The digital and social landscape continues to evolve in ways we may not have expected. Here, Kepios founder Simon Kemp takes us through the updates in our latest Digital 2023 Report.

User identities now equal to more than sixty percent of the world’s population.

If you thought digital growth was starting to settle into a more predictable pattern, prepare yourself for some surprises.

Our new Digital 2023 July Global Statshot Report – published in partnership between We Are Social and Meltwater – reveals a wealth of important headlines and trends, including:

A big new milestone for social media use;

The adoption of AI technologies by everyday internet users;

The rapid growth of Threads;

Changes in how the world accesses news content;

A new top ranking for India;

The surprising truth about gaming amongst older generations;

The ongoing confusion at Twitter

That’s just a brief taster of the insights you’ll find in the full report though, which is packed with 300+ slides exploring what people are really doing on the internet, social media, mobile devices, and online shopping platforms.

And given the importance of some of the latest trends and stories, we’ve produced an “extra large” Statshot this quarter, which includes additional insights into social media use and a whole section on digital news trends.

The definitive source of digital data

In addition to thanking We Are Social and Meltwater for making these reports possible, I’d also like to offer my heartfelt thanks our wonderful data partners, without whom the Global Digital Reports series would be a lot less informative:

Before we begin this quarter’s analysis, please note that there have been some important changes to the source data that we include in the Global Digital Reports series over recent weeks:

As we highlighted last quarter, GWI revised its methodology starting with its Q4 2022 wave of research. As a result, please beware of comparing figures in this quarter’s report with data published in previous reports in this series, especially those published prior to April 2023.

We continue to see incongruous trends in the data published in the ad tools of various social media platforms. We’ll explore some of these changes in detail below, but please exercise caution when analysing trends in social media audience data.

For further details, please refer to our comprehensive guide to changes in data sources, research methodologies, and reporting approaches.

Top takeaways

If you need fast insights, I’d recommend starting with the video below, which will help you understand all of this quarter’s top headlines and trends.

Once you’ve watched that, scroll down for the full report.

The complete Digital 2023 July Global Statshot Report

You’ll find this quarter’s complete report in the embed below (click here if that’s not working for you), but read on past that to find our in-depth analysis of what all these numbers actually mean.

The state of digital in July 2023

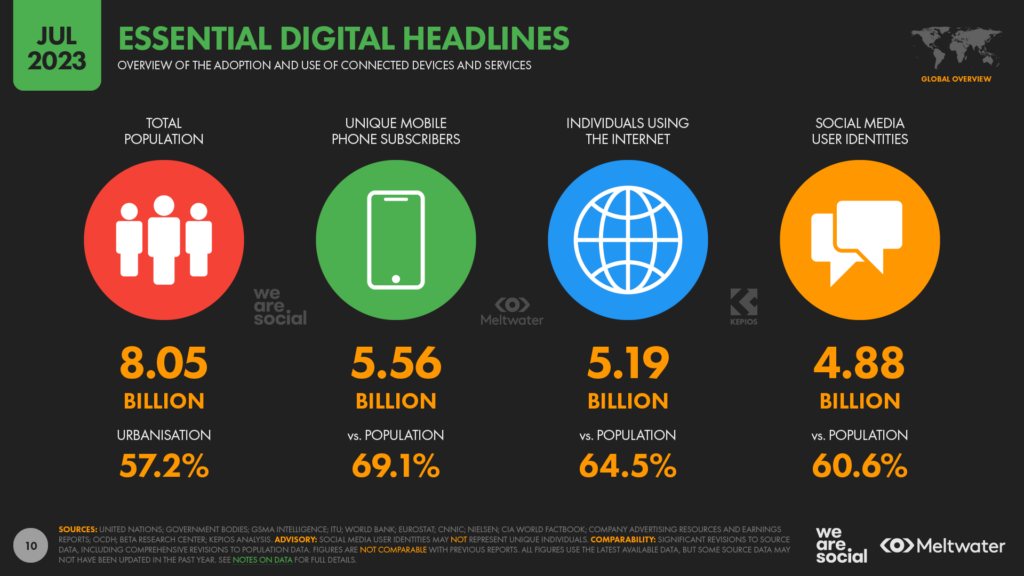

As always, let’s begin with the latest headlines for digital adoption and use around the world:

Data from the United Nations shows that the world’s population had reached 8.05 billion by the start of July 2023. That figure was just under 1 percent higher than the figure for the same time last year, with the world’s population growing by 70 million over the past 12 months.

The latest analysis from GSMA Intelligence shows that there are now 5.56 billion unique mobile subscribers around the world, equating to 69.1 percent of the global population. Mobile phone adoption increased by 2.7 percent over the past year, thanks to almost 150 million new users.

The reported number of people using the internet has grown by 2.1 percent over the past year, to reach 5.19 billion in July 2023. This figure equates to 64.5 percent of the world’s population, although delays in reporting mean that actual internet penetration is likely higher than these figures suggest.

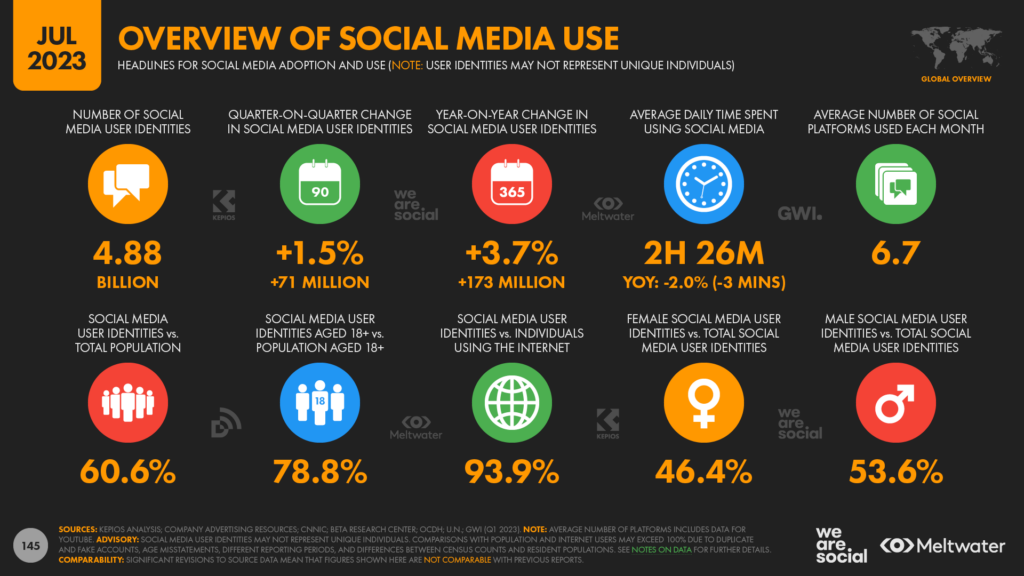

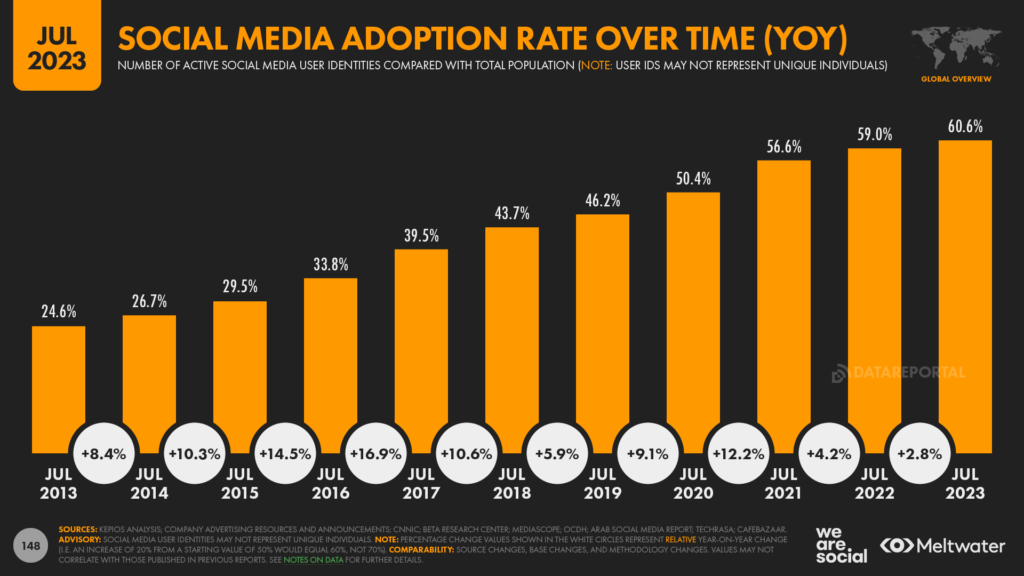

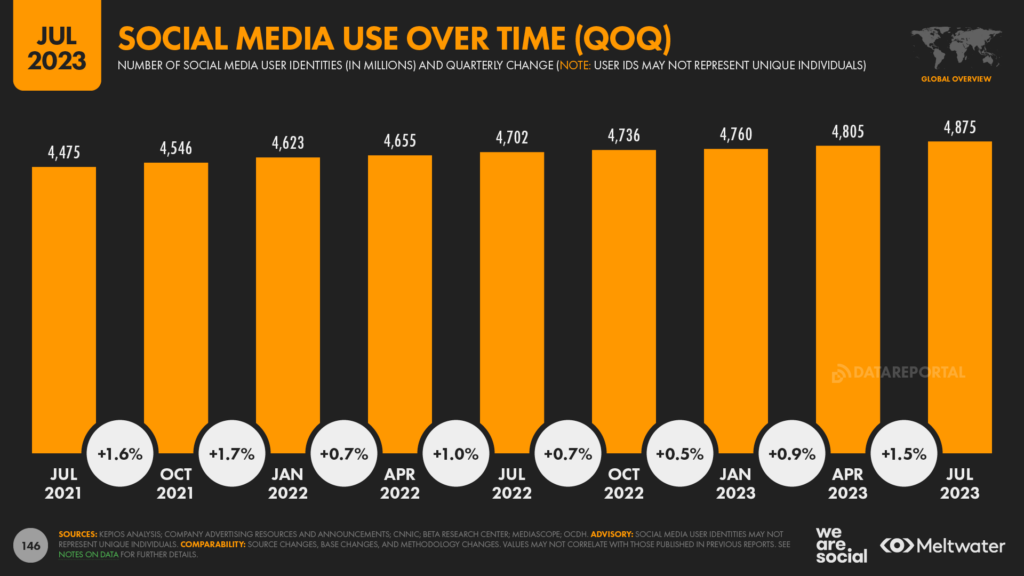

The number of active social media user identities now equates to 60.6 percent of the world’s population, with the global total reaching 4.88 billion in July 2023. Social media adoption increased by 3.7 percent since this time last year, thanks to the addition of 173 million new active identities.

That’s a handy overview of the latest global state of digital, but the real insights come when we dig deeper into the data, so let’s dive into this quarter’s numbers…

Social media users reach new milestone

Kepios analysis reveals that a total of 4.88 billion distinct user identities accessed social media platforms over the past 30 days.

This figure equates to 60.6 percent of the world’s total population, marking yet another important milestone in global social media adoption.

It’s important to stress that this 4.88 billion figure doesn’t necessarily represent unique individuals, because active user identities likely include a number of duplicate and false accounts, as well as accounts that represent “non-human” entities such as businesses, pets, music bands, and the like.

However, with messaging platforms and social networks still the primary destinations for the world’s 5.19 billion internet users, the comparison between active user identities and population still provides a reliable benchmark for social media use.

Social media’s rapid ascent

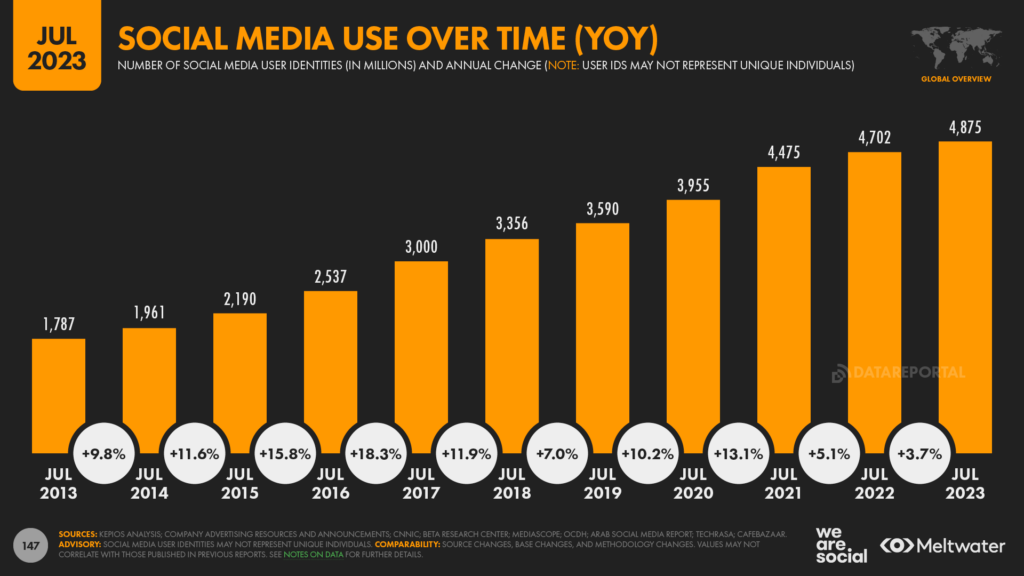

This momentous milestone in social media adoption comes just 20 years after the advent of the first “fully fledged” social networks, such as Friendster (2002), LinkedIn (2003), and Myspace (2003).

Moreover, Kepios analysis shows that the global social media adoption rate has doubled in just the past 8 years.

Just under 30 percent of the world’s population used social media in July 2015, when there were slightly more than 2.5 billion active social media user identities.

We passed the “halfway” point in July 2020, when COVID-19 lockdowns fuelled rapid increases in social media use that pushed the global adoption rate to 50.4 percent.

Current growth rates have slowed considerably compared with the double-digit increases that we saw during 2020 and 2021, but the global adoption rate has still increased by a relative 2.8 percent (+1.6 percentage points) over the past year [remember that the global population has also increased during the past year, which explains why the adoption growth rate doesn’t match the user growth rate].

Looking more closely at recent growth, it’s also worth highlighting that social media user identities have grown faster over the past three months than at any other time since the start of 2022.

The global user total has increased by 71 million identities over the past 90 days (+1.5 percent), meaning that the global figure increased by an average 777,000 users per day between April and June 2023.

And the key takeaway here is that social media growth remains strong, despite overall adoption passing that momentous 60 percent mark.

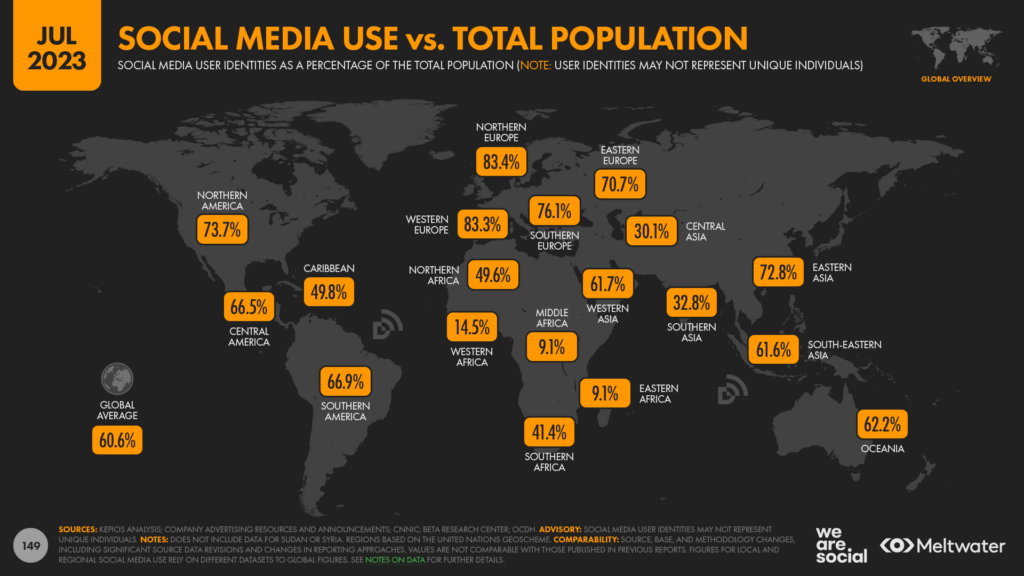

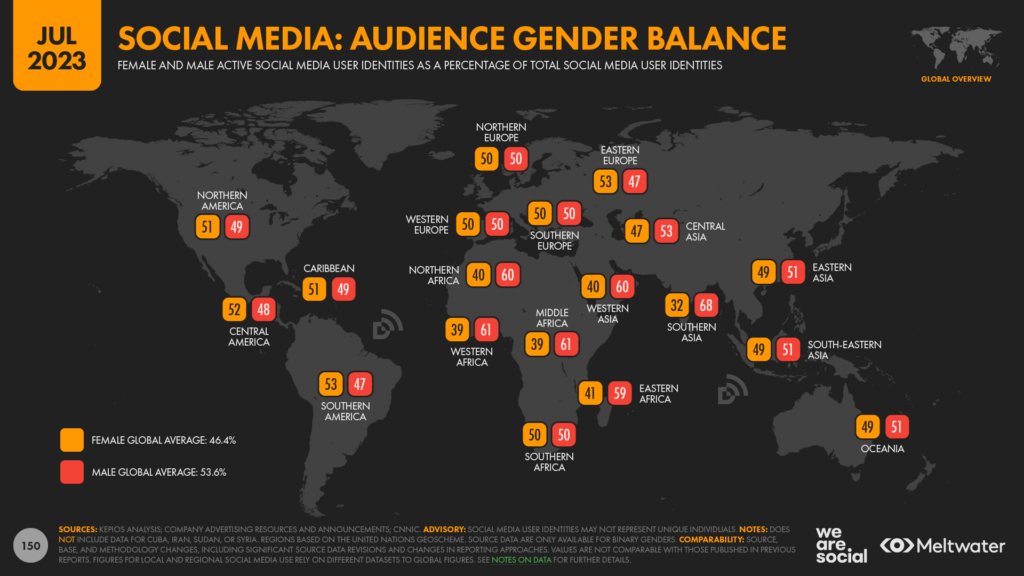

Social media use still uneven around the world

However, social media use still isn’t evenly distributed around the world.

Adoption rates are highest in Northern and Western Europe, where active social media user identities equate to more than 83 percent of regional populations.

For easier comparison, these figures suggest that roughly 5 in every 6 people living in these regions use social media today.

Meanwhile, the number of active user identities across North America points to an adoption rate that’s closing in on three-quarters of the region’s total population.

Eastern Asia isn’t far behind either, with high social media use across China, Japan, and South Korea pointing to an adoption rate in excess of 70 percent of the total regional population.

However, Eastern Asia is also home to the country with the world’s lowest levels of social media use.

The internet – at least as the rest of the world knows it – is still blocked for everyday citizens in North Korea, which means that only a tiny fraction of the country’s elite can access social media platforms.

Meanwhile, data suggests that just 1 in 11 people across Middle and Eastern Africa use social media today.

And the adoption rate is only marginally better in Western Africa, where data suggest that barely 1 in 7 people used a social platform within the past 30 days.

But lower levels of social media adoption aren’t confined to countries in Africa.

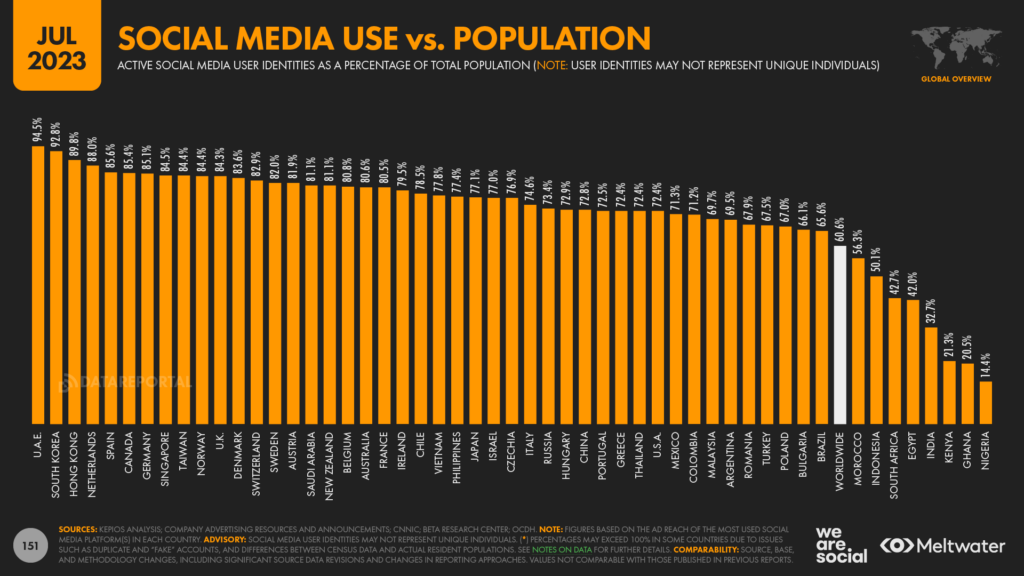

The latest data indicates that fewer than 1 in 3 people across Southern Asia use social media today, with the adoption rate in Pakistan still languishing below 30 percent.

Women still underrepresented on social media

One of the biggest impacts on social media adoption rates across Southern Asia is a stark gender “gap”, with women only half as likely as men to use social media across the region as a whole.

This digital divide is at its most extreme in Afghanistan, where men account for a massive 84 percent of the country’s social media users.

But a large gender imbalance is clearly evident in Pakistan too, where men account for close to three-quarters of all active social media accounts in July 2023.

Anecdotally, we know that some women in Southern Asia set the gender of their social media profiles to “male” in order to avoid online harassment, and this practice may have a small impact on these gender balance figures.

However, broader internet adoption figures show that many women across Southern Asia are still unable to access the internet, which is by far the greatest contributing factor to this digital gender divide.

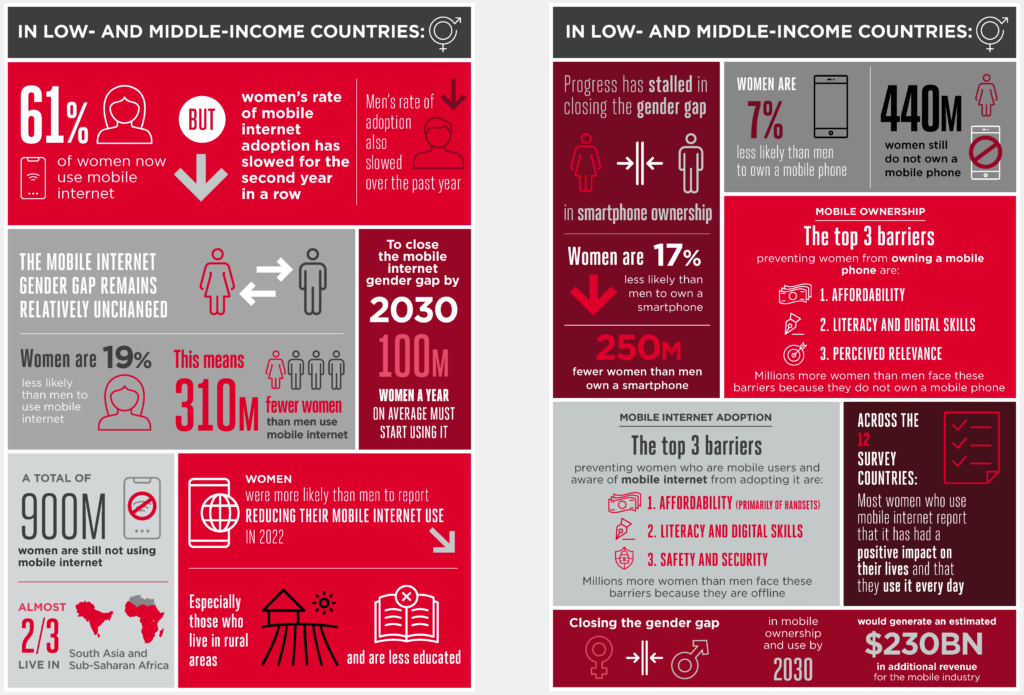

Inequality of access remains a pervasive issue

Southern Asia is home to the greatest number of women who are unable to access the internet, although the problem is not unique to the region.

A recent report from GSMA Intelligence reveals that:

“There are 900 million women in low- and middle-income countries (LMICs) who are still not using mobile internet, almost two-thirds of whom live in South Asia and Sub-Saharan Africa.”

The report’s authors go on to state that – globally – women are 19 percent less likely than men to use mobile internet, but given that mobile access dominates internet use across LMICs, this figure is likely highly representative of the gender gap in overall internet use too.

What’s more, GSMA Intelligence reports that the internet adoption rate amongst women has actually slowed for the second year in a row, although adoption rates for men have also slowed over the past 12 months.

As a result, the report’s authors state that 100 million women per year will need to start using the internet between now and 2030 if we’re to close the digital gender gap in time to reach the UN’s Sustainable Development Goals (SGDs).

But that sounds increasingly challenging, especially when we consider that 100 million new female users per year represents an increase of roughly 65 percent compared with current levels.

GSMA cites the primary barriers to internet adoption as:

Affordability, especially in terms of mobile handsets

Literacy and digital skills

Safety and security

However, the stark gender divide in the adoption of technologies like social media also suggests that many women in Southern Asia and Sub-Saharan Africa face patriarchal resistance when it comes to accessing the internet.

But as GSMA Inteligence’s Mobile Gender Gap Report 2023 illustrates, such misogyny results in everyone suffering, not just women:

“Addressing the mobile gender gap provides significant benefits. Mobile and mobile internet can be life changing, providing access to critical information, services and opportunities from anywhere, including those related to health care, education, financial services and income generation.”

Restricting women’s digital access also perpetuates the very economic challenges that define “lower- and middle-income” countries:

“GSMA research has found that closing the gender gap in mobile internet use in LMICs could deliver an additional $700 billion in GDP growth over five years. In 2020 alone, the Alliance for Affordable Internet (A4AI) estimated that the gender gap in internet use resulted in 32 LMICs missing out on $126 billion in GDP.”

GSMA Intelligence’s complete Mobile Gender Gap Report 2023 makes for essential – if somewhat sobering – reading, so I’d strongly recommend downloading the full study.

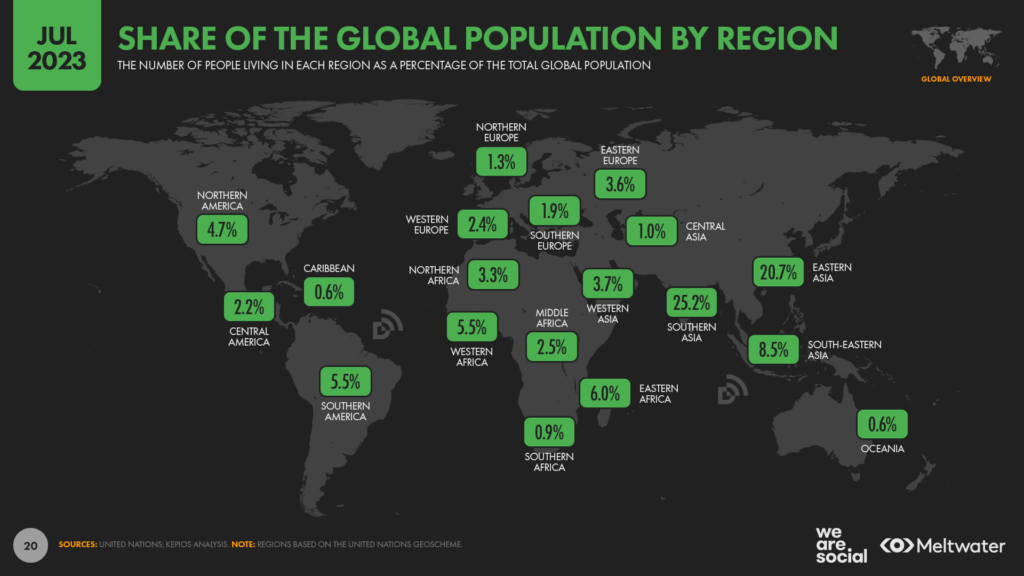

India tops global population ranks

Data from the United Nations shows that India has now “officially” overtaken China to become the world’s most populous nation.

The UN’s World Populations Prospects dataset shows that India is now home to almost 3 million more people than China, with the “switch-over” at the top of the rankings occurring sometime in the middle of April 2023.

Moreover, India’s population is currently growing at an annual rate of just over 0.8 percent, while China’s population is actually shrinking at a rate of 0.02 percent per year.

Together, these two nations account for more than 35 percent of the world’s total population in July 2023, meaning that more than 1 in 3 people on Earth call one of these two countries home.

And no other country comes close to matching their size, either.The United States ranks third in absolute population terms, but the country only accounts for 4.23 percent of the global total, and America’s population is still four times smaller than the population of either India or China.

Meanwhile, India’s Southern Asian neighbours have also seen meaningful increases in population figures over recent months.

Bangladesh’s population has grown by more than 1 percent over the past year, while Pakistan’s population grew at well over double the global average, with close to 2 percent year-on-year growth.

As a result, Southern Asia is now home to more than a quarter of the world’s total population, with three countries across the region – India, Pakistan, and Bangladesh – ranking amongst the world’s 10 most populous nations.

Special focus: digital news

The Reuters Institute for the Study of Journalism (RISJ) has just published its excellent annual study of global digital news behaviours, and – as always – the findings of its 2023 report offer just as many important insights for marketers as they do for journalists and publishers.

Top takeaways

One of the central themes in this year’s report is that generations that have grown up with digital technologies have fundamentally different behaviours compared with older generations who grew up in “less digital” times.

Critically, the ways in which today’s younger generations learn about the world – whether that’s accessing and consuming news content, discovering and learning about brands, or any other facet of learning – are fundamentally different to those of their parents’ generation.

And what’s more, these changes driving these differences are accelerating.

To paraphrase a key sentence in Rasmus Klein’s foreword to this year’s RISJ report, organisations no longer need to contend solely with digital transformation, but also with a continual transformation of digital.

For example, the exponential rise of TikTok in recent years has already had a profound impact on news consumption amongst people in their teens and early twenties, but – as we’ll explore in more detail below – most news brands are yet to achieve any meaningful results on the short video platform.

Moreover, as Klein goes on to stress in his foreword, these changes are almost certainly unidirectional:

“[W]e have every reason to expect this to be a one-way change: people’s information needs and interests evolve in the course of their life, but their platform preferences rarely regress. Those born in the 1980s did not suddenly come to prefer landline phones over mobiles when they became parents or bought a house, nor did those born in the 1960s return to black-and-white television when they entered middle age. There are no reasonable grounds for expecting that those born in the 2000s will suddenly come to prefer old-fashioned websites, let alone broadcast and print, simply because they grow older.”

In other words, the underlying trends that we see in media consumption are not temporary shifts in behaviour due to COVID-19 lockdowns, or transitory fads in technology.

Indeed, our analysis of data from various reputable sources including the RISJ and GWI suggests that the world’s media consumption behaviours really have changed forever.

And as a result, organisations everywhere – regardless of the industries or categories in which they operate – need to make sense of these changes if they’re to remain relevant.

However, it’s also important to stress that brands do not need to jump on every bandwagon, nor do they need to be present on all platforms, all the time.

Instead, our task as marketers, journalists, and educators is to identify where people go to find information, and understand how they choose to consume that information, in order to deliver the most relevant and accessible value.

So what does the latest data tell us about these evolving behaviours?

General interest in news

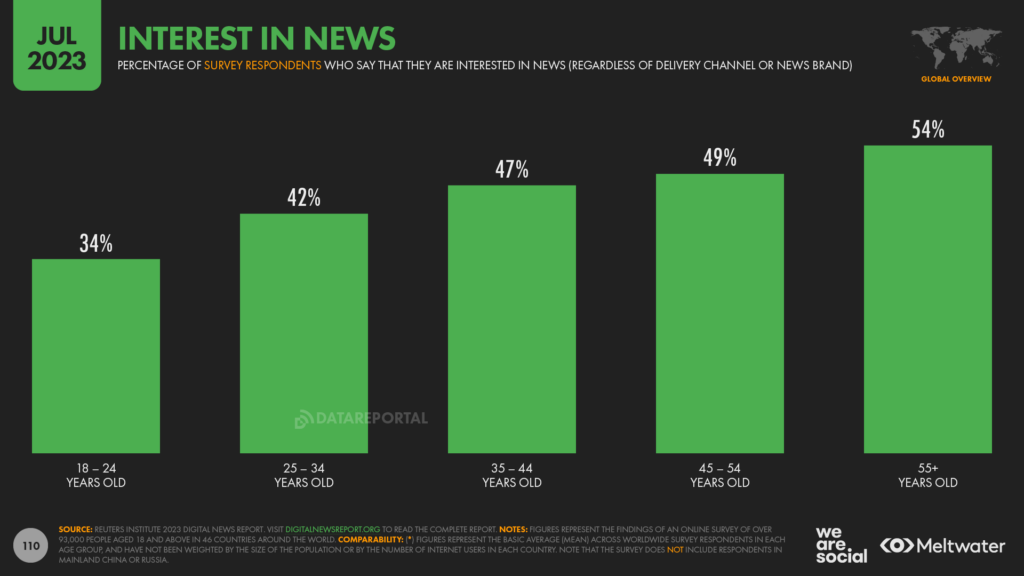

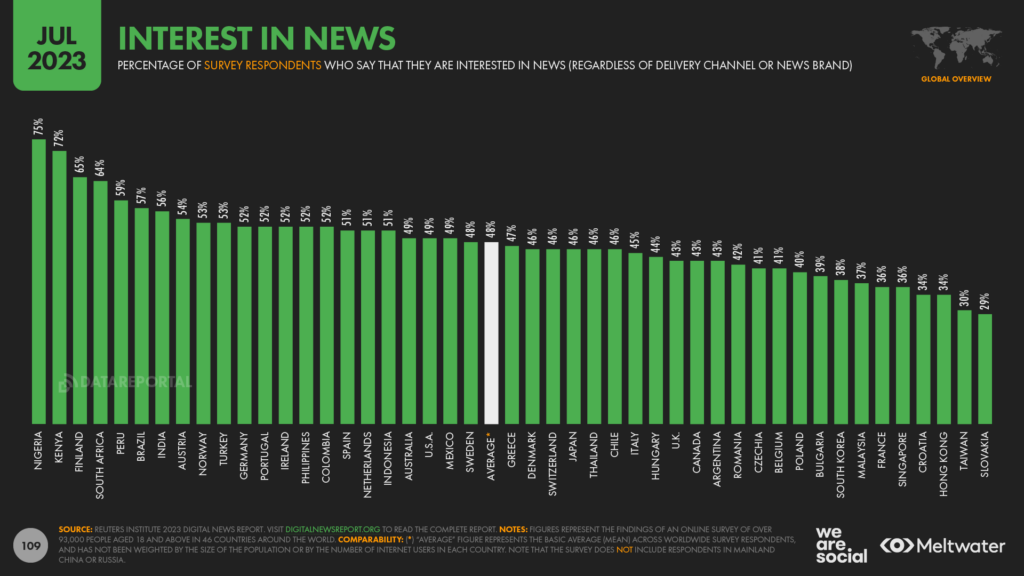

One of the most profound findings in this year’s Digital News Report is the stark differences between age groups when it comes to interest in news.

The RISJ’s 2023 study reveals that barely 1 in 3 people aged 18 to 24 are interested in news today – regardless of delivery channel or news brand – compared with more than half of adults aged 55 and above.

But interest in news also varies significantly by geography.

This year’s study found that three-quarters of online adults in Nigeria are interested in news, compared with less than 1 in 3 online adults in Slovakia and Taiwan.However, perhaps the most striking finding here is that less than half of all online adults are interested in news.

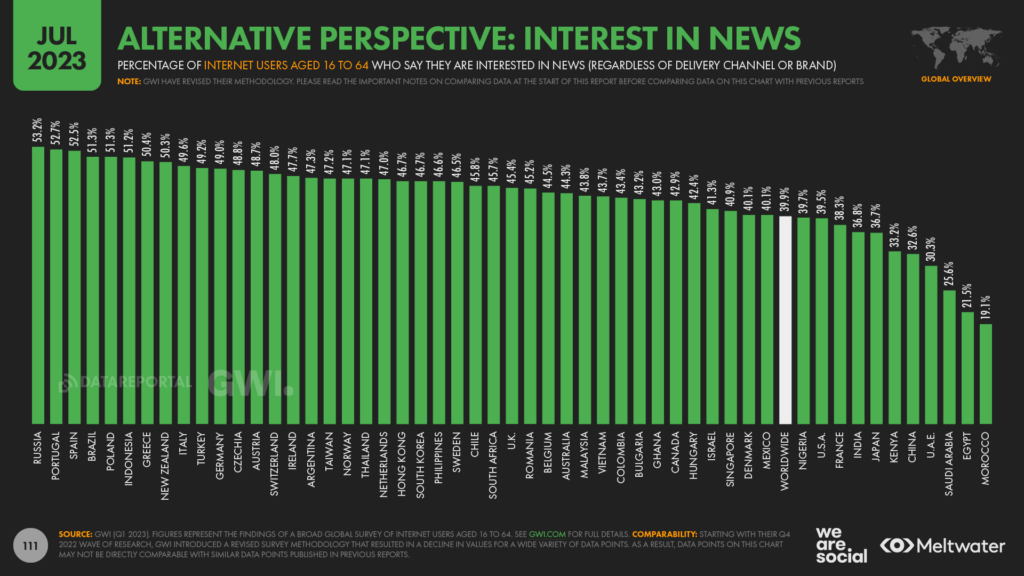

And these trends are evident in other research too.

GWI reports that fewer than 4 in 10 working-age internet users are interested in news and current affairs, regardless of the medium or channel of delivery.

The geo-specific values in GWI’s survey differ from those we see in the RISJ’s data, but both studies reveal important differences across countries and cultures.

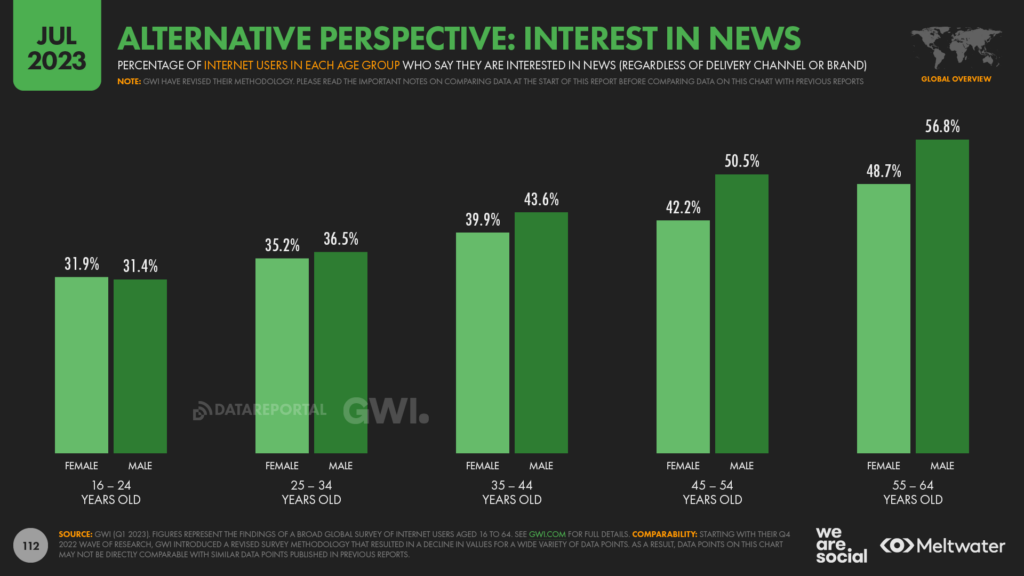

However, the trends by age in both studies tell a similar story.

Similar to the values that we saw in the RISJ’s data, GWI also reports that just 1 in 3 internet users aged 16 to 24 are interested in news content, whereas that figure climbs above 50 percent amongst internet users aged 55 to 64.

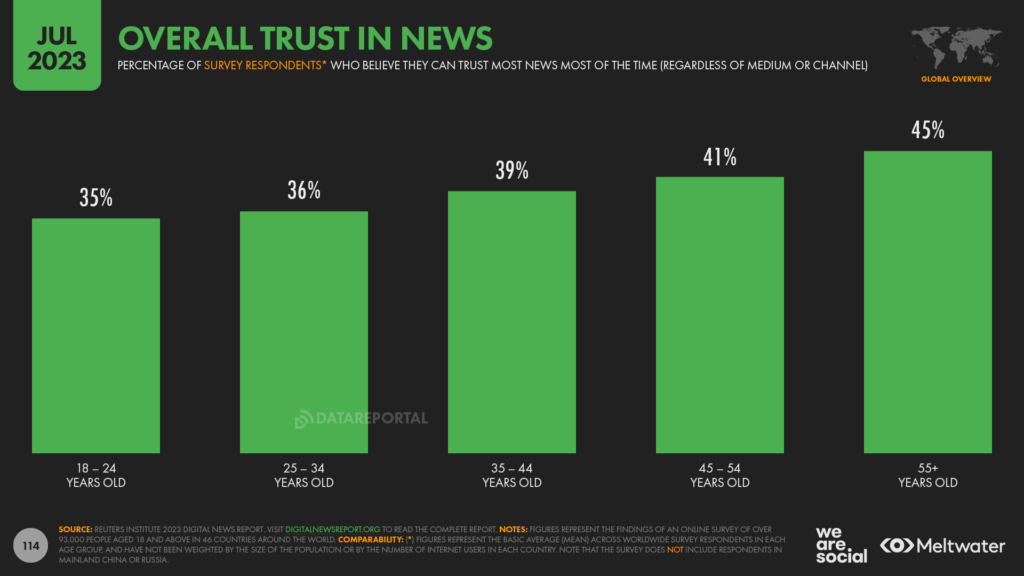

Trust in news

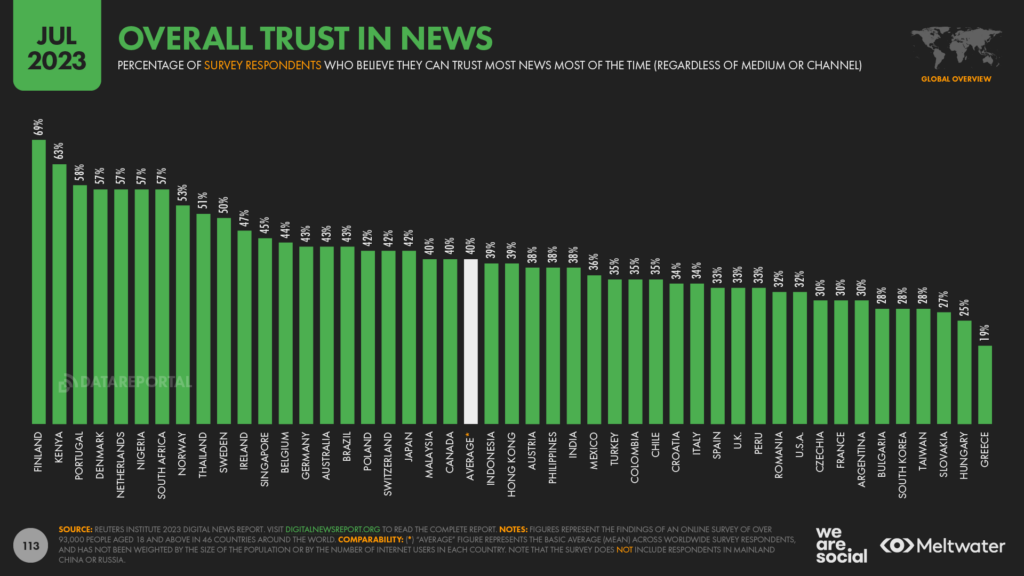

Another of the worrying trends in the 2023 edition of the RISJ’s Digital News Report is a widespread lack of trust in news media.

At a worldwide level (excluding China and Russia), just 4 in 10 respondents to the RISJ survey said that they trust news content overall.

Once again though, the data show marked differences by geography, from a high of 69 percent in Finland, to a dire low of just 19 percent in Greece.

Interestingly, trust in news tends to increase with age, although the data doesn’t make it clear whether this is a direct consequence of the channels through which each age group tends to consume news.

However, the fact that barely 1 in 3 internet users aged 18 to 24 trusts the news should be of grave concern to us all.

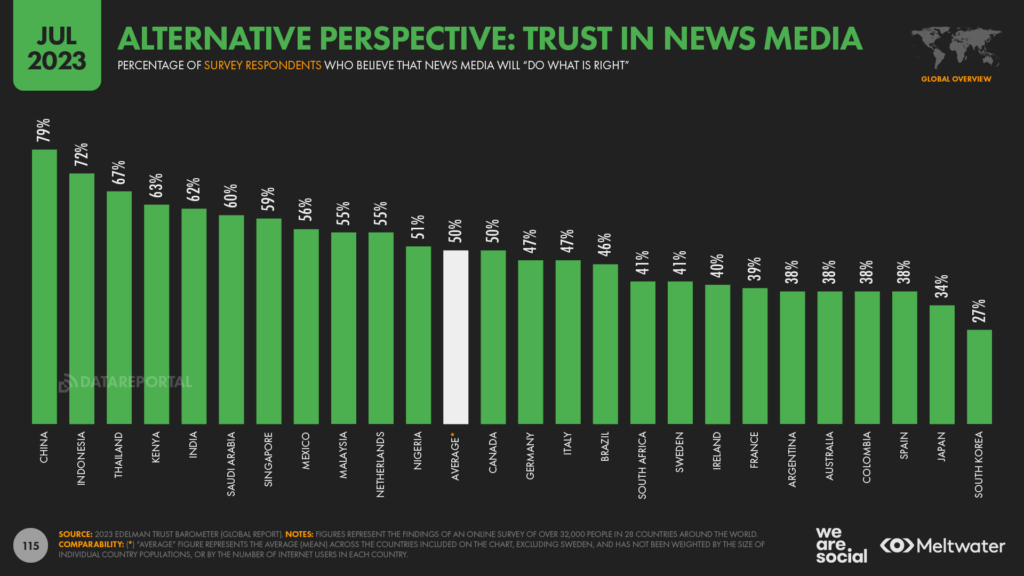

More broadly, overall levels of trust in news have declined again this year, with the global average down by two percentage points compared with the findings of the 2022 Digital News report.And this pattern echoes trends in the 2023 edition of Edelman’s Trust Barometer, which also shows a two percentage point decline in trust in the media at a worldwide level.

Impact beyond news

While these findings have clear ramifications for the news industry, the associated trends have profound implications for brands beyond the news category too.

In particular, a general disinterest in news – coupled with a distinct lack of trust in news content – may mean that “factual” marketing claims no longer deliver the assurance that marketers might hope.

Edelman’s 2023 Trust Barometer report does show that global audiences tend to trust businesses more than they trust news media, with 62 percent of survey respondents saying that they trust businesses will “do the right thing”, compared with just 50 percent for news media.

However, marketers should factor the overall decline in trust when defining their brand messaging.

And this is especially important in the context of marketing claims made in social media, where trust tends to be lower than trust in media such as television.

Channels used for news

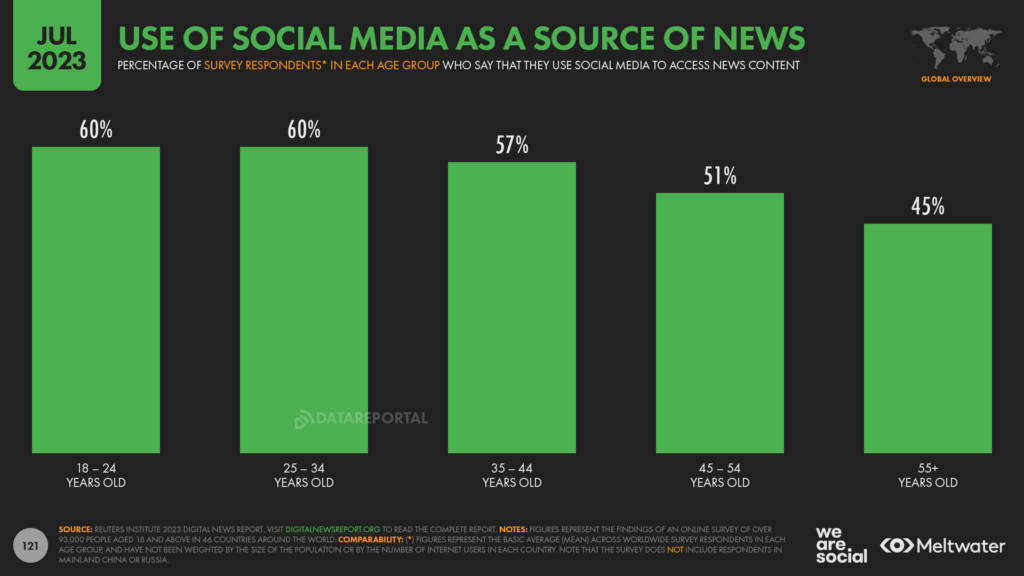

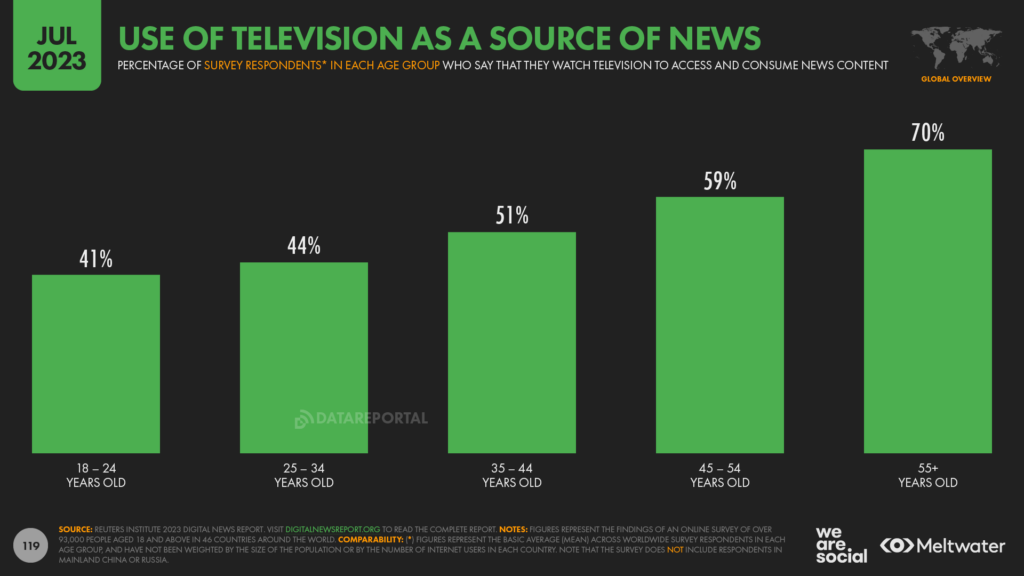

Around the world, roughly 4 in 5 internet users aged 18 and above say that they turn to online channels to access and consume news content.

Social media is increasingly a primary destination for news content too, with online adults of all ages only slightly less likely to turn to social media than they are to watch television when consuming news content.

However, preferences and trends within specific age groups tell a more interesting story.

For example, the RISJ reports that 6 in 10 internet users between the ages of 18 and 24 use social media to access and consume news-related content, compared with 45 percent of internet users aged 55 and above.

Conversely, just 41 percent of internet users aged 18 to 24 told the RISJ that they turn to television to access and consume news content, compared with 7 in 10 internet users aged 55 and above.

And it’s that high figure amongst older users that skews TV’s apparent role in overall news consumption.

Indeed, the RISJ’s data shows that less than half (48 percent) of internet users below the age of 55 use TV as a source of news, compared with 57 percent who use social media.To reiterate, that means people below the age of 55 are more likely to get their news from social media than they are to get it from television.

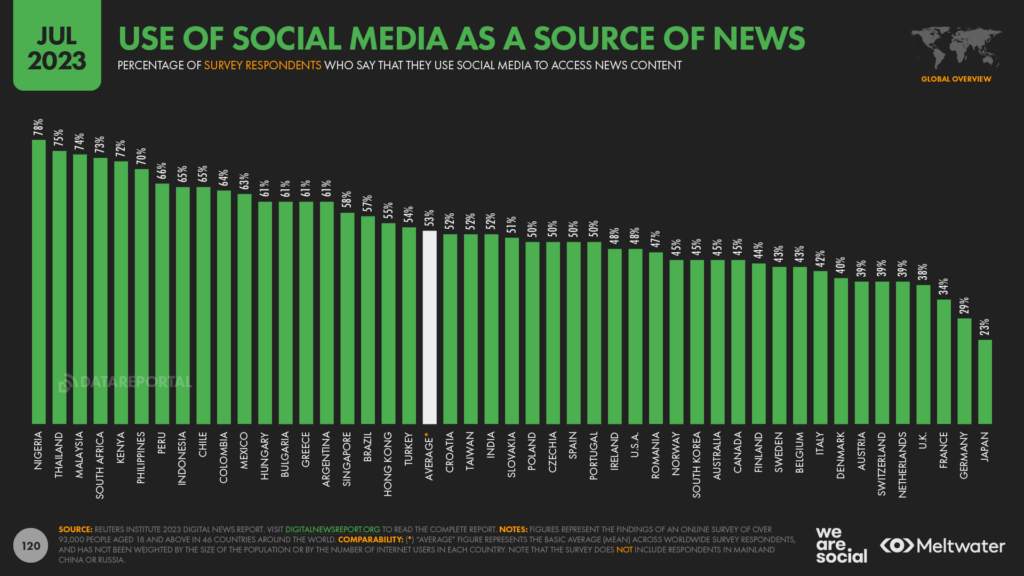

Social media’s role in news

Across the full survey sample, an average of 53 percent of RISJ respondents say that they use social media to access and consume news content.

However, this varies markedly between countries, from a low of just 23 percent in Japan, to a high of 78 percent in Nigeria.

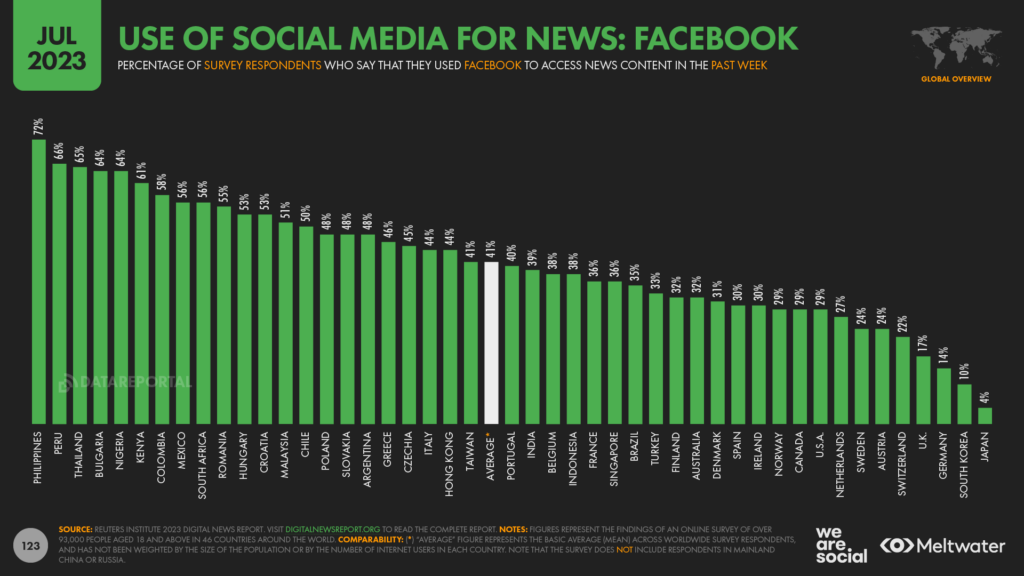

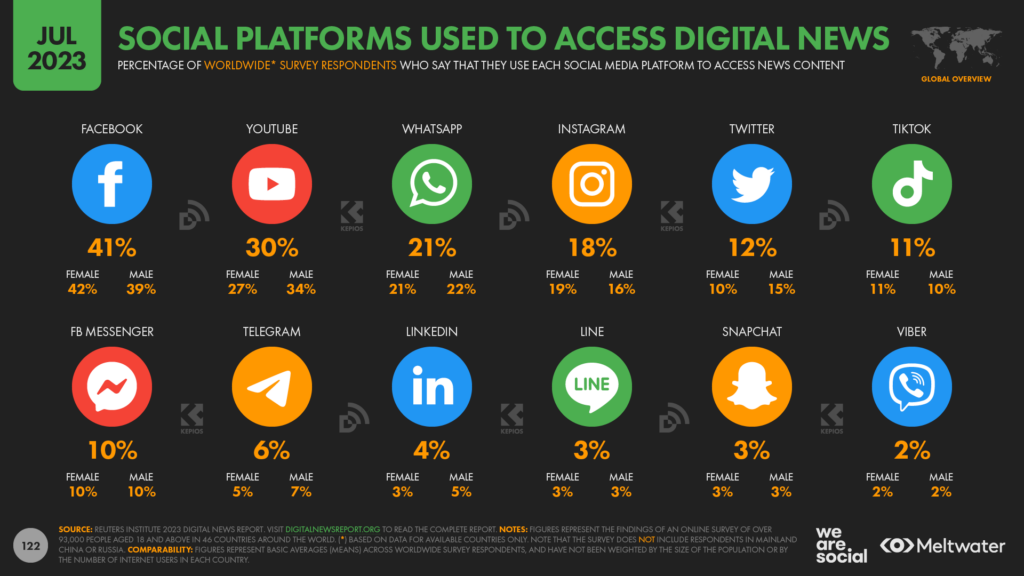

News on Facebook

In terms of the specific platforms that people use for news, Facebook still comes out as the primary social channel for news at a worldwide level.

More than 4 in 10 worldwide respondents say that they consumed some form of news content on Facebook within the past week, which is more than twice the number that said they get news from physical print media such as newspapers and magazines.

However, Facebook’s role in news content varies significantly around the world.

Nearly three-quarters (72 percent) of respondents in the Philippines say they consumed news content on Facebook in the past seven days, compared with just 4 percent in Japan.

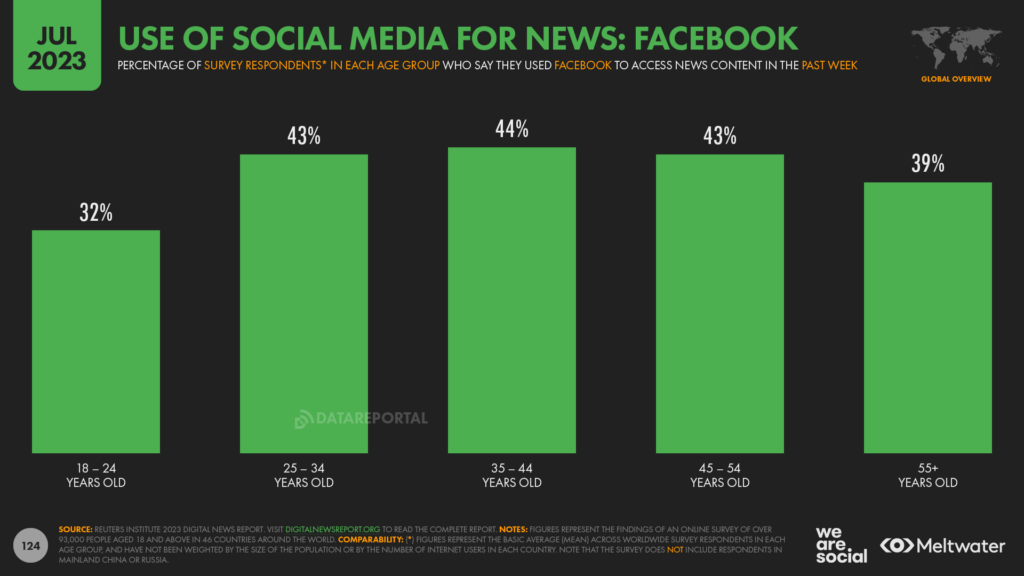

And Facebook’s role also varies by age.

Somewhat surprisingly, 32 percent of respondents aged 18 to 24 say that they consumed news content on Facebook in the past week – a figure which is 1.6 times higher than the equivalent figure for TikTok.

Indeed, despite endless media clickbait proclaiming the “death” of Facebook use amongst young people, the fact remains that the platform is still the primary source of social media news for audiences aged 18 to 24 [side note: when media headlines are so clearly misaligned with everyday reality, it’s perhaps unsurprising that so few young people trust the media].

But Facebook is even more popular amongst older audiences, and it’s interesting to note that people over the age of 55 are actually more likely to use Facebook for news than people aged 18 to 24 are.

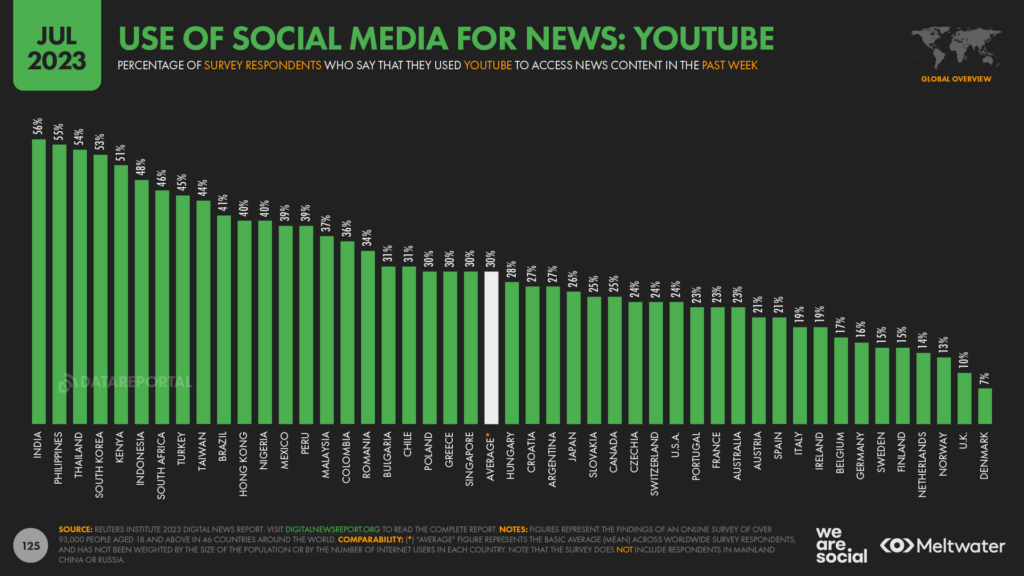

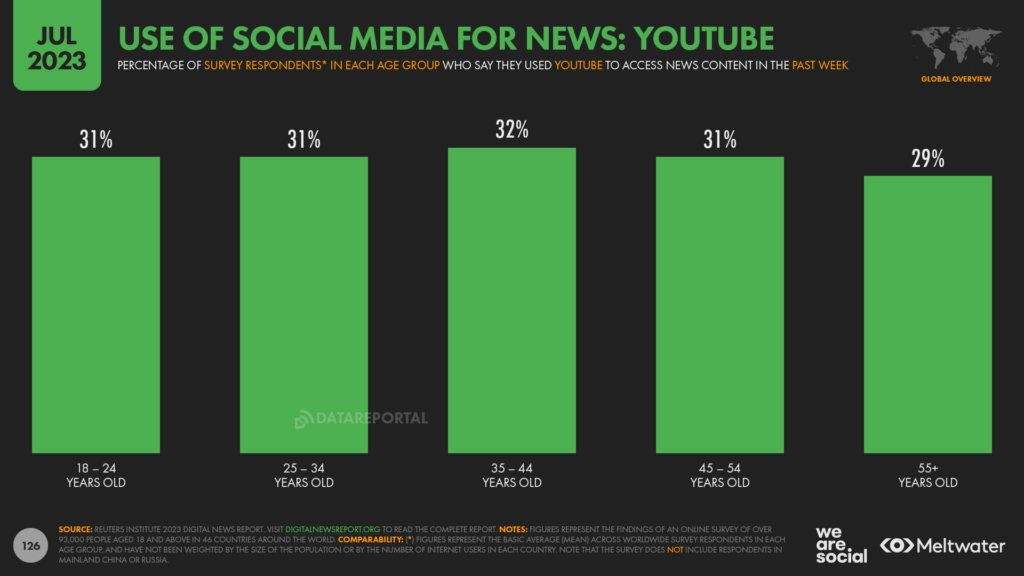

News on YouTube

YouTube ranks second amongst the social channels used for news, with 3 in 10 respondents watching news content on the video platform in the past seven days.

People in India are the most likely to turn to YouTube for news, with 56 percent of respondents in the country telling the RISJ survey that they had done so within the past week.

YouTube is considerably less popular for news in the UK though, where just 1 in 14 respondents (7 percent) said that they watched news content on the platform in the past seven days.

The data for YouTube use by age offers some more interesting insights however, in the sense that YouTube’s popularity as a news source is relatively consistent across all adult audiences.

People aged 55 and above are slightly less likely to turn to YouTube to watch news content, but there’s only a 3 percentage point difference between YouTube use in this age group versus the top age group (people aged 35 to 44).

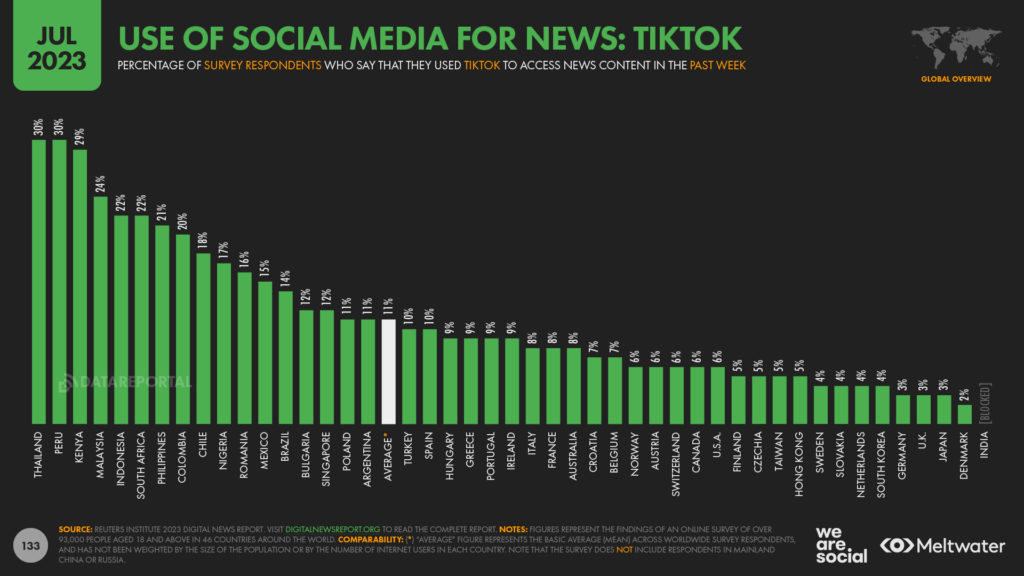

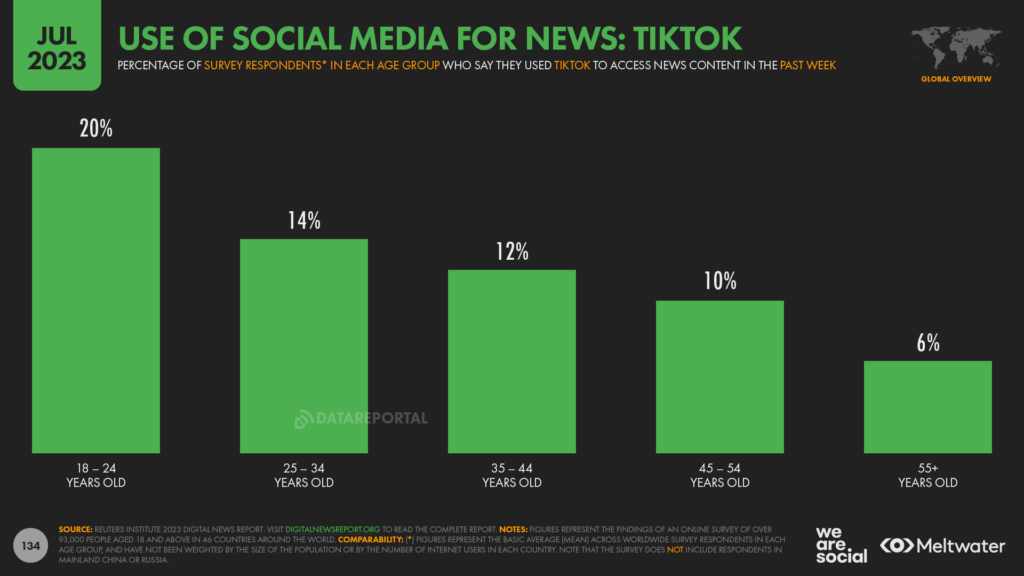

News on TikTok

Looking more broadly, RISJ data shows that people turn to a broad range of social media platforms to access and consume news content.

And the rise of TikTok is particularly interesting in this regard, with roughly 1 in 9 respondents to this year’s Digital News survey telling the RISJ that they use the platform for news.

TikTok’s 11 percent is still behind Twitter (12 percent) and Instagram (18 percent), but the number of respondents who say that they use TikTok for news jumped by almost 60 percent this year, compared with the RISJ’s 2022 findings.

Once again though, TikTok’s role in delivering news content varies significantly around the world, from a high of 30 percent in Thailand, to a low of 2 percent in Denmark.

And as you might expect, TikTok’s role also varies considerably by age, with people aged 18 to 24 more than three times as likely as people aged 55 and above to turn to the short video platform for news.

However, as we’ll see in the next section, the fact that 1 in 5 people aged 18 to 24 now get news from TikTok has some particularly important consequences.

Top digital news brands

But in order to understand changing news behaviours, it’s also important to explore the specific sources – i.e. news “brands” – that command the greatest share of attention by medium and channel.

Top news brands on the web

For example, if we look at news brands on the web, it’s fascinating to see that Yahoo! still tops the global rankings.

The latest data from Similarweb suggests that yahoo.com still attracts more than 400 million unique visitors each month, with each of those visitors making an average of 8 visits to the site each month.

It’s important to note that yahoo.com is a “portal” though, and while news features prominently on the site’s homepage, news isn’t the only reason why people visit the platform.

Indeed, news.yahoo.com – the platform’s dedicated news service – ranks just 20th in the latest data, with roughly 60 million unique visitors each month.

QQ and MSN are also portals, and these sites take second and third spots (respectively) in the latest rankings.

The website of the UK’s public broadcaster, the BBC, ranks fourth in Simialrweb’s latest data, whilst Indian news channel Aaj Tak ranks fifth.

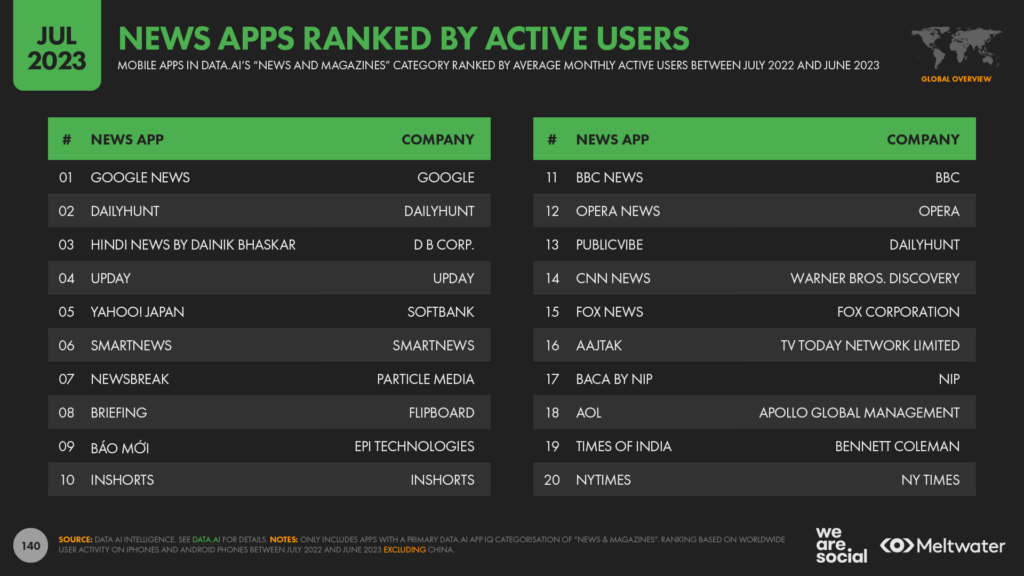

Top news apps

When it comes to the mobile apps people turn to in order to get news, Google News tops the latest rankings in data.ai’s “News & Magazines” App IQ category.

DailyHunt, an Indian news aggregator, ranks second, while another Indian news app – Hindi News by Dainik Bhaskar – ranks third.

Interestingly, aggregator services claim all of the top 10 spots in data.ai’s latest ranking of news apps, with the BBC’s news app the first single-brand offering to make the rankings at number 11.

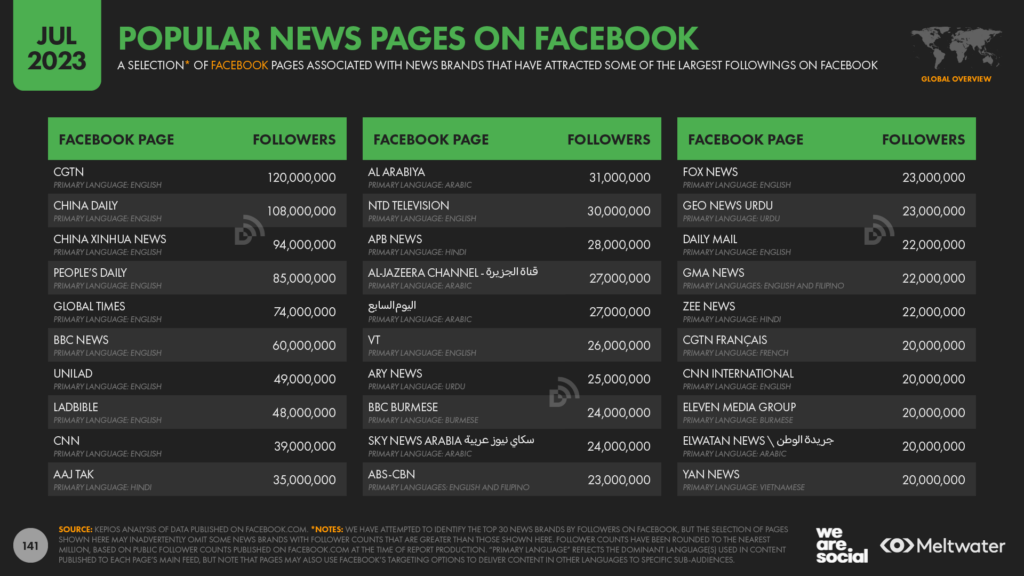

Top news pages on Facebook

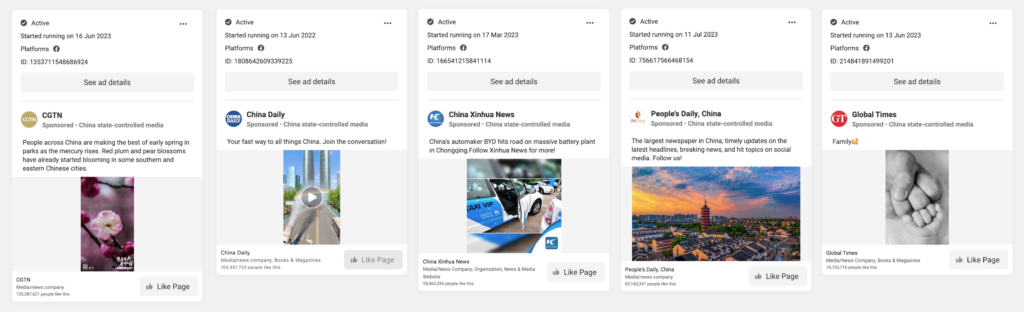

Meanwhile, one of the most startling findings in our digital news data is the size of global audiences amassed by various Chinese state-controlled media on Facebook.

CGTN is the largest news page on the platform, with a staggering 120 million followers.

For context, CGTN is part of China Global Television Network, which Facebook labels as “China state-controlled media”.

And this has particular salience when we consider that the Chinese government has blocked access to Facebook within its home country.

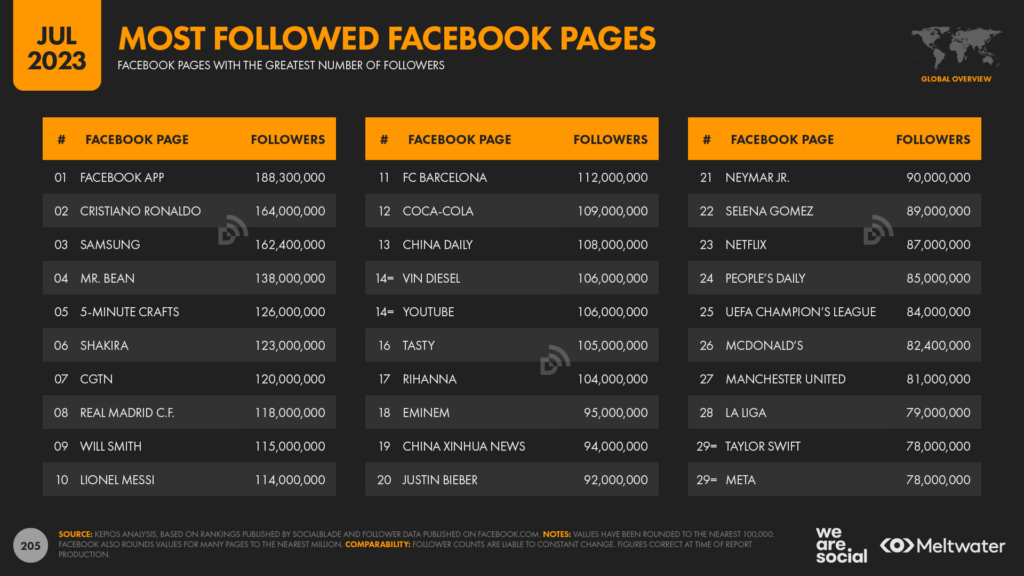

However, CGTN isn’t the only Chinese state-controlled outlet to rank amongst Facebook’s top news pages.Indeed, all of the top five news brands on Facebook have a “China state-controlled media” label: CGTN, China Daily, China Xinhua News, People’s Daily, and Global Times.

Moreover, the first four of these pages have a sufficiently large following that they also qualify for the latest ranking of the top 30 pages on Facebook at a worldwide level, regardless of category.

For comparison, these four pages all have larger followings than the Facebook pages of McDonald’s, Manchester United, and even Taylor Swift.

Meanwhile, Global Times’s Facebook page only just misses the global top 30, with its 74 million followers ranking it 32nd-equal with Jason Statham’s page.

But what’s particularly interesting about these findings is that none of these Chinese news brands enjoys similar success on other social platforms.For example, CGTN only just makes our ranking of the 30 largest news brands on Twitter, where its account has 13 million followers.

Moreover, all five of these top Chinese news brands have invested heavily in Facebook advertising to grow their global reach, and each of them had at least one active Facebook ad campaign running at the time of writing.

Crucially, many of these campaigns are specifically designed to attract Facebook Page Likes:

And when we consider that all five of these outlets have significantly smaller followings on other social platforms, it seems likely that a significant share of their Facebook followers have been recruited through paid Facebook advertising.

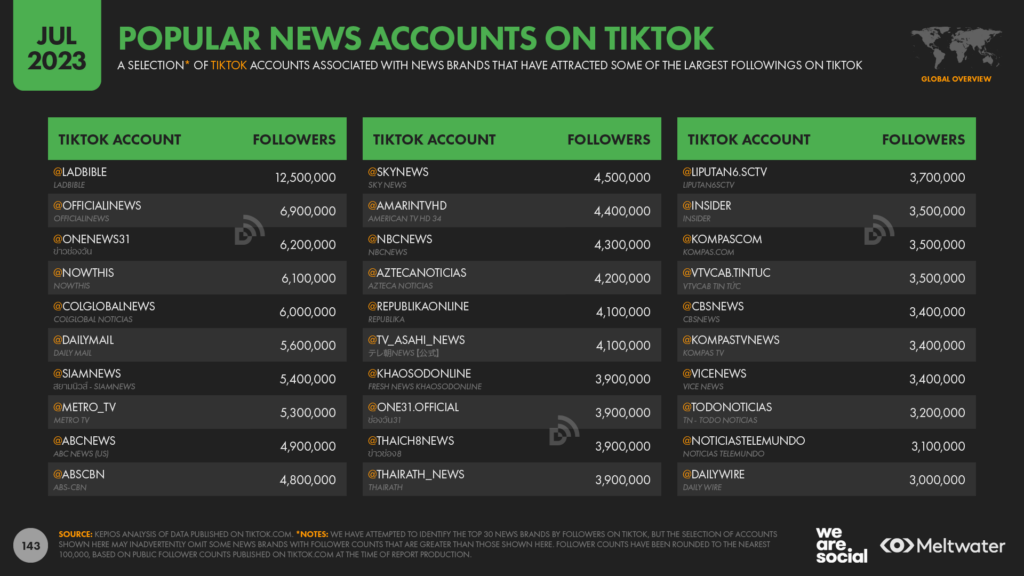

Top news-centric accounts on TikTok

But there are some equally surprising trends when we look at news on TikTok.

It’s worth noting that we’ve adopted a broader definition of “news” for our TikTok analysis (as compared with the rankings of news websites and mobile apps), to better reflect the nature of news content and consumption behaviours on TikTok.

Based on this broader definition, the UK’s LADbible tops our latest ranking of news-centric accounts on TikTok by followers, complementing the eighth place that the brand enjoys in our ranking of news pages on Facebook.

Indonesia’s Officiali News ranks second amongst our top TikTok news brands, while Thailand’s ข่าวช่องวัน (@OneNews31) ranks third.

More broadly, a number of relatively “established” Western news brands feature in our ranking of the 30 largest news brands on TikTok, including the UK’s Daily Mail, America’s ABC, and the UK’s Sky News.

However, a full two-thirds of the top 30 comprises news brands from Asia and Latin America.

Some of these have been long-standing news fixtures in their home countries, such as the Philippines’ ABS-CBN, and Japan’s TV Asahi.

However, some of the top 30 brands are relatively new entrants to the news industry that have capitalised on TikTok’s momentous growth across regions such as South-East Asia.

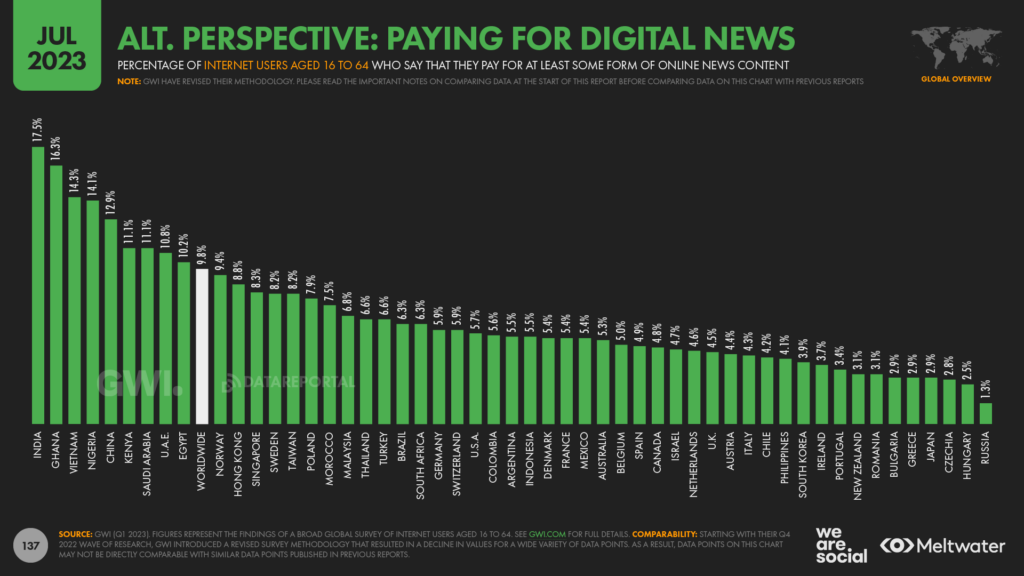

Paying for news

Just before we conclude this year’s deep-dive analysis of digital news trends, let’s take a look at the role of paid content in the digital news landscape.

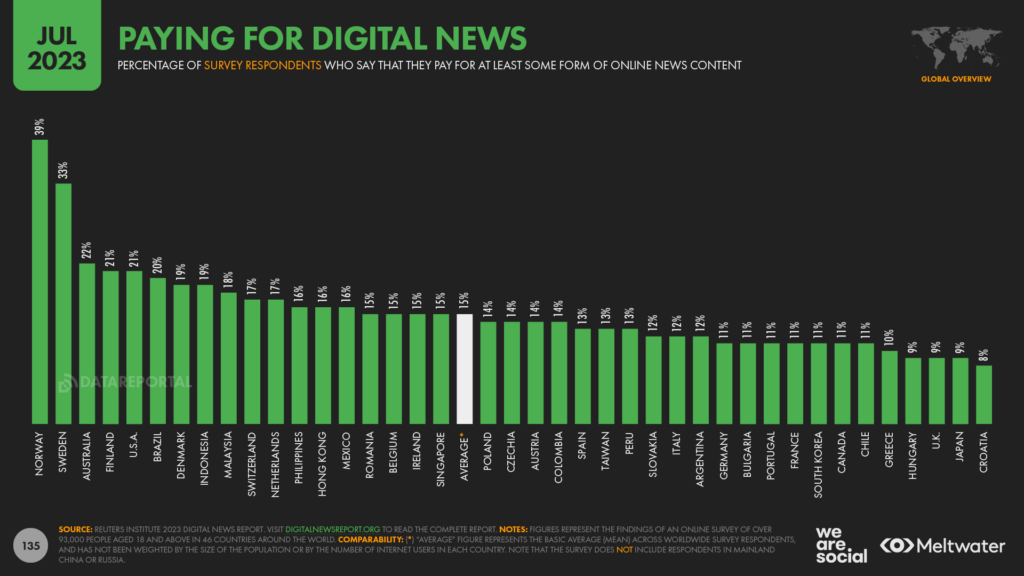

Overall, RISJ’s 2023 study found that just 15 percent of online adults pay for digital news content, although this figure varies from a low of 8 percent in Croatia, to a high of 39 percent in Norway.

Interestingly, however, the number of people who pay for news doesn’t appear to be correlated with GDP per capita.

For example, 1 in 5 respondents in Brazil say that they pay for digital news content, compared with just 1 in 11 respondents in the UK. Similarly, people in Indonesia are more likely to pay for digital news than people in Switzerland.

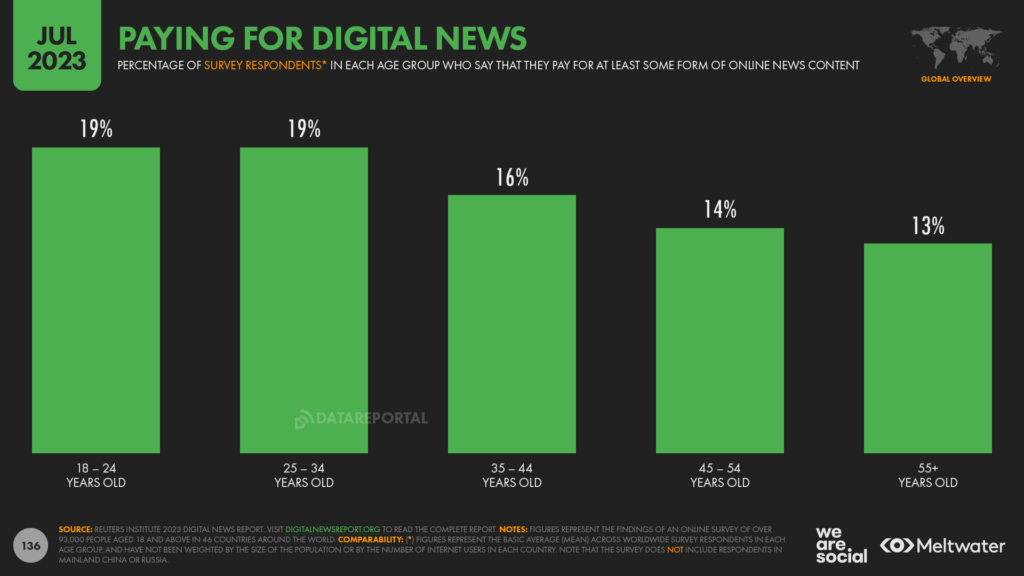

Meanwhile, despite claiming to be significantly less interested in news compared with older generations, people between the ages of 18 and 34 are actually the most likely to say they pay for digital news content.

Just under 1 in 5 people in this cohort say they pay for online news, compared with just 1 in 8 people aged 55 and above.

But GWI’s latest research paints a more pessimistic picture, with the company’s global survey finding that fewer than 1 in 10 working-age internet users paid for an online news service in the past month.

However, GWI’s data reinforces the idea that the willingness to pay for news isn’t necessarily driven by wealth.

Indeed, India tops GWI’s ranking of the countries where people are most likely to pay for news (17.5 percent), followed by Ghana (16.3 percent) and Vietnam (14.3 percent).

At the other end of the spectrum, GWI reports that Russians are the least likely to pay for news (1.3 percent), while fewer than 3 percent of working-age internet users in Hungary, Czechia, Japan, Greece, and Bulgaria say that they paid for any form of online news content in the past month.

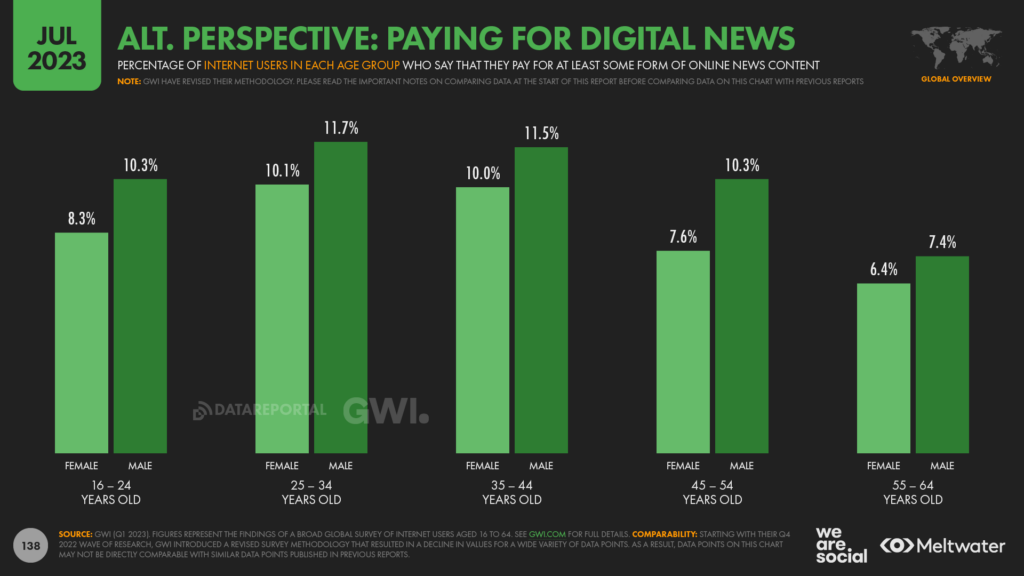

GWI also finds that older people are less likely to pay for online news compared with younger generations.

The company’s latest data reveals that fewer than 1 in 14 internet users aged 55 to 64 paid for digital news content in the past 30 days.

However, this figure only rises to 1 in 9 amongst internet users aged 25 to 24, reinforcing the gloomy outlook for news brands in GWI’s data.

In context: paying for digital news

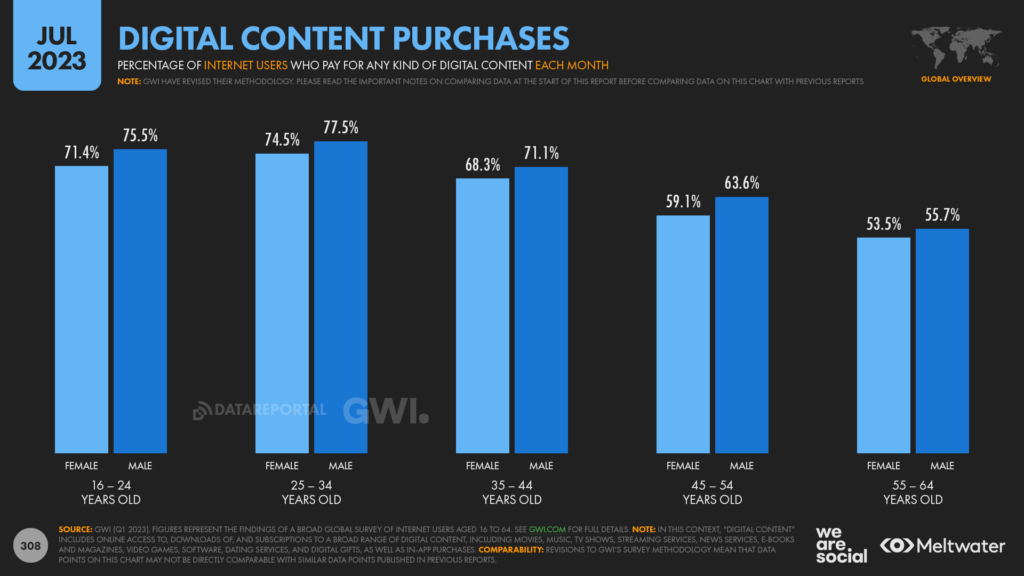

Looking more broadly, GWI’s research reveals that just 54.6 percent of internet users aged 55 to 64 paid for any kind of digital content in the past month, compared with 73.6 percent for users aged 16 to 64.

For comparison, that means Gen Z is 35 percent more likely than Baby Boomers to pay for digital content.

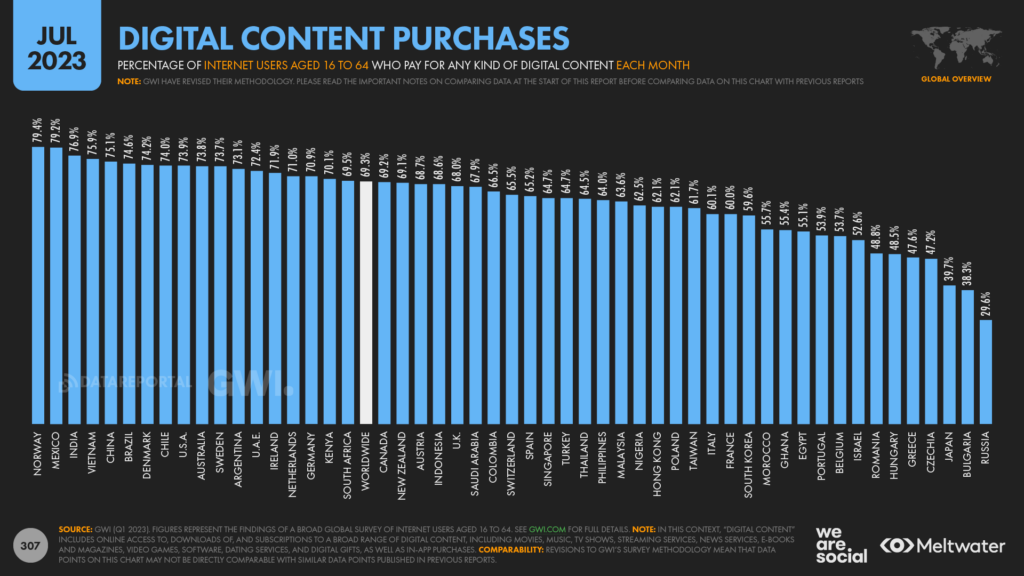

However, willingness to pay for digital content varies considerably depending on the country and the type of content involved.

For example, roughly 7 in 10 working-age internet users paid for at least one form of digital content in the past month, with that figure varying from a high of 79.4 percent in Norway, to a low of 29.6 percent in Russia.

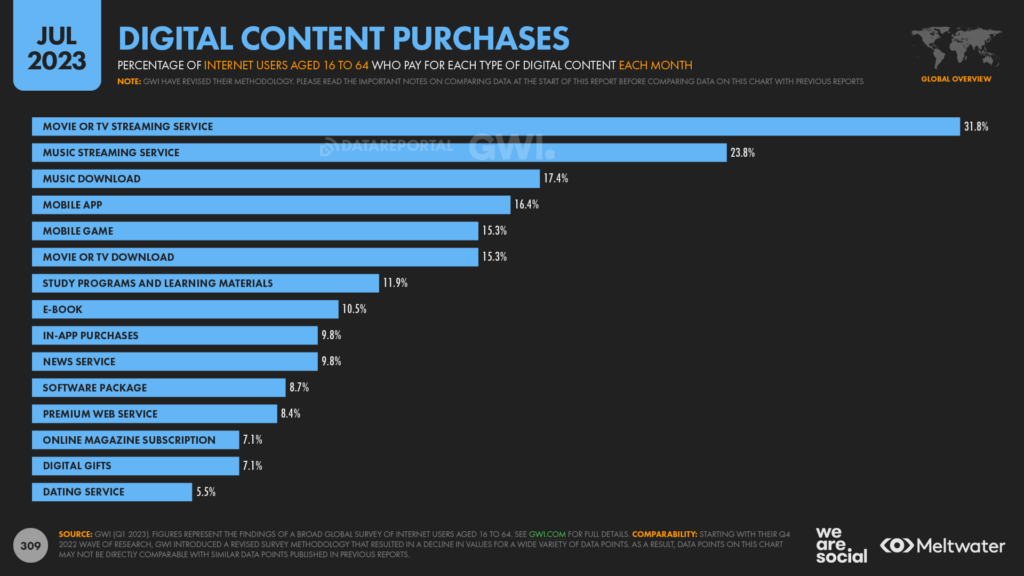

Movie and TV streaming is the most popular form of paid digital content, with almost 1 in 3 internet users between the ages of 16 and 64 saying that they paid for one of these services in the past month.

Music streaming services rank second, with 23.8 percent of the same cohort saying that they paid for a service like Spotify or Pandora in the past 30 days.

But – somewhat surprisingly – paid music downloads rank third, meaning that people are still more likely to pay for a music download than they are to pay for a mobile apps or a mobile game.However, news services fall some way down the ranking, and it’s worth highlighting that people are now three times more likely to pay for a TV streaming service than they are to pay for digital news.

Time spent with digital media increases

Following that deep-dive into digital news, let’s return our attention to broader trends in the world’s digital behaviours.

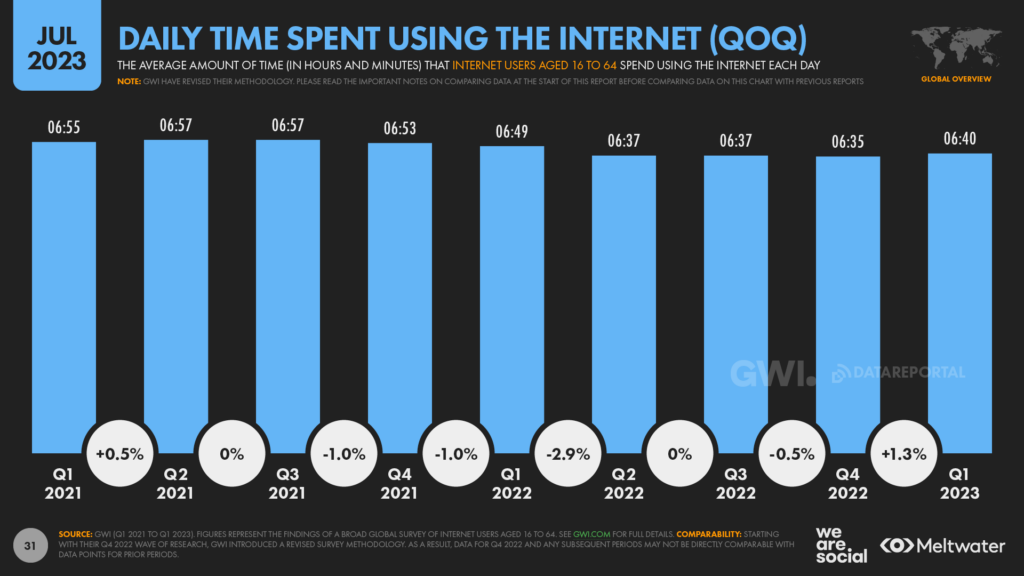

In contrast to the declines that we highlighted in our recentreports, GWI’s latest data shows that working-age internet users actually spent more time using the internet and social media in Q1 2023 than they did in the last three months of 2022.

The time that people spend using the internet overall increased by an average of five minutes per day during the past three months (+1.3 percent), to reach a worldwide average of 6 hours and 40 minutes per day.

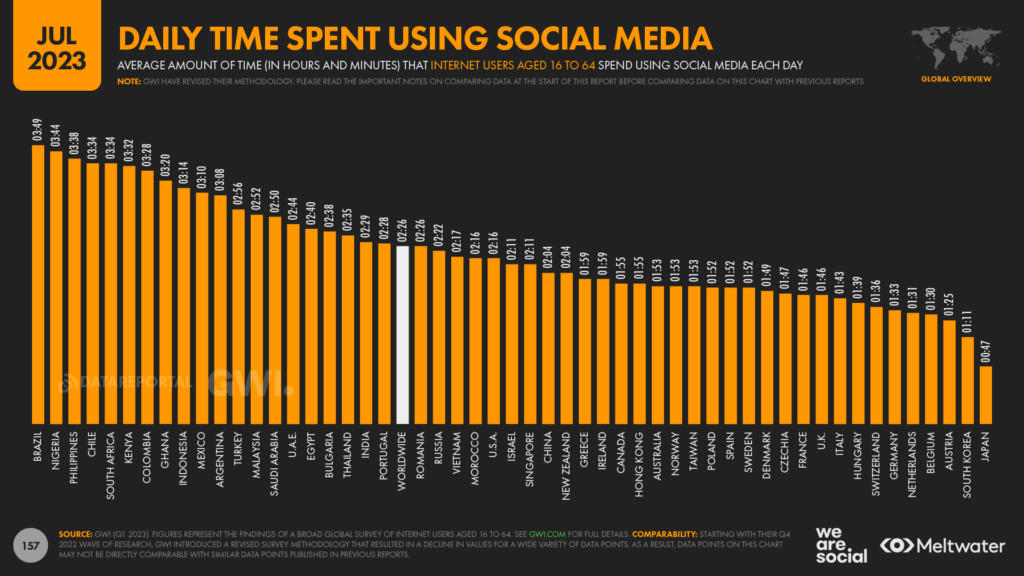

Meanwhile, the amount of time that people spend using social media increased by two minutes per day (+1.4 percent), to reach 2 hours and 26 minutes per day.

Average social media use still varies meaningfully around the world though, from a high of 3 hours and 49 minutes per day, per user in Brazil, to a low of just 47 minutes per day in Japan.

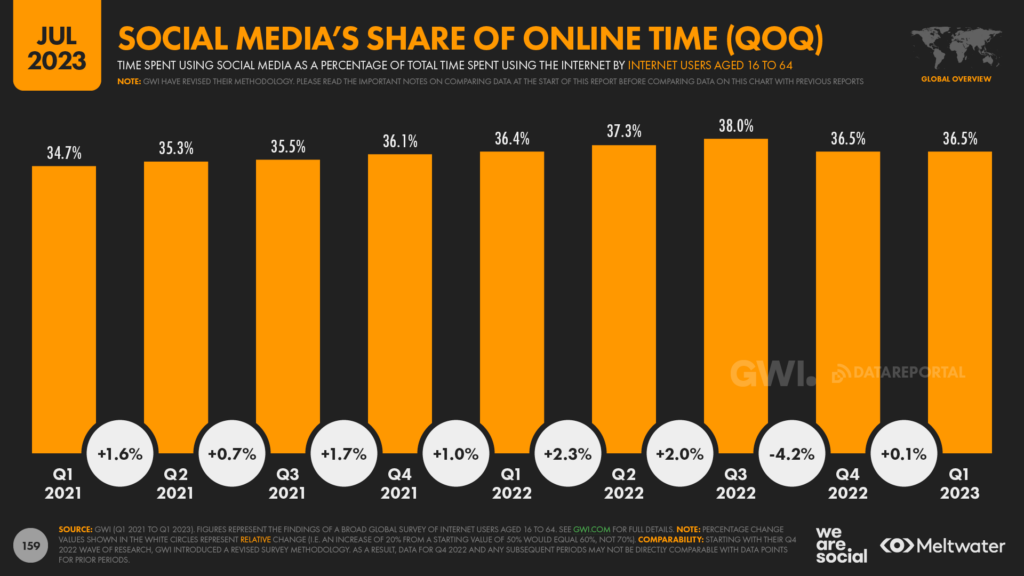

Overall, social media’s share of total internet time crept up a fraction over the past quarter (+0.1 percent), and following a meaningful drop in our April 2023 report, the latest values have returned to roughly the same levels that we saw this time last year.

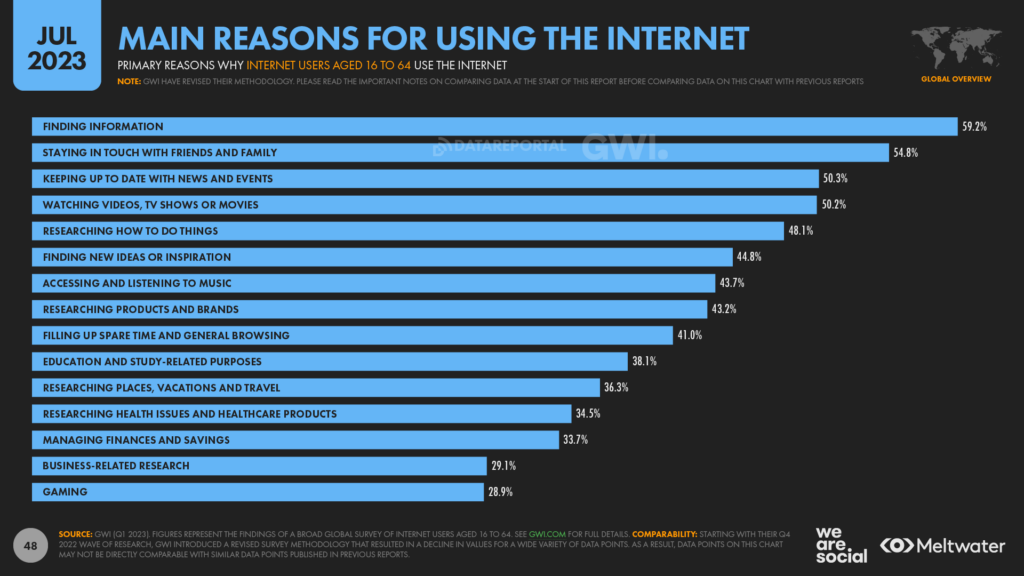

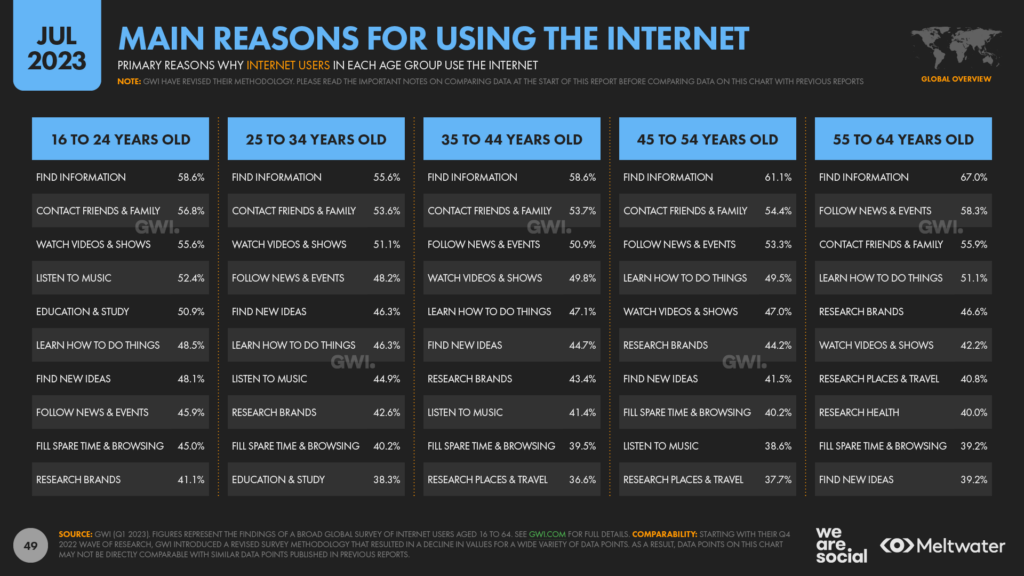

Finding information differs by age

Meanwhile, one of the most intriguing findings in GWI’s latest data is that the prevalence of looking for information on the internet varies meaningfully by age.

“Finding information” remains the primary motivation for going online at a global level, with roughly 6 in 10 people between the ages of 16 and 64 saying that this is one of the main reasons why they use the internet.

And “finding information” remains the primary motivation across all age groups too.

But the interesting takeaway from this data is that the relative importance of finding information varies by age.

GWI’s research shows that people aged 25 to 34 are the least likely to choose this option, with just 55.6 percent of this cohort citing it as a primary motivation.

However, that figure climbs to 67 percent amongst users aged 55 to 64, meaning that this older age group is more than 20 percent more likely to cite “finding information” as a reason for going online, as compared with people aged 25 to 34.

But to put these figures in context, it’s worth highlighting that the average number of options selected in answer to this question in GWI’s survey also varies by age.

At an average of 7.17, people aged 16 to 24 select the greatest number of answers in response to this specific question, compared with an average of 6.79 for people aged 55 to 64.

For comparison, the average across all age groups is 7.03.

Trends in use of OpenAI

The latest data reveals that OpenAI is now one of the 20 most visited sites on the web.

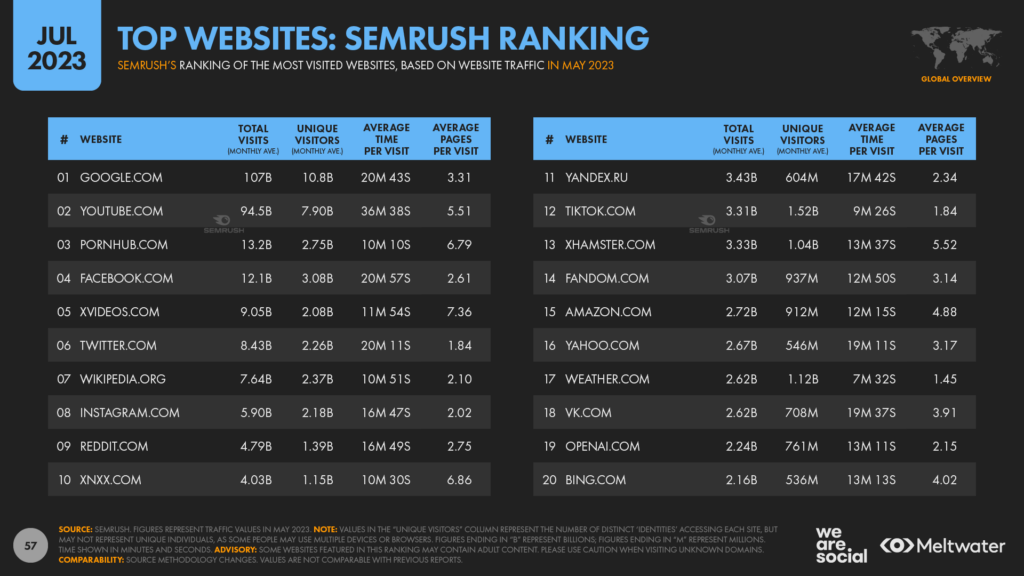

Analysis from Similarweb ranked openai.com 17th in the world based on global traffic in May 2023, while Semrush ranked the site 19th for the same period.

More specifically, Similarweb reports that OpenAI’s website attracted 295 million unique visitors in May, for a total of 1.86 billion visits.

For context, that equates to roughly 6.3 visits per unique visitor.

Similarweb’s data also shows that traffic to openai.com was roughly evenly split between mobiles and computers, although computer traffic appears to be slightly higher than that of mobile.

But it’s also interesting to note that users spent an average of just 4 minutes on the site per visit, which is considerably lower than the average for the top 20 sites overall.

Semrush’s data tells a similar story to that of Similarweb, albeit with different figures.

The company’s analysis points to more than 761 million unique visitors to openai.com in May 2023, for a total of 2.2 billion site visits.

Interestingly however, Semrush reports that visitors spent an average of more than 13 minutes on openai.com, with this figure closer to the average for these top 20 sites compared with the trend in Similarweb’s findings.

It’s important to stress that “unique visitors” are more akin to unique devices than unique human individuals, but even then, these figure highlights just how quickly the world has adopted tools like ChatGPT and Dall•E.

Is AI’s novelty already waning?

However, Similarweb also reports that traffic to openai.com actually declined in recent weeks, compared with recent peaks.

The company’s analysis suggests that the site’s worldwide traffic dropped by 9.7% in June 2023 compared with the previous month, while unique visitors were down 5.7% month-on-month.

On the other hand though, Similarweb also reports that openai.com still attracts roughly 40 percent more traffic than bing.com – not to mention more than 10 times as much traffic as Google’s Bard – so Microsoft’s deal with OpenAI still appears to be delivering value.

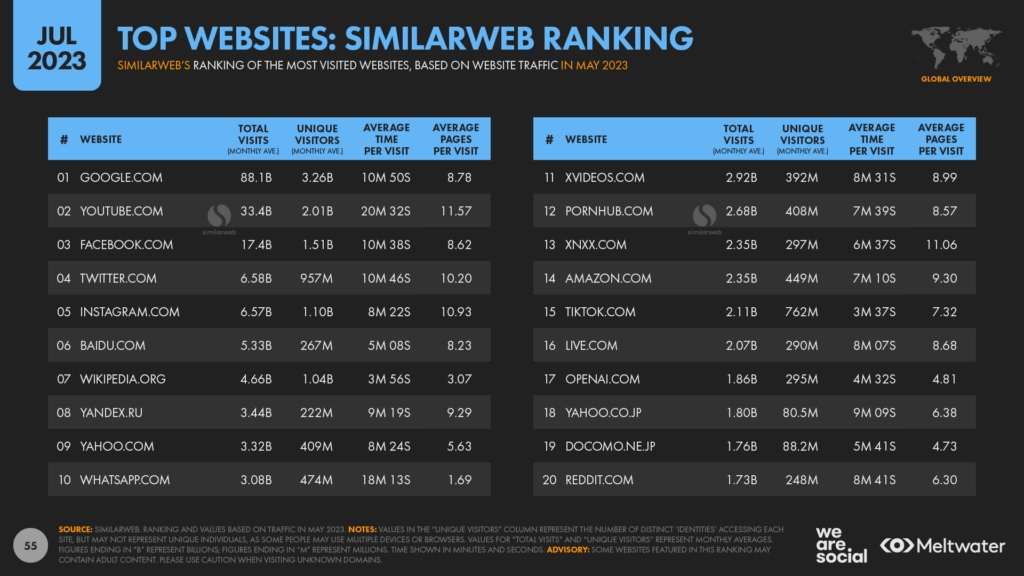

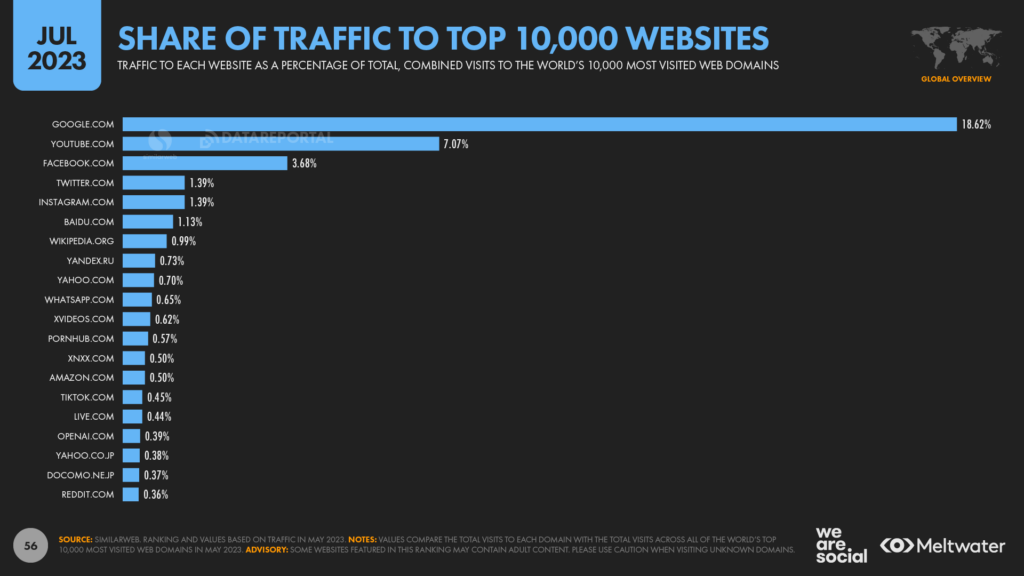

Google still dominates the web

But comparisons with Bing and Bard don’t tell the whole story, because this web traffic data also reveals that OpenAI still has a long way to go before it “wins the internet”.

Indeed, just two domains – Google.com and YouTube.com – still account for more than a quarter of global traffic to the world’s top 10,000 web domains.

For context, these 10,000 websites attract a combined total of close to half a trillion visits each month.

But Similarweb data indicates that the top two Alphabet domains alone attracted more than 120 billion total visits in May 2023.

Meanwhile, only six websites – Google, YouTube, Facebook, Twitter, Instagram, and Baidu – can claim at least one percent share of the global traffic to those top 10,000 sites.

However, between them, these six websites accounted for one-third (33.3 percent) of traffic in May 2023.

And looking more broadly, Similarweb’s data shows that just 71 websites accounted for half of total global traffic to the top 10,000 sites in May 2023.

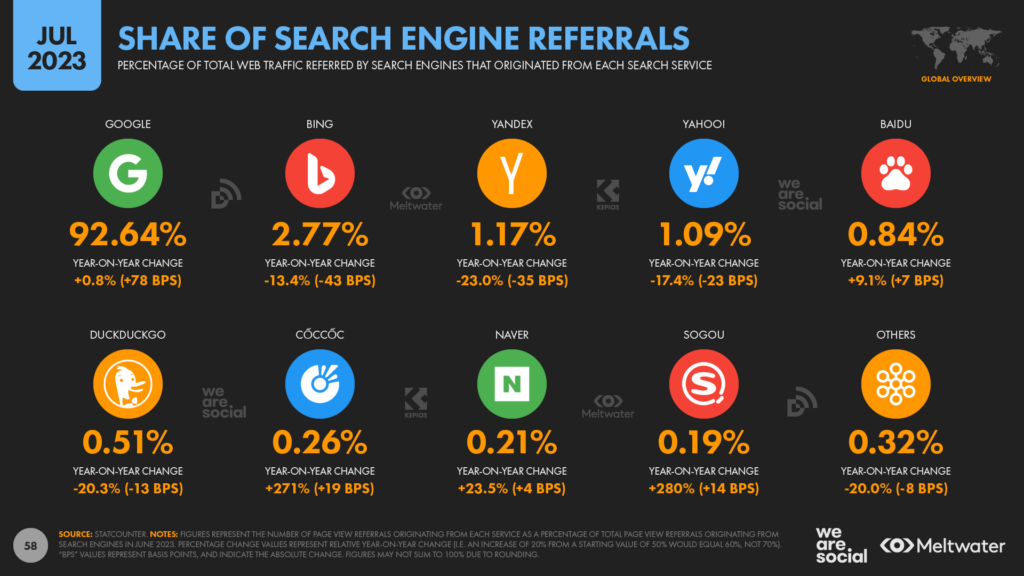

Google still top for search

Furthermore, figures published by Statcounter suggest that Google has actually consolidated its position as the top search engine over the past 12 months.

The company’s data shows that Google is now responsible for 92.6 percent of all web traffic referrals originating from search engines, with the platform’s share increasing by a relative 0.8 percent (+0.78 percentage points) since June 2022.

Conversely, Bing’s share has actually fallen by a relative 13.4 percent (-0.43 percentage points) over the past year, to reach 2.77 percent in June 2023.

However, it’s important to remember that these figures represent the traffic that search engines refer to third-party websites.

And the critical consideration here is that tools like ChatGPT deliver their value without needing to refer users to external web properties.

So, while Google Search may still be a top choice for marketers looking to direct traffic to web properties, it’s important to remember that search engines and large language models (LLMs) such as ChatGPT will likely play quite different roles in satisfying the world’s evolving information needs.

Social media’s role in marketing strengthens

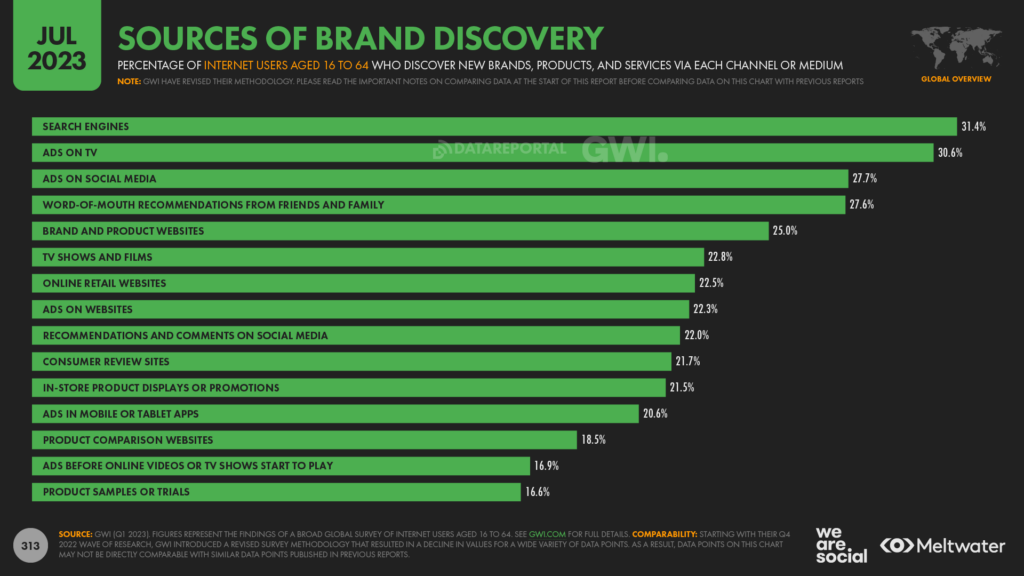

GWI’s latest wave of research reveals that social media has overtaken word-of-mouth recommendations when it comes to introducing people to new brands, products, and services.

Social media ads are now the third most significant source of discovery behind search engines and ads on TV, with 27.7 percent of working-age internet users saying that they discover brands via paid placements on social platforms.

That figure is only marginally up from the 27.6 percent that GWI reported this time last year, but the overall role of word-of-mouth recommendations has slipped over the past twelve months, from 28.6 percent in Q1 2022, to 27.6 percent today.

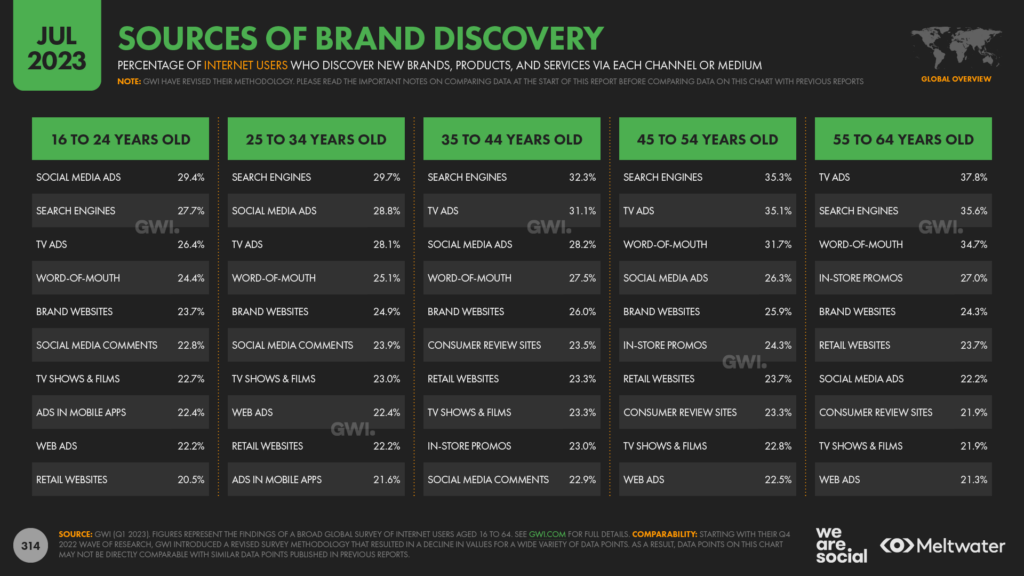

Social media ads are particularly important when it comes to marketing to younger people, with GWI reporting that this channel is the top source of new brand discovery for internet users aged 16 to 24.

Word of mouth remains more important amongst older age groups though, especially in comparison with social media ads.

Amongst internet users aged 55 to 64, TV ads are still the primary source of brand discovery, ahead of search engines.

Word-of-mouth recommendations then rank third for this age group at 34.7 percent, whereas social media ads only rank seventh, at 22.2 percent.

Social research

But data shows that social media plays a valuable role at subsequent stages of the “buyer journey” too.

GWI’s research reveals that social networks are the second most popular online destination for people looking for information about brands, products, and services, behind search engines.

However, social networks are the top choice amongst internet users aged 16 to 34, with close to half of all consumers in this age group saying that they turn to social channels when researching brands.

And despite pervasive media headlines to the contrary, there’s little evidence to suggest that people are deserting brands on social media channels either.

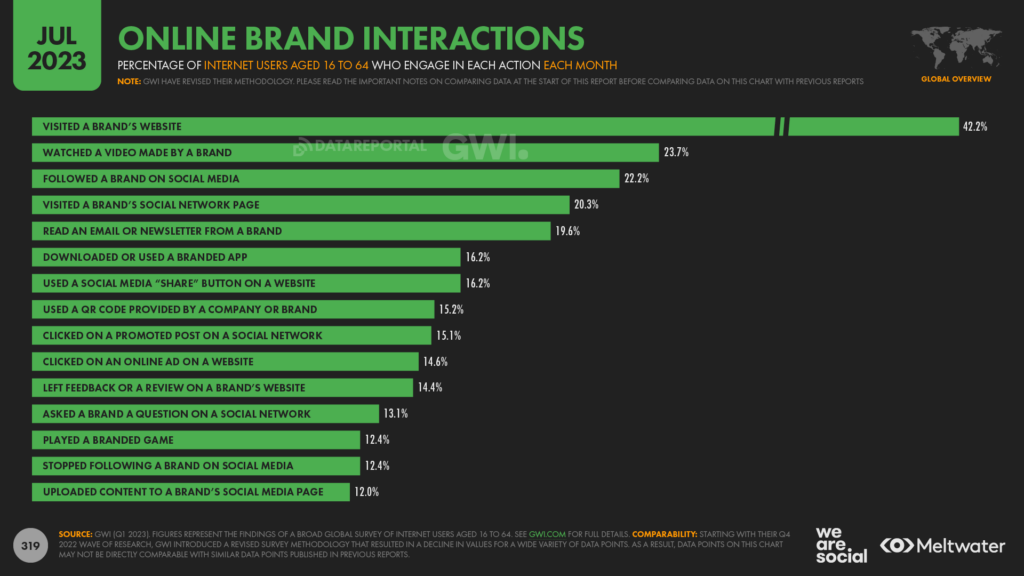

For example, when we look at online brand interactions over the past month, GWI’s data reveals that more than 1 in 5 working-age internet users started following at least one new brand on social media in just the past 30 days.

Meanwhile, just 12.4 percent of respondents say that they stopped following a brand on social media in the past month

In other words, reputable research indicates that people are now following more brands on social media than ever before.

Meta reaches half a billion in India

Sticking with social media marketing, the latest figures published in Meta’s advertising resources reveal that ads across the company’s various platforms now reach more than half a billion users in India alone.

The company’s global, “deduplicated” advertising audience across Facebook, Instagram, and Messenger now stands at 3.01 billion, with India accounting for 526 million of this total.

For comparison, data published in the company’s own ad planning tools indicates that ads across Meta properties now reach 266 million users in the United States, 189 million in Indonesia, and 166 million in Brazil.

This means that India is clearly Meta’s top global market in terms of absolute reach, although it’s worth stressing that significant differences in average revenue per user (ARPU) mean that the US remains Meta’s most valuable country.

India tops the user rankings across all of Meta’s platforms though, with the country home to at least half a billion WhatsApp users, 367 million Facebook users, 332 million Instagram users, and 130 million Messenger users.

Indian women more likely to use Instagram

It’s interesting to note that Instagram’s Indian user base has been steadily closing the gap versus Facebook, especially since the country’s government blocked access to TikTok in June 2020.

And in fact, Meta’s latest data reveals that women in India are actually now more likely to use Instagram than they are to use Facebook.

Figures published in the company’s own ad planning tools reveal that ads on Instagram now reach 96 million women in India, compared with the 86.3 million Indian women that marketers can reach with ads on Facebook.

But these figures serve as yet another reminder of the poor gender balance in India’s online audiences, with women accounting for just one-third of India’s Instagram audience, and less than a quarter of Facebook’s Indian user base.

Threads: the next big thing?

But what about Meta’s newest addition, Threads?

Well, the company itself announced that it took just five days for Threads to attract 100 million sign-ups, which many media outlets have highlighted was even faster than the two months it took ChatGPT to reach this milestone.

Meanwhile, data.ai has revealed that Threads reached 150 million worldwide app downloads just a week after its launch, and the service also attracted 100 million active users during those first seven days.

India appears to have delivered the largest share of app downloads to date, accounting for 1 in 3 downloads around the world.

India’s dominance is perhaps unsurprising though, given that the country is by far Instagram’s largest market [note: Threads users sign up via an existing Instagram account].

Brazil ranks second in terms of Threads downloads, delivering 22 percent of the worldwide total, while the United States ranks third, with 16 percent.

But it’s particularly interesting to note that Japan ranks fifth, especially given how important Japan is to Twitter’s global numbers.

Data.ai’s numbers suggest that Threads may already have between 7 and 8 million users in Japan, although this figure is still considerably below the 68 million active accounts shown in Twitter’s latest ad reach data.

Remember that Threads still isn’t available in the EU though – the “bundling” of Threads with Instagram has fallen foul of the bloc’s privacy regulations – so we may see quite different geographic splits if the app does become available across Europe in the near future.

Data.ai also reports that Threads was the fastest mobile app launch of all time, with the new platform’s momentum more than 5 times faster than that of the previous record holder, Pokémon Go.

However, it’s worth highlighting that Threads’ launch was doubtless accelerated by its close ties with Instagram, with those ties making it exceptionally easy for users to “sign up” and start using Meta’s new service.

But why did Meta choose to align Threads with Instagram instead of Facebook, when the latter boasts 1½ times as many monthly active users?

Well, data from GWI may offer some useful insights here.

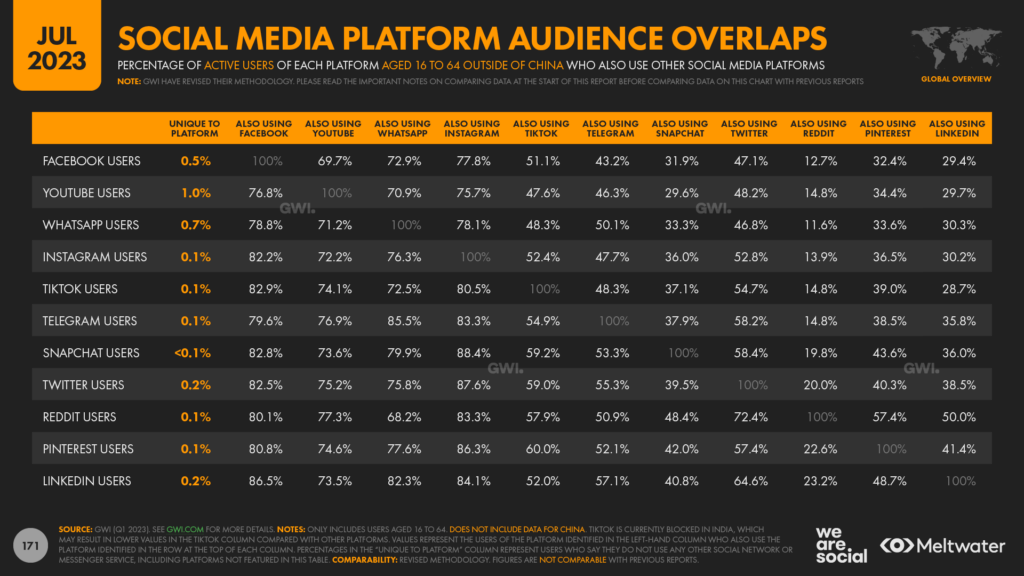

If we explore audience overlaps, we see that Twitter users appear to have the greatest affinity for Instagram compared with all other social platforms.

GWI’s data shows that 87.6 percent of active Twitter users also use Instagram each month, compared with 82.5 percent for Facebook, 75.2 percent for YouTube, and 59 percent for TikTok.

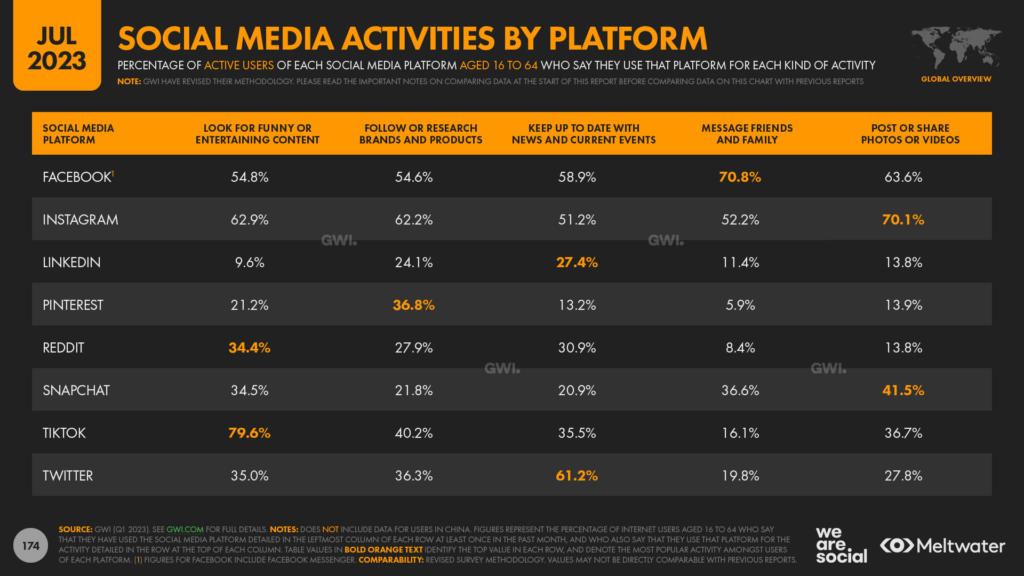

However, GWI’s data also reveals that Instagram users are more likely to use Instagram to look for funny and entertaining content than they are to use it to keep up to date with news and current events, so it will be interesting to see how motivations for using the new Threads service evolve.

For context, staying up to date with news and current affairs is the top motivation for Twitter use today, with more than 6 in 10 active users citing this a top use case.

But on the other hand, it’s also worth noting that Instagram has the highest score when it comes to people using the platform to engage with brands and marketing content, and this may bode well for the commercial outlook of the Threads service.

However, my sense is that Zuck and team may have conceived Threads to be far more than just another advertising channel.

Given the role that content published to platforms like Twitter and Reddit has played in informing Large Language Models (LLMs) like ChatGPT, there’s a good chance that Threads has also been designed to inform and fuel Meta’s own AI tool, LLaMa.

Moreover, Twitter has recently imposed rate limits on how much content its users can access, while Reddit has dramatically increased the cost to access its API.

These actions will likely have a major impact on data collection for LLM tools, which may result in commercial opportunities for Meta to licence Threads content to third-party AI tools.

But there’s another question that plenty of people have been asking in recent days: how has Threads impacted Twitter?

#WhatsHappening with Twitter?

Well, following the concerns that we raised in last quarter’s deep-dive into the state of Twitter use and engagement, we’ve actually seen some more encouraging trends in the latest Twitter data.

For starters, research from GWI suggests that Twitter’s core fans remain loyal to the platform, despite its significant changes over the past year.

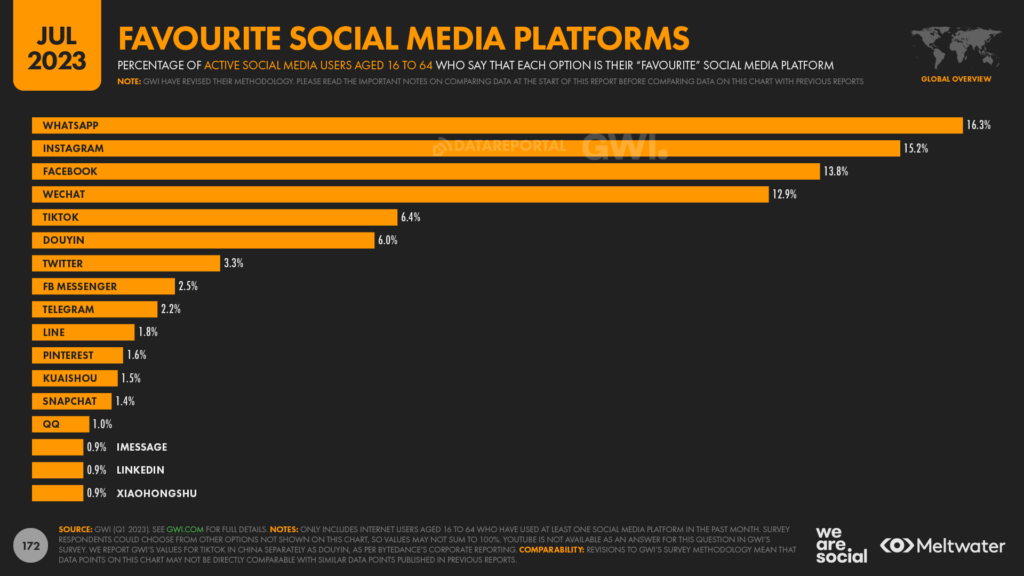

3.3 percent of the world’s social media users still state that Twitter is their “favourite” social media platform, with that figure remaining unchanged since this time last year.

Admittedly, 3.3 percent is only a small share of the world’s social media users, but that’s enough to rank Twitter seventh in GWI’s latest survey, and fifth amongst platforms outside of mainland China.

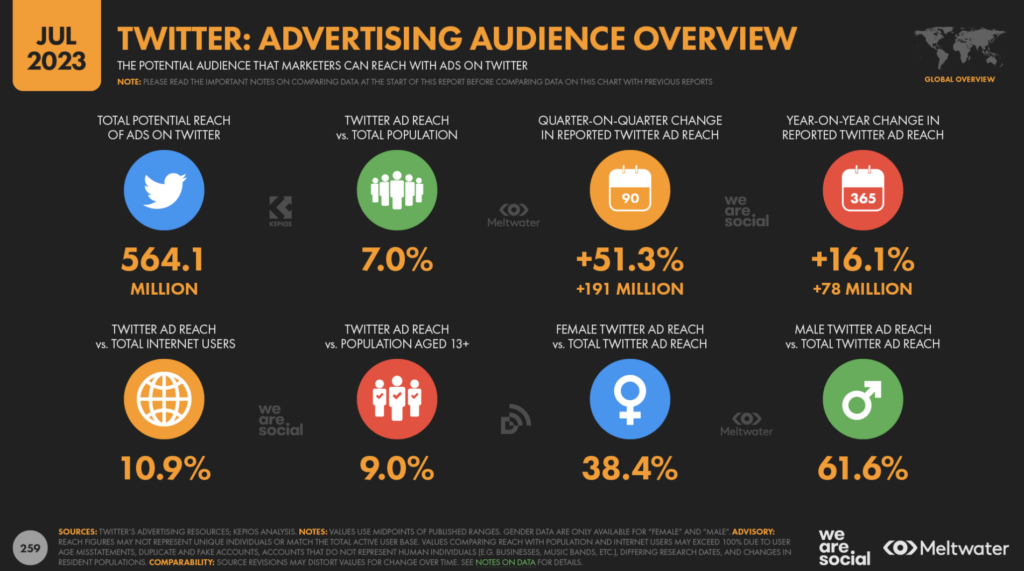

Wild fluctuations in Twitter’s Audience data

But in a trend that we reported in significant detail in our Digital 2023 April Global Statshot Report, the audience reach figures published in Twitter’s own ad tools continue to fluctuate wildly.

Indeed, global reach totals have shown differences of well over 100 percent in just the past few days, while figures for individual countries have shown differences of up to 300 percent.

Given these wild differences, it’s tricky to know how reliable Twitter’s published audience figures are, or which “set” of figures most accurately reflects its current audience.

However, Twitter itself has reportedly been telling advertisers that it has around 535 million “monetisable” monthly active users, so we’ve used the dataset published in Twitter’s tools that most closely matches that figure as the basis for the Twitter figures we’ve reported this quarter.

And in fact, these figures are the highest we’ve ever seen for Twitter’s global ad reach, which should offer some mild relief for Elon and team.

We’d still advise significant caution when analysing this data though, especially given the ongoing fluctuations in the company’s own numbers.

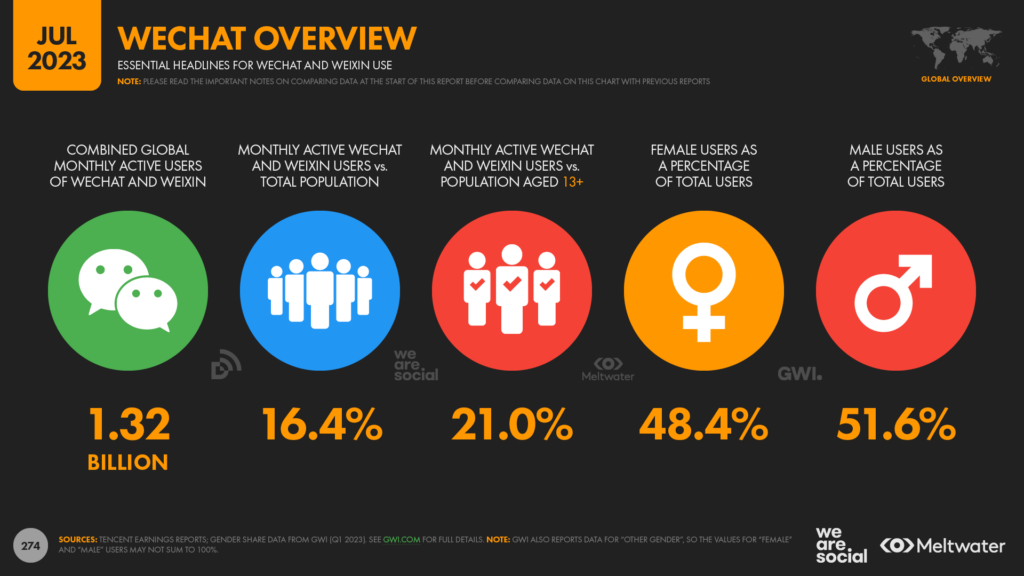

WeChat gains momentum

Despite already being well established, WeChat continues to consolidate its position as the top social media platform amongst social media users in mainland China.

Tencent reports that the combined audience of WeChat and 微信 (Weixin) has now reached 1.32 billion monthly active users, which equates to more than 1 in 5 of the “eligible” global population (i.e. people aged 13 and above).

The latest figures show that WeChat’s combined active user base has grown by 2.4 percent over the past year, with 31 million new users joining the service in the twelve months ending 31 March 2023.

Furthermore, at a worldwide level, the number of social media users who state that WeChat is their “favourite” platform has increased from 11.8 percent this time last year, to 12.9 percent today.

For comparison, that 1.1 percentage point growth equates to a relative increase of 9.3 percent in just the past year.

But – given the geographic specificity of WeChat’s popularity – it’s probably more representative to focus on the figures for China.

And the data here tells a powerful story, with a hefty 47.3 percent of social media users in China saying that WeChat is their favourite platform.

This is all the more impressive when we consider that the popularity of Douyin – the mainland Chinese equivalent of TikTok – has also grown rapidly over recent months.

This time last year, 19.2 percent of Chinese social media users selected Douyin as their favourite platform, but that figure has grown by a relative 16.6 percent over the past year, reaching 22.4 percent in GWI’s latest wave of research.

But Chinese users are still twice as likely to identify WeChat over Douyin as their favourite social platform.

And moreover, despite the vast majority of the app’s users residing in just one country, WeChat is now so popular amongst Chinese women aged 35 to 44 that it tops the global ranking for this demographic.

However, WeChat is still almost entirely dependent on China for its success.

GWI reports that the country accounts for more than 86 percent of WeChat’s total global user base, while users in China account for more than 99 percent of those who say that WeChat is their “favourite” social platform.

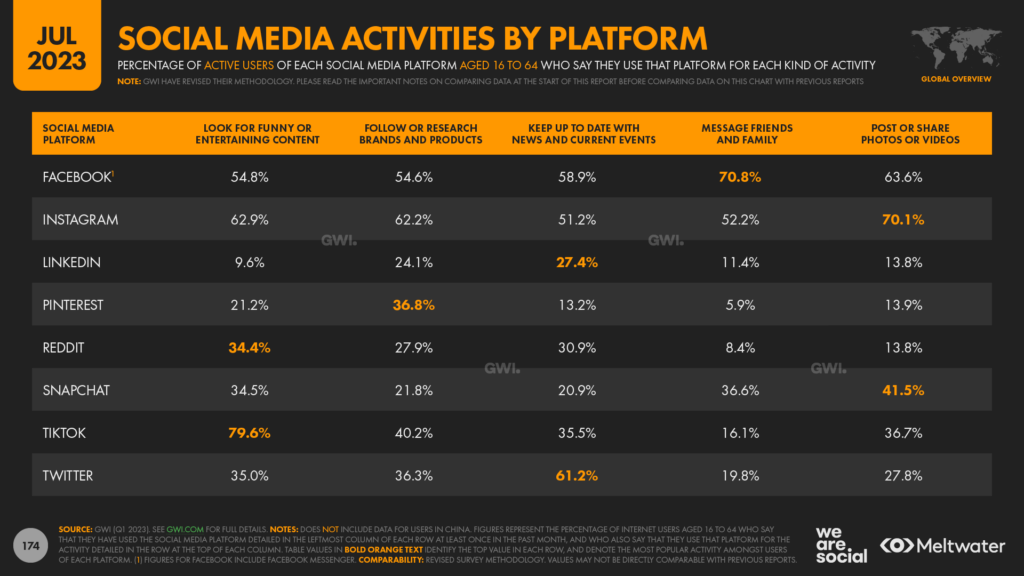

Instagram is a key opportunity for brands

Comparing activity across the top social platforms, Instagram users are the most likely to use the platform to engage with brands.

GWI reports that 62.2 percent of Instagram users say that they visit the platform to research purchases or see content from brands, compared with 54.6 percent of Facebook users, and just over 40 percent of TikTok users.

However, marketers may want to note that just 1 in 3 active users (36.3 percent) uses Twitter to seek out brand content, while this figure drops to a scant 21.8 percent for Snapchat.

These lower figures don’t mean that marketing and advertising content don’t work on Twitter or Snapchat though; they simply reveal that brand content isn’t a primary draw for users of these platforms, especially when compared with platforms like Instagram.

So, my advice here would be to treat each platform differently, and carefully consider people’s motivations for using each service when selecting your platform mix, and when crafting marketing content and campaigns.

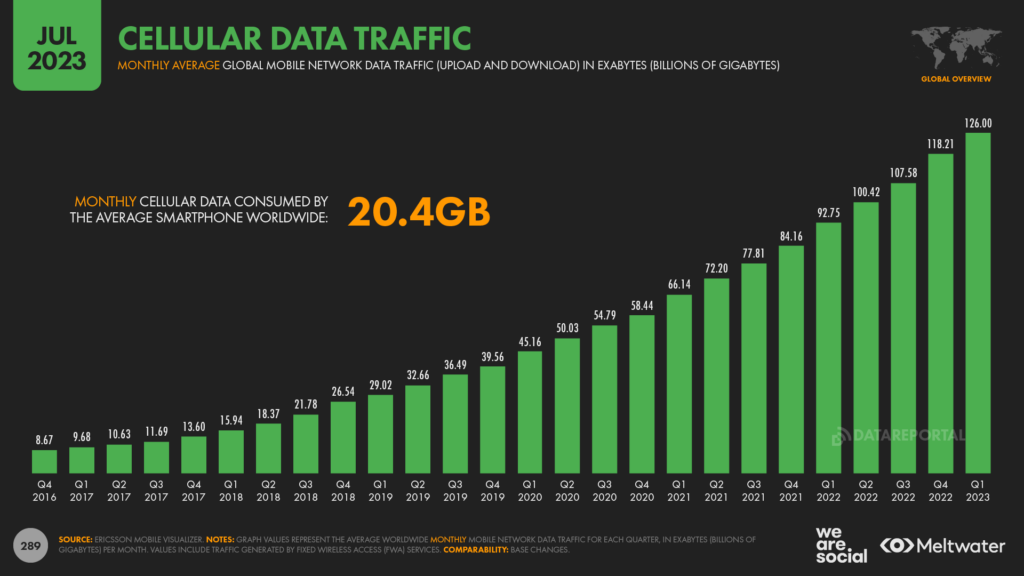

Cellular data consumption soars

New data from Ericsson reveals that the typical smartphone user now consumes more than 20GB of cellular data each month.

Users’ average monthly data consumption has increased by 28 percent over the past year, from 15.9GB per month this time last year, to 20.4GB per month today.

Meanwhile, Ericsson reports that total global cellular data traffic averaged 126 billion gigabytes per month across the first quarter of 2023, representing an increase of 36 percent versus the same period in 2022.

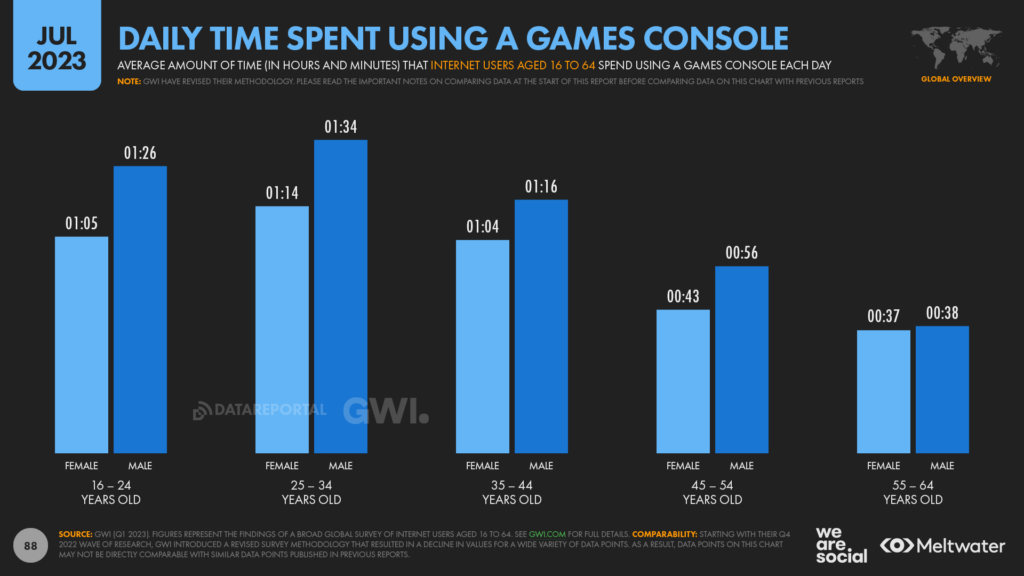

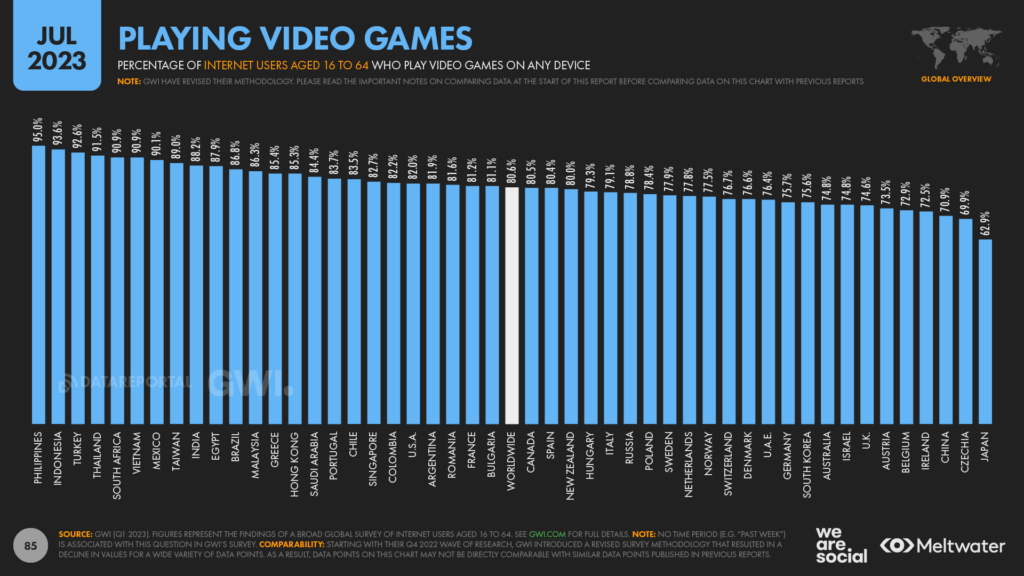

Beware of gaming stereotypes

Marketers may be surprised to learn that internet users aged 55 to 64 spend an average of 38 minutes per day using a games console.

For comparison, this is 1 minute more than the average time this age group spends consuming physical print media such as newspapers and magazines.

And what’s more, the time that this age group spends using games consoles is roughly the same for both men and women.

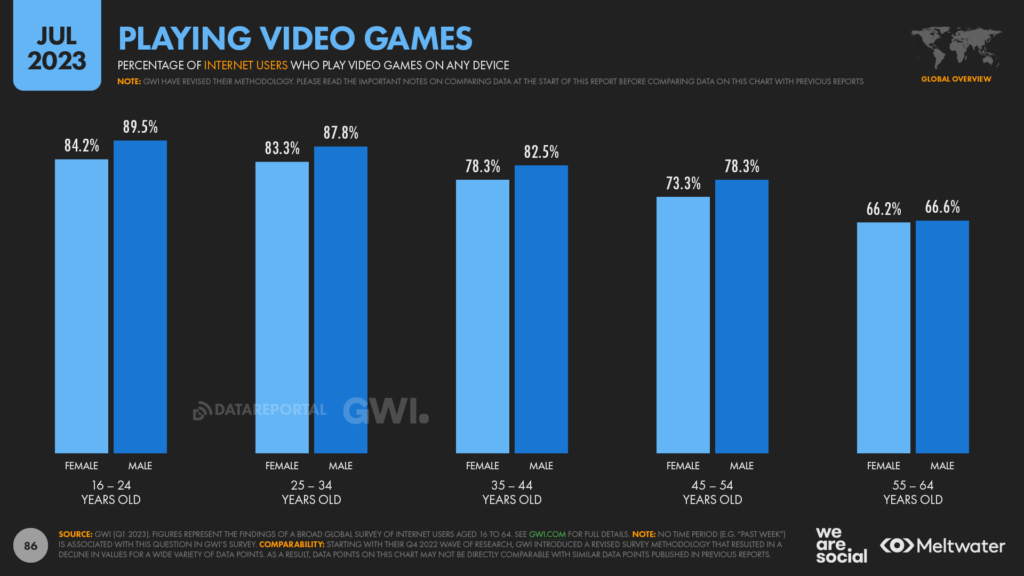

More broadly, roughly two-thirds of internet users aged 55 to 64 play video games on any device.

As is true across all age groups, smartphones are the most popular gaming device for older generations, with roughly half of all internet users aged 55 to 64 saying that they play games on these handsets.

Meanwhile, roughly 3 in 10 say that they play video games on a laptop or desktop computer, while almost 14 percent play games on a tablet.

However, 1 in 8 internet users in this age group (12.5 percent) also say that they use a games console, with almost all of these gamers owning their own console device (as opposed to borrowing their children’s Playstations and Xboxes).

When it comes to gaming activity by country, GWI’s data shows that video games are universally popular, but they’re a particularly big draw across South-East Asia.

Perhaps surprisingly, Japanese people are the least likely to say that they play video games, but well over 6 in 10 internet users in the country still qualify as gamers.

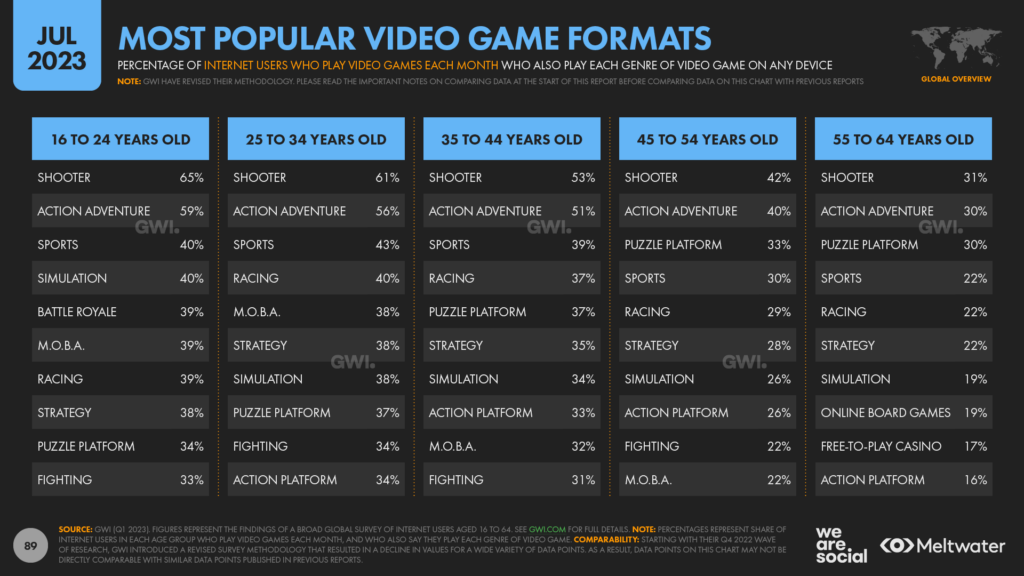

Overall, GWI’s latest data reveals that shooter formats (e.g. Halo and Call of Duty) top the genre preferences of older age groups, just as they do across all age groups.

However, puzzle platforms (e.g. Limbo and Journey) and online board games (e.g. Hearthstone and Gwent) are disproportionately popular amongst older age groups.

It’s also important to note genre preferences vary meaningfully between genders, and puzzle platform titles are the most popular genre for women aged 55 to 64.

So, while video games are popular across all generations, this data suggests that marketers may want to adopt different gaming strategies for different demographics.

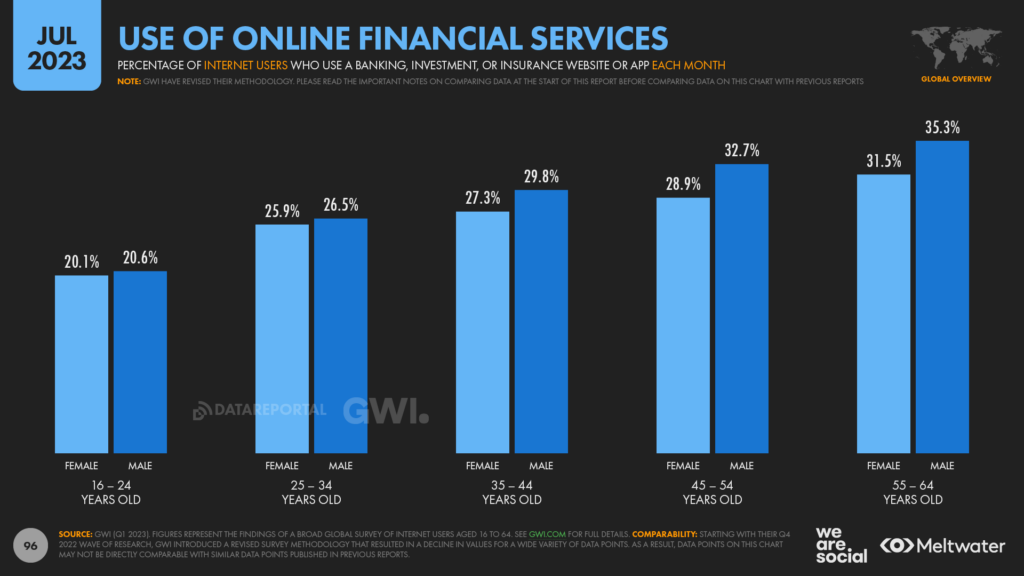

Young people slow to adopt internet banking

More great data from GWI shows that young people are significantly less likely to use online financial services compared with their parents’ generation.

Barely 1 in 5 women aged 16 to 24 used an online banking, investment, or insurance website or app in the past month, versus 31.5 percent for women aged 55 to 64.

Similarly, just 20.6 percent of men in that younger age bracket used one of these online financial services, compared with 35.3 percent of men in the older age group.

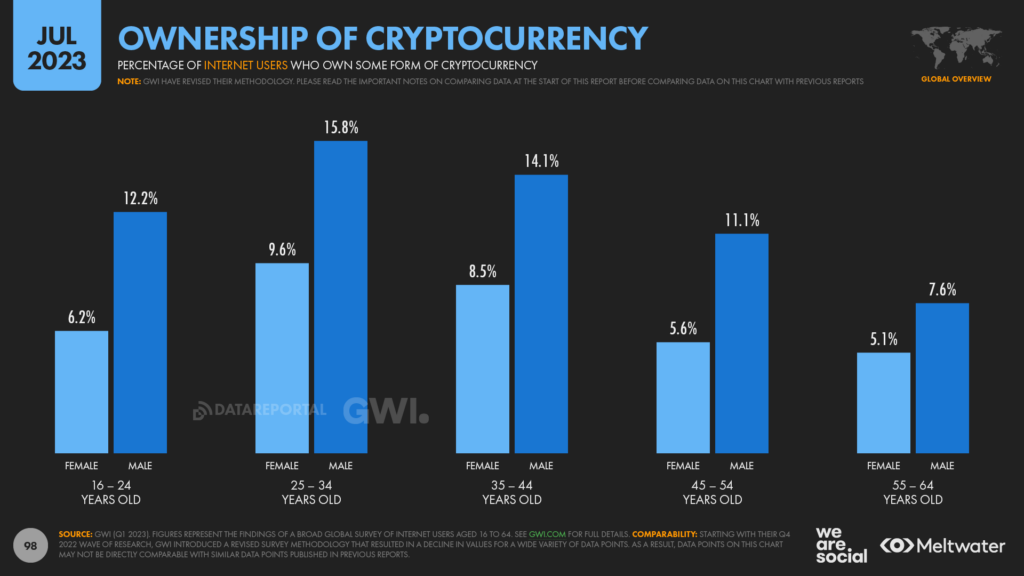

However, it’s interesting to note that 12.2 percent of male internet users aged 16 to 24 say they own at least some form of cryptocurrency.

And while the figure for crypto adoption is still quite a bit lower than the figure for use of more “conventional” online financial services, the two numbers are much closer than one might expect.

For comparison, men in this younger cohort are roughly 60 percent as likely to hold crypto investments as they are to use online banking, whereas that figure falls to just 22 percent amongst men aged 55 to 64.

These figures may in part be due to differences in earning power, but they may also suggest that younger people feel “underserved” by current approaches to internet banking.

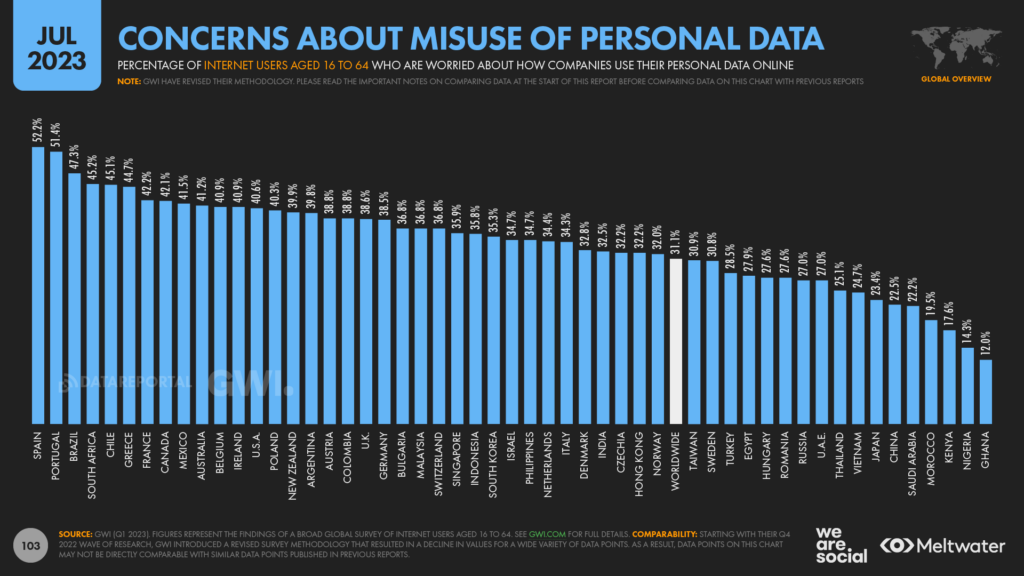

Concerns about misuse of data

Concerns about companies’ potential misuse” of personal data appear to be waning, according to the latest wave of research from GWI.

Two years ago, 33.6 percent of respondents said they were worried about how companies might use their personal data online, but that figure has fallen to just 31.1 percent today.A 2.5 percentage-point drop might not sound like much, but that change represents a 7.5 percent relative decline in concern in the space of just two years.

However, it’s unclear whether this change is due to an increased sense of wellbeing, or simply greater apathy towards the topic of online safety and security, especially now that people are spending less time online compared with the height of pandemic-era lockdowns.

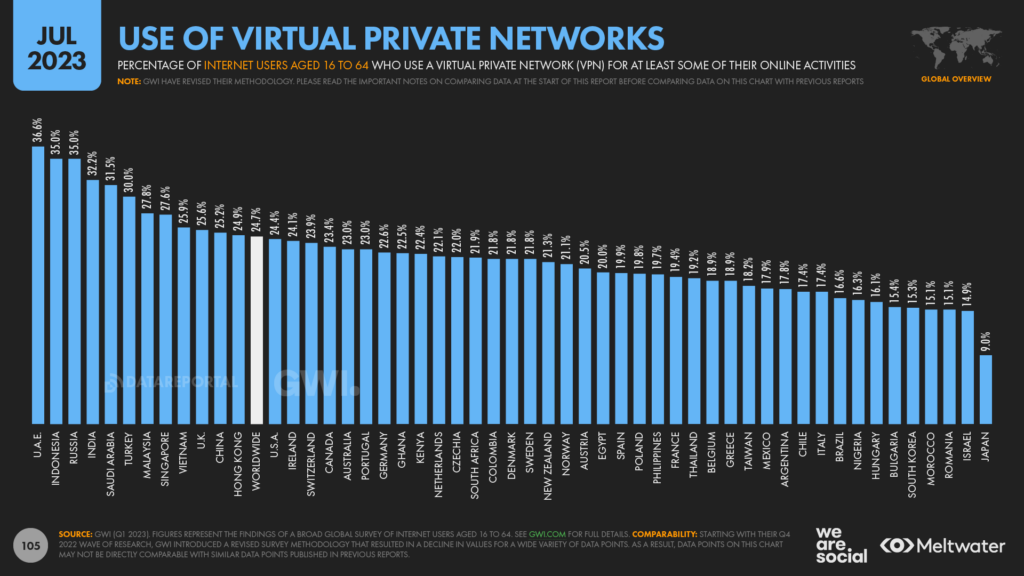

However, it’s interesting to note that the use of both ad blockers and VPNs has declined during the same period, suggesting that people are either less worried about online privacy today than they were two years ago, or that rising costs of living have forced some people to abandon their use of these tools.

Wrapping up

Still here? Thanks for sticking with me through all 10,000+ words of this quarter’s analysis!

That’s all for this quarter’s report, but I’ll be back with our final Statshot report of 2023 in late October, when we’ll also take a look ahead at the trends we believe will define success in 2024 and beyond.Before that though, if you’d like to stay in touch with my regular updates and analysis, feel free to connect with me on LinkedIn, Twitter, and Threads, where you’ll find me as @eskimon.

Reports

Reports