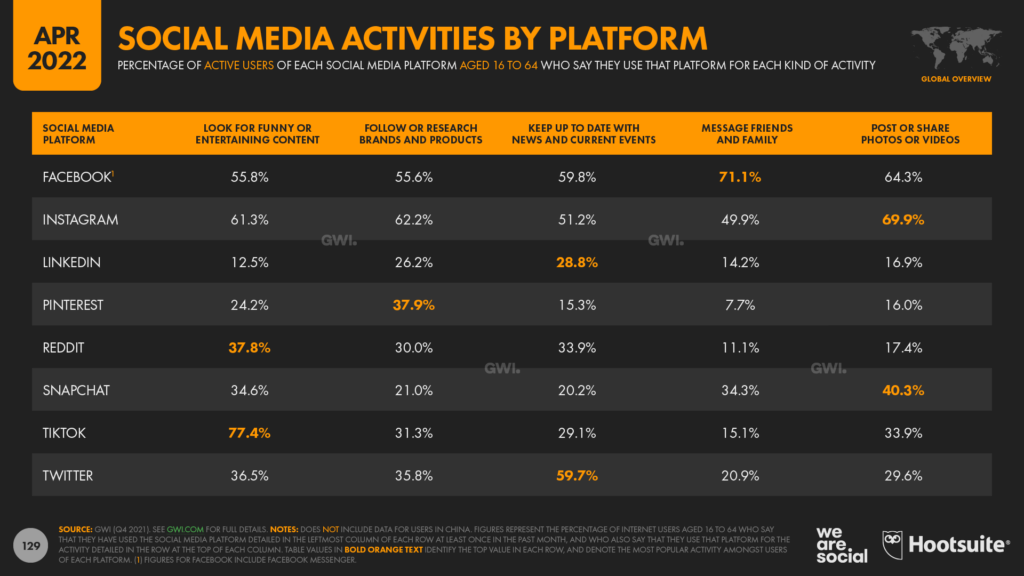

Users’ activities vary across social platforms

One of the new additions to this quarter’s report explores people’s activities across different social media platforms.

And this new GWI dataset reveals some fascinating insights.

For example, 7 in 10 Facebook users say that they use the platform to communicate with friends and family, making this the most popular activity on Facebook.

However, just 15 percent of TikTok’s users say that they use the platform for this kind of communication.

Instead, GWI’s data clearly demonstrate that TikTok is an entertainment channel, with a massive 77 percent of the platform’s users saying that they use TikTok to look for funny and entertaining content.

Meanwhile, Instagram and Snapchat users appear to be most interested in publishing their own content.

And this specific data point highlights one of the key differences in current behaviours between Instagram and TikTok.

Almost 7 in 10 Instagram users (69.9 percent) say that they publish photos and videos to Instagram, compared with just 1 in 3 TikTok users (33.9 percent) who say that they post videos to TikTok.

Another interesting takeaway for marketers is that Pinterest users seem to be particularly interested in brand-related content, with 37.9 percent of the platform’s users saying that they use the platform to follow or research brands.

Staying up to date with news and current events is the top platform activity amongst users of both LinkedIn and Twitter.

These findings have clear value for brands looking to develop a more strategic approach to social media marketing, because they highlight the different usage contexts and user motivations across each platform.

As you might expect though, users’ activities still vary meaningfully by geography and by demographic, so be sure to check out GWI’s full dataset if you’d like to learn more about the potential implications of this data for your brand.

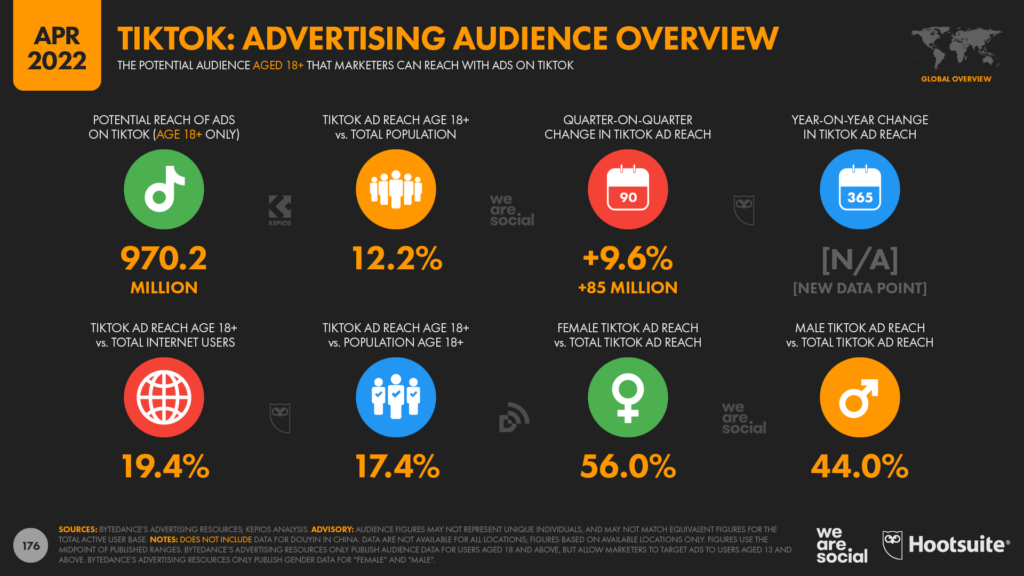

Growth in TikTok’s advertising audience accelerates

The latest numbers published in Bytedance’s advertising resources reveal that TikTok’s advertising reach grew faster in the first three months of 2022 than it did in the final three months of 2021.

Marketers can now reach 970 million users aged 18 and above with ads on TikTok, which is almost 10 percent higher than the number of users that they could reach at the start of this year.

For context, that means TikTok’s adult audience is currently growing at a rate of almost 1 million new users every day.

Interestingly, TikTok’s advertising tools allow marketers to target ads to users aged 13 and above, but the same tools only provide audience reach data for users aged 18 and above.

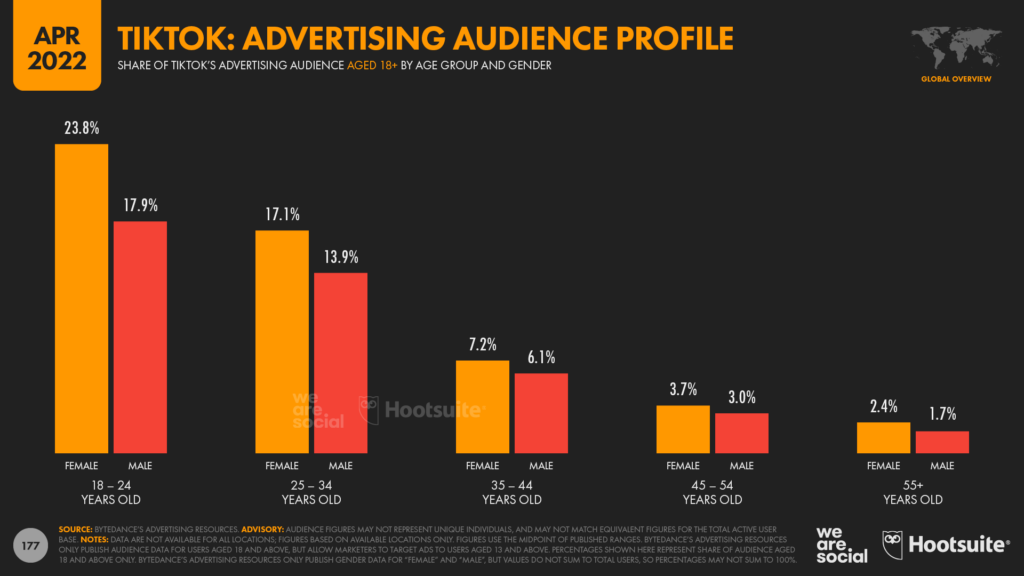

However, if we look at the demographic profile of audiences aged 18+, it seems likely that users below the age of 18 will account for a meaningful share of the platform’s overall user base, so it’s safe to assume that TikTok’s total ad reach is considerably higher than the published figures suggest.

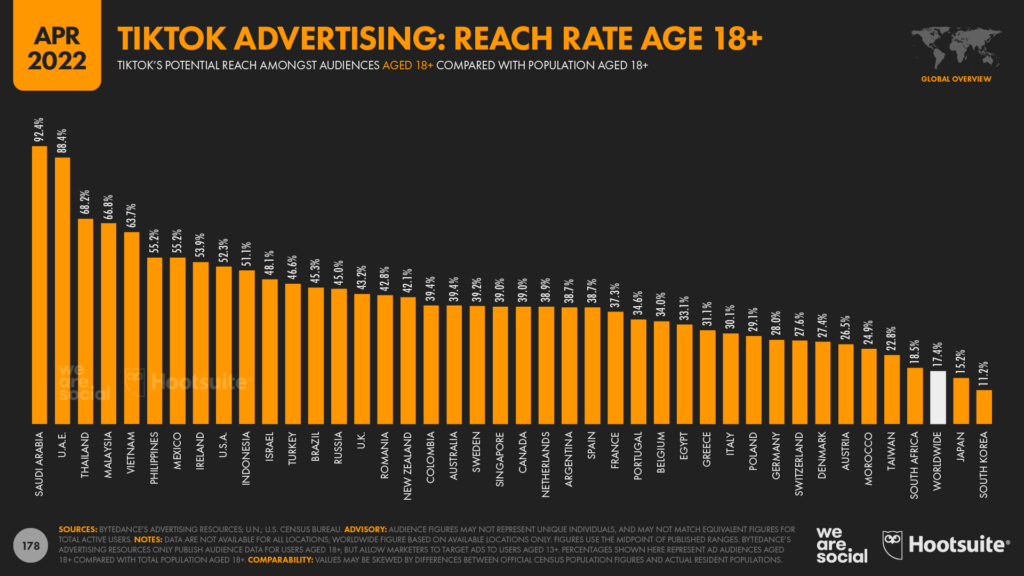

Individual country data reveals that TikTok is particularly popular with audiences in the Middle East and South-East Asia.

Saudi Arabia and the UAE see the highest rates of adoption amongst adults aged 18 and above, although it’s worth noting that these figures may be somewhat skewed by differences between official census counts and actual resident populations.

Meanwhile, TikTok’s audience reach figures are now equivalent to more than two-thirds of the adult population in Thailand and Malaysia, and they’re also well over 50 percent for South-East Asia as a whole.

Bytedances’s latest ad reach figures also suggest that more than half of all US adults now use TikTok every month.

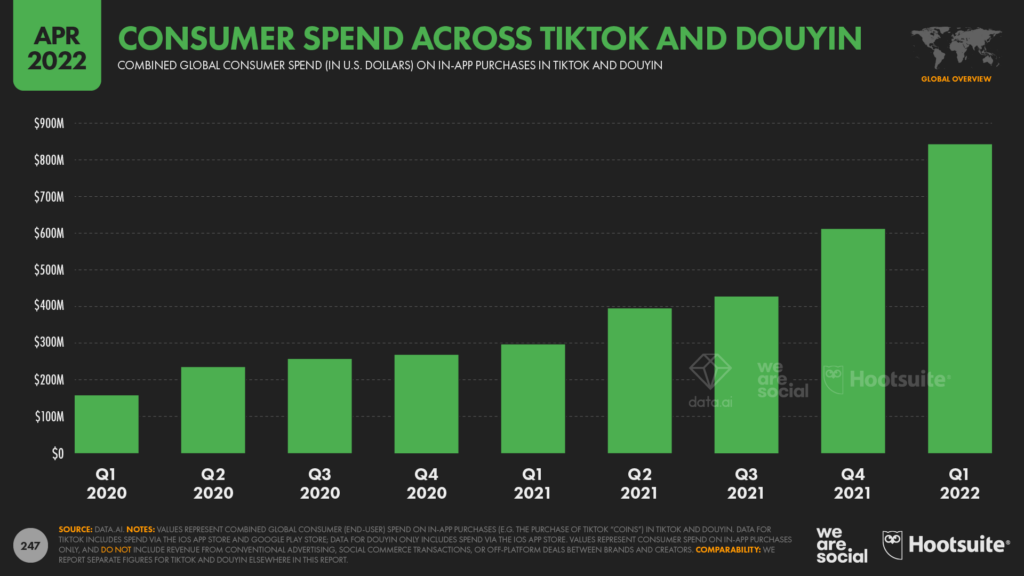

Consumer spend on TikTok hits new records

But it’s not just TikTok’s user numbers that are showing healthy growth.

New research published by Data.ai reveals that users spent more than USD $620 million on TikTok in the first three months of 2022, and an additional USD $220 million on the platform’s Chinese sister app, Douyin.

The combined USD $840 million total is 40 percent higher than the platforms’ in-app spend for the previous three-month period, and is the largest sum ever earned by a mobile app in a single quarter via end-consumer spend.

However, what makes these figures particularly impressive is that they only include in-app purchases of the platforms’ “coins”, which allow the platforms’ users to buy virtual gifts for creators, in an act somewhat akin to tipping.

In other words, these figures do not include conventional advertising spend or social commerce transactions, nor do they include marketing deals struck between brands and influencers.

The United States accounted for the greatest share of TikTok’s consumer revenue in Q1, with Americans spending more than USD $310 million on in-app purchases between January and March 2022.

Crucially, US consumer spend on TikTok has more than doubled in the first 3 months of 2022, with data.ai reporting quarter-on-quarter growth of 125 percent in Americans’ in-app TikTok purchases.

Meanwhile, alongside China, users in Kuwait, Germany, and Saudi Arabia also delivered meaningful contributions to global consumer spend in TikTok in Q1 2022.

Data.ai reports that consumers around the world have now spent a combined total of more than USD $3.7 billion across TikTok and Douyin since the apps first appeared in app stores back in 2014, and well over half of that figure can be attributed to in-app purchases during the past 12 months.

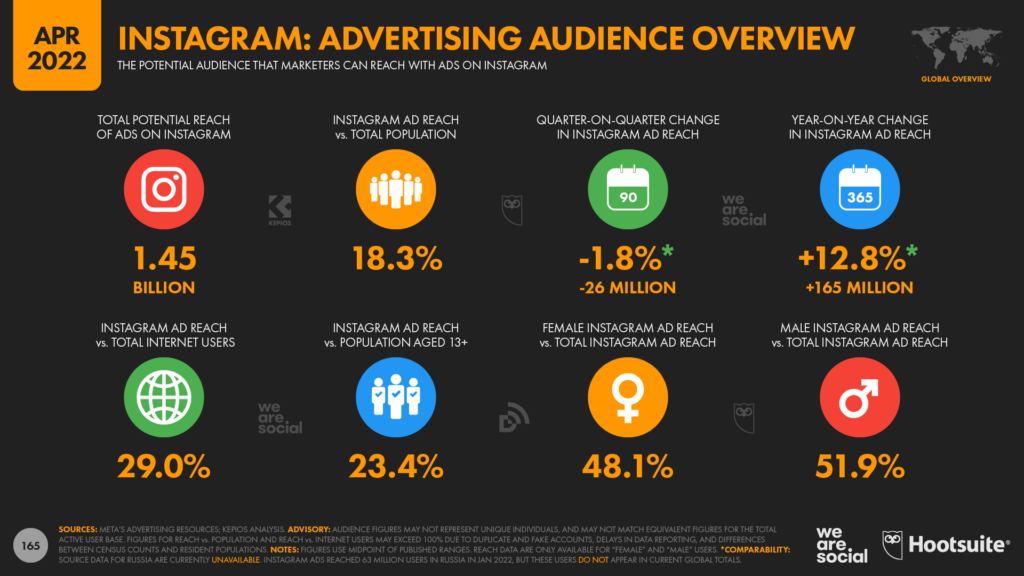

Impact of the Ukraine conflict on Meta’s audience data

Meta’s audience reach numbers show the profound impact of people fleeing Ukraine due to the country’s ongoing conflict with Russia.

At the time of reporting, Meta’s combined ad audience figure for Ukraine – which represents a combined but “deduplicated” audience across Facebook, Instagram, and Messenger – was 1.7 million users lower than the figure that the same tools reported for the country in January 2022.

This represents a drop of 7 percent compared with the start of the year, and – tellingly – women accounted for 1.4 million (80 percent) of the country’s displaced users.

Meta’s data doesn’t show any clear indication of where these people might have gone, however.

The company’s combined audience total for Poland has increased by 550,000 since January (+2.3 percent), but even if all of those new users were Ukrainian refugees, that figure would only account for about a third of the total 1.7 million displaced Ukrainian users.

Meanwhile, Meta’s audience figures in the country’s other immediate neighbours – Moldova, Romania, Hungary, Slovakia, and Belarus – only show modest increases in the tens of thousands.

This may be partly due to the way that Meta assesses people’s location based on what it considers to be their “home”, and the company may not include displaced users in another country’s total until they’ve remained there for a certain period of time.

Meanwhile, Meta has not published ad audience data for users in Russia for any of its various platforms since the outbreak of the war in Ukraine in late February.

If a marketer tries to select Russia as a location for ad targeting, the company’s tools currently display a warning that reads:

“Your ad includes or excludes locations that are currently restricted. Please remove affected locations from your audience settings.”

It’s unclear how long this restriction might last, and it seems that Meta is the only social media company currently limiting ad targeting in this way.

However, this restriction has had a meaningful impact on Meta’s overall audience numbers.

For context, in January 2022, Meta’s tools reported that:

Ads on Facebook could reach 8.6 million users in Russia

Ads on Instagram could reach 63.0 million users in Russia

Ads on Messenger could reach 2.9 million users in Russia.

None of these users now appear in Meta’s audience figures for these platforms, which has inevitably had a negative impact on each platform’s overall reach.

Despite these changes, global audience totals for Facebook and Messenger have still grown quarter on quarter, but Instagram’s reach has seen a more significant adjustment.

The latest global audience total for Instagram is 1.8 percent lower than the figure we reported in January 2022, equating to a drop in reach of 26 million users in just the past 3 months.

However, it’s unlikely that Meta has “lost” all of these users; rather, the company is simply preventing advertisers from targeting them with ads, likely due to the sanctions imposed by the US Government.

For reference, we estimate that – if it hadn’t been for these Russian restrictions – Instagram’s global ad audience would likely have grown by roughly 38 to 40 million users over the past three months, which would have equated to quarter-on-quarter growth of roughly 2.6 percent.

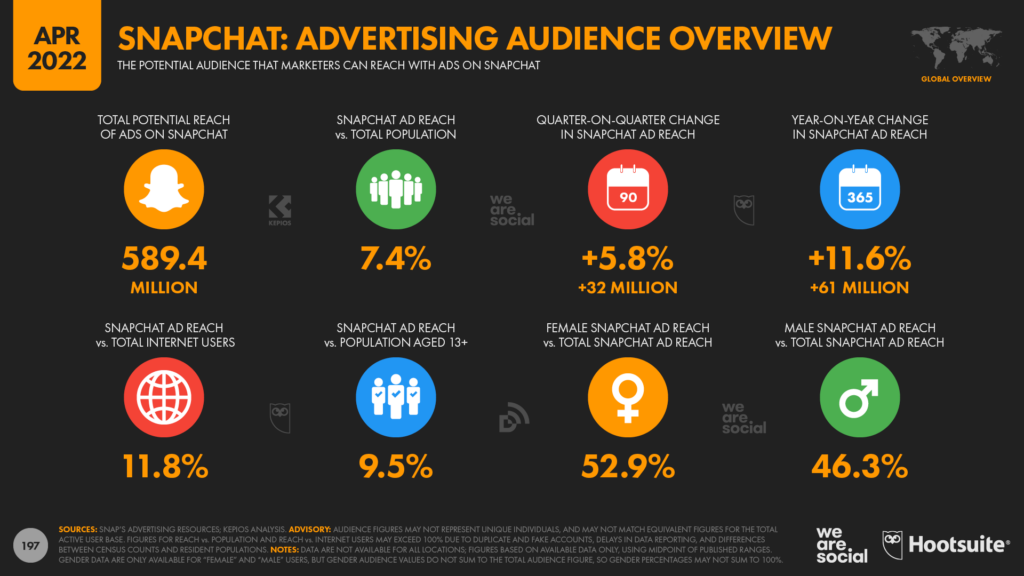

Snapchat continues its growth spurt

The latest figures published in Snap’s advertising resources reveal that Snapchat added another 32 million users to its global ad audience over the past 3 months, delivering impressive quarter-on-quarter growth of almost 6 percent.

Snap’s tools indicate that marketers can now reach more than 589 million users on Snapchat, which is 11.6 percent more than they could reach on the platform this time last year.

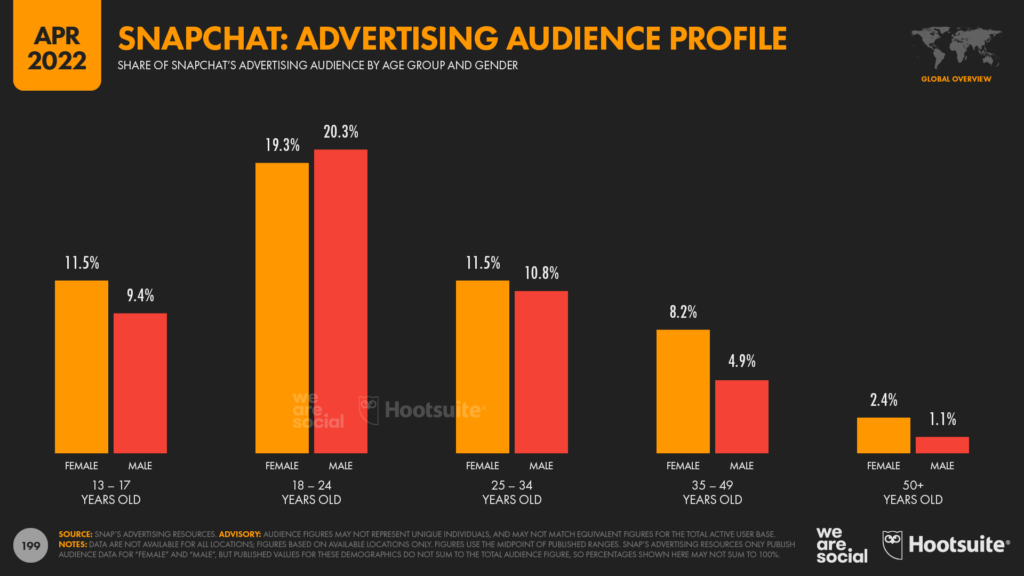

Importantly, Snapchat continues to gain momentum amongst younger users too, although the majority of the platform’s recent growth has come from users in their early 20s.

The company’s ad reach data suggests that audiences aged 13 to 17 grew by 3.7 percent over the past 3 months, compared with growth of 6.7 percent amongst users aged 18 to 24, and growth of 5.8 percent overall.

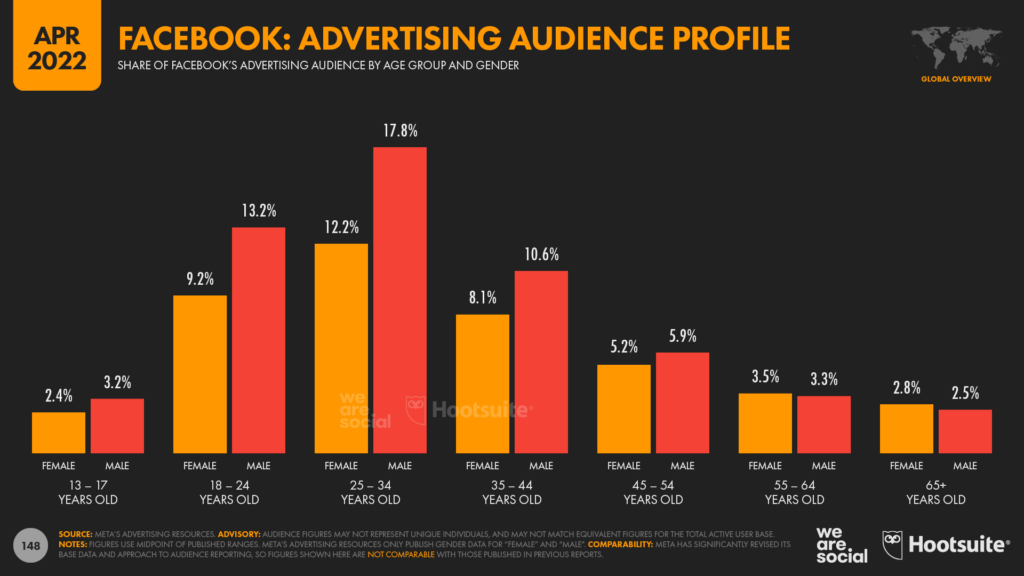

Facebook’s young audiences are still growing

And while we’re on the subject of younger audiences, Meta’s data offer plenty of evidence to counter recurring media reports that younger users are “abandoning” Facebook.

The company’s latest audience data reveals that marketers can now reach an additional 2.8 million teenagers on Facebook compared with January 2022, equating to quarter-on-quarter growth of 1.3 percent amongst this important demographic.

These trends may vary by country of course, but therein lies one of the most important takeaways for marketers: audience trends in one part of the world may have very little bearing on audience trends elsewhere, so do your due diligence, and check the data for your specific market(s).To help with that, be sure to check out our (free!) individual platform reports.

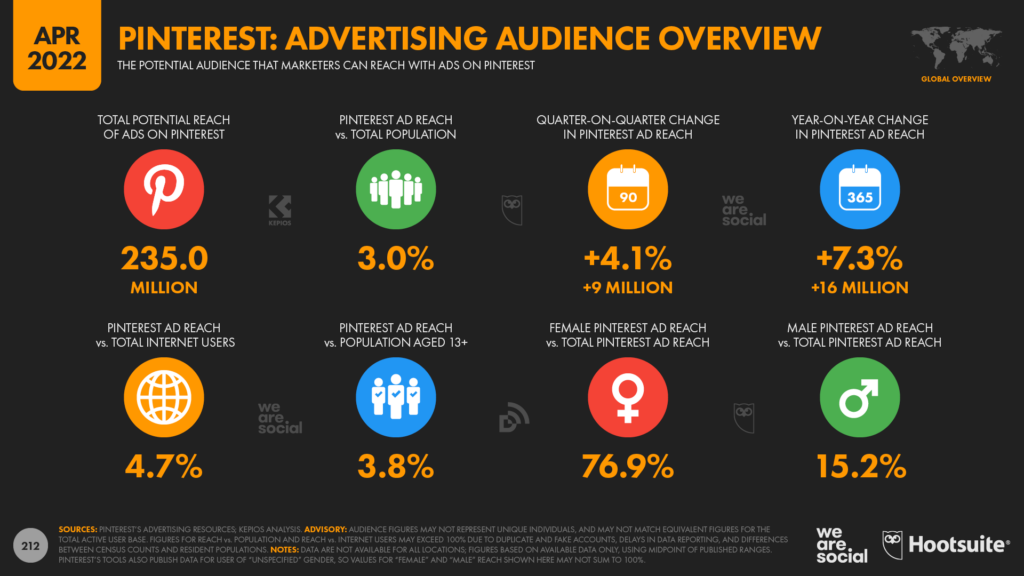

Pinterest returns to growth

After a dip in global reach at the end of last year, Pinterest’s planning tools suggest that the platform’s ad audience has already recovered its losses.

Global Pinterest ad reach stood at 235 million in April 2022, pointing to quarter-on-quarter growth of 4.1 percent.

Other data in this quarter’s report may also be of interest to marketers considering Pinterest ads, especially those in visual categories such as fashion.

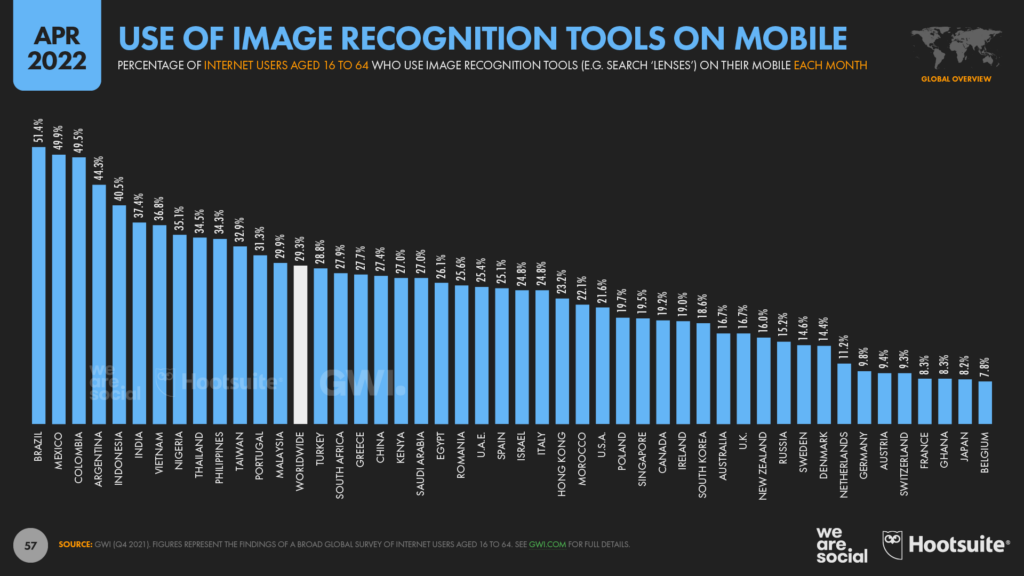

GWI reports that roughly 3 in 10 working-age internet users around the world now use image recognition tools each month, but that figure rises to more than 50 percent in Brazil, and just below 50 percent in Mexico and Colombia.

So, with Pinterest’s “Lens” tool offering compelling options when it comes to searching with images as search queries, there may be more to Pinterest marketing opportunities than sponsored pins alone.

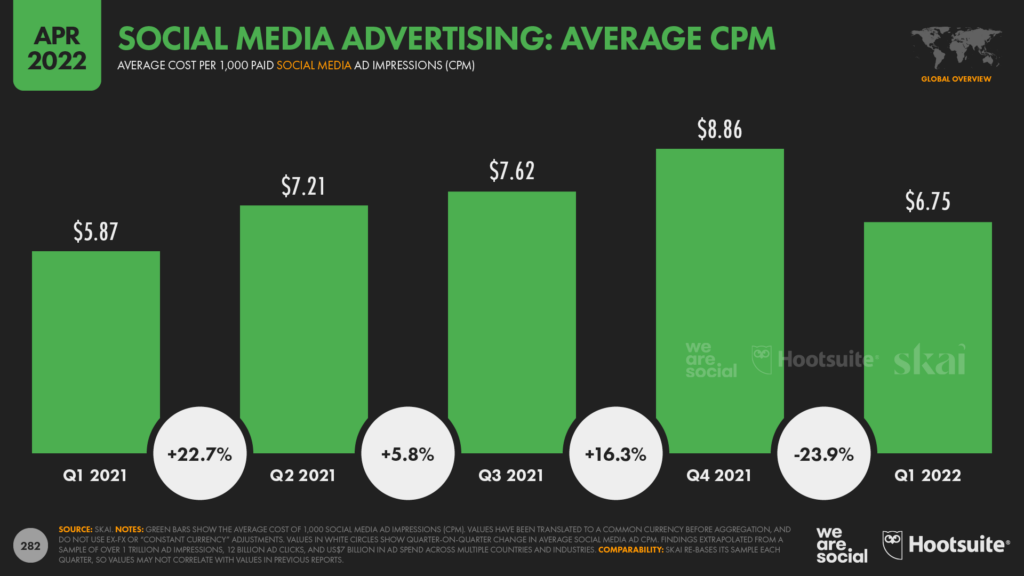

Social media CPMs are up again

Our partner Skai.io reports that the cost of 1,000 social media ad impressions (CPM) increased by 15 percent between Q1 2021 and Q1 2022.

Global CPMs averaged USD $6.75 across the first three months of this year, based on the company’s analysis of more than 1 trillion ad impressions around the world.

That CPM figure is roughly 24 percent lower than the average price marketers paid in Q4, but Q1 is typically the “cheapest” quarter of the year for ad spend, especially when compared to the ‘holiday’ quarter that precedes it.

For context, if current year-on-year growth trends were to continue through to Q4 this year, marketers should expect to pay an average of more than USD $10 for 1,000 social media ad impressions during the Q4 2022 holiday season.

On average, that would mean that each social media ad impression would cost more than 1 cent – the first time that we’d have seen global social media CPM averages break this threshold.

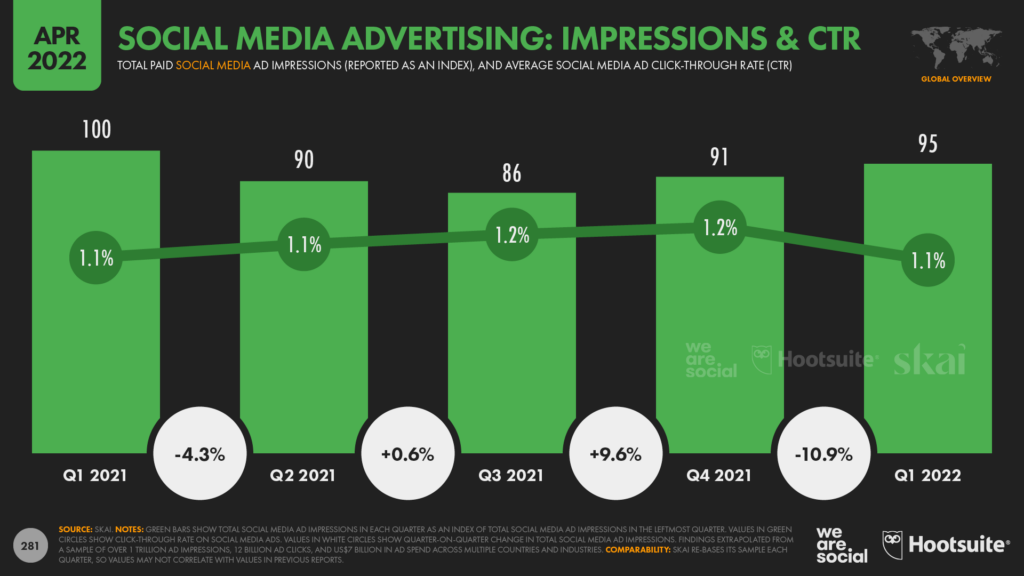

Compounding these price increases, Skai’s data also reveals that marketers should expect less bang for their advertising buck than they could have expected just a few months ago.

Despite overall social media ad spend in Q1 2022 increasing by 10 percent compared with the same period a year before, advertisers only managed to deliver 95 percent of the social media ad impressions that they delivered in Q1 2021.

Social media click-through rates (CTR) also fell sharply in the first three months of this year compared with the previous three-quarters, although Skai’s analysts caution that this may be partly due to an increased preference for video advertising.

For context, many of the marketers I’ve spoken with in recent weeks have recalibrated their social media spend to put less emphasis on “direct-response” ads, saying that performance ads have become significantly less cost-effective following the implementation of Apple’s ATT policies.

As a result, many of these marketers are now investing more heavily in video-centric “brand” advertising, which is typically less reliant on user interaction (e.g. clicking through to a website) to deliver the desired outcome.

Digital’s role in B2B communications

We’ve included a special section on digital’s evolving role in the workplace in this quarter’s report, using excellent data from GWI’s Work survey.

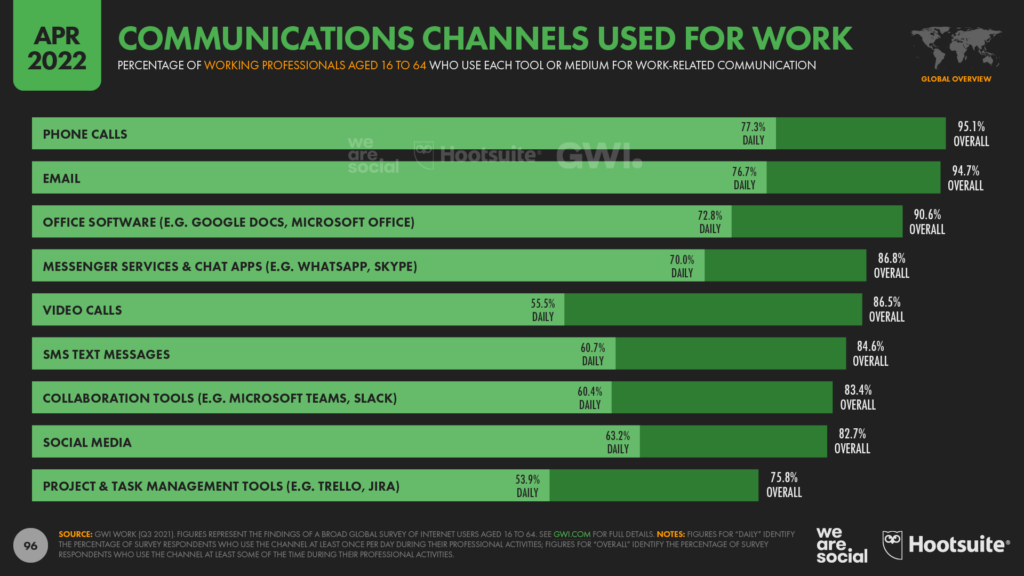

And perhaps the most important takeaway from this latest update to the company’s B2B dataset is that professionals still prefer to use a wide variety of communications channels for their work activities.

Despite the rise of video calling and messaging platforms, voice calls still top the ranking of devices and platforms used for work-related comms.

More than 95 percent of working professionals between the ages of 16 and 64 say they engage in phone calls at work at least occasionally, while 77 percent say that they do so every day.

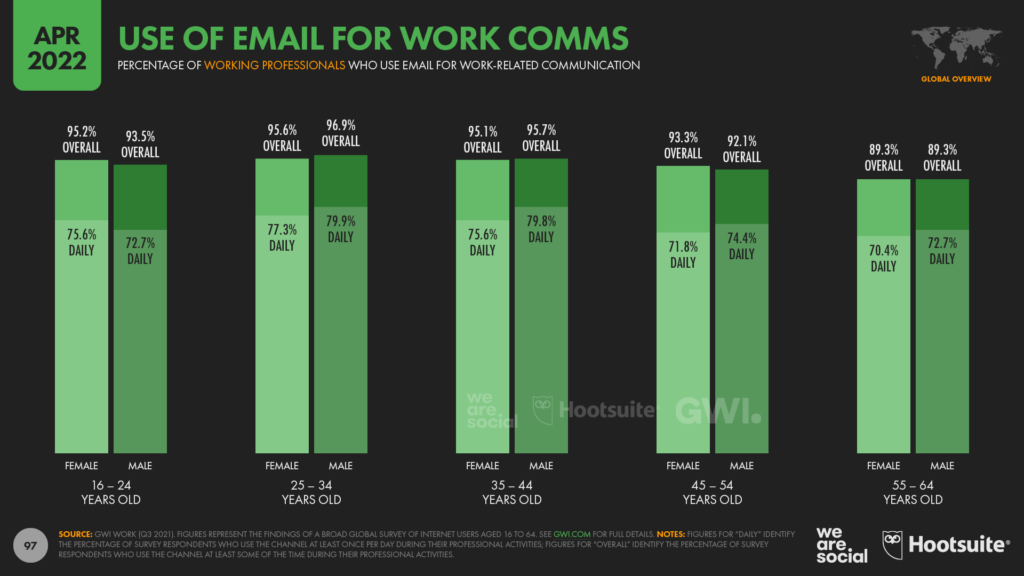

Email has also shown remarkable resilience, with almost 95 percent of survey respondents confirming that email continues to be a regular part of their working life.

Reading and writing emails remain some of our most frequent activities at work too, with 76.7 percent of working professionals saying that they use email at least once per day.

And – perhaps surprisingly – younger people are actually more likely to use email for work than their older colleagues are.

Indeed, younger millennials between the ages of 25 and 34 are the biggest users of email at work.

More than 96 percent of this cohort say that they use email at least some of the time, while nearly 4 in 5 say that they use email every day.

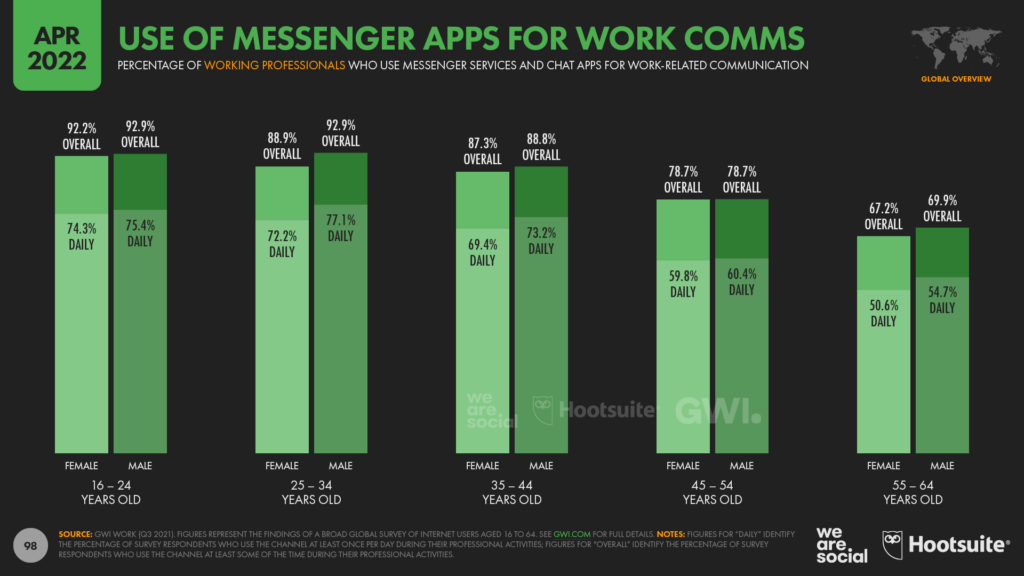

Messenger services like WhatsApp have now overtaken text messages as a preferred means of communication at work, with almost 87 percent of respondents using these platforms at least some of the time, and 7 in 10 saying that they use them every day.

Working professionals in Gen Z are the most likely to use chat apps for work, with more than 92 percent of this demographic using them at least some of the time, and almost three-quarters using them on a daily basis.

Colleagues in the Baby Boomer generation have been slower to adopt these platforms compared to younger age groups, but nonetheless, more than two-thirds of working professionals aged 55 to 64 say that they use messengers for work-related comms.

Perhaps unsurprisingly given the “Zoom effect”, the role of video calls has jumped significantly since the start of the COVID-19 pandemic.

GWI’s data shows that 71.7 percent of working professionals engaged in video calls towards the end of 2019, but just two years later, that figure had jumped to 86.5 percent – a relative increase of more than 20 percent.

Social media at work

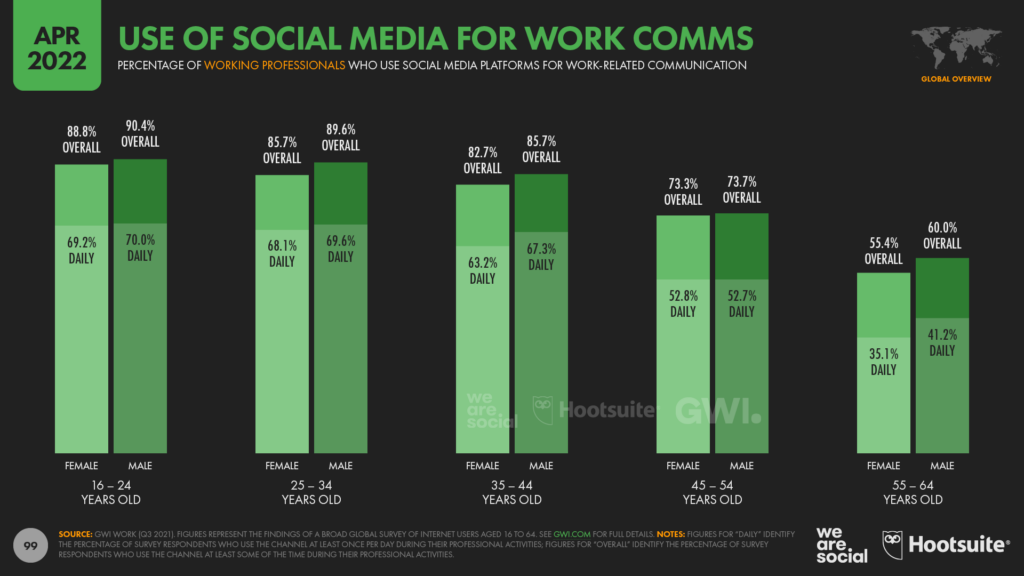

Meanwhile, more than 4 in 5 working professionals now use social media for work-related communications.

Social media platforms also rank relatively highly for frequency of use, with nearly two-thirds (63.2 percent) of professionals between the ages of 16 and 64 saying that they use social media for daily work communication.

Perhaps unsurprisingly, younger generations are much more likely to use social media for professional communications.

Roughly 9 in 10 professionals in the Gen Z demographic say that they use social media for work conversations, with roughly 7 in 10 saying that they do so every day.

However, fewer than 6 in 10 Baby Boomers use social media for any kind of work communication, and fewer than 4 in 10 use social platforms for work comms on any given day.

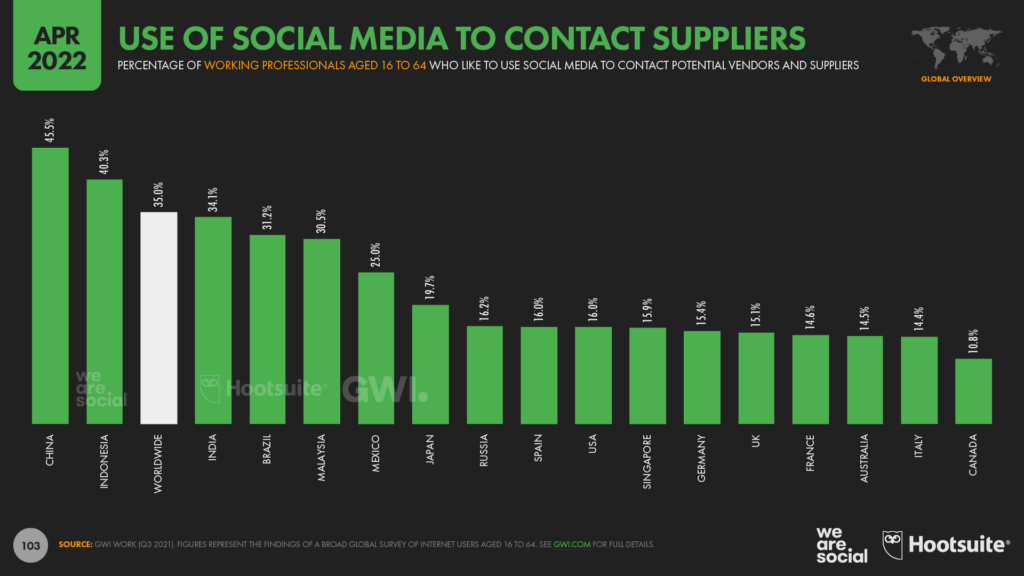

The use of social media for workplace communication also varies significantly by geography.

For example, GWI’s data reveals that – at a worldwide level – roughly 1 in 3 working professionals now uses social media to communicate with external suppliers and vendors.

However, this figure rises to more than 45 percent in China, and more than 40 percent in Indonesia.

At the other end of the spectrum, fewer than 1 in 9 Canadian professionals uses social media to communicate with external partners, and these figures reach a maximum of 1 in 6 across Europe.

The B2B buyer journey

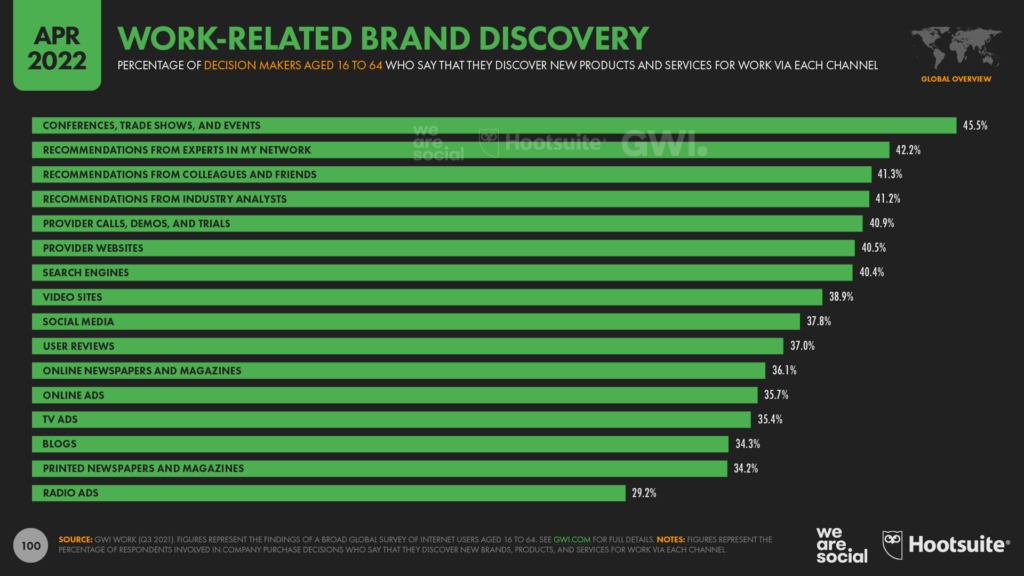

Events and word-of-mouth remain the primary ways in which B2B buyers discover new products and services, but GWI’s data reveals that working professionals rely on a wide variety of channels to learn about new offerings that might be relevant to their work.

The data also reveals that brand and product websites remain a critical channel for B2B marketing, with more than 4 in 10 B2B decision makers saying that they discover new brands and products through such sites.

Meanwhile, almost 38 percent of B2B decision makers say that they discover new products and services relevant to their work via social media channels.

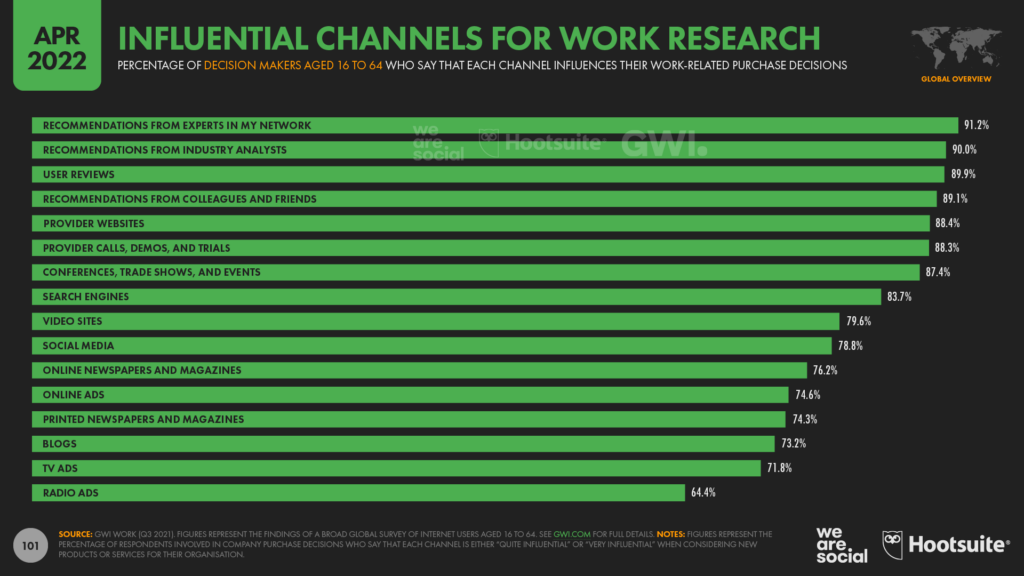

Conversations with experts, colleagues, and peers remain the primary sources of information when B2B buyers are researching purchases, with roughly 9 in 10 corporate decision-makers citing these channels as influential in their work-related research.

However, 88 percent of decision-makers also cited suppliers’ websites as being influential in their evaluation of potential partners, putting this channel ahead of demos, trials, and even trade shows when it comes to B2B product research.

Roughly 8 in 10 B2B decision-makers also say that social media plays an influential role in their research, putting social media ahead of trade press outlets like online and offline magazines in terms of influence in the B2B buyer journey.

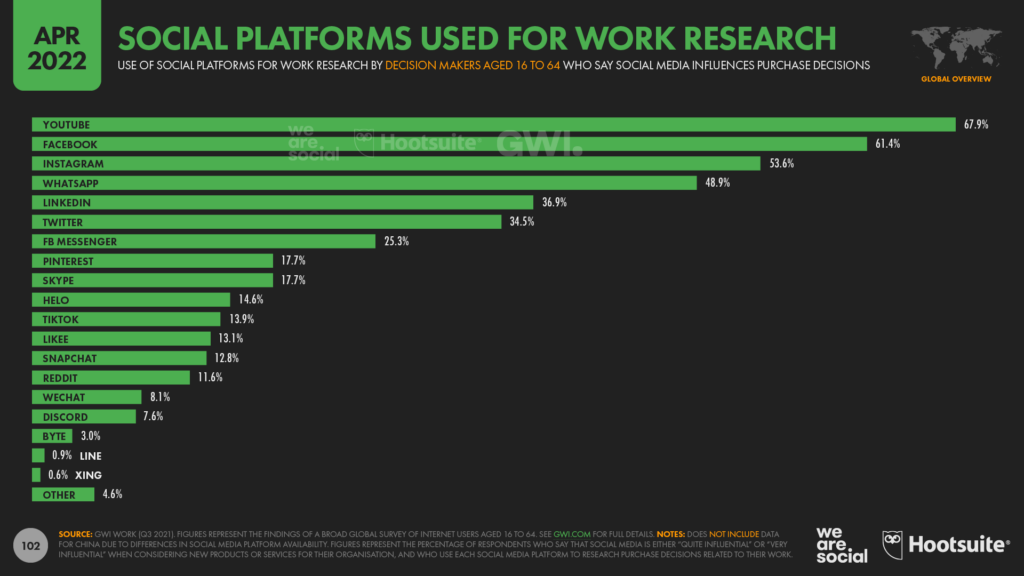

When it comes to researching potential suppliers on social media, B2B purchasers are most likely to turn to YouTube.

More than two-thirds (67.9 percent) of decision-makers who use social media platforms when researching potential partners cited the video platform as part of their research journey.

Somewhat surprisingly though, these same decision-makers said they were more likely to use Facebook (61.4 percent), Instagram (53.6 percent), and WhatsApp (48.9 percent) than they were to use LinkedIn (36.9 percent) when researching potential B2B suppliers and partners.

Meanwhile, despite its reputation as being a place for entertainment and memes, TikTok has already earned a place in the B2B world too, with 13.9 percent of decision-makers who use social media as part of their purchase journey saying that they visit the platform when researching potential vendors.

It’s worth noting that channel preferences and platforms’ relative influence vary meaningfully by geography and demographic though, so be sure to dig into GWI’s full Work dataset if you’d like to know more about how these latest trends will impact your company’s success.

Quick stats

Just before we wrap up this quarter’s analysis, here are a few “random” stats we identified in the latest numbers:

Online shoppers visiting ecommerce websites via a laptop or desktop computer are twice as likely to convert as shoppers visiting via a mobile phone. (Source: Contentsquare’s 2022 Digital Experience Benchmark Report)

TikTok posts tagged with #FYP (“for you page”) have now delivered a combined total of more than 22.5 trillion views – an increase of more than 21 percent (4 trillion new views) in just the past three months. (Source: Kepios analysis of data published on TikTok.com)

“Wordle” was one of the 20 most-searched terms on Google around the world in the first quarter of 2022. (Source: Google Trends)

“TikTok” was one of the 10 most-searched queries on YouTube in the first three months of 2022. (Source: Google Trends)

The world’s internet users appear to be increasingly interested in the weather. Google searches for “tiempo mañana” have increased by a massive 1,850 percent (19.5x) over the past five years, while searches for “weather tomorrow” are up by 1,250 percent (13.5x) over the same period. (Source: Google Trends)

Wrapping up

Just in case you’re still hungry for numbers, you’ll find loads more stats that I haven’t been able to cover in this article in our complete Digital 2022 April Global Statshot Report, which you’ll find in the embed towards the top of this article.

And if you’re looking for more social media data, you might be interested in our individual platform reports, which we typically update a couple of weeks after we publish these Statshot reports, once the operating companies have released their quarterly earnings reports.

That’s all for this quarter’s report though – thanks for sticking with me all the way to the finish! Give me a wave on Twitter or Linkedin if you made it this far, and let me know which of this quarter’s findings stood out most for you.

I’ll be back again towards the end of July with our next Statshot report.